Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Nine Energy Service Inc (NYSE:NINE) presented its Q2 2025 investor presentation on August 6, 2025, highlighting the company’s performance amid challenging market conditions. The oilfield services provider reported revenue at the upper end of guidance despite industry rig count declines, with technology-based business lines showing sequential growth while maintaining its asset-light strategy.

Trading at $0.71 per share, Nine Energy continues to navigate a complex energy landscape where oil and natural gas price fluctuations directly impact drilling and completion activity. The company’s strategic focus on technology-driven solutions appears to be yielding results in specific service segments, even as overall financial metrics showed a slight sequential decline.

Quarterly Performance Highlights

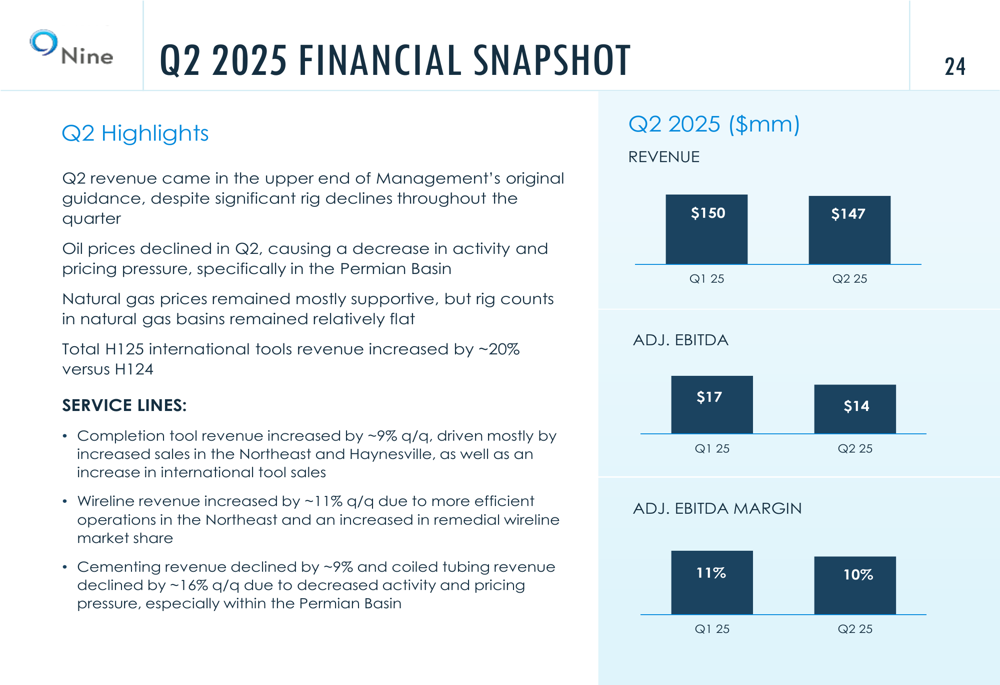

Nine Energy reported Q2 2025 revenue of $147 million, slightly down from $150 million in Q1 2025 but within the company’s guidance range. Adjusted EBITDA decreased to $14 million from $17 million in the previous quarter, with margins contracting from 11% to 10%.

As shown in the following quarterly financial snapshot:

The company’s performance varied across service lines, with completion tool revenue increasing approximately 9% quarter-over-quarter and wireline revenue growing by about 11%. However, cementing revenue declined by approximately 9% during the same period.

