Domino’s Pizza Australia rejects Bain Capital takeover report after share surge

Neo Performance Materials Inc. (TSX:NEO) showcased strong financial performance and strategic positioning in its Q1 2025 investor presentation on May 9, 2025. The company reported significant year-over-year growth in adjusted EBITDA and highlighted progress on key initiatives, particularly its European permanent magnet facility.

Q1 2025 Performance Highlights

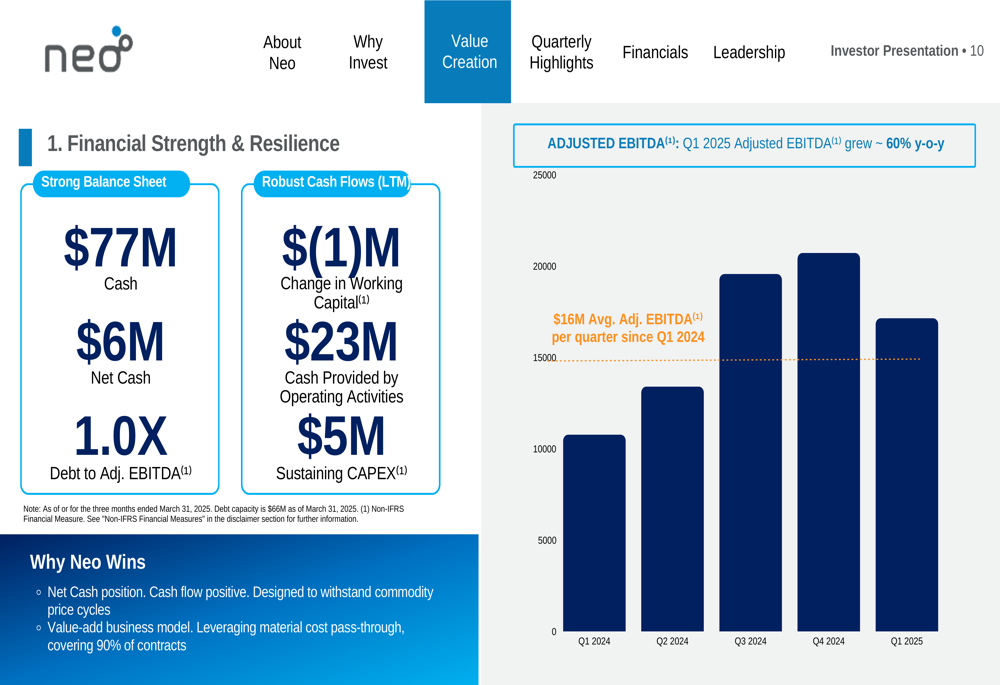

Neo Performance Materials reported impressive financial results for Q1 2025, with adjusted EBITDA growing approximately 60% year-over-year. The company maintained its 2025 guidance for adjusted EBITDA between $55 million and $60 million, reflecting confidence in its business strategy and market position.

The company’s financial strength was emphasized through key metrics including $77 million in cash, $6 million in net cash, and a debt to adjusted EBITDA ratio of 1.0x. Neo has maintained an average quarterly adjusted EBITDA of $16 million since Q1 2024, demonstrating consistent performance.

As shown in the following financial performance chart:

Neo’s robust cash flows include $23 million in cash provided by operating activities over the last twelve months, with sustaining capital expenditures of $5 million. The company attributes its resilience to a value-added business model designed to withstand commodity price cycles, with material cost pass-through covering 90% of contracts.

The company’s revenue remains well-diversified across both business segments and geography. Revenue breakdown by segment shows Rare Metals at 37%, Magnequench at 32%, and Chemicals & Oxides at 32%. Geographically, Europe and China each account for 30% of revenue, followed by Japan and North America at 16% each.

