Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

NCR (NYSE:VYX) Atleos Corp (NYSE:NATL) reported its first quarter 2025 results on Thursday, May 8, 2025, showcasing strong services growth and margin expansion despite a modest decline in overall revenue. The company’s strategic shift toward recurring revenue streams continues to yield positive results, with services growth offsetting hardware timing issues and foreign exchange headwinds.

Quarterly Performance Highlights

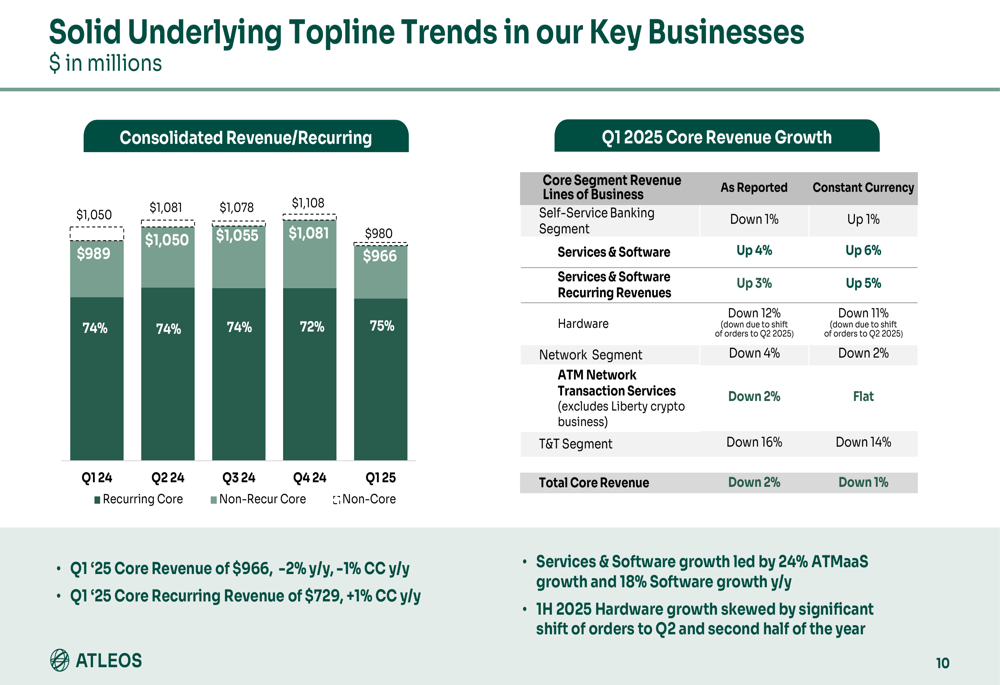

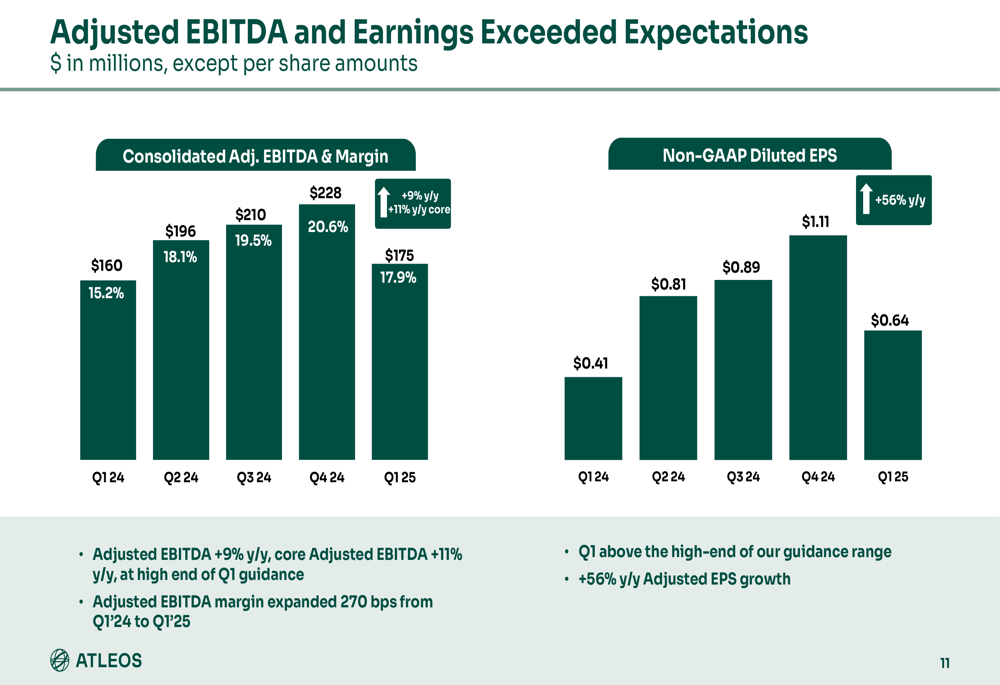

NCR Atleos reported Q1 2025 core revenue of $966 million, representing a 2% year-over-year decline (1% decline in constant currency). However, the company’s recurring revenue mix reached a new high of 76%, demonstrating continued progress in its business transformation. Adjusted EBITDA grew 9% year-over-year to $175 million, with margins expanding 270 basis points to 17.9%.