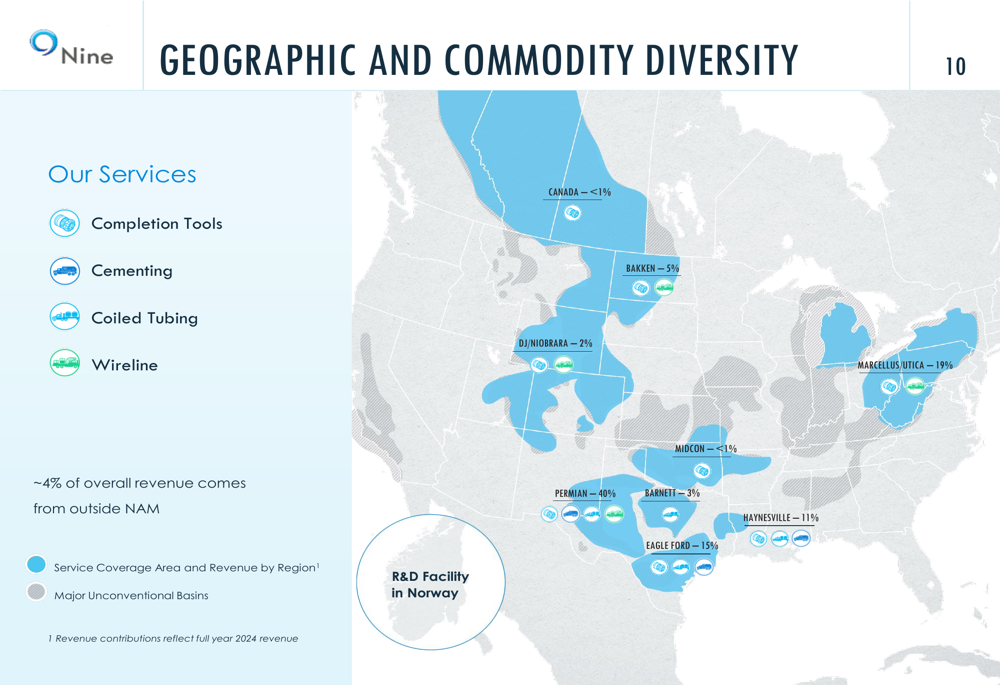

Nine Energy maintained a diversified geographic footprint, with the Permian Basin representing its largest market at 40% of revenue. Other significant regions include the Marcellus/Utica (19%), Eagle Ford (15%), and Haynesville (11%), providing some insulation from regional market fluctuations.

The company’s geographic diversity is illustrated in this regional breakdown:

Strategic Initiatives

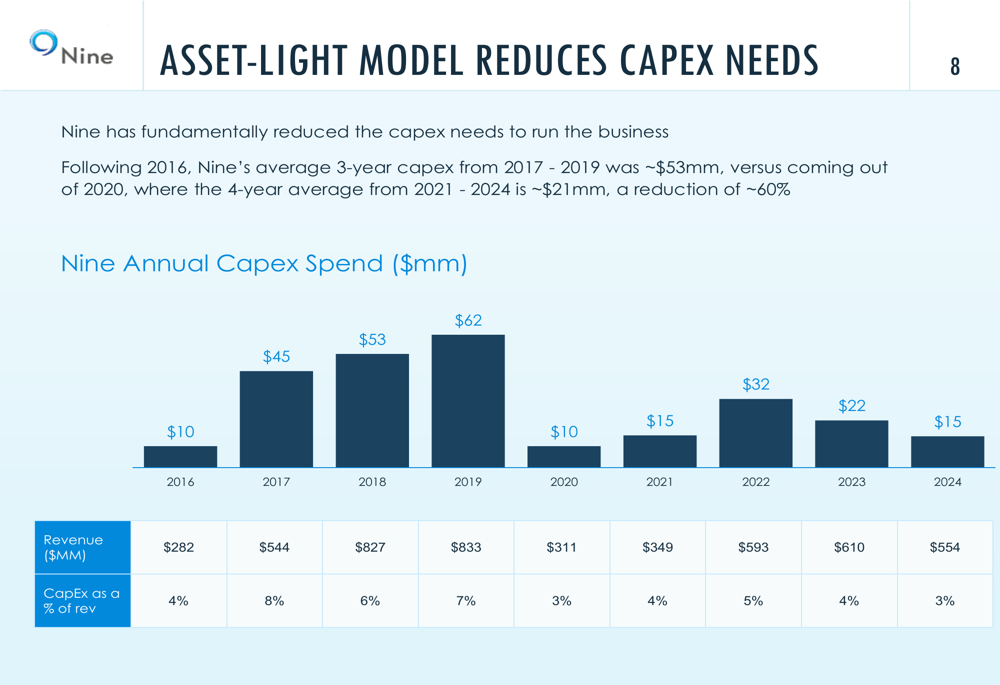

Nine Energy’s presentation emphasized its asset-light business model, which has fundamentally reduced capital expenditure requirements. Following the industry downturn in 2020, the company has maintained significantly lower capex levels, averaging approximately $21 million annually from 2021-2024 compared to approximately $53 million from 2017-2019—a reduction of about 60%.

