China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

Nova Ljubljanska Banka dd Ljubljana (LJSE:NLBR) shares rose 2.56% to €176 following the release of its Q3 2025 financial results on November 6, 2025, as investors responded positively to the bank's continued expansion across Southeast Europe despite some margin pressure.

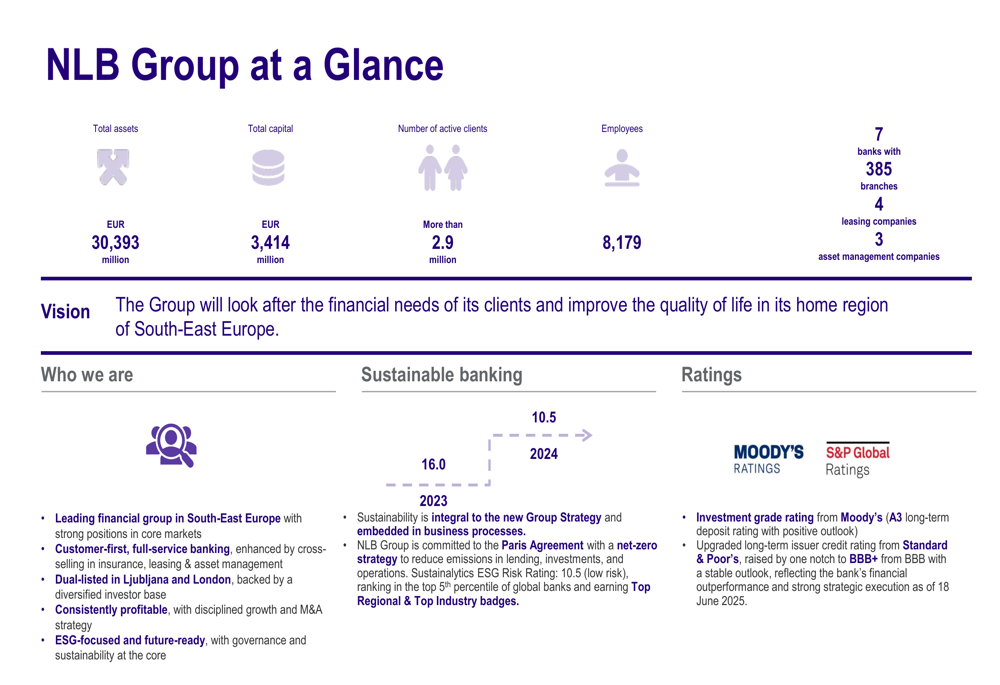

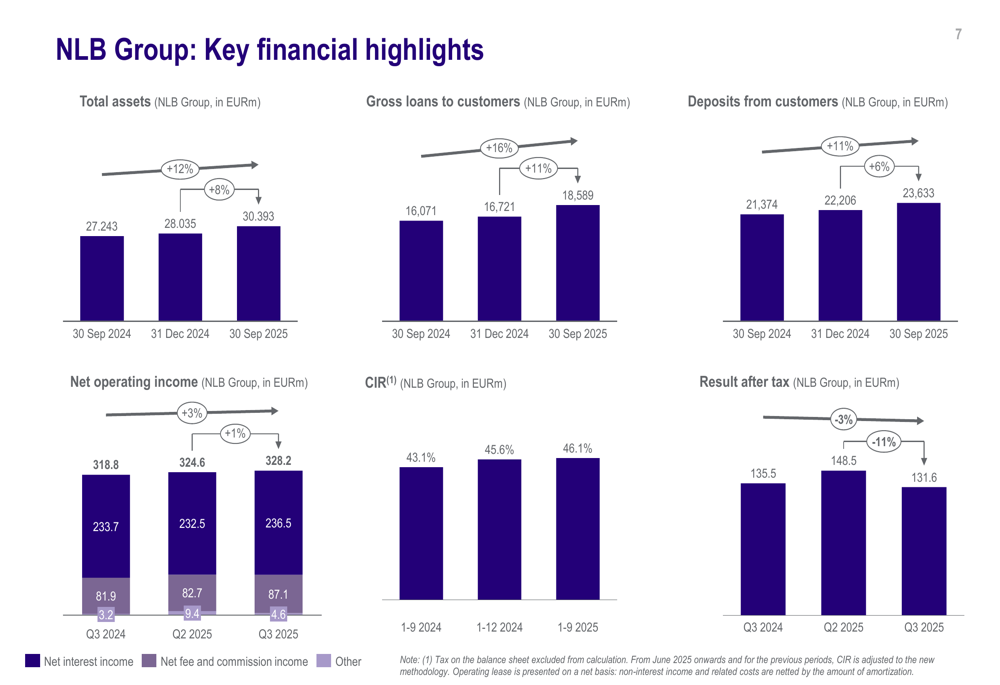

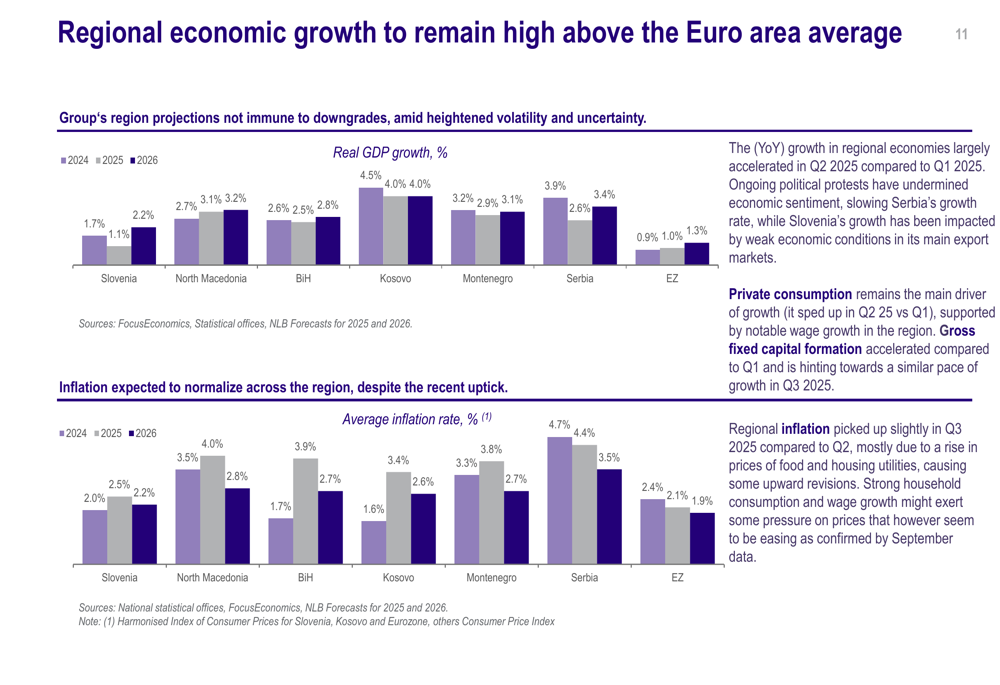

The Slovenia-based banking group demonstrated solid growth metrics across its operations in seven countries, with total assets reaching €30.4 billion, representing an 11.6% increase year-over-year. This growth comes amid a regional economic environment that continues to outperform the Eurozone average, though with some signs of moderating momentum.

As shown in the following chart of the bank's regional economic footprint, NLB maintains significant market positions across its core territories:

Quarterly Performance Highlights

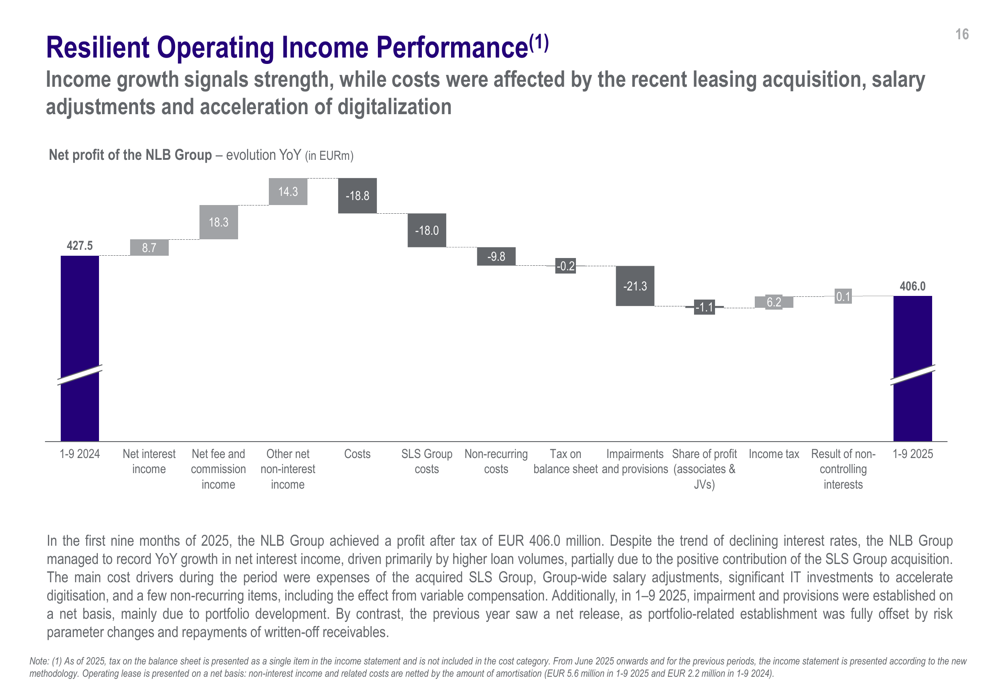

For the first nine months of 2025, NLB Group reported a profit after tax of €406.0 million. However, the quarterly profit trend showed some pressure, with Q3 2025 result after tax at €131.6 million, down from €135.5 million in Q3 2024 and €148.5 million in Q2 2025.

The bank's loan portfolio expanded significantly, with gross loans to customers increasing 15.7% year-over-year to €18.6 billion as of September 30, 2025, compared to €16.1 billion a year earlier. Customer deposits grew at a slower pace of 10.6% to €23.6 billion, resulting in the loan-to-deposit ratio increasing to 77%, as confirmed in the earnings call.

This financial performance is illustrated in the following key metrics chart:

CEO Blaž Brodnjak emphasized the bank's delivery on strategic promises during the earnings call, stating, "We are delivering what we promise," while highlighting the group's digital transformation efforts and regional growth potential.

