US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Nordic Aqua Partners (OB:NOAP) resumed commercial sales in mid-February 2025 after implementing corrective measures to address previous challenges, according to the company’s Q1 2025 presentation delivered on May 15, 2025. The land-based salmon producer reported revenue of €2.3 million for the quarter, marking a significant improvement from zero revenue in the same period last year.

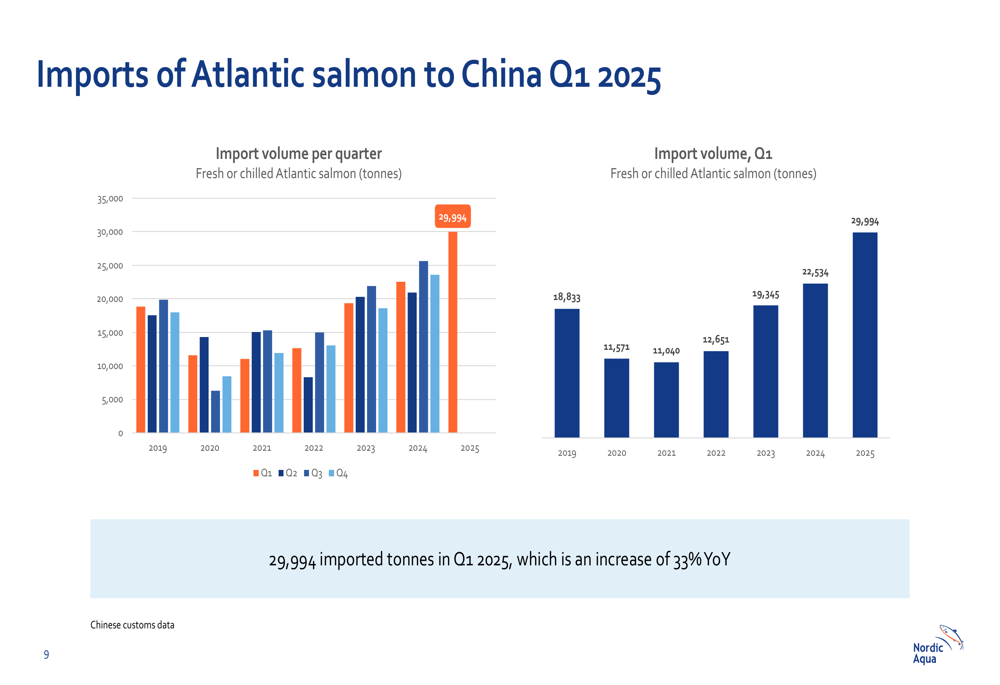

The company is operating in a growing Chinese salmon market, with imports of Atlantic salmon to China reaching 29,994 tonnes in Q1 2025, representing a 33% year-over-year increase. Norway remains the dominant supplier, increasing its import volumes to China by 77% to 16,069 tonnes in Q1 2025 and capturing 56% market share.

As shown in the following chart of Atlantic salmon imports to China:

