S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

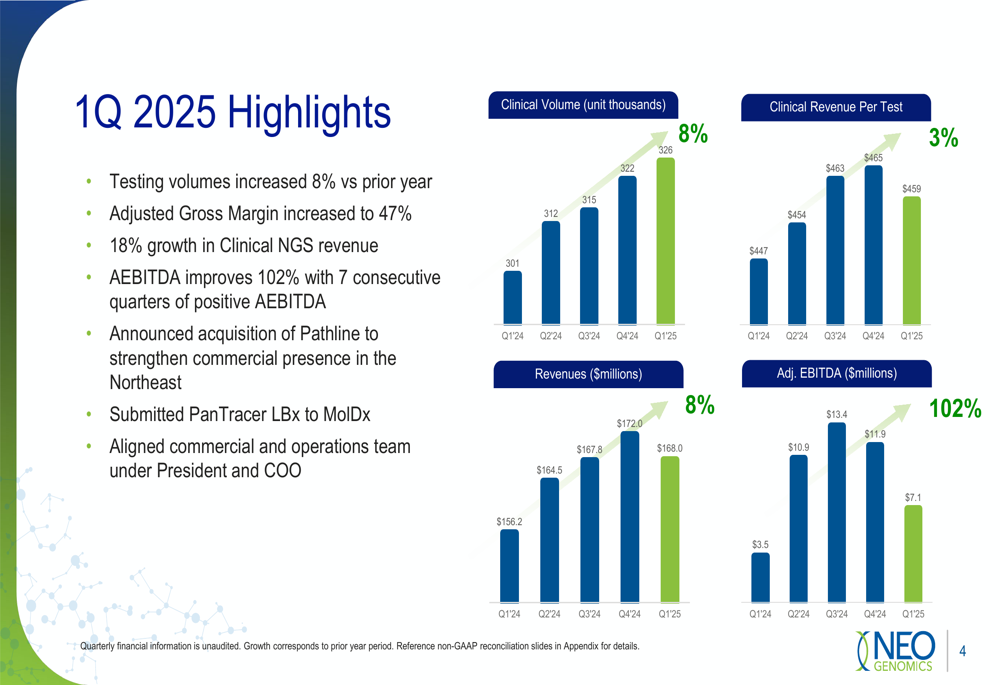

NeoGenomics, Inc. (NASDAQ:NEO) presented its first quarter 2025 financial results on April 29, 2025, showcasing a strong performance that marks a significant improvement following disappointing Q4 2024 results. The cancer diagnostics company reported 8% revenue growth and a remarkable 102% increase in Adjusted EBITDA year-over-year, signaling potential momentum shift after previous challenges that had pushed the stock near its 52-week lows.

The company’s shares closed at $9.97 on April 28, 2025, down 2.92% from the previous session, with premarket trading on the presentation day showing an additional 1.71% decline to $9.80. This market skepticism comes despite the positive quarterly results, suggesting investors may still be cautious following the company’s challenging 2024 performance.

