Intel stock spikes after report of possible US government stake

Introduction & Market Context

Northeast Bancorp (NASDAQ:NBN) released its fourth quarter fiscal year 2025 presentation on July 29, revealing strong financial performance with net income reaching $25.2 million, a significant increase from the $15.1 million reported in the same quarter last year. The bank’s stock responded positively, trading up 2.81% at the time of the presentation, with premarket activity showing even stronger gains of 3.42%.

The presentation comes after a mixed first quarter 2025 performance where NBN missed EPS expectations but exceeded revenue forecasts. The bank continues to position itself as a specialized lender with a focus on low loan-to-value (LTV) real estate investments and a growing SBA (LON:SBA) loan business.

Quarterly Performance Highlights

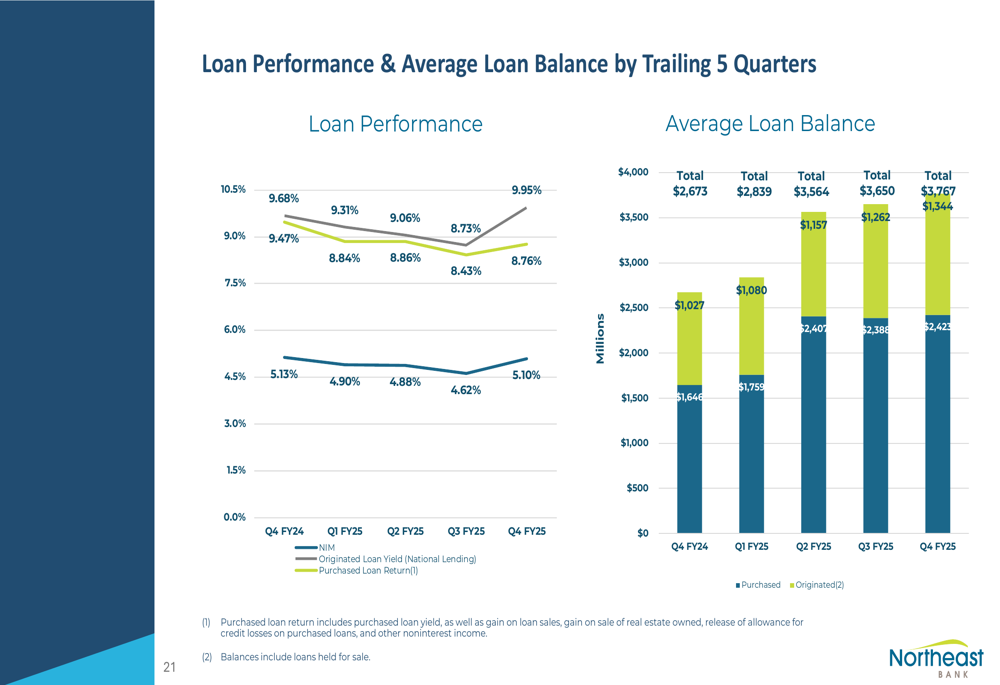

Northeast Bancorp reported basic earnings per share of $3.06 for Q4 FY25, contributing to a full-year EPS of $10.31. Total (EPA:TTEF) loan volume for the quarter reached $362.6 million, with year-to-date volume of $2.1 billion. The bank’s net interest margin expanded to 5.10% in Q4, up from 4.82% for the full year.

As shown in the following financial highlights chart, the bank’s purchased loan return remained strong at 8.76% for the quarter:

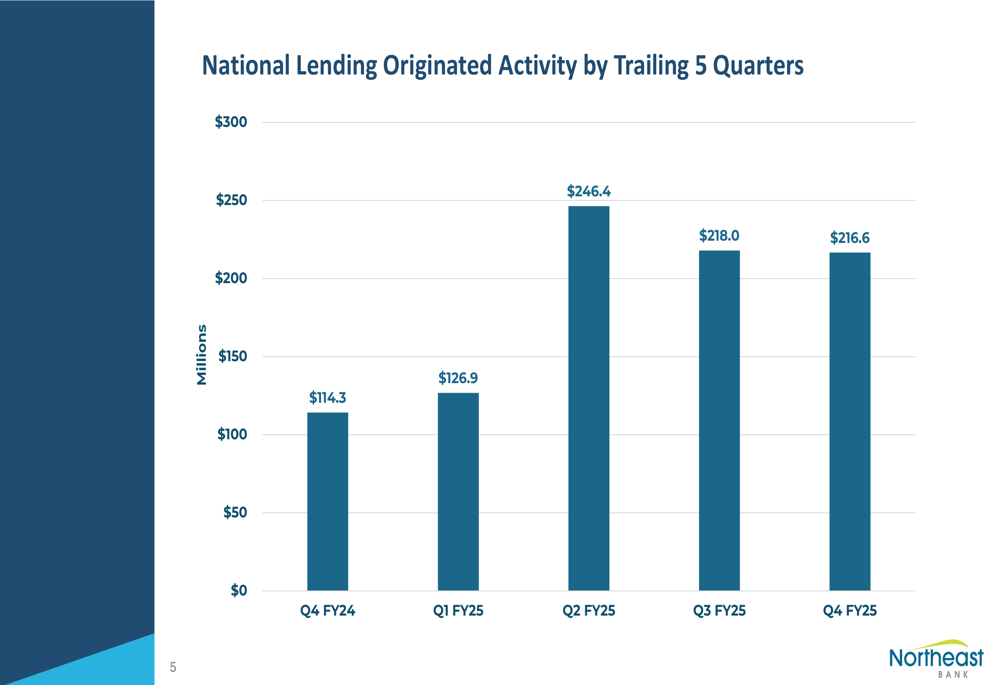

Net income has shown consistent growth over the past five quarters, reaching its highest point in Q4 FY25:

The bank’s revenue components show a healthy mix of interest income and fee-based revenue, with base net interest income growing steadily:

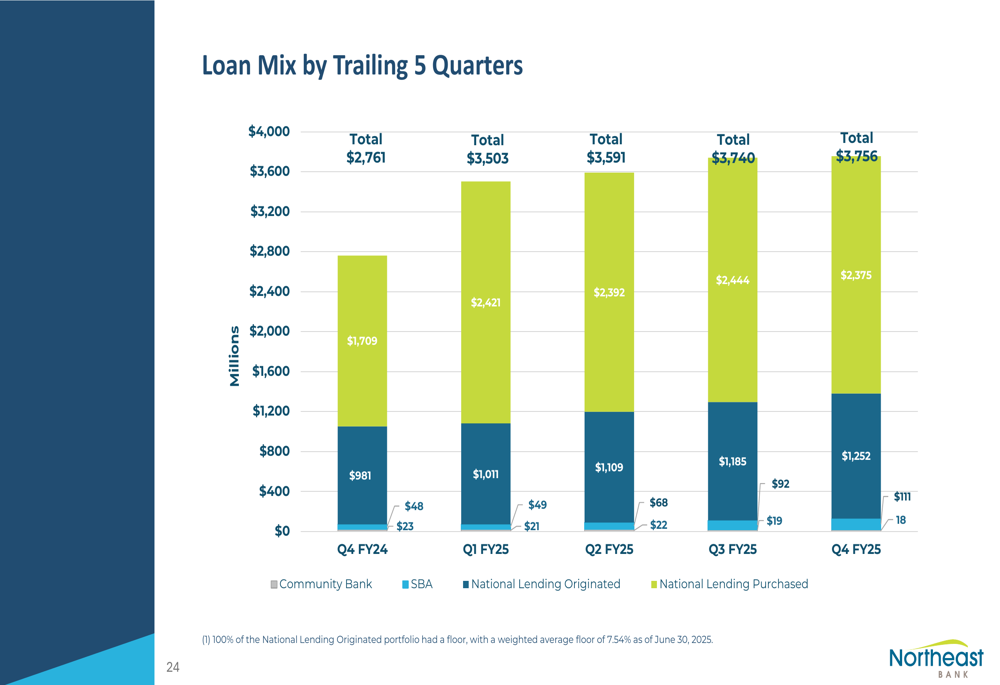

Loan Portfolio Analysis

Northeast Bancorp’s total loan portfolio stood at $3.76 billion as of June 30, 2025, consisting of 8,461 loans with an average balance of $444,000. The portfolio maintains a conservative weighted average loan-to-value ratio of 50%, reflecting the bank’s risk-averse lending approach.

