TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Nokia Corporation (HEL:NOKIA) presented its third-quarter 2025 financial results on October 23, showing solid performance with 9% year-over-year net sales growth despite ongoing margin pressures. The telecommunications equipment provider’s stock surged 8.43% following the announcement, as the company beat earnings expectations with an EPS of $0.06 versus the forecasted $0.0495, representing a 21.21% positive surprise.

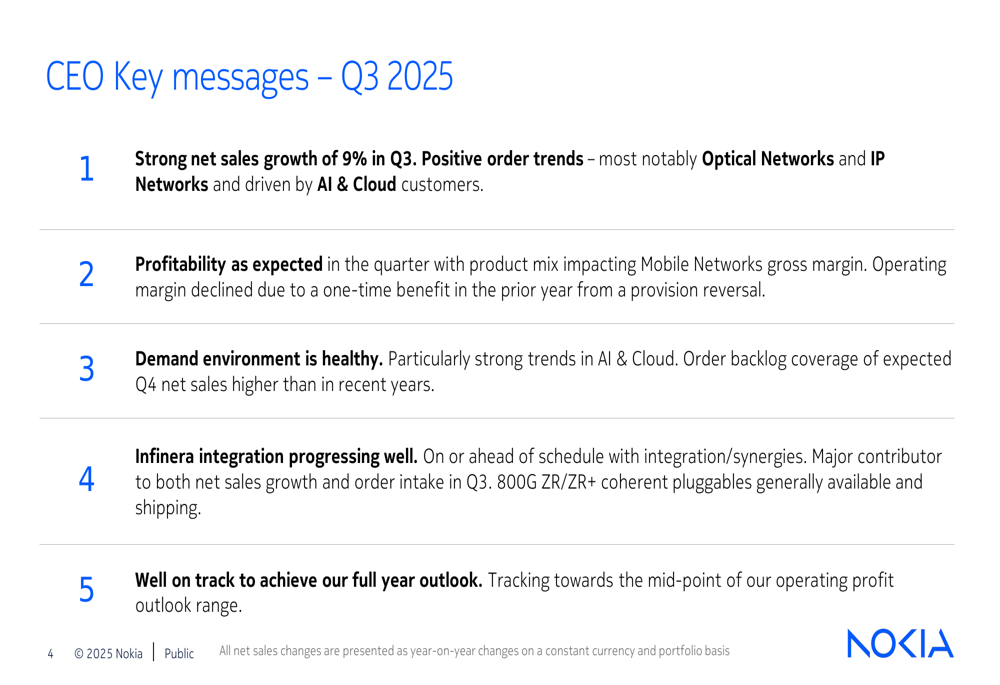

CEO Justin Hotard emphasized the company’s strategic positioning in the growing AI market, stating, "The AI supercycle is accelerating demand for providers of advanced and trusted connectivity." This focus on AI and cloud infrastructure is becoming increasingly central to Nokia’s growth strategy as traditional telecom equipment markets face stabilization.