Quarterly Performance Highlights

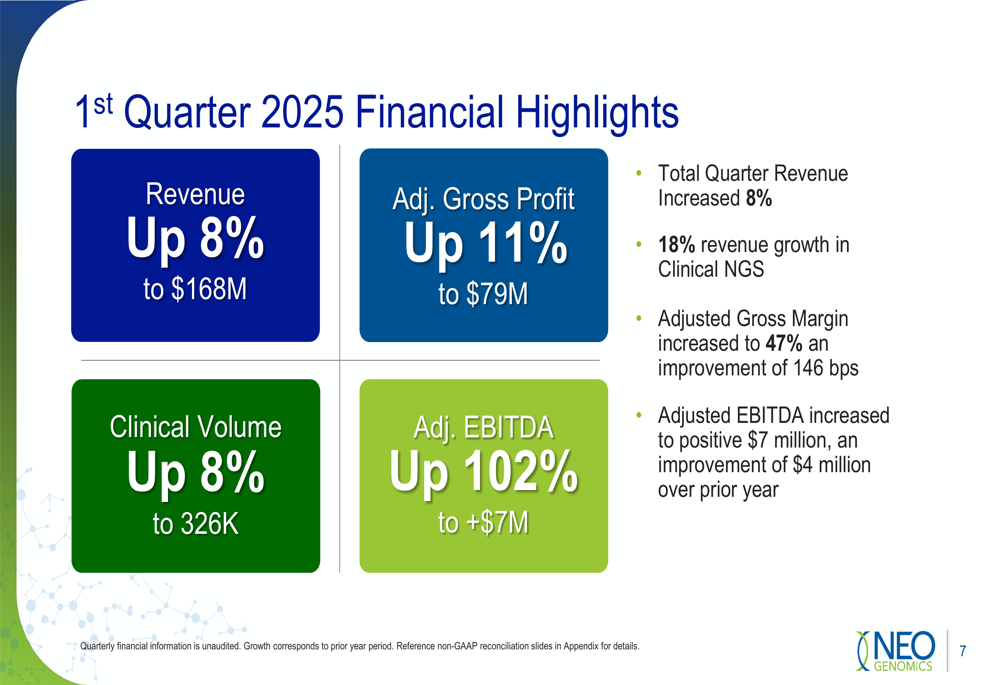

NeoGenomics reported solid financial metrics for Q1 2025, with total revenue reaching $168 million, representing an 8% increase compared to the same period last year. This growth was driven by an 8% increase in clinical testing volumes and a 3% improvement in clinical revenue per test, attributed to favorable test mix and pricing initiatives.

As shown in the following chart of quarterly financial highlights:

The company’s adjusted gross profit increased 11% year-over-year to $79 million, with adjusted gross margin expanding to 46.8%, a 146 basis point improvement from Q1 2024. Most notably, adjusted EBITDA more than doubled to $7.1 million, marking the seventh consecutive quarter of positive AEBITDA and demonstrating the company’s progress toward sustainable profitability.

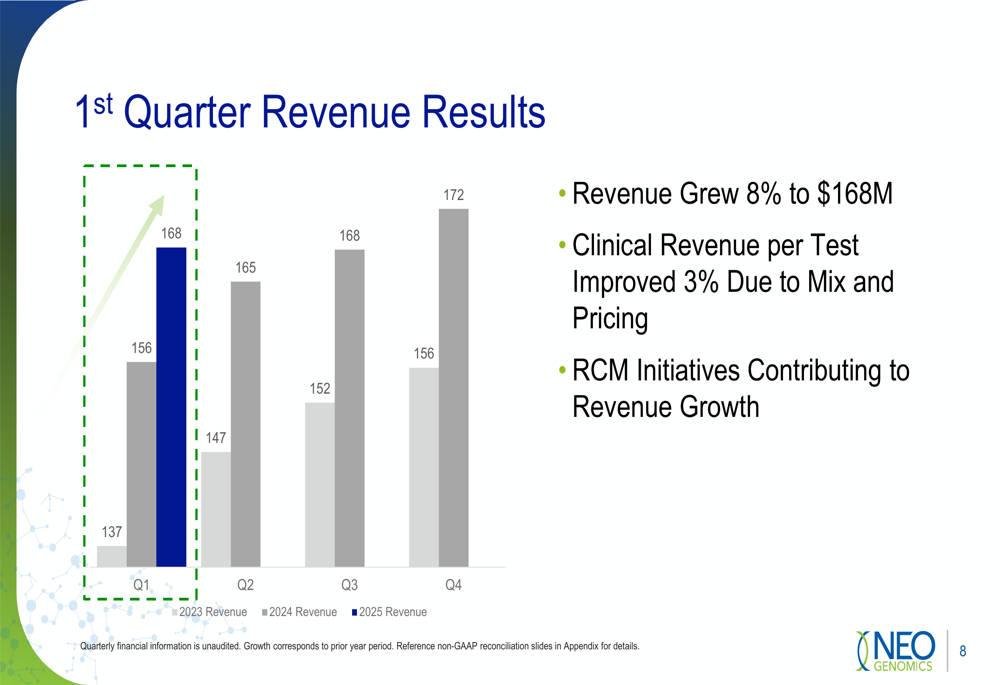

The revenue growth trend is clearly illustrated in this quarterly progression:

Clinical NGS (Next-Generation Sequencing) revenue grew by an impressive 18% year-over-year and now represents approximately 31% of total clinical revenue. This shift toward higher-value testing services reflects NeoGenomics’ strategic focus on advanced diagnostic capabilities. Additionally, five recently launched NGS tests now account for 22% of total clinical revenue, highlighting the company’s successful innovation efforts.