Strategic Initiatives

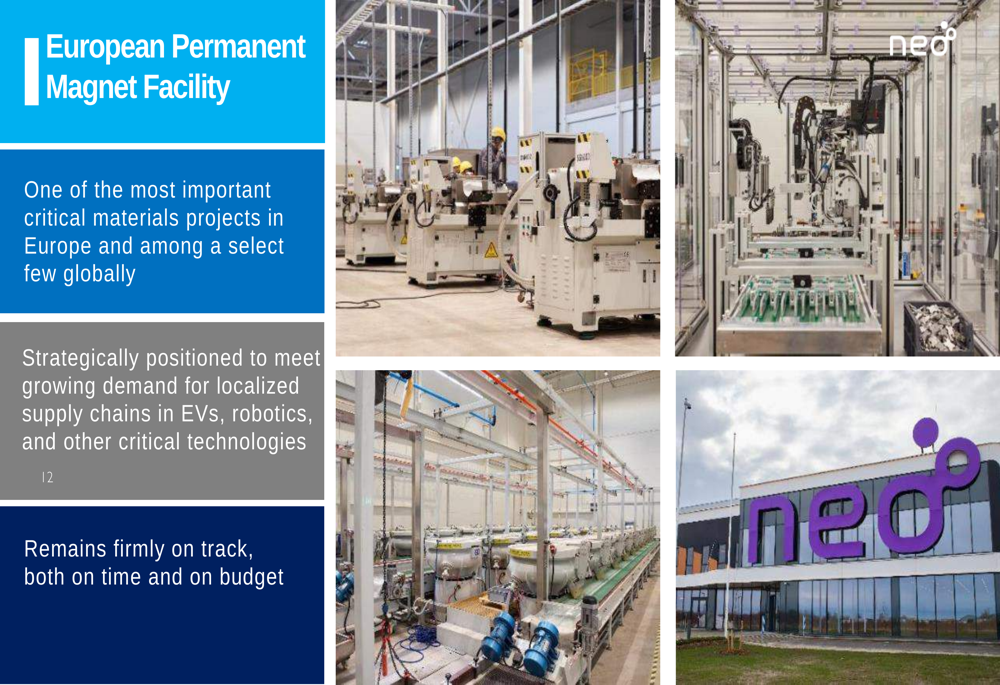

Neo’s most significant strategic initiative is its European permanent magnet facility, which remains on schedule and on budget. This facility represents one of the most important critical materials projects in Europe and positions Neo to meet growing demand for localized supply chains in electric vehicles, robotics, and other critical technologies.

The European permanent magnet facility can be seen in the following images:

The company reached a significant milestone in April 2025 with its first shipment of magnets to a Tier 1 customer. Neo produced and shipped over 18,000 sintered magnet pieces as initial samples, which are EV traction motor grade. Production part approval is scheduled for the first half of 2026, with mass production expected later that year.

Neo has also made progress on other strategic initiatives, including the opening of NAMCO (Neo Automotive Materials & Chemicals Organization) in September 2024, a world-class emissions control catalyst production facility with up to 50% additional capacity ready to be deployed.

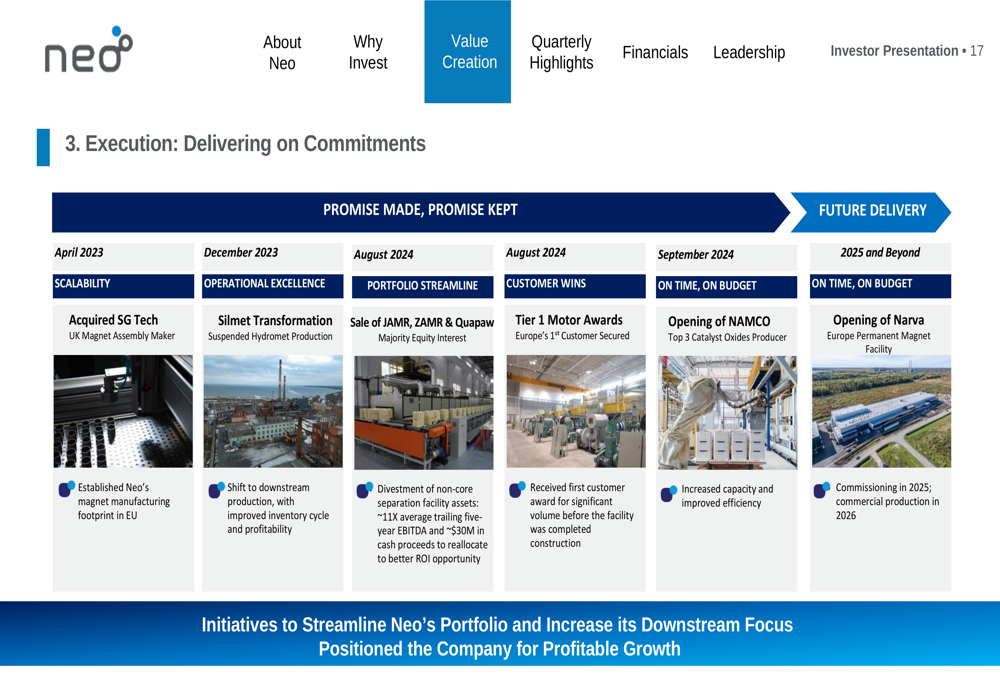

The company’s execution timeline demonstrates consistent delivery on commitments:

Competitive Industry Position

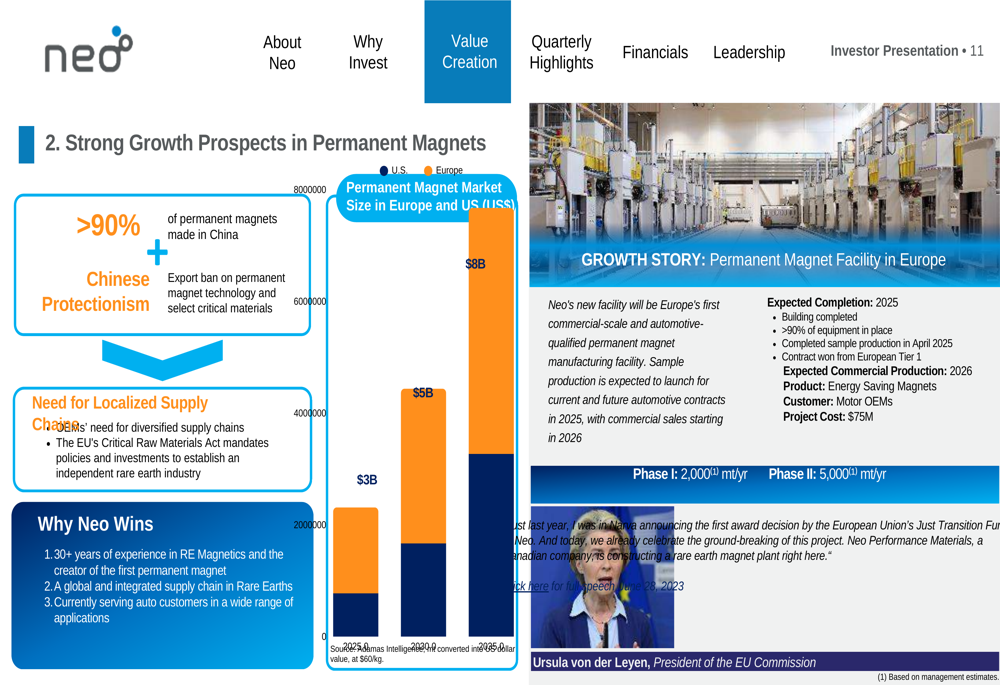

Neo Performance Materials positions itself as the #1 integrated Rare Earth Magnetics Company outside of Asia, with a unique competitive advantage in the critical materials market. The company operates in a landscape where over 90% of permanent magnets are currently made in China, creating significant opportunities for diversified supply chains.

The permanent magnet market is projected to grow substantially, with the U.S. market expected to increase from approximately $3 billion in 2023 to $5 billion by 2035, and the European market from approximately $5 billion to $8 billion in the same period.

This growth potential is illustrated in the following slide:

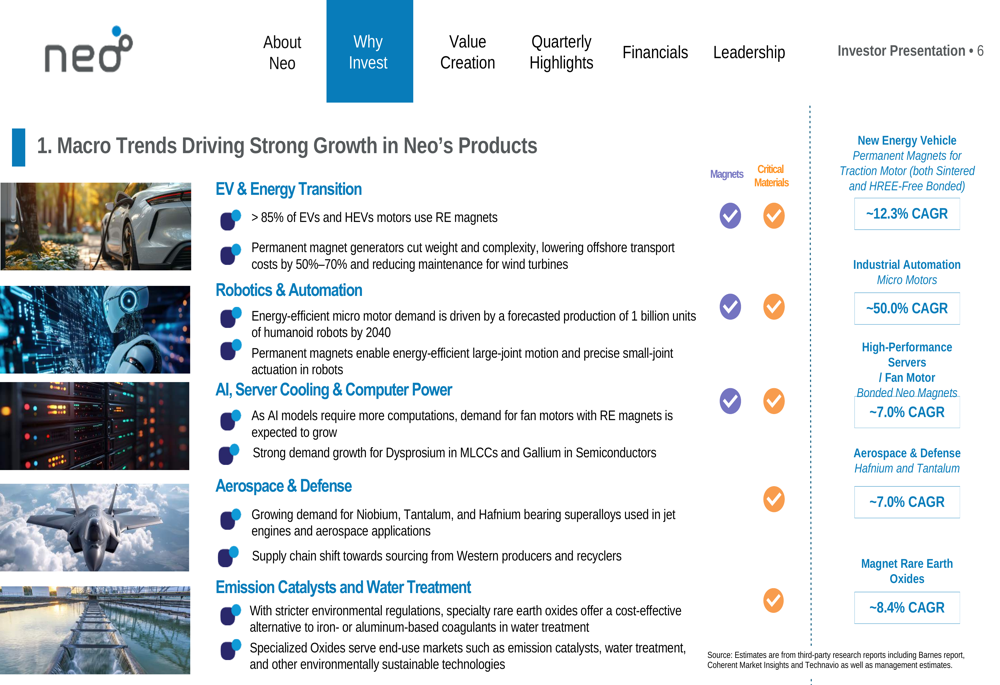

Neo’s competitive position is strengthened by macro trends driving demand for its products, including electric vehicle adoption, energy transition, robotics and automation, AI and server cooling, and aerospace and defense applications. These markets feature strong growth rates, with New Energy Vehicle Permanent Magnets for Traction Motors expected to grow at a CAGR of 12.3% and Industrial Automation Micro Motors at approximately 50.0% CAGR.

Forward-Looking Statements

Looking ahead, Neo Performance Materials expects to complete its European permanent magnet facility in 2025, with commercial production beginning in 2026. The facility will have an initial capacity of 2,000 metric tons per year in Phase I, with potential expansion to 5,000 metric tons per year in Phase II.

The company maintains its 2025 adjusted EBITDA guidance of $55-60 million and continues to advance its strategic review to maximize shareholder value. Neo’s management emphasized that the company is a net beneficiary of shifting geopolitics due to its regionally diversified, vertically integrated model.

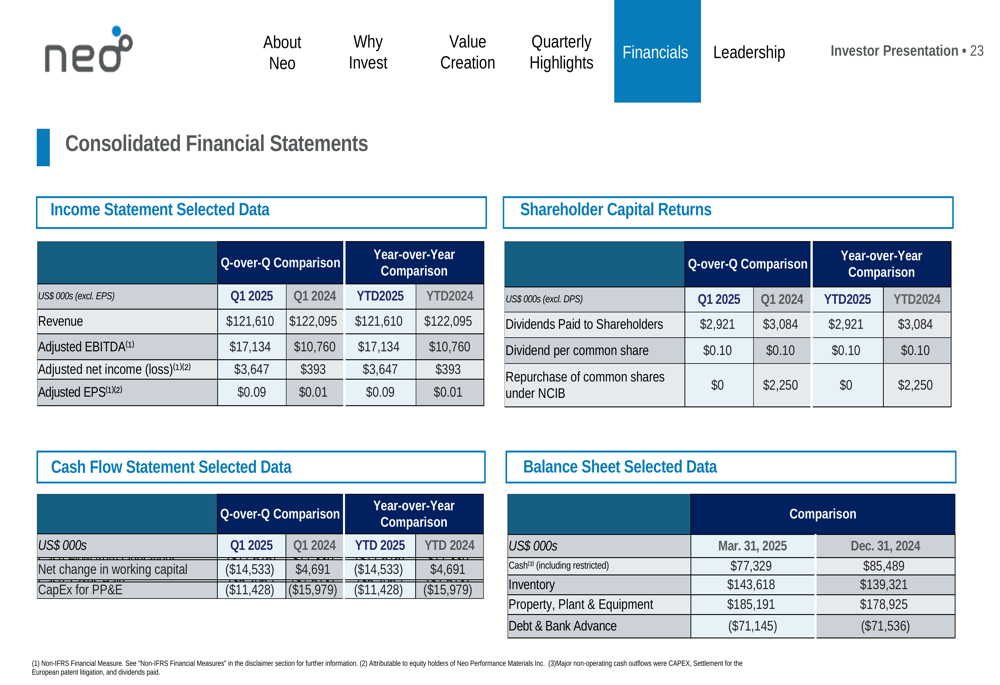

Neo’s comprehensive financial overview provides insight into its current performance and future outlook:

With a strong balance sheet, growing EBITDA, and strategic positioning in critical materials markets experiencing secular growth trends, Neo Performance Materials appears well-positioned to capitalize on increasing demand for secure, non-Chinese supply chains for rare earth magnets and other critical materials essential to energy transition and digital transformation technologies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.