Quarterly Performance Highlights

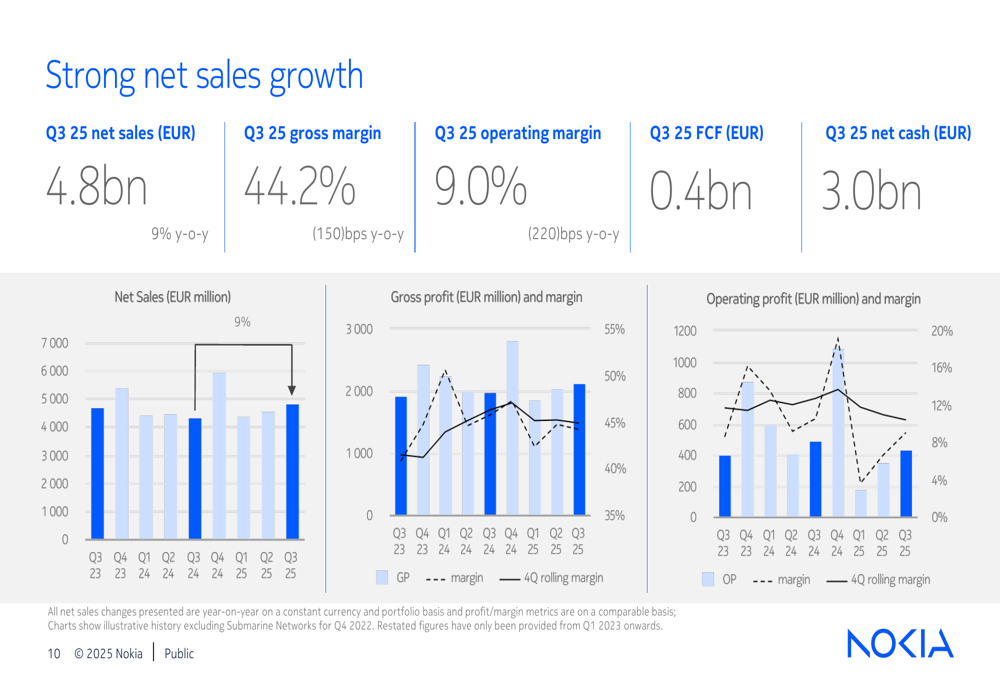

Nokia reported strong Q3 2025 financial results with net sales reaching €4.8 billion, representing 9% year-over-year growth on a constant currency and portfolio basis. However, profitability metrics showed some pressure, with gross margin declining 150 basis points to 44.2% and operating margin falling 220 basis points to 9.0% compared to the same period last year.

As shown in the following chart of Nokia’s quarterly performance:

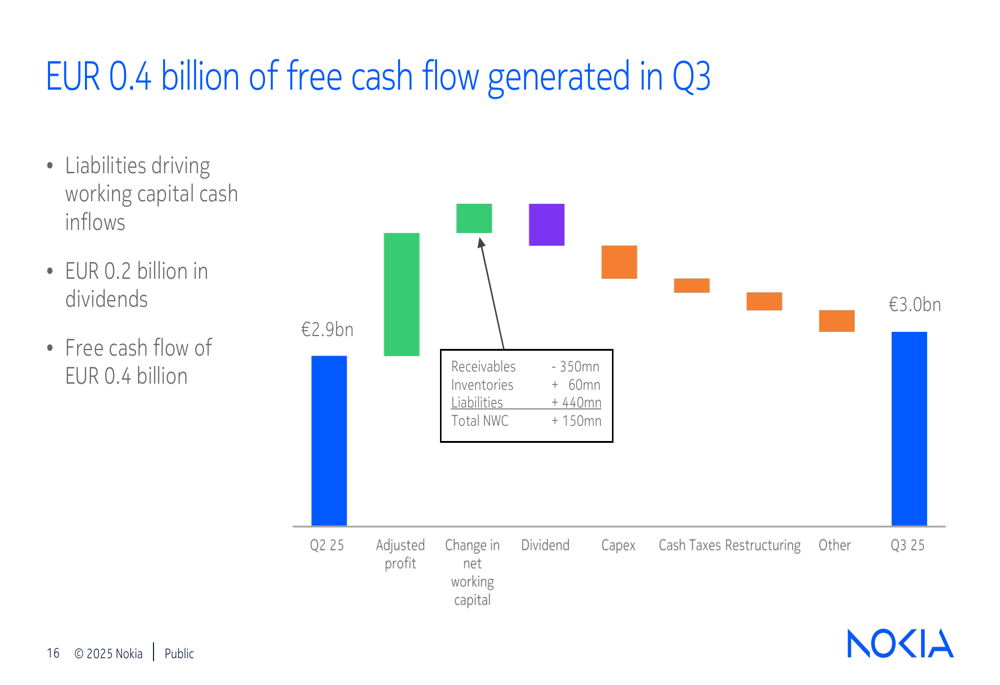

The company generated €0.4 billion in free cash flow during the quarter, maintaining a solid net cash position of €3.0 billion. This performance was primarily driven by working capital improvements, particularly from liabilities, as illustrated in this cash flow breakdown:

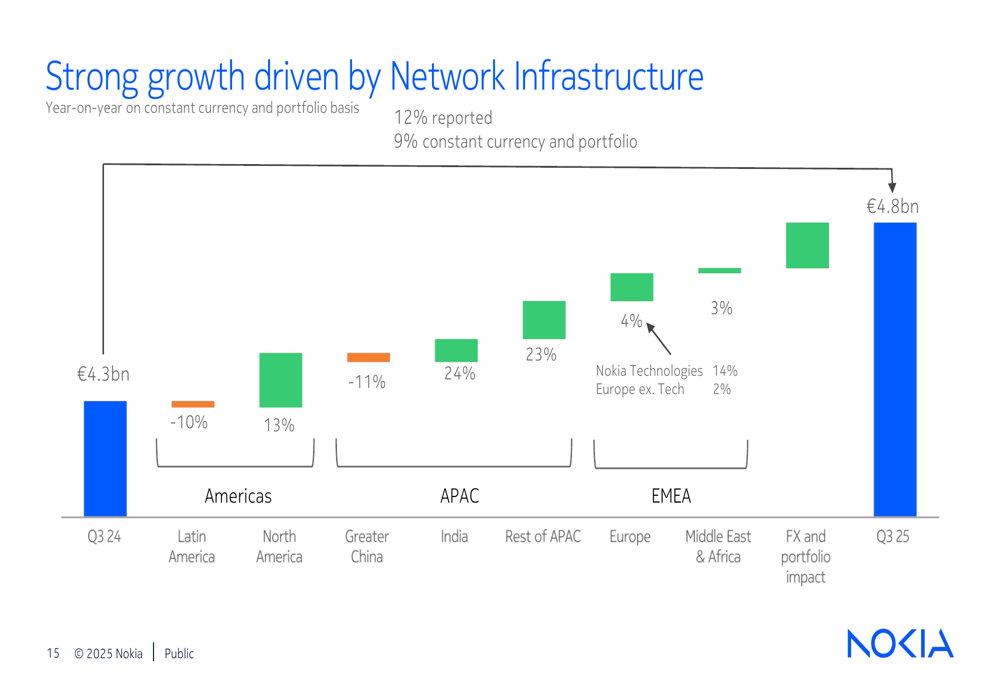

Regional performance varied significantly, with India (24%) and Rest of APAC (23%) showing the strongest growth, while North America grew 13%. Conversely, Latin America declined by 10% and Greater China fell by 11%, as shown in this geographic breakdown:

Segment Analysis

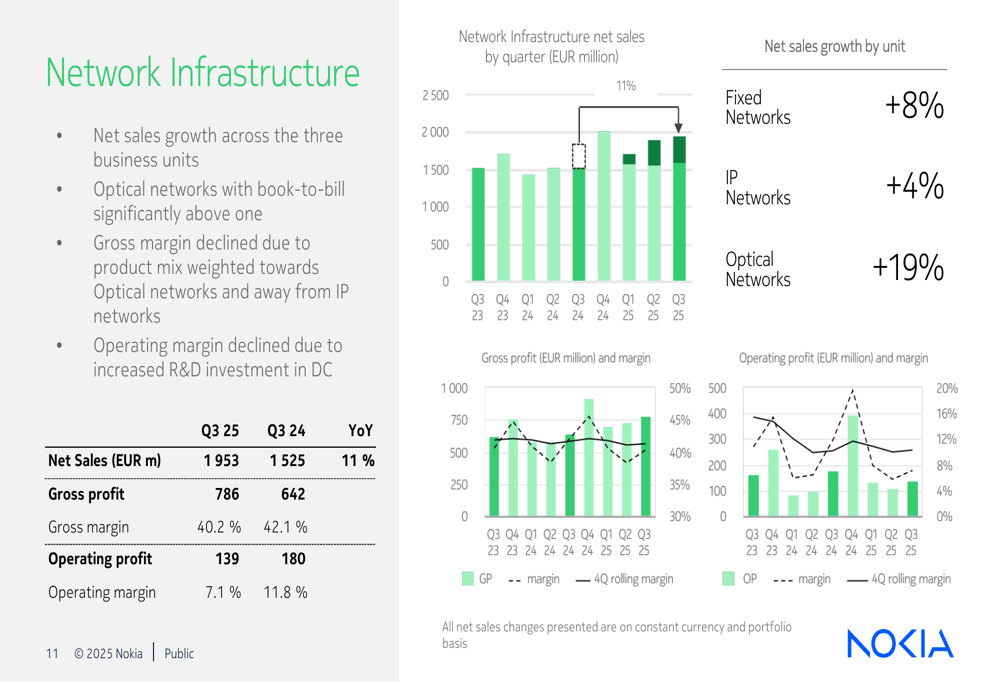

Network Infrastructure emerged as Nokia’s strongest performer, with sales growing 11% year-over-year to €1,953 million, driven by robust demand in Optical Networks. However, both gross margin and operating margin declined due to product mix and increased R&D investments.