Detailed Financial Analysis

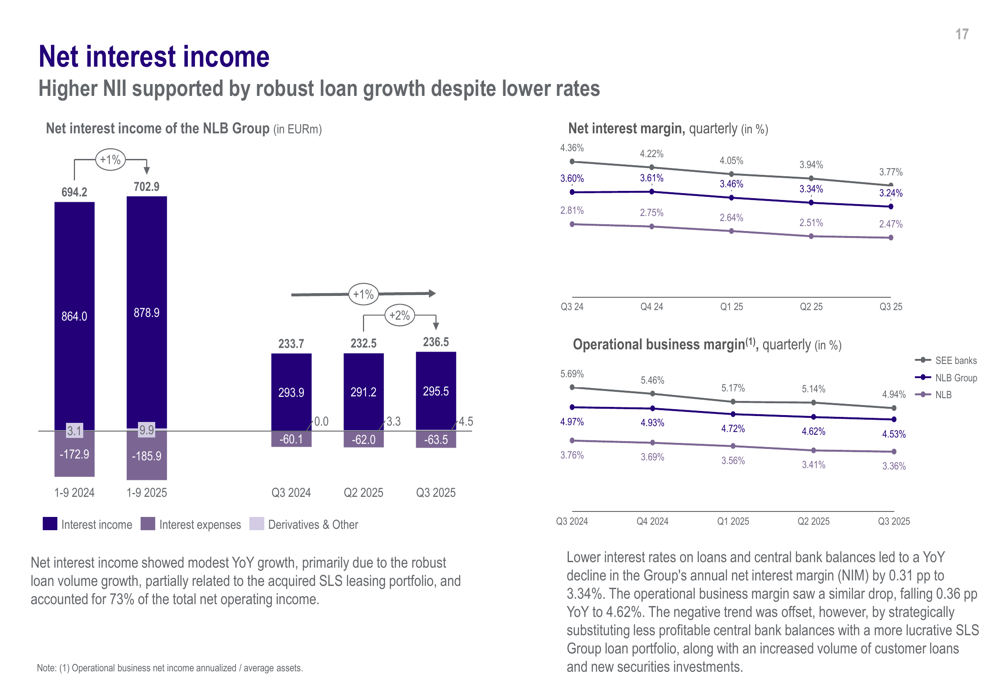

NLB's net interest margin has been under pressure, declining steadily from 3.60% in Q3 2024 to 3.24% in Q3 2025, reflecting the challenging interest rate environment. Despite this compression, net interest income showed modest growth, partially supported by the acquisition of the SLS leasing portfolio.

The following chart details the evolution of the bank's net interest income and margin:

Cost-to-income ratio increased to 46.1% for the first nine months of 2025, compared to 43.1% in the same period of 2024, indicating some pressure on operational efficiency. The bank's cost of risk remained low at 9 basis points for the first nine months of 2025, compared to -12 basis points in the same period of 2024.

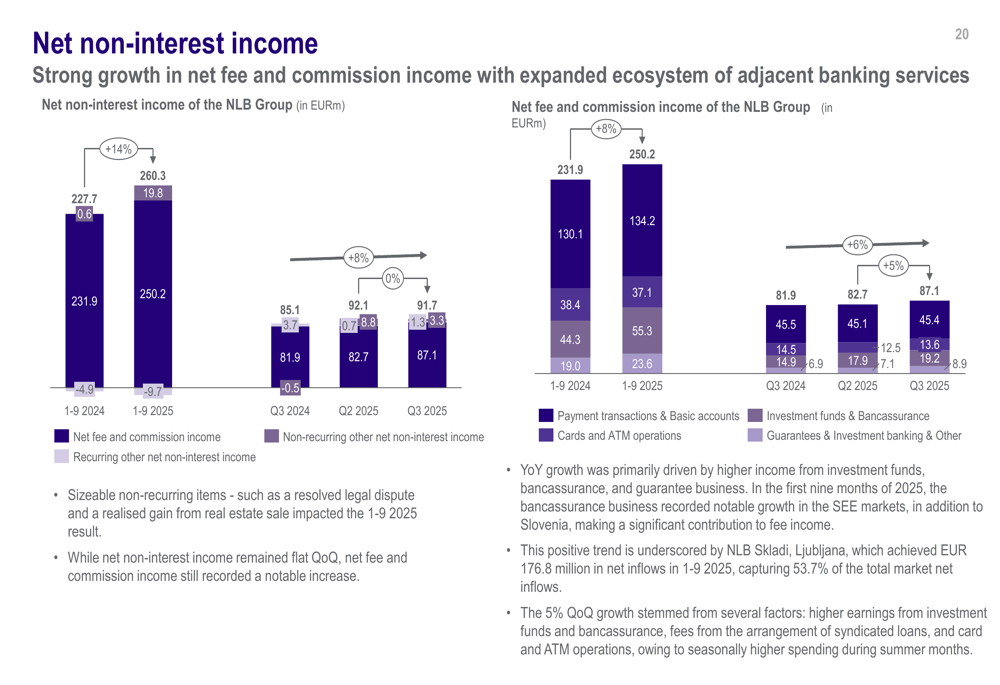

A bright spot in the financial performance was the growth in fee and commission income, which increased by 8% year-over-year according to the earnings call. This growth was primarily driven by higher income from investment funds, bancassurance, and guarantee business, with NLB Skladi (the group's asset management arm) capturing a significant portion of market net inflows.

