US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Introduction & Market Context

Northpointe Bancshares Inc. (NPB) released its first quarter 2025 earnings presentation on April 23, highlighting substantial growth in its mortgage purchase program and a significant increase in earnings. The company, which operates primarily through its digital banking platform with just one physical branch in Grand Rapids, reported that its stock closed at $13.13 prior to the earnings release, trading within its 52-week range of $11.43 to $14.98.

The bank’s strategic focus on mortgage banking and digital deposit gathering appears to be yielding results, with earnings up 70% compared to the same quarter last year, despite operating in a competitive banking environment.

Quarterly Performance Highlights

Northpointe reported net income to common stockholders of $15.0 million for Q1 2025, or $0.49 per diluted share, representing a substantial improvement from $8.85 million ($0.34 per share) in Q4 2024 and $9.84 million ($0.38 per share) in Q1 2024.

The company achieved a return on average assets of 1.31% and return on average equity of 13.17%, while maintaining an efficiency ratio of 55.15%. Tangible book value per share reached $14.17, reflecting 14% growth over the prior year.

As shown in the following summary of first quarter highlights:

Mortgage Purchase Program Growth

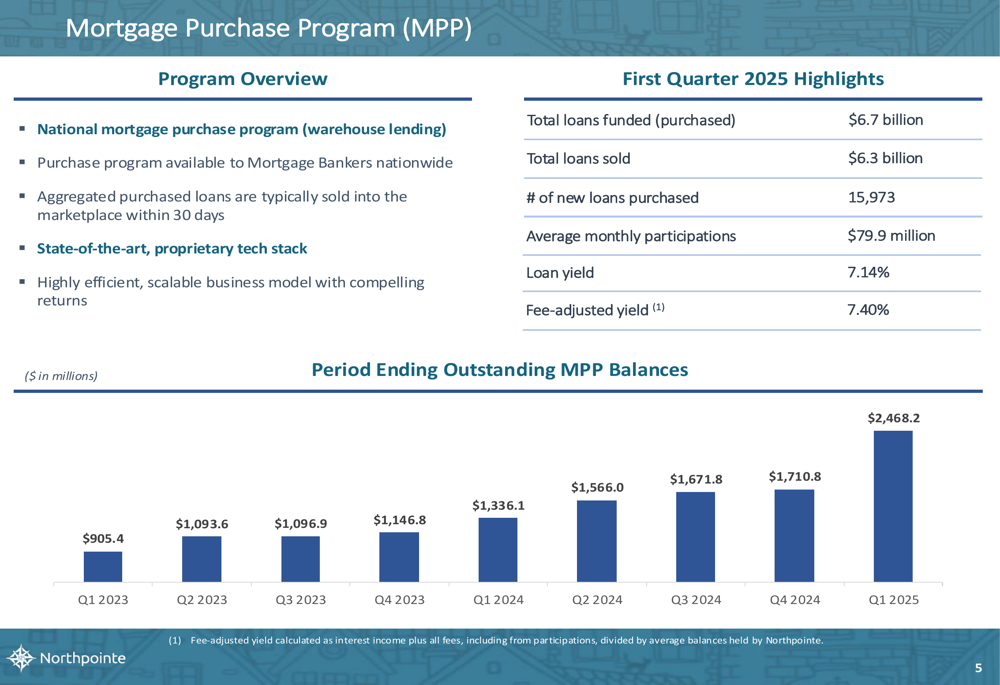

The standout performer for Northpointe continues to be its Mortgage Purchase Program (MPP), which grew by $757.4 million during the quarter, representing an annualized growth rate of 177%. This national mortgage purchase program, available to mortgage bankers nationwide, has become a cornerstone of Northpointe’s business strategy.

During Q1 2025, the MPP funded $6.7 billion in total loans and sold $6.3 billion, purchasing 15,973 new loans. The program generated a loan yield of 7.14% (7.40% on a fee-adjusted basis), providing a significant boost to interest income. The period-ending outstanding MPP balances have grown consistently from $905.4 million in Q1 2023 to $2.47 billion in Q1 2025.