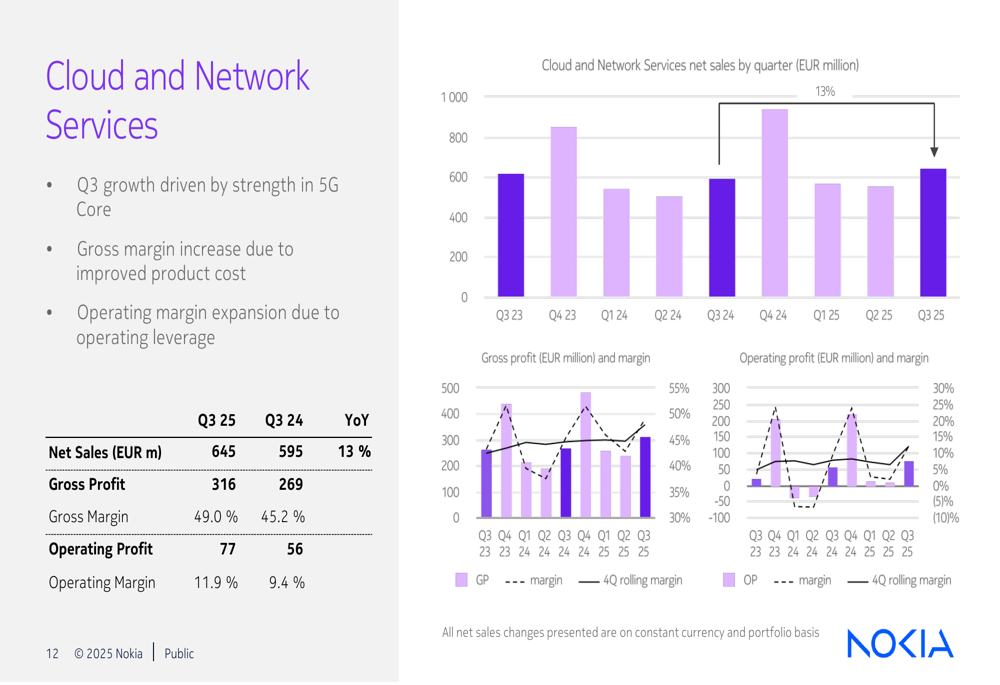

Cloud and Network Services also demonstrated strong momentum with 13% sales growth to €645 million. The segment improved both gross margin and operating profit, benefiting from 5G Core deployments and improved product costs.

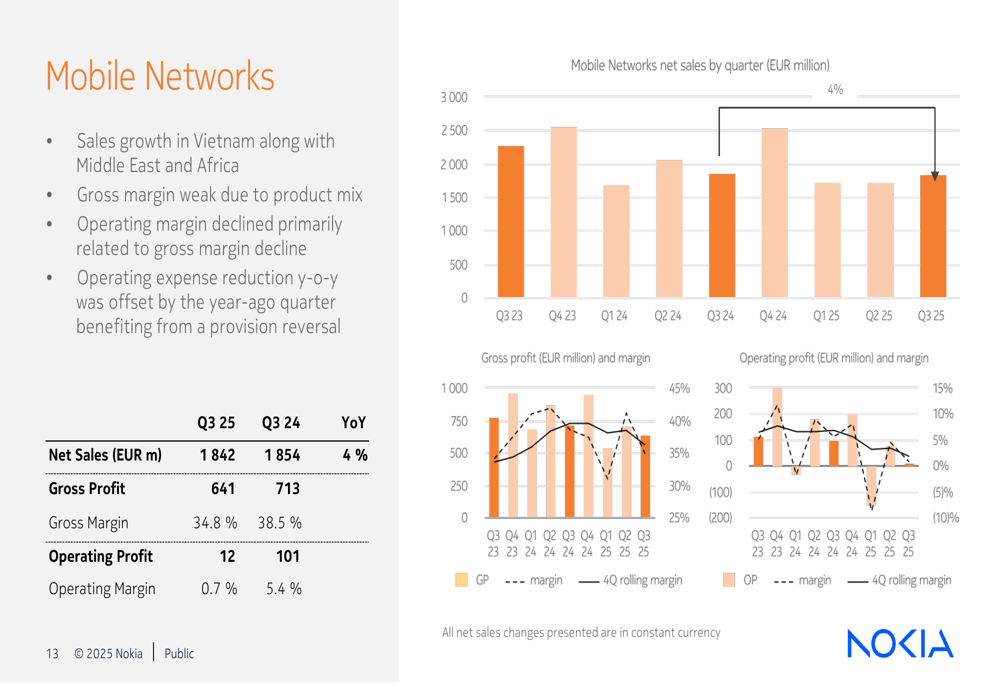

Mobile Networks faced challenges with a 4% sales decline to €1,842 million. More concerning was the significant drop in operating profit to just €12 million from €101 million a year earlier, primarily due to unfavorable product mix.