As shown in the following chart of consolidated revenue and recurring revenue trends:

The company’s adjusted earnings per share grew significantly, increasing 56% year-over-year to $0.64, exceeding analyst expectations. This strong bottom-line performance was driven by improved margins across segments and effective cost management initiatives.

As illustrated in the following chart of adjusted EBITDA and earnings performance:

"We had a very successful first quarter, with results at or above our expectations," said Tim Oliver, President and CEO of NCR Atleos. "Our recurring revenue mix reached a new high, and we saw significant margin expansion across our business segments."

Segment Performance

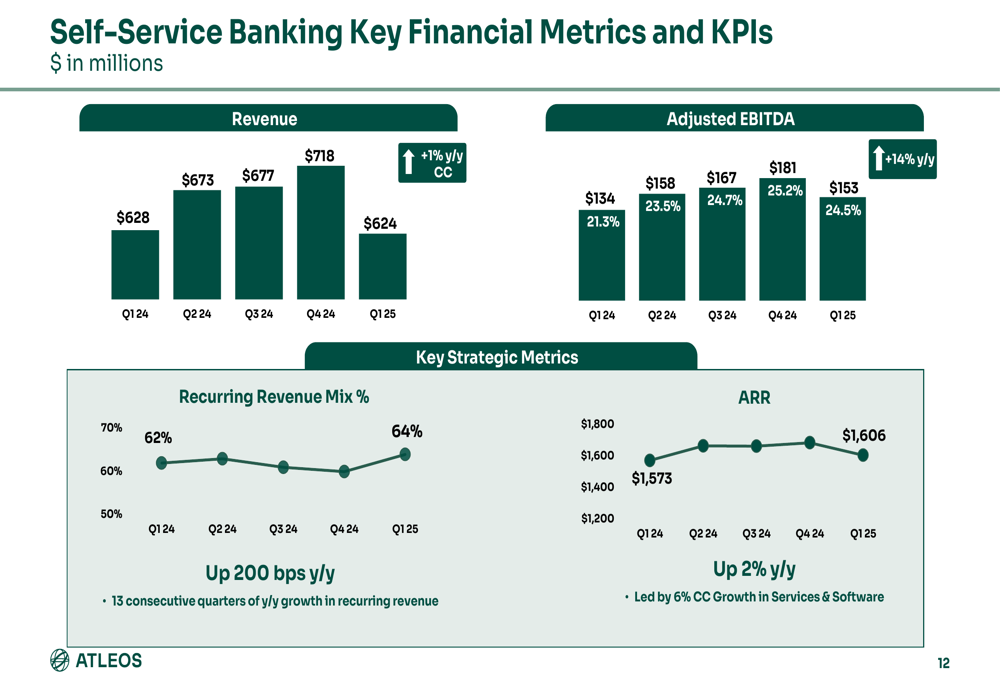

The Self-Service Banking segment, which represents the largest portion of NCR Atleos’ business, saw revenue increase in constant currency terms due to service expansion, though this was partially offset by hardware timing and foreign exchange impacts. Services growth was particularly strong, with ATMaaS (ATM as a Service) revenue increasing 24% year-over-year and ATMaaS unique customers growing 40% year-over-year.

The segment’s key financial metrics show consistent improvement in recurring revenue mix and adjusted EBITDA margins:

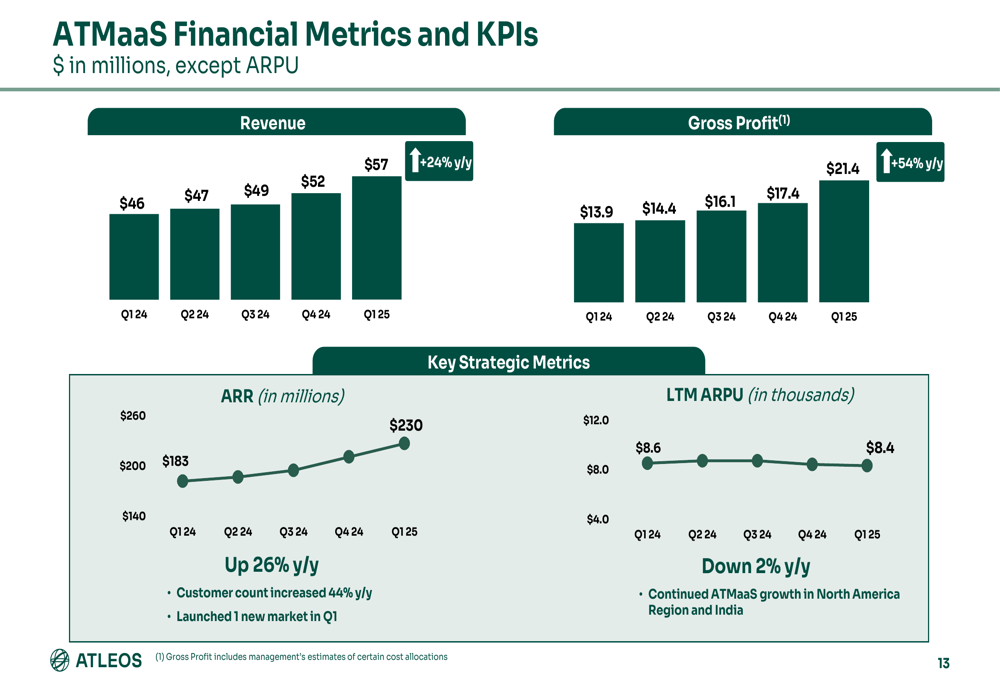

The ATMaaS business continues to be a strategic growth driver for the company, with revenue increasing 24% year-over-year to $57 million in Q1 2025, while gross profit surged 54% to $21.4 million:

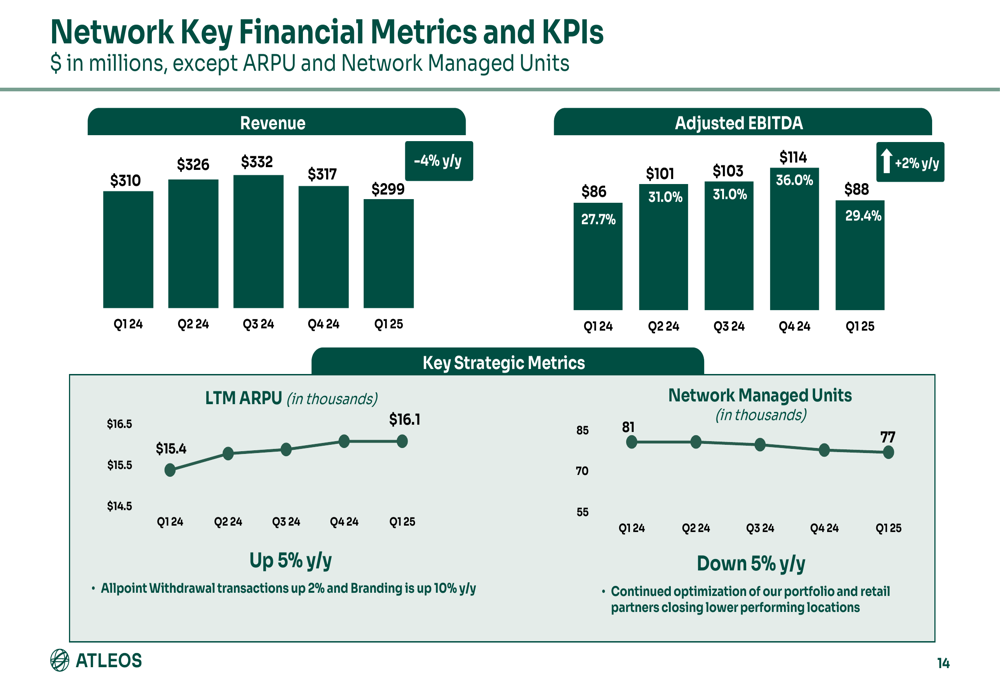

The Network segment faced some headwinds, including regulatory changes affecting the Liberty X crypto business and softness in international transactions. Despite these challenges, the segment’s adjusted EBITDA margin expanded by 170 basis points year-over-year to 29.4%, driven by a mix shift to higher-margin transactions.

As shown in the following chart of Network segment performance:

Financial Analysis

NCR Atleos’ Q1 2025 results demonstrate the company’s ability to drive profitability improvement despite top-line challenges. The shift toward higher-margin services and software revenue continues to benefit overall profitability, with services and software growing 4% year-over-year (6% in constant currency).