This capital efficiency strategy is clearly demonstrated in the following chart:

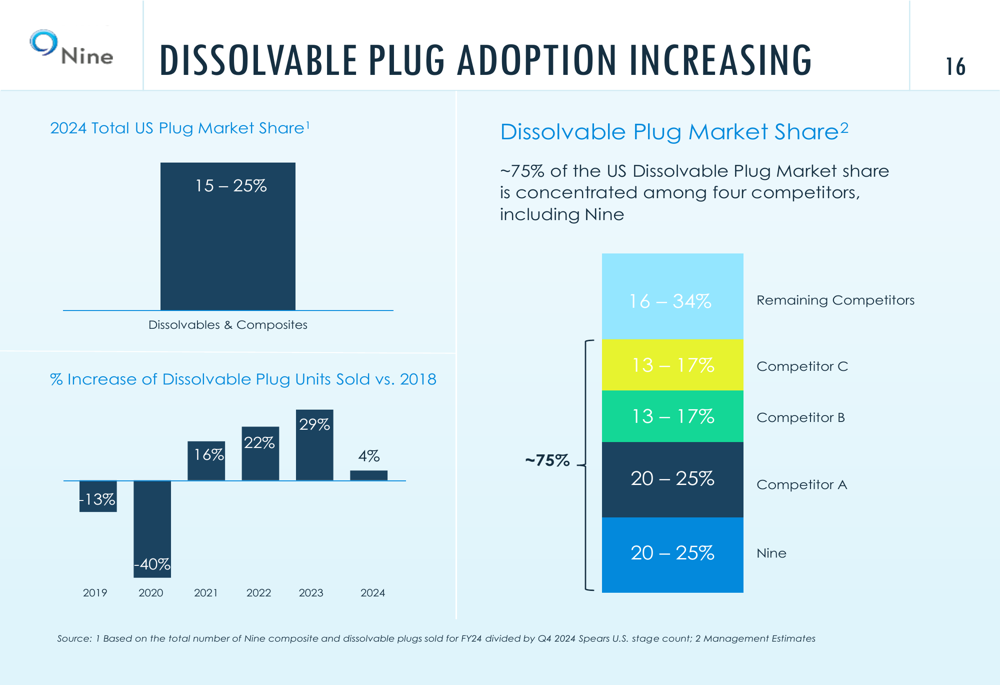

The company continues to focus on technology-driven solutions, with approximately 60% of its business coming from technology-based services. Nine Energy has established a strong position in the dissolvable plug market, claiming 20-25% market share in this growing segment that represents 15-25% of the total U.S. plug market.

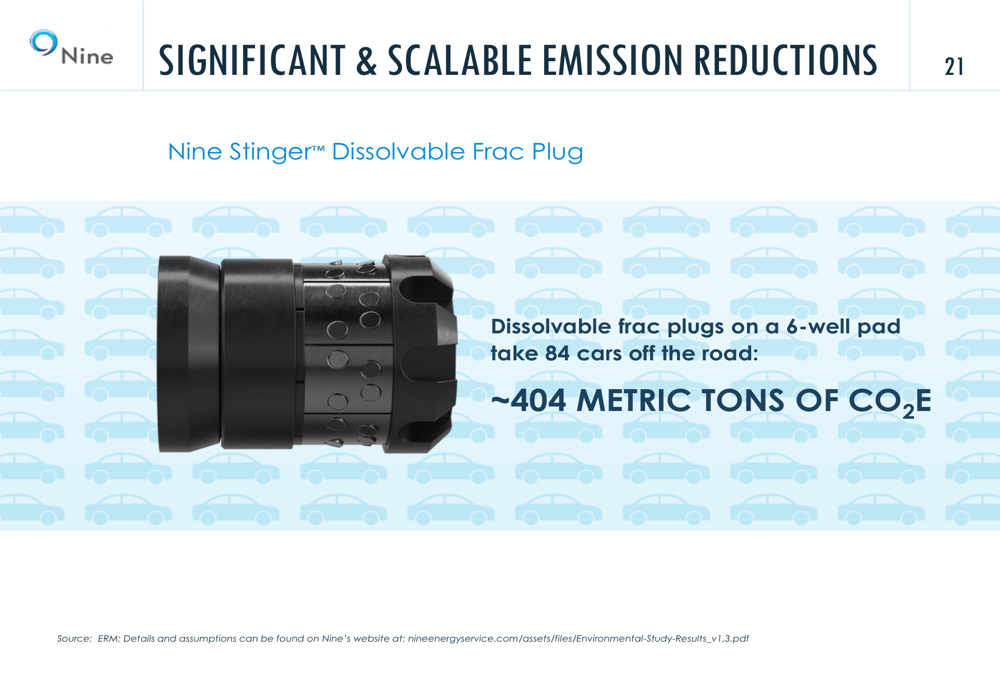

The Stinger™ dissolvable frac plug represents a key product in Nine’s technology portfolio, offering benefits including shorter design, predictable dissolution, and strong patent protection. The company emphasized the environmental benefits of this technology, noting that using dissolvable frac plugs on a six-well pad can reduce emissions equivalent to taking 84 cars off the road.