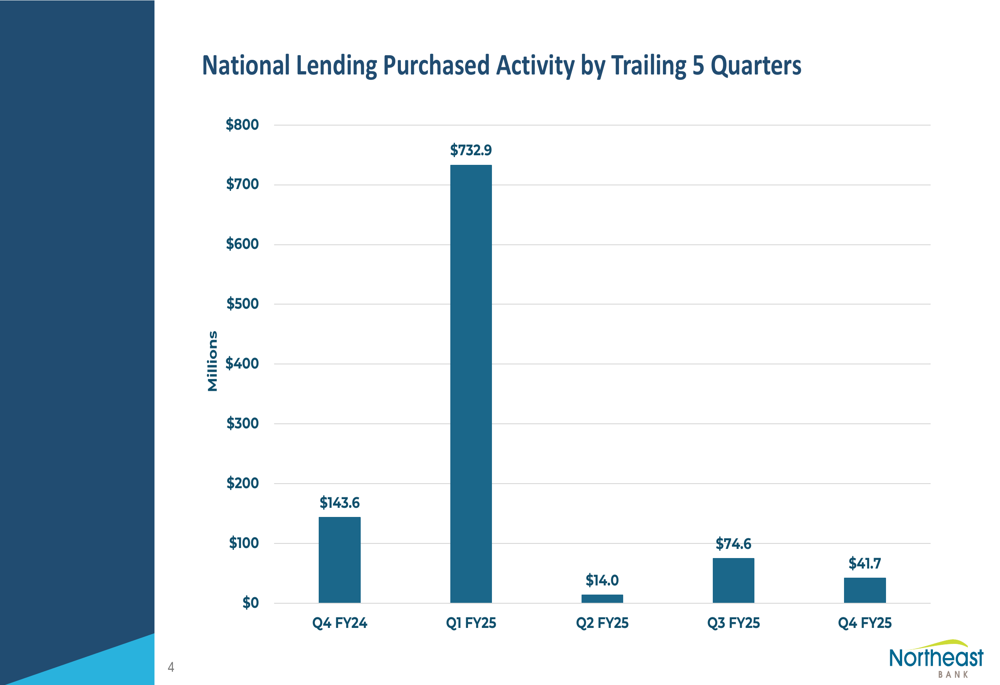

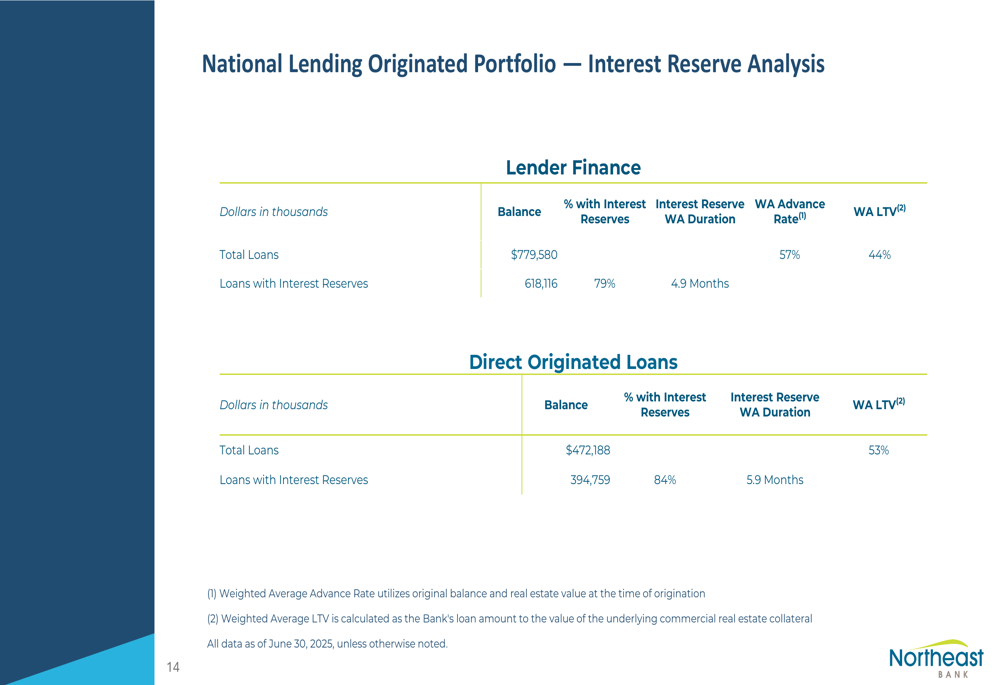

The loan portfolio is divided between the National Lending Division (accounting for 99.5% of total loans) and the Community Banking Division. Within the National Lending segment, purchased loans represent the largest category at $2.38 billion, followed by lender finance loans at $779.6 million and direct originated loans at $472.2 million.

