ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Nilfisk Holding A/S (CPH:NLFSK) presented its third-quarter 2025 results on November 20, revealing a period of transition marked by positive organic growth across all regions but also significant restructuring efforts. The cleaning equipment manufacturer's stock fell 3.2% following the announcement, trading at 96.8 DKK, moving closer to its 52-week low of 73.8 DKK and well below its 52-week high of 119.8 DKK.

The company reported revenue of 238.7 million EUR, slightly below analyst expectations of 241.7 million EUR, while implementing substantial structural changes including the divestment of its US high-pressure washer business and production consolidation initiatives.

Quarterly Performance Highlights

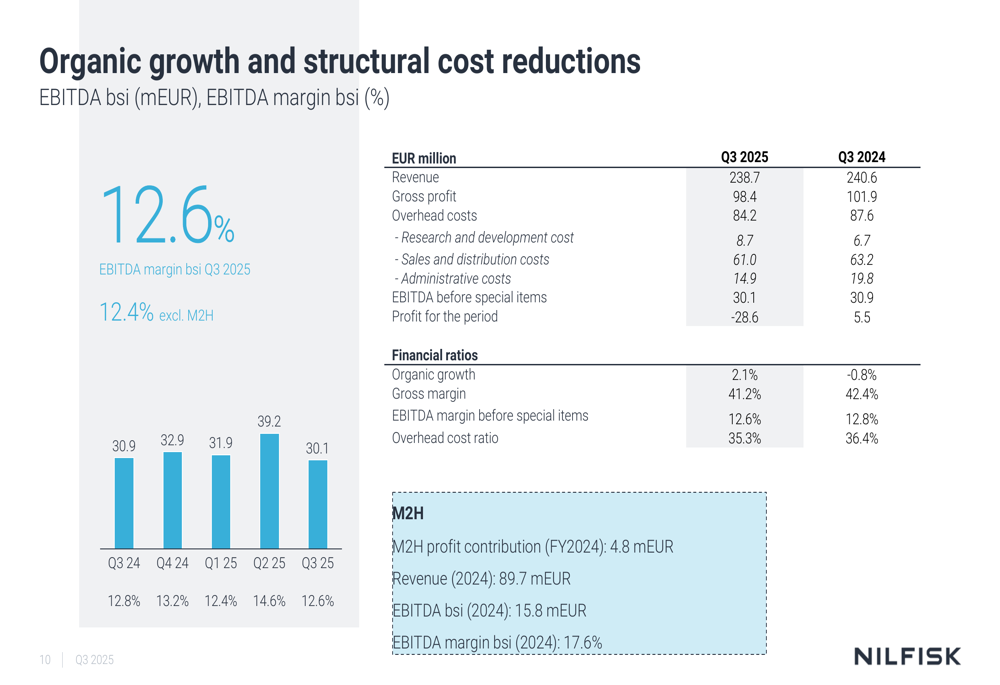

Nilfisk delivered organic growth of 2.1% in Q3 2025, a notable improvement compared to the -0.8% reported in the same period last year. However, revenue slightly decreased from 240.6 million EUR in Q3 2024 to 238.7 million EUR in the current quarter, primarily due to divestments and currency effects.

The company achieved an EBITDA before special items of 30.1 million EUR, representing a margin of 12.6%, slightly down from 12.8% in Q3 2024. This performance reflects both positive growth initiatives and ongoing cost challenges.

As shown in the following financial comparison chart:

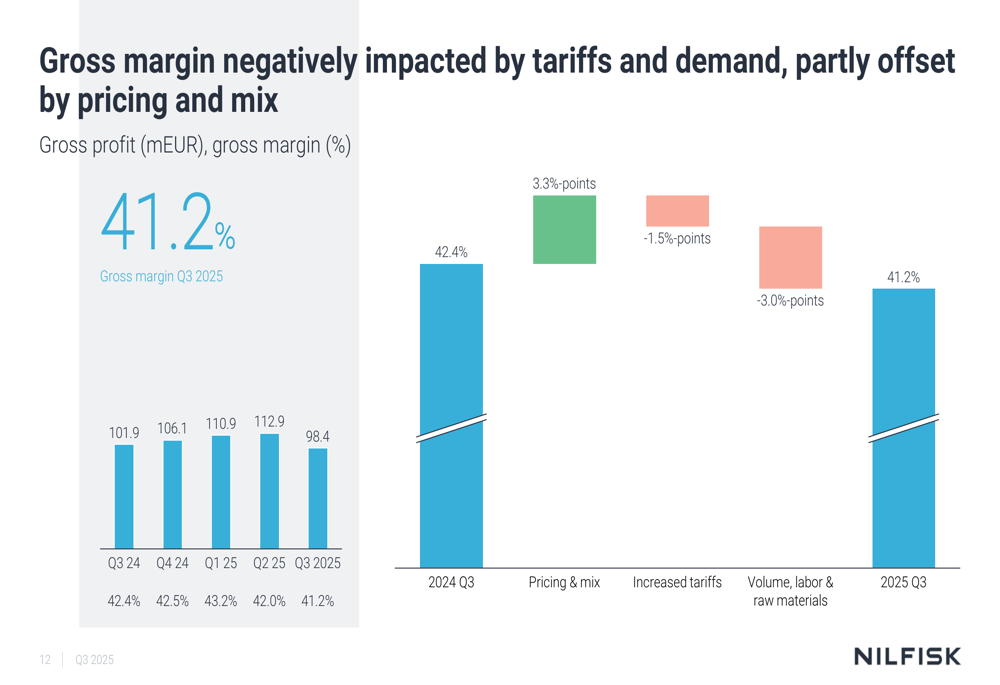

Gross margin declined to 41.2% from 42.4% in the prior year, impacted by increased tariffs and volume challenges, despite positive contributions from pricing and mix improvements. The company's gross profit breakdown reveals the specific factors affecting margin performance:

Regional Performance Analysis

Nilfisk reported organic growth across all three geographical regions, with particularly strong performance in the Americas and Asia-Pacific markets when excluding divested businesses.

The regional breakdown shows varied performance across markets:

In the EMEA region, organic growth reached 2.8%, marking the sixth consecutive quarter of growth. This was driven by strong service growth and solid performance in the professional segment, though overall reported growth was only 0.1% due to the impact of consumer and private label businesses.

The Americas region achieved 4.3% organic growth, but the figure rises to an impressive 9.1% when excluding the recently divested US high-pressure washer business. This underscores the strategic rationale behind the divestment decision.

The APAC region continued its recovery with 7.9% organic growth, representing the third consecutive quarter of positive growth in this market.

Strategic Initiatives & Restructuring

Nilfisk is implementing significant structural changes to improve long-term competitiveness. A key initiative is the consolidation of its North American production footprint, with manufacturing operations moving from Brooklyn Park to Querétaro, Mexico. This consolidation aims to deliver multiple operational benefits:

The company has also finalized the divestment of its US high-pressure washer business in October 2025, which had been underperforming compared to core segments. Additionally, Nilfisk is conducting a strategic product portfolio review to reduce complexity and focus on higher-margin offerings.