The environmental impact of Nine’s technology solutions is highlighted in this visual:

Nine Energy is also expanding into new markets through its technology offerings, including the refrac market, international markets, and restricted completion environments. The company’s ESG technology initiatives include dissolvable pumpdown rings that reduce horsepower requirements by approximately 48%, water usage by about 28%, and diesel fuel consumption by roughly 42%.

Financial Position & New Credit Facility

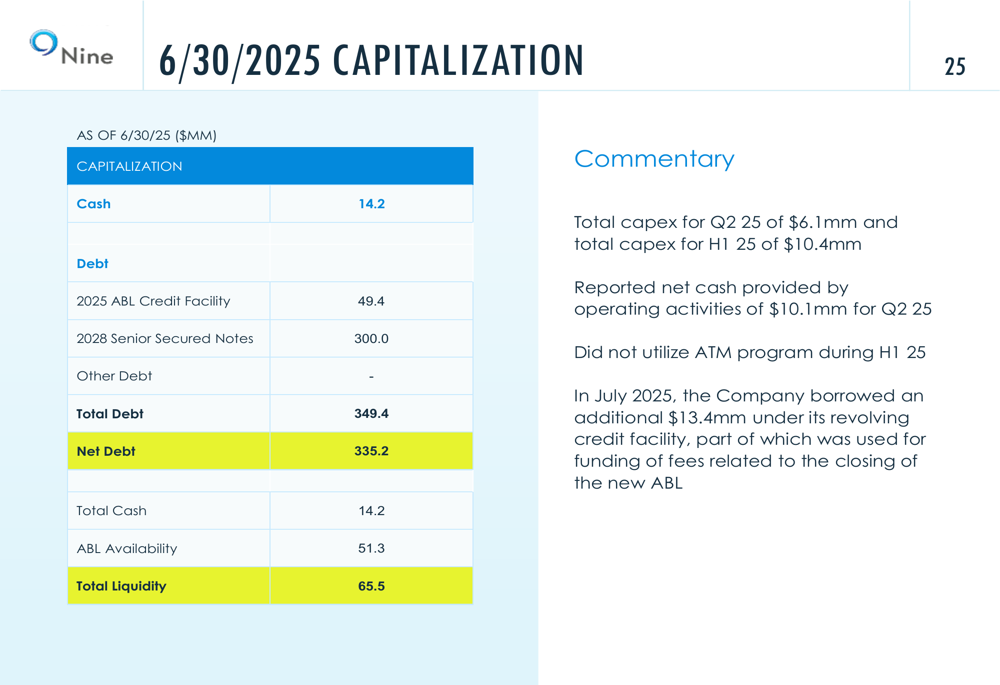

As of June 30, 2025, Nine Energy reported a cash position of $14.2 million and total debt of $349.4 million, resulting in net debt of $335.2 million. The company’s capitalization structure is detailed below:

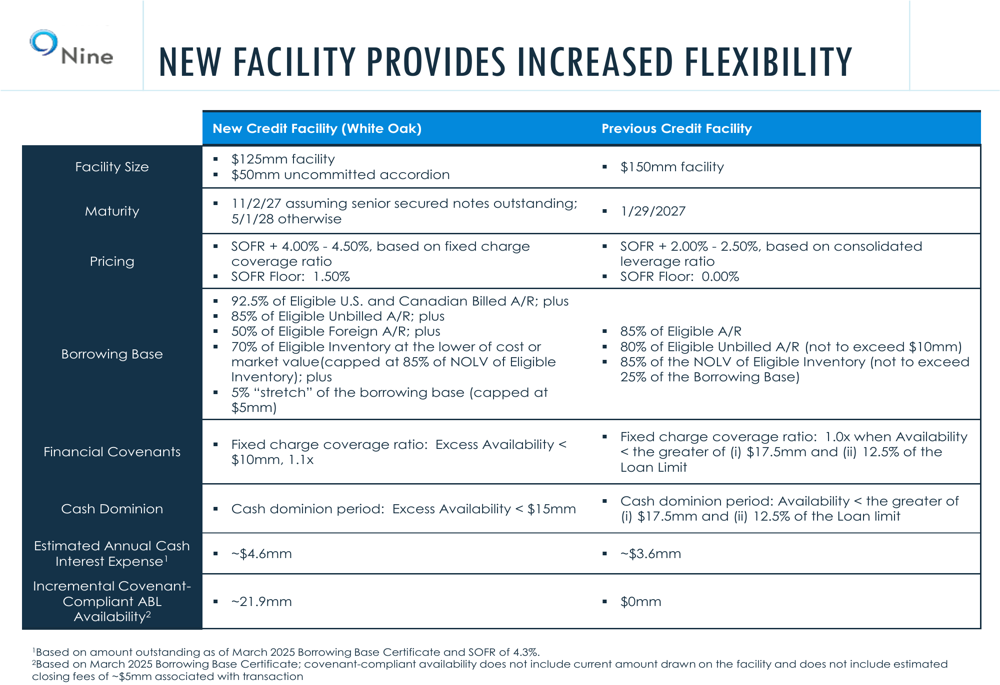

A significant development in Q2 was the establishment of a new revolving credit facility with White Oak, replacing the company’s previous facility. The new arrangement provides $125 million in commitments with an uncommitted accordion of up to $50 million. While the facility size is smaller than the previous $150 million arrangement, the improved borrowing base terms have increased Nine’s covenant-compliant availability by approximately $21.9 million.

The key differences between the new and previous credit facilities are illustrated here:

The new facility extends the maturity by nine months to November 2027 but comes with higher pricing (SOFR + 4.00%-4.50% versus the previous SOFR + 2.00%-2.50%), which is expected to increase Nine’s annual cash interest expense by approximately $1 million. Despite this higher cost, management emphasized that the arrangement provides greater flexibility and improved liquidity.

Forward-Looking Statements

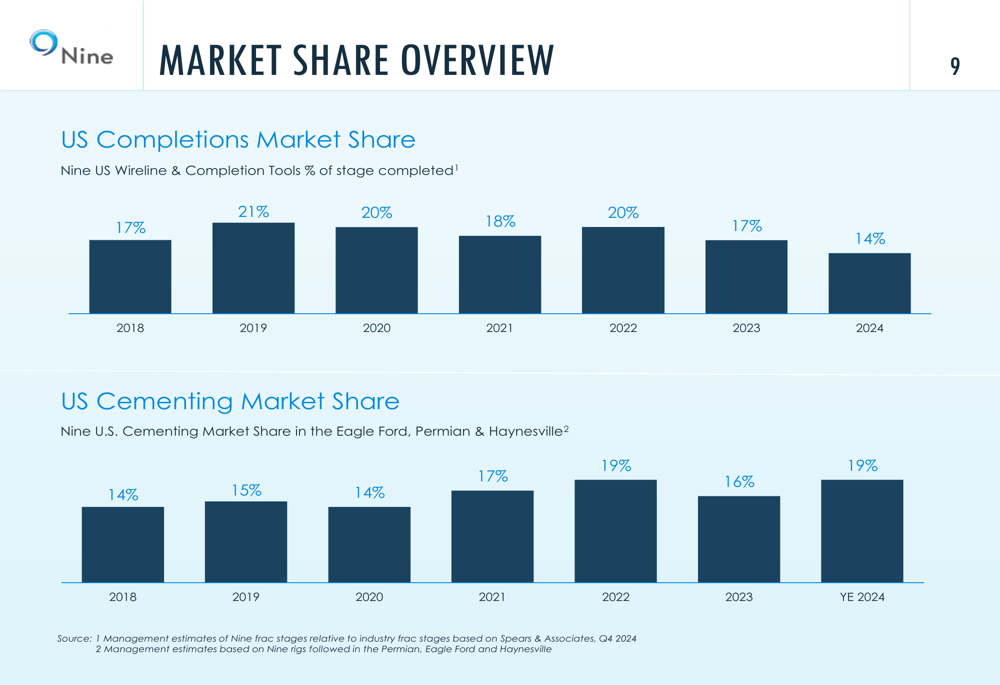

Nine Energy’s market position shows some mixed trends, with U.S. completions market share declining from 17% in 2023 to 14% in 2024, while U.S. cementing market share in key basins increased from 16% to 19% over the same period. This competitive landscape is captured in the following chart:

The company continues to invest in technology development, particularly in its completion tools segment, which showed the strongest growth in Q2. Nine Energy’s dissolvable plug adoption has increased significantly since 2018, though 2024 showed more modest growth of 4% compared to 29% in 2023.

The trend in dissolvable plug adoption is shown here:

While Nine Energy did not provide specific guidance for the remainder of 2025 in the presentation materials, the company’s emphasis on its asset-light model and technology-driven strategy suggests a continued focus on cash flow generation and capital efficiency amid market uncertainties. The new credit facility provides additional financial flexibility as the company navigates fluctuating commodity prices and industry activity levels.

With a strong safety record, diverse customer base including major energy companies, and growing technology portfolio, Nine Energy appears positioned to leverage its strengths while managing the challenges of a competitive oilfield services market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.