The breakdown of non-interest income components is shown in the following chart:

The bank's operating income performance remained resilient despite various headwinds, as illustrated in this comprehensive breakdown:

Strategic Initiatives & Regional Positioning

NLB Group continues to pursue its digital transformation strategy, with digital penetration reaching 60% toward a goal of 80% by 2030. During the earnings call, management highlighted new mobile app launches and the introduction of Apple Pay as key digital initiatives.

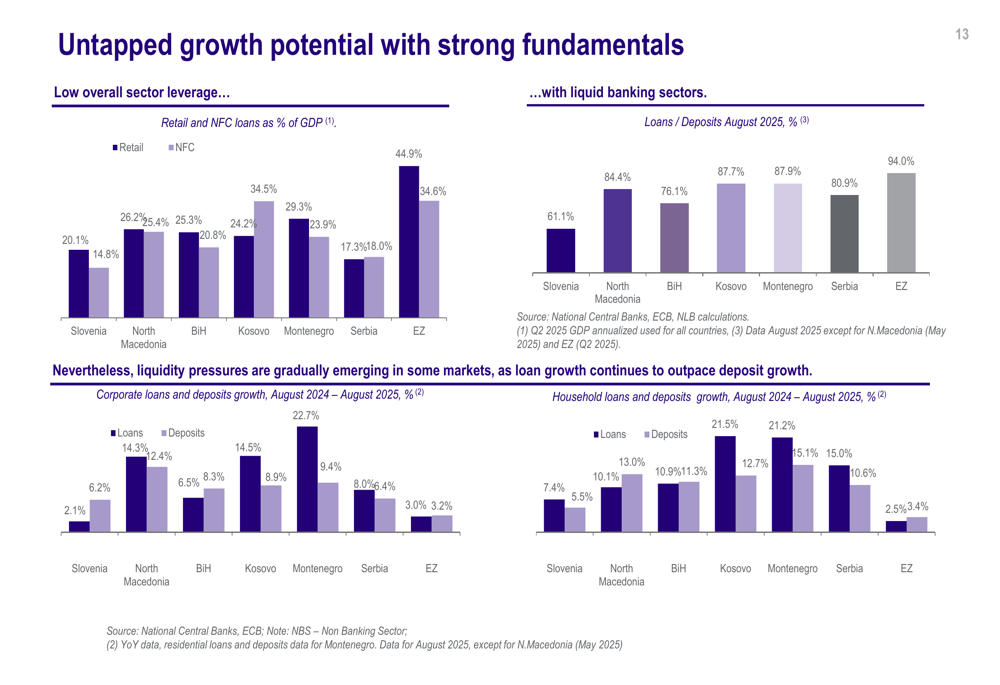

The bank maintains strong market positions across its core territories, with particularly dominant shares in Slovenia (33.0%), Republic of Srpska (21.4%), and Kosovo (17.6%). This regional diversification provides both stability and growth opportunities, as many of these markets remain underpenetrated compared to Western European standards.

The following chart illustrates the untapped growth potential in NLB's markets:

The regional economic environment continues to support NLB's growth strategy, with GDP growth rates in Southeast Europe generally exceeding Eurozone averages:

Forward-Looking Statements

NLB Group paid its first dividend tranche of €6.43 per share in June 2025 and has proposed a second tranche, reflecting its commitment to shareholder returns. The bank maintains a strong capital position with a Tier 1 ratio of 15%, providing flexibility for both organic growth and potential acquisitions.

Management expressed a positive outlook during the earnings call, projecting high single-digit revenue growth and continued low double-digit loan growth. The bank is exploring potential M&A opportunities in the region, particularly in Croatia, Albania, and Bosnia, while also planning expansion into insurance, fleet management, and leasing.

Challenges acknowledged by management include slower growth in Slovenia due to industrial challenges, potential regulatory actions in Serbia, and macroeconomic pressures in Central and Western Europe that may affect regional growth. Despite these headwinds, NLB's diversified regional presence and ongoing digital transformation position it well for continued growth in the medium term.

The bank's credit profile has improved, with S&P upgrading NLB to BBB+ with a stable outlook in June 2025, while Moody's maintains an A3 rating with a positive outlook, reflecting the group's strengthening financial position and regional importance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.