Quarterly Performance Highlights

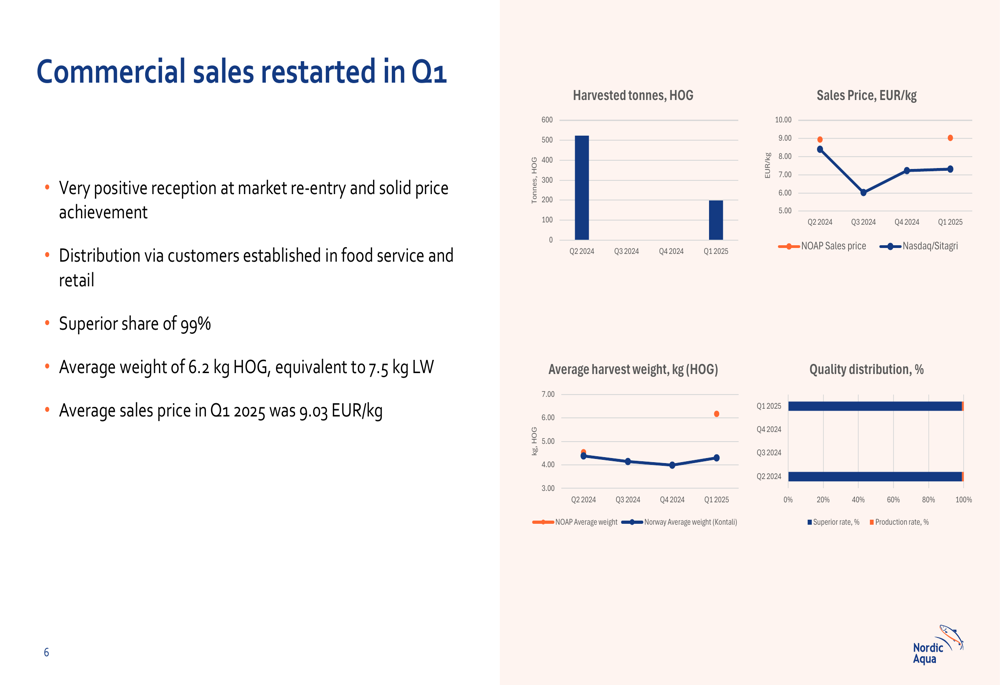

Nordic Aqua harvested approximately 200 tonnes (head-on gutted) during Q1 2025, with an average weight of 6.2 kg HOG, equivalent to 7.5 kg live weight. The company reported a superior share of 99% for its harvested fish, indicating high quality production.

The company’s commercial restart showed positive results with an average sales price of 9.03 EUR/kg in Q1 2025. Sales totaled €2.3 million, with €1.8 million from commercial sales and €0.5 million from non-core markets.

The following chart illustrates key commercial metrics including harvested volumes, sales prices, and quality distribution:

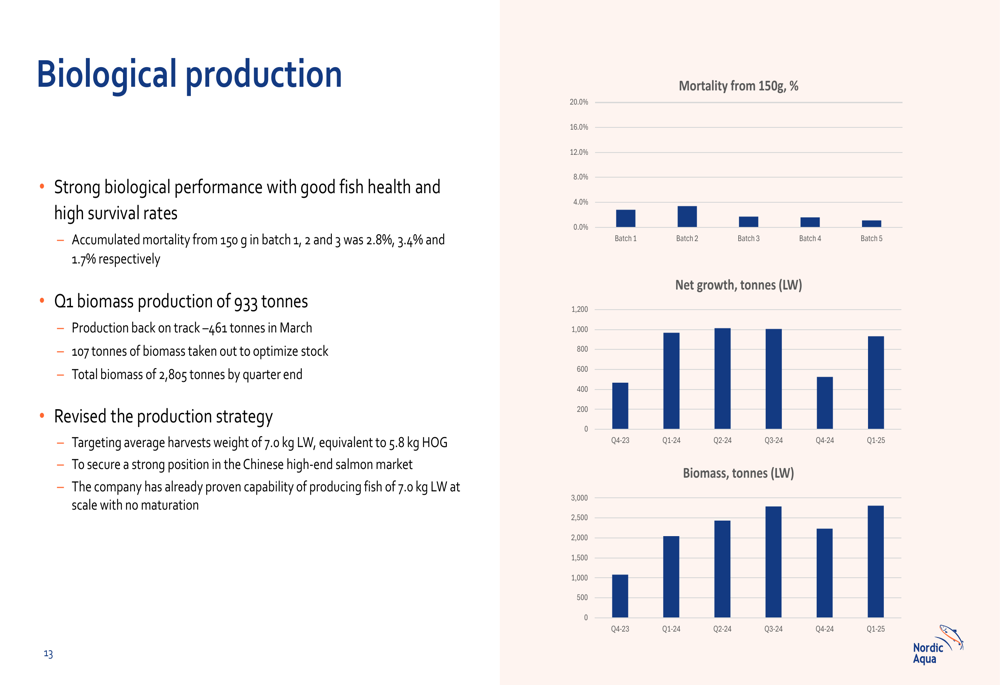

Nordic Aqua reported strong biological performance with good fish health and high survival rates. Accumulated mortality from 150g in batches 1, 2, and 3 was 2.8%, 3.4%, and 1.7% respectively. Q1 biomass production reached 933 tonnes, with total biomass of 2,805 tonnes by quarter end.

The biological production metrics are illustrated in the following charts:

Detailed Financial Analysis

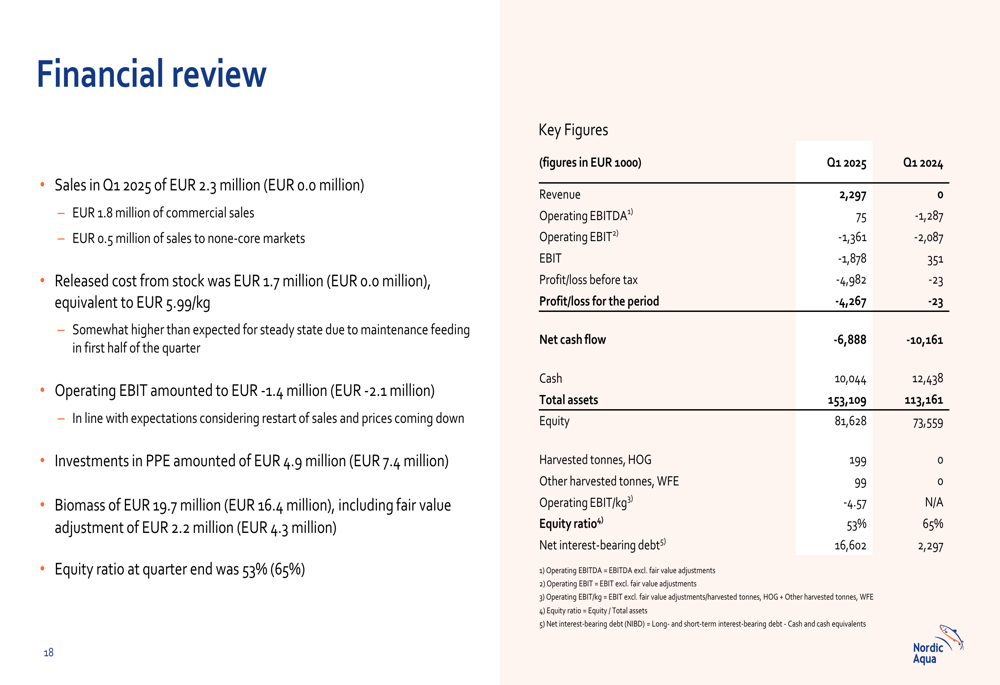

Despite the return to sales, Nordic Aqua continued to report losses in Q1 2025. The company posted an operating EBIT of -€1.4 million, an improvement from -€2.1 million in Q1 2024. Operating EBIT per kg was -4.57 EUR.

Released cost from stock was €1.7 million, equivalent to €5.99/kg, which the company noted was "somewhat higher than expected for steady state due to maintenance feeding in first half of the quarter."

The comprehensive financial results are shown in the following table:

Net financial expenses increased significantly to €3.1 million in Q1 2025 compared to €0.4 million in Q1 2024, contributing to a loss for the period of €4.3 million, compared to a minimal loss of €23,000 in Q1 2024.

The company’s balance sheet showed total assets of €153.1 million, with biomass valued at €19.7 million including fair value adjustment. The equity ratio decreased to 53% from 65% in the same period last year, while net interest-bearing debt increased to €16.6 million from €2.3 million.