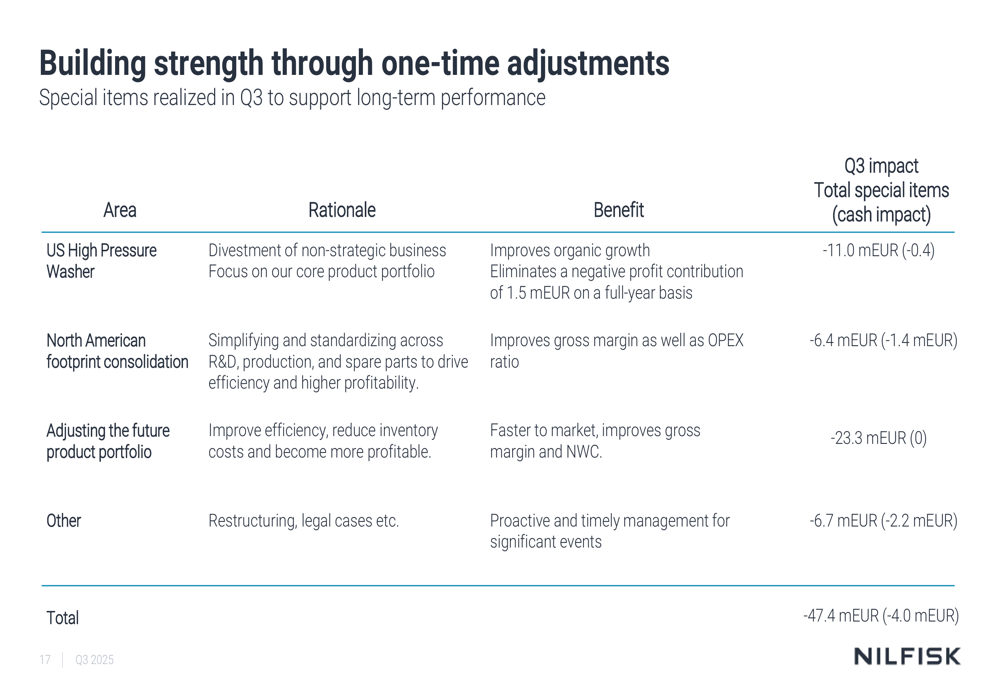

These restructuring efforts have resulted in substantial special items and impairments totaling 47.4 million EUR, though the actual cash impact is limited to 4.0 million EUR. The breakdown of these one-time adjustments shows the scope of the company's transformation:

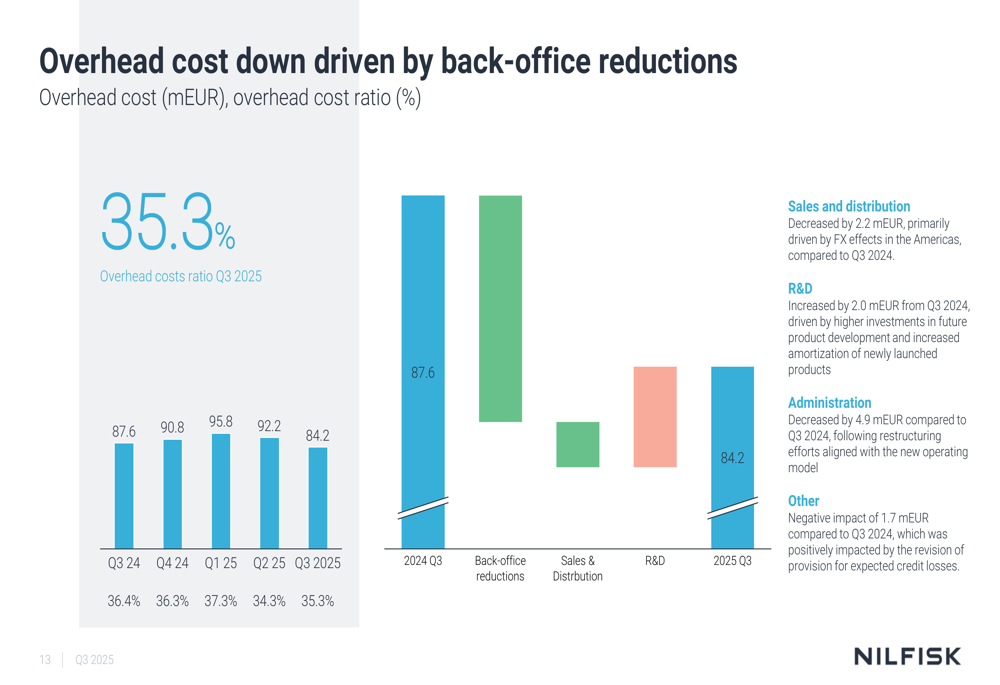

Nilfisk has made progress in reducing overhead costs, which decreased from 87.6 million EUR in Q3 2024 to 84.2 million EUR in Q3 2025. This reduction has been primarily driven by back-office efficiencies, as illustrated in the following chart:

Financial Outlook & Guidance

Looking ahead, Nilfisk has revised its organic growth guidance to approximately 1% for the full year 2025, while maintaining its EBITDA margin target of 13-14% before special items. This outlook is based on assumptions of stable market conditions in EMEA, reduced uncertainty in the US market, and moderate growth in the APAC region.

The company's cash flow position showed improvement in Q3, with free cash flow of 10.5 million EUR and a gearing ratio of 2.3x. Management emphasized that ongoing efforts to optimize working capital and reduce inventory levels will remain priorities for the remainder of 2025.

Despite the positive organic growth across regions, the revised guidance and significant restructuring charges reflect a company in transition, working to balance growth initiatives with necessary operational adjustments in a challenging market environment. Investors will be watching closely to see if these strategic changes translate into improved profitability and sustainable growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.