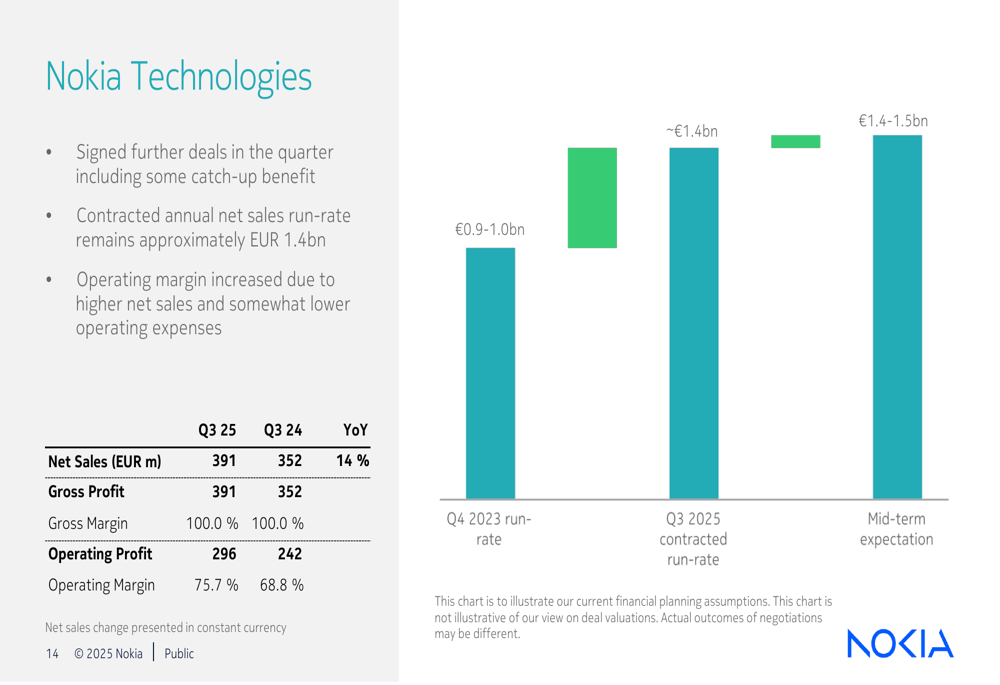

Nokia Technologies, the company’s licensing business, delivered 14% growth to €391 million with an impressive operating margin of 75.7%, up from 68.8% in Q3 2024.

Strategic Initiatives

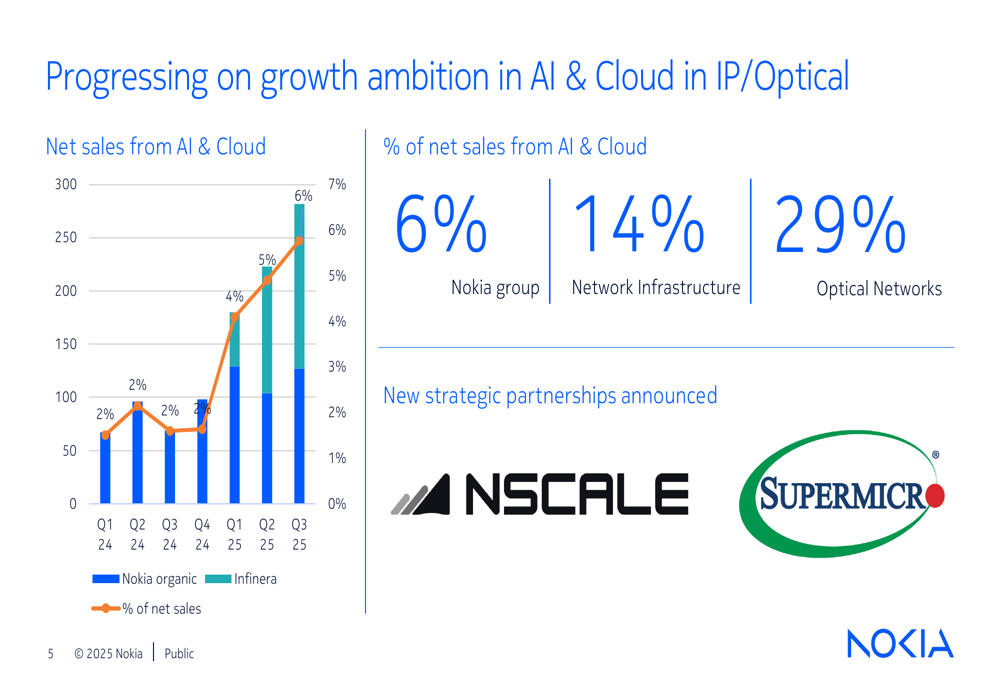

Nokia is strategically focusing on AI and cloud infrastructure opportunities, particularly in IP and Optical Networks. The company reported that AI & Cloud now represents 6% of Nokia Group net sales, 14% of Network Infrastructure, and 29% of Optical Networks.