The following chart provides a detailed breakdown of the loan portfolio:

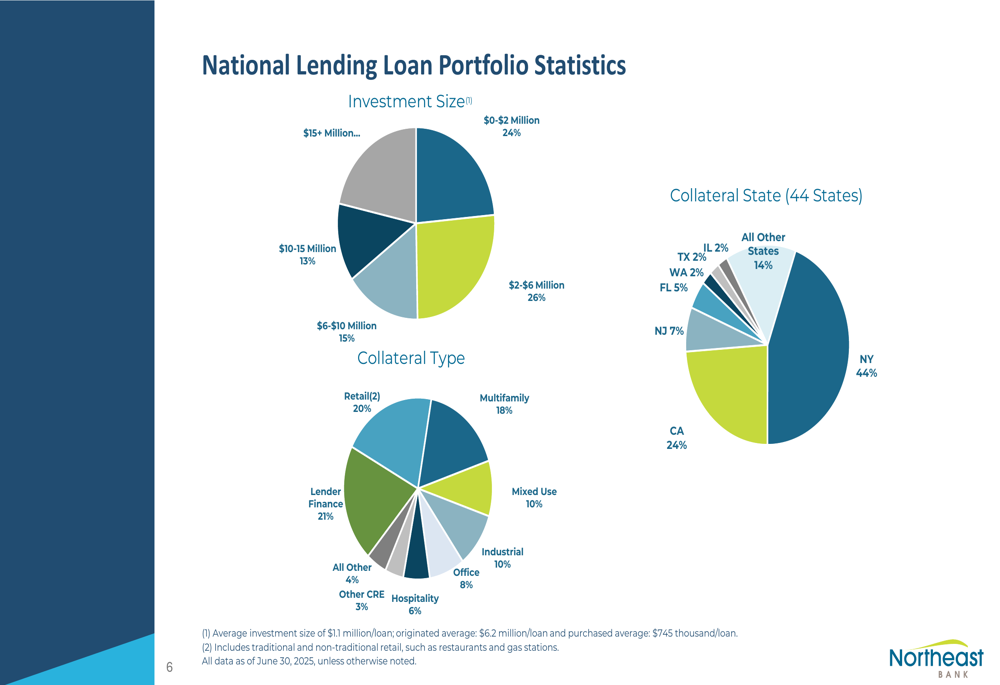

The National Lending portfolio shows significant diversification across collateral types, with multifamily (18%), lender finance (21%), and retail (20%) representing the largest segments. Geographically, the portfolio is heavily concentrated in New York (44%) and California (24%), which may present concentration risk:

Given the bank’s significant exposure to New York City, the presentation specifically addressed its position regarding rent-controlled or rent-stabilized properties:

Asset Quality and Risk Management

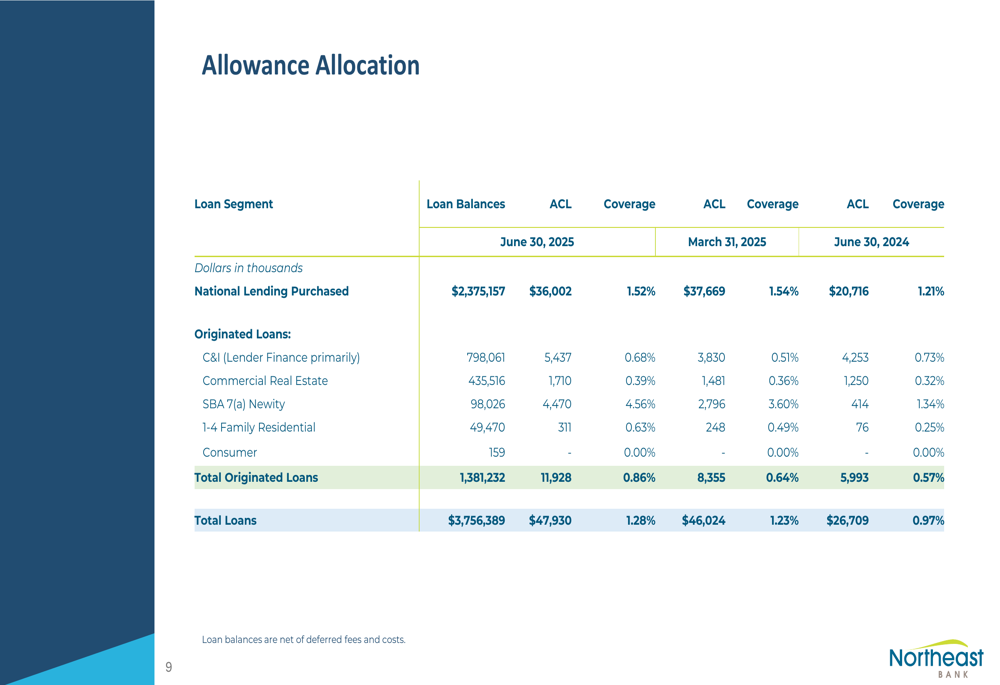

While Northeast Bancorp maintains strong overall performance, the presentation revealed some concerning trends in asset quality metrics. Non-performing loans as a percentage of total loans increased to 0.93% as of June 30, 2025, up from 0.84% in the previous quarter. Similarly, classified commercial loans rose to $32.1 million from $28.6 million in the prior quarter.