Strategic Initiatives & Expansion

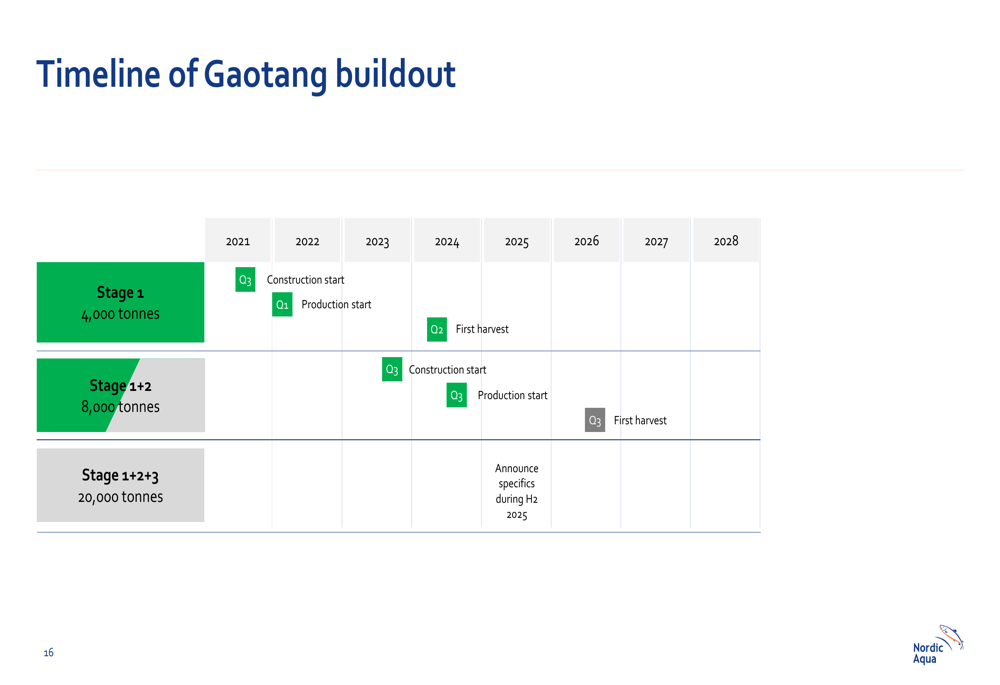

Nordic Aqua continues to advance its expansion plans, with Stage 2 construction progressing on schedule. The company completed its first inlay of eggs for Stage 2 in Q3 2024 and remains on track for the first harvest in Q3 2026.

The company estimates total CAPEX for Stage 2 at €77 million, including €63 million for farming technology and €14 million in improvement capex for off-flavor handling. As of Q1 2025, €22 million had been accrued.

The timeline for the company’s expansion plans is illustrated below:

To support its growth, Nordic Aqua signed a Strategic Cooperation Agreement with Bank of China in November 2024 and secured a short-term credit facility of €13 million in April 2025 to provide bridge funding.

Forward-Looking Statements

Nordic Aqua has revised its production strategy to target an average harvest weight of 7.0 kg live weight, noting that the company "has already proven capability of producing fish of 7.0 kg LW at scale with no maturation."

The company expects a full-year 2025 harvest of 3,000 tonnes HOG. Stage 2 is on schedule to double production capacity to 8,000 tonnes, with first harvest expected in Q3 2026.

Nordic Aqua continues to emphasize its competitive advantages in the Chinese market, highlighting its value proposition based on freshness, safety, sustainability, and agility as the only high-quality, continuously supplied Atlantic Salmon produced in China.

As summarized in the company’s outlook:

While Nordic Aqua shows signs of operational improvement with the resumption of sales and better biological performance, the company continues to face financial challenges with ongoing losses and increasing debt. The success of its expansion plans and ability to achieve profitability will be critical factors for investors to monitor in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.