Strategic Initiatives

NeoGenomics outlined several strategic initiatives aimed at driving sustainable growth across its business segments. In the clinical division, the company is expanding its salesforce to up to 140 representatives while focusing on community oncology with targeted product launches.

The company’s clinical growth strategy is illustrated in this comprehensive overview:

A significant development announced during the quarter was the acquisition of Pathline, which strengthens NeoGenomics’ commercial presence in the Northeast region. This strategic move is expected to improve turnaround time for testing services in this key market and contribute an additional $12-14 million in revenue for fiscal year 2025.

The company also highlighted its partnership with EPIC to accelerate integration, scheduled to roll out in the second half of 2025, along with an Adaptive MRD Partnership to enhance its testing capabilities.

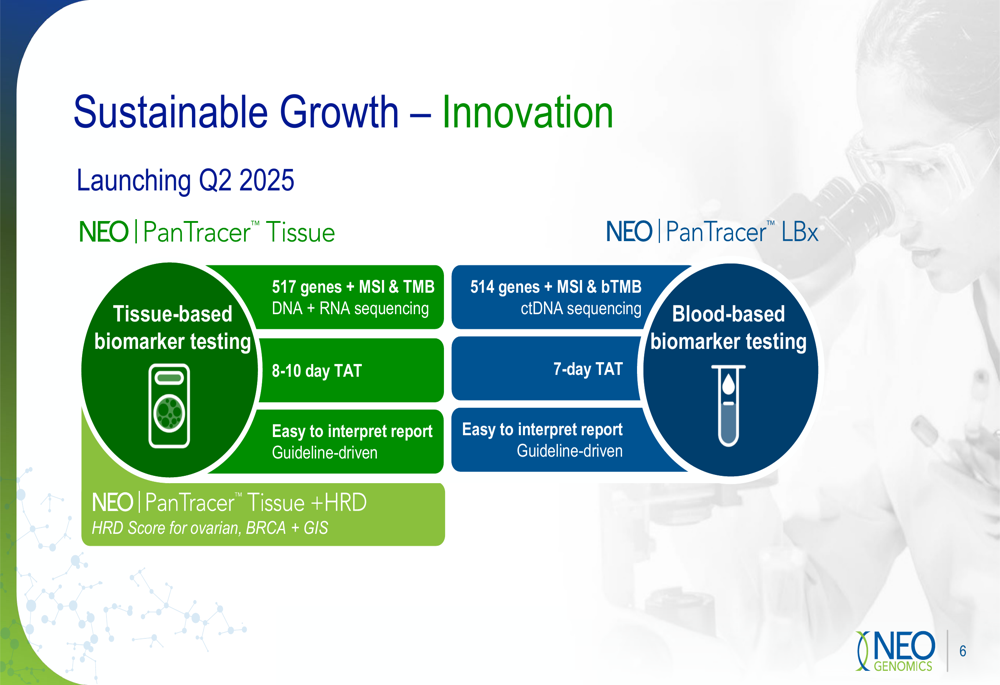

On the innovation front, NeoGenomics is preparing to launch two major new products in Q2 2025:

The PanTracer Tissue and PanTracer LBx platforms represent significant advancements in the company’s diagnostic capabilities. PanTracer Tissue will offer comprehensive tissue-based biomarker testing with 517 genes plus MSI & TMB DNA + RNA sequencing, delivering results with an 8-10 day turnaround time. Meanwhile, PanTracer LBx will provide blood-based biomarker testing with 514 genes plus MSI & bTMB ctDNA sequencing and a 7-day turnaround time. The company has already submitted PanTracer LBx to MolDx for review.