The company maintained a strong financial position with $688 million in liquidity as of March 31, 2025, including $352 million in unrestricted cash and $336 million in revolving credit availability. Total (EPA:TTEF) debt stood at $2.914 billion, resulting in a net leverage ratio of 3.2x.

Free cash flow was impacted by seasonal working capital changes, with adjusted free cash flow of negative $23 million for the quarter. However, management expects cash flow to improve throughout the year, consistent with historical patterns.

Strategic Initiatives

NCR Atleos continues to execute on its strategic priorities, focusing on growing efficiently, prioritizing service, and embracing simplicity. The company’s Innovation Lab has received strong customer response, and the company launched customer advocacy panels to drive service improvements.

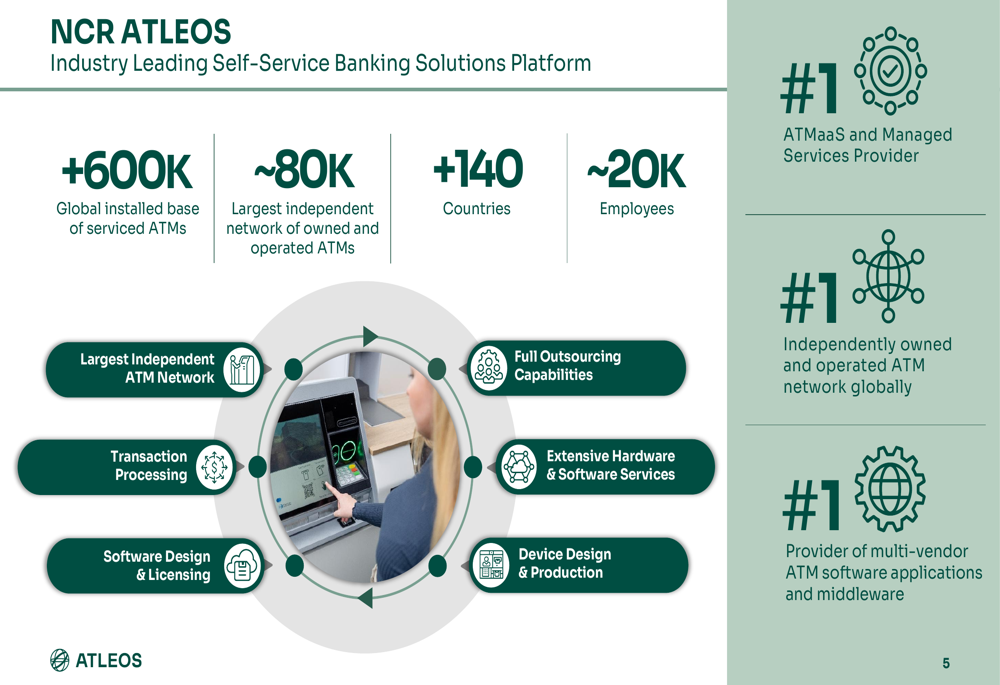

The company’s position as a leading self-service banking solutions provider is supported by its extensive global footprint and comprehensive capabilities:

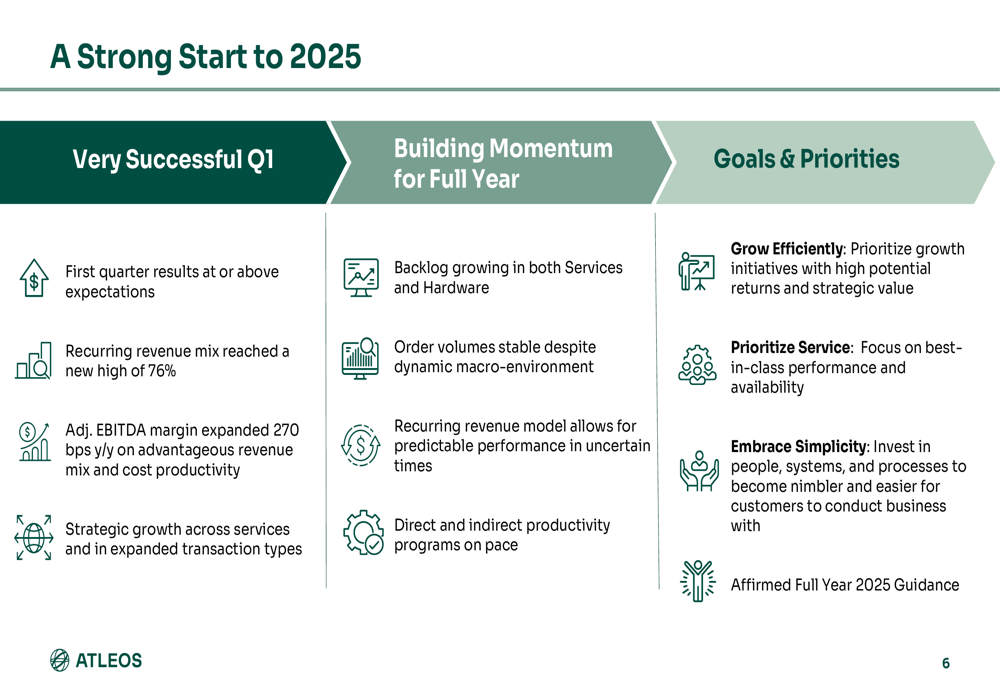

Management highlighted several strategic achievements in Q1 2025, including strong customer response to its Innovation Lab, sustained market service levels, and service-led improvement driving increased demand:

In the Network segment, the company expanded its partnership with 7-Eleven for Allpoint, grew its U.K. deposit network, and enhanced access to cash deposit capabilities and locations. These initiatives support the company’s focus on expanding transaction types and volumes across its network.

Forward Outlook

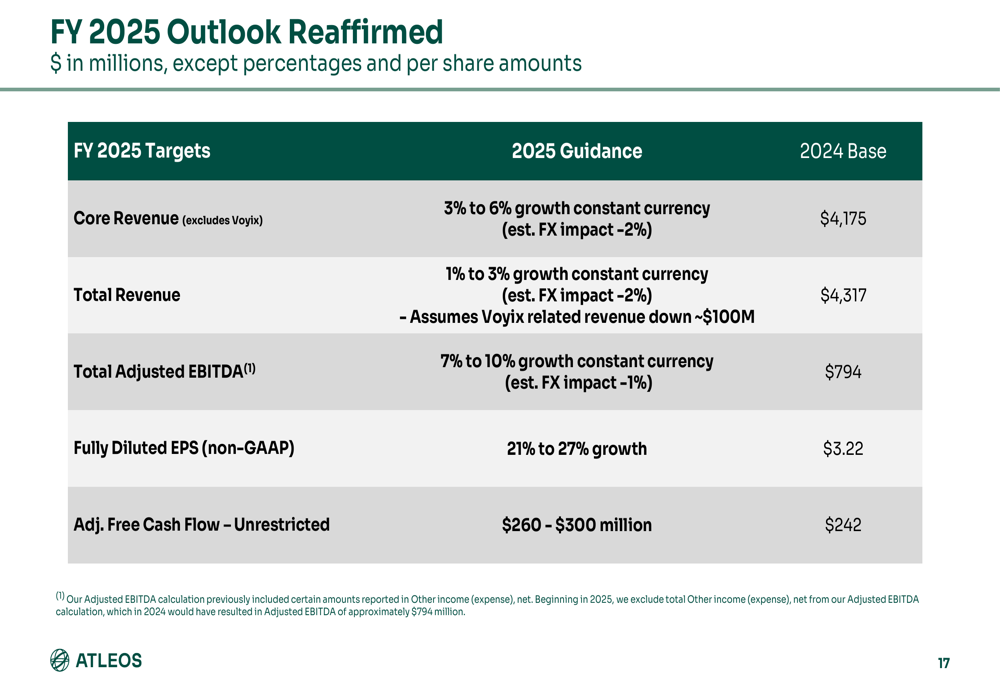

NCR Atleos reaffirmed its full-year 2025 guidance, projecting core revenue growth of 3% to 6% in constant currency, total revenue growth of 1% to 3% in constant currency, and adjusted EBITDA growth of 7% to 10% in constant currency. The company expects fully diluted non-GAAP EPS growth of 21% to 27% and adjusted free cash flow of $260-$300 million.

As shown in the following guidance summary:

Management expressed confidence in building momentum for the full year, noting that the backlog is growing in both services and hardware, and order volumes remain stable despite a dynamic macroeconomic environment. Direct and indirect productivity programs are on pace to deliver expected benefits.

The stock was trading at $30.00 in pre-market trading on May 8, up 1.9% from the previous close of $29.44, suggesting a positive initial market reaction to the results. Year-to-date, the stock has shown resilience compared to its performance in the previous year, when it experienced significant volatility following earnings releases.

With its strategic focus on expanding recurring revenue streams, particularly in the high-growth ATMaaS business, and continued margin expansion across segments, NCR Atleos appears well-positioned to deliver on its full-year 2025 targets despite the modest revenue decline in the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.