The bank has responded by increasing its allowance for credit losses to 1.28% of gross loans, up from 1.23% in the previous quarter and 0.97% a year ago:

The detailed breakdown of nonperforming assets shows additions of $15.26 million during the quarter, partially offset by resolutions of $12.56 million, resulting in a net increase in nonperforming assets:

Deposit Growth and Funding

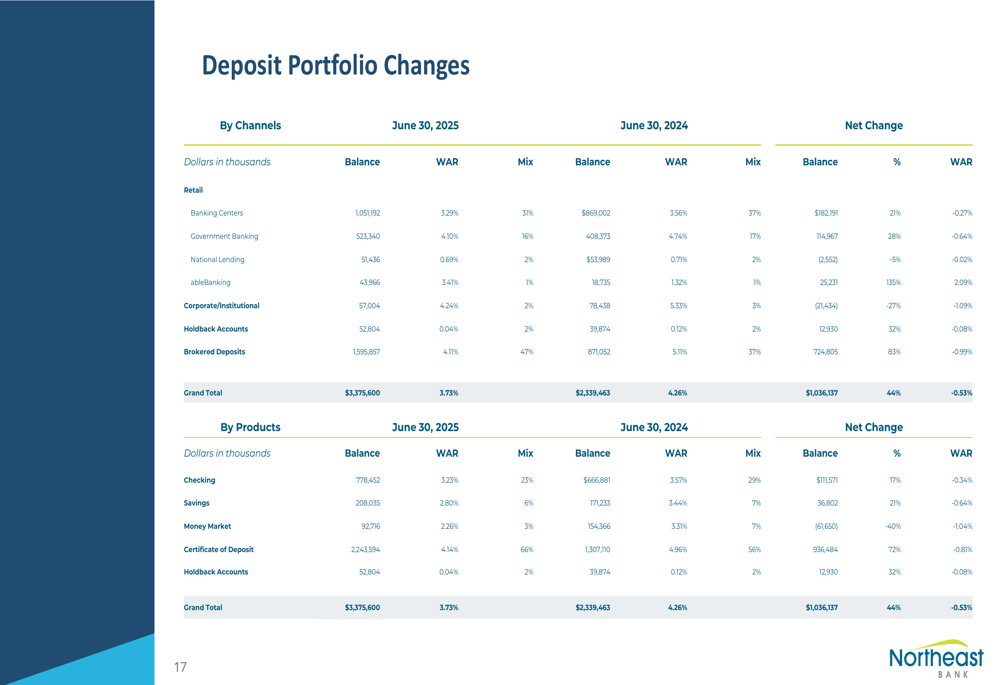

Northeast Bancorp has successfully grown its deposit base while reducing its cost of funds. The average cost of deposits decreased to 3.93% in Q4 FY25 from 4.36% in Q4 FY24, with the period-end cost falling to 3.73%:

The deposit mix has shifted significantly over the past year, with certificates of deposit growing from $1.31 billion to $2.24 billion, while maintaining stable levels of demand and checking accounts:

This deposit growth has supported the bank’s lending activities and contributed to improved net interest margins.

Forward-Looking Statements

Northeast Bancorp appears well-positioned for continued growth despite some emerging asset quality concerns. The bank’s strategic focus on low LTV real estate loans (average 50% LTV across the portfolio) provides a significant cushion against potential market downturns.

The presentation highlighted the bank’s return profile, with regularly scheduled interest and accretion generating 8.65% returns across the National Lending portfolio, supplemented by accelerated accretion and fees from loan payoffs:

While the bank faces challenges from potential further deterioration in asset quality and geographic concentration risk, its conservative underwriting approach and improving cost of funds position it favorably in the current banking environment.

In the recent earnings call, CEO Rick Wayne highlighted the bank’s fee income potential, noting they were "on a run rate making $25,000,000 of fee income," while COO Pat Dignan emphasized their strategic patience and focus on "real estate with low LTVs." These statements align with the presentation’s emphasis on risk-managed growth and diversified revenue streams.

As Northeast Bancorp navigates fiscal year 2026, investors will likely focus on whether the bank can maintain its strong earnings trajectory while managing the emerging asset quality concerns highlighted in this presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.