As illustrated in this strategic growth chart:

The company also unveiled a new 50G PON solution for enterprise connectivity, featuring massive capacity with up to 50Gb/s downstream and upstream capabilities, enhanced security features, and improved availability through redundant components.

Nokia announced a significant win with Vodafone Three, marking its re-entry as a RAN supplier to the operator. Under this agreement, Nokia will supply approximately 7,000 sites while maintaining its core network position.

CEO Justin Hotard highlighted in his key messages that the Infinera integration is progressing well, contributing to both net sales growth and order intake, with 800G ZR/ZR+ pluggables now generally available.

Outlook & Forward Guidance

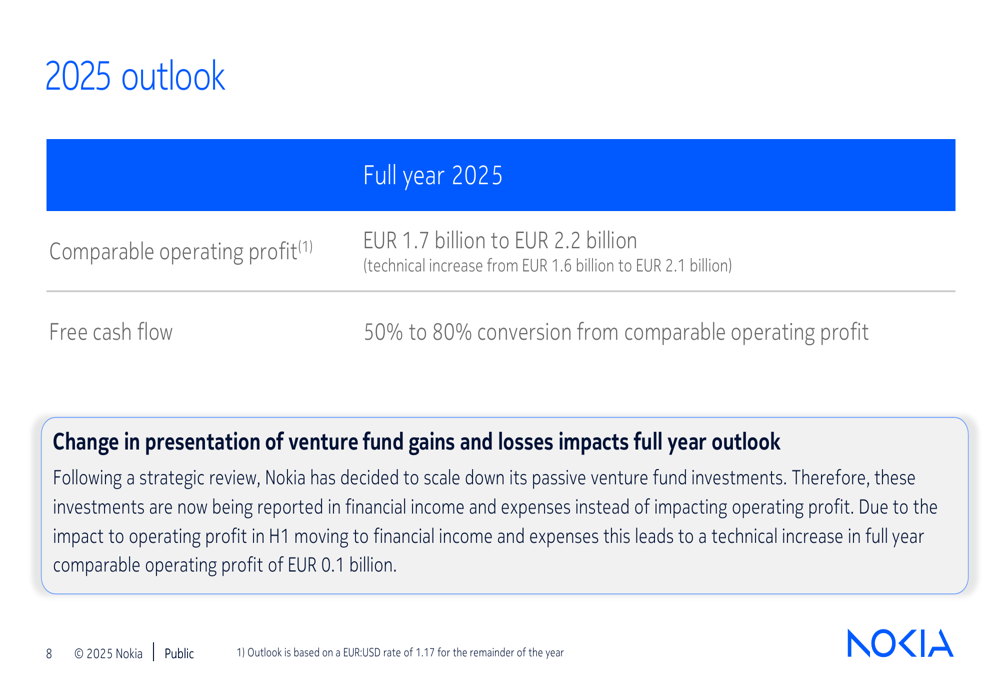

Nokia maintained its 2025 outlook with comparable operating profit expected to be between €1.7 billion and €2.2 billion, representing a technical increase from the previous range of €1.6-2.1 billion. The company expects free cash flow conversion of 50% to 80% from comparable operating profit.

Management indicated they are tracking toward the midpoint of the operating profit outlook range, with a healthy demand environment particularly in AI & Cloud. Order backlog is reported to cover expected Q4 net sales better than in recent years.

CFO Marco Wirén emphasized a shift in approach, stating, "We want to avoid these large-scale restructuring programs going forward," indicating a preference for continuous improvement over major restructuring initiatives.

Nokia also announced its upcoming Capital Markets Day scheduled for November 19, 2025, in New York, where it is expected to provide more details on its long-term strategy and 6G standardization investments.

With its stock trading near its 52-week high of €5.30 following the earnings release, Nokia appears well-positioned to capitalize on growing demand for advanced connectivity solutions, particularly as AI infrastructure deployment accelerates globally.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.