Forward-Looking Statements

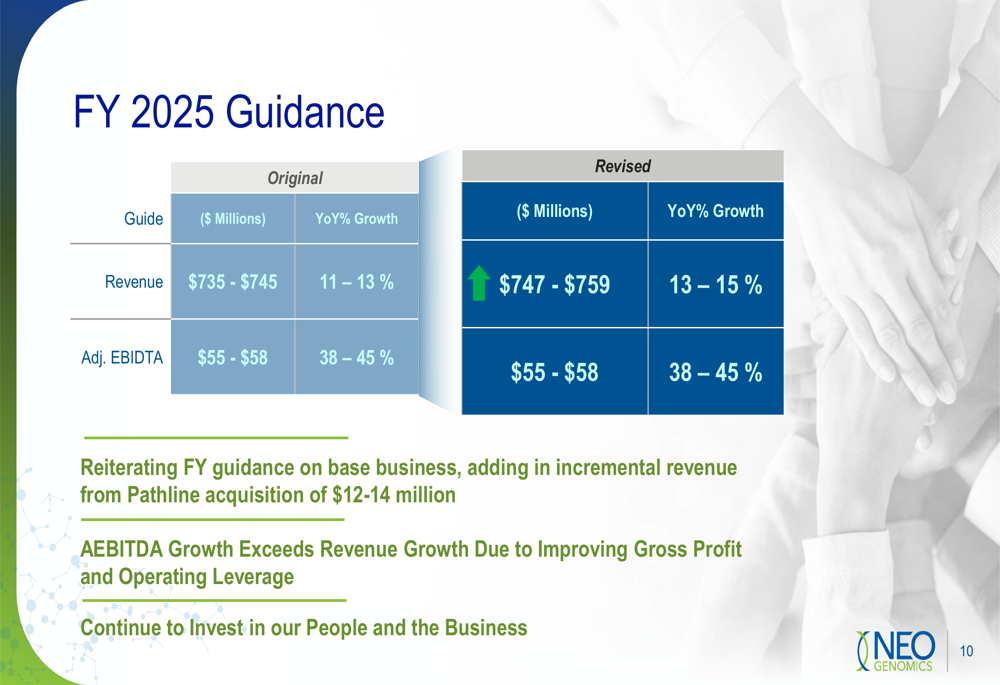

Based on the strong Q1 performance and the Pathline acquisition, NeoGenomics has raised its full-year 2025 revenue guidance while maintaining its adjusted EBITDA targets, as shown in the following guidance summary:

The revised revenue guidance of $747-759 million represents a 13-15% year-over-year growth, up from the original projection of $735-745 million (11-13% growth). This increase primarily reflects the expected $12-14 million contribution from the Pathline acquisition. The company maintained its adjusted EBITDA guidance at $55-58 million, representing 38-45% growth compared to 2024.

Management emphasized that AEBITDA growth is expected to exceed revenue growth due to improving gross profit margins and operating leverage, even as the company continues to invest in research and development and business development initiatives to drive innovation.

Financial Analysis

A deeper look at NeoGenomics’ financial position reveals both strengths and challenges. While the company reported positive adjusted EBITDA of $7.1 million, it still posted a net loss on a GAAP basis. Cash flow from operations improved slightly year-over-year but remained negative at -$25.3 million for Q1 2025.

The company’s cash position remains substantial at $358.1 million, though this represents a 7% decrease from the $384.8 million reported in Q1 2024. This cash reserve provides NeoGenomics with financial flexibility to pursue its strategic initiatives and weather any potential market challenges.

The first quarter’s key performance metrics are summarized in this comprehensive overview:

Looking ahead, NeoGenomics appears positioned for continued growth through its dual focus on clinical expansion and innovative product development. The company’s ability to translate revenue growth into improved profitability will be crucial for rebuilding investor confidence following the challenges of 2024.

As management noted in their summary, the momentum continues with revenue and volume growth of 8% and a 102% adjusted EBITDA improvement. With increased focus on R&D and business development to drive innovation, including the upcoming launch of PanTracer LBx in Q2, NeoGenomics is working to establish a stronger foundation for sustainable growth in the competitive cancer diagnostics market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.