The following chart illustrates the remarkable growth trajectory of the Mortgage Purchase Program:

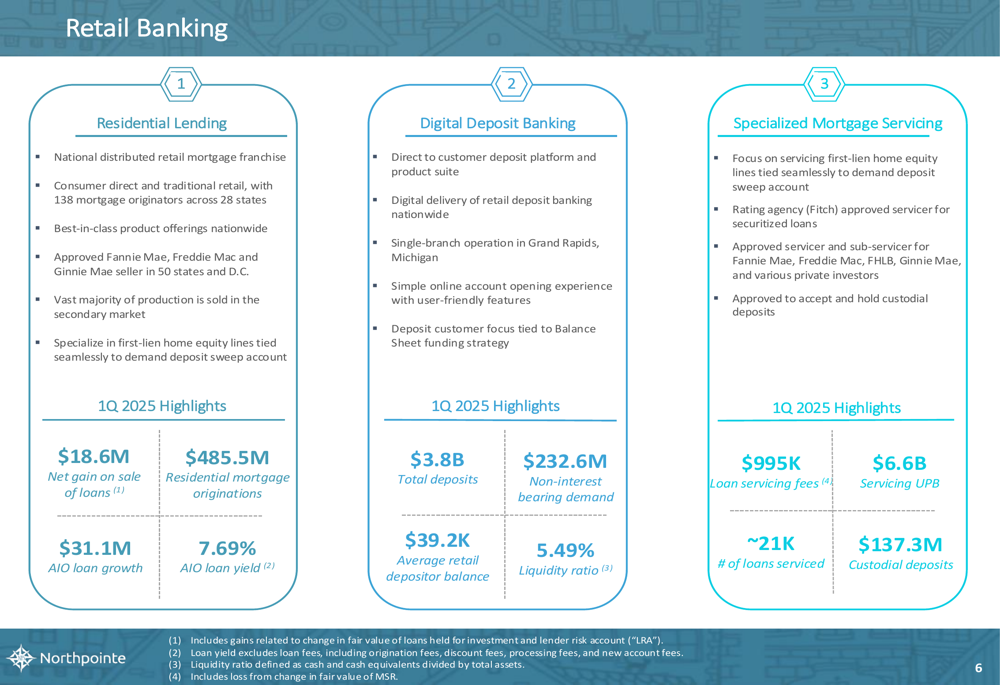

Retail Banking Operations

Northpointe’s retail banking operations are divided into three key areas: Residential Lending, Digital Deposit Banking, and Specialized Mortgage Servicing. The residential lending arm generated $18.6 million in net gain on sale of loans and $485.5 million in residential mortgage originations during the quarter.

The company’s digital deposit platform has accumulated $3.8 billion in total deposits, including $232.6 million in non-interest bearing demand deposits. The average retail depositor balance stands at $39,200, reflecting the company’s focus on attracting substantial deposit relationships despite having just a single physical branch.

The specialized mortgage servicing division is focused on servicing first-lien home equity lines, with approximately 21,000 loans being serviced and $6.6 billion in servicing unpaid principal balance. This generated $995,000 in loan servicing fees during the quarter.

The breakdown of these three business segments is illustrated below:

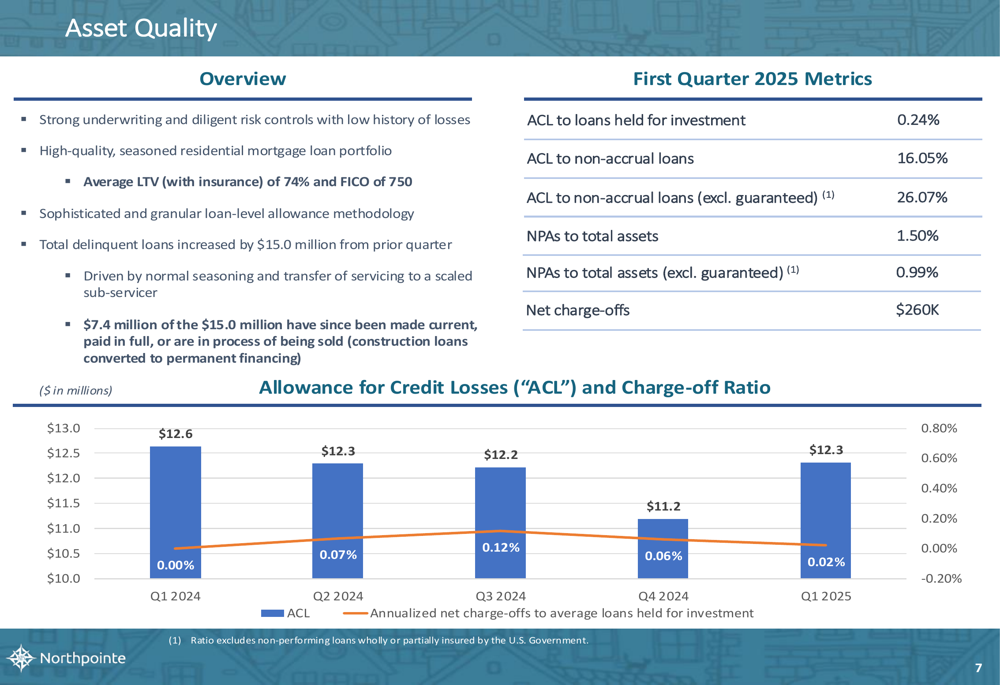

Balance Sheet and Asset Quality

Northpointe’s total assets grew to $5.86 billion as of March 31, 2025, up from $5.22 billion at the end of 2024 and $4.87 billion a year earlier. Total (EPA:TTEF) deposits increased to $3.82 billion, representing annualized growth of 47% from the previous quarter.

The company maintains strong asset quality metrics, with an allowance for credit losses (ACL) to loans held for investment ratio of 0.24%. Non-performing assets to total assets stood at 1.50% (0.99% excluding guaranteed loans), while net charge-offs for the quarter were just $260,000.

The following slide details the company’s asset quality metrics:

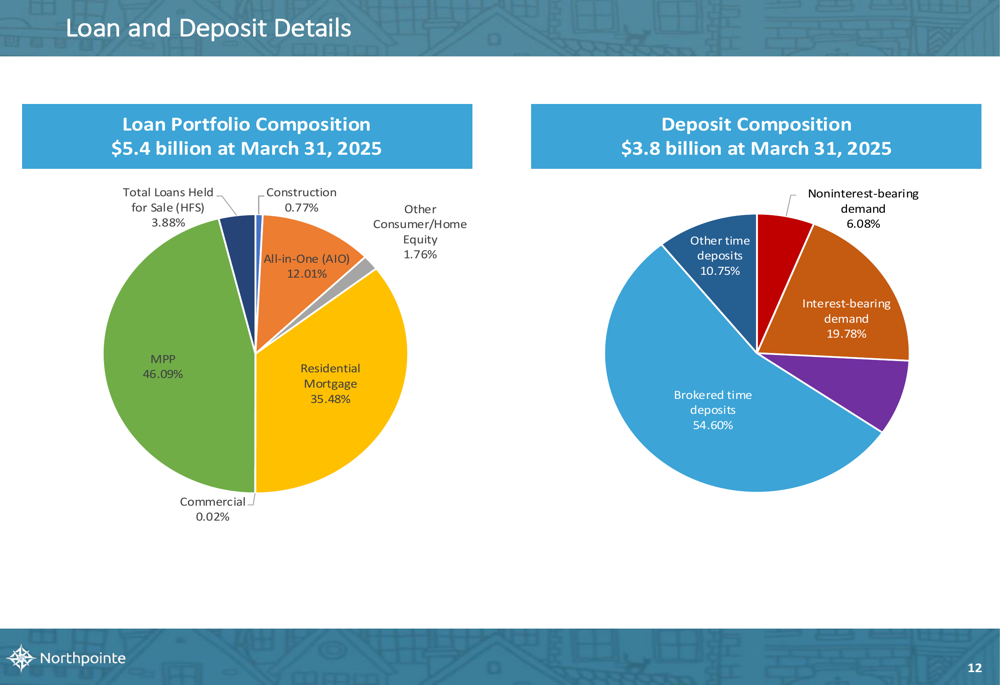

The loan portfolio is predominantly focused on residential mortgages, with the MPP comprising 46.09% of the total loan portfolio, followed by residential mortgages at 35.48% and All-in-One loans at 12.01%. Commercial loans represent just 0.02% of the portfolio, highlighting the company’s specialized focus.

On the deposit side, brokered time deposits make up 54.60% of the total, followed by interest-bearing demand deposits at 19.78% and other time deposits at 10.75%. The deposit composition reflects the company’s digital-first strategy and reliance on wholesale funding sources.

The composition of the loan and deposit portfolios is illustrated in the following pie charts:

Financial Performance Details

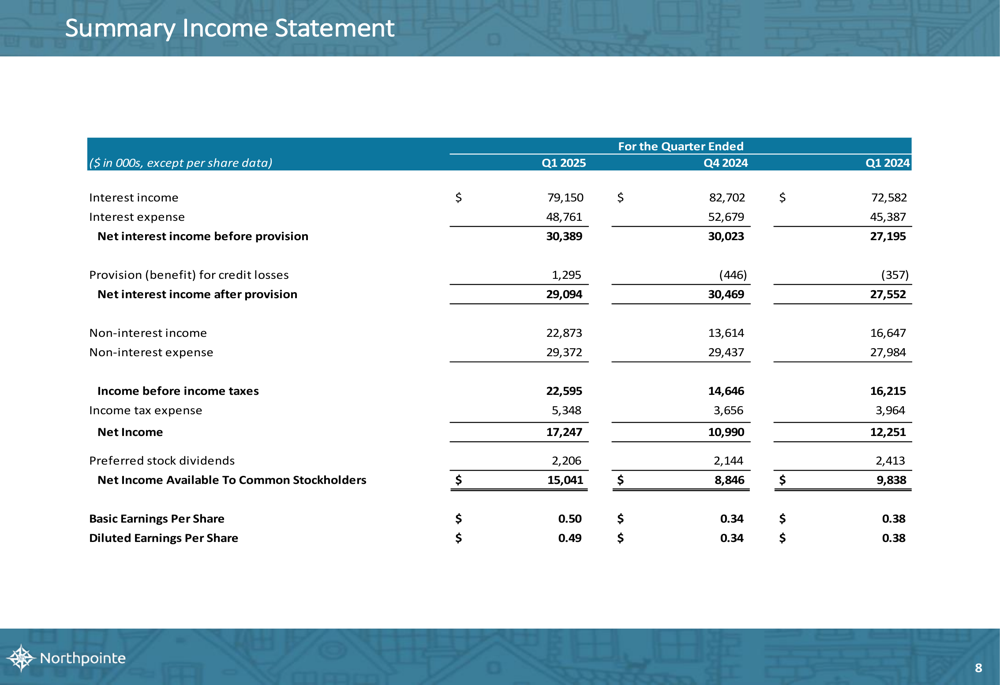

Northpointe’s income statement shows significant improvement in both net interest income and non-interest income. For Q1 2025, interest income was $79.15 million, down slightly from $82.70 million in Q4 2024 but up from $72.58 million in Q1 2024. After accounting for interest expense, net interest income before provision was $30.39 million, a slight increase from $30.02 million in the previous quarter.

Non-interest income surged to $22.87 million in Q1 2025, up from $13.61 million in Q4 2024 and $16.65 million in Q1 2024, contributing significantly to the overall earnings growth. This increase in non-interest income, combined with stable non-interest expenses of $29.37 million, helped drive the improvement in bottom-line results.

The detailed income statement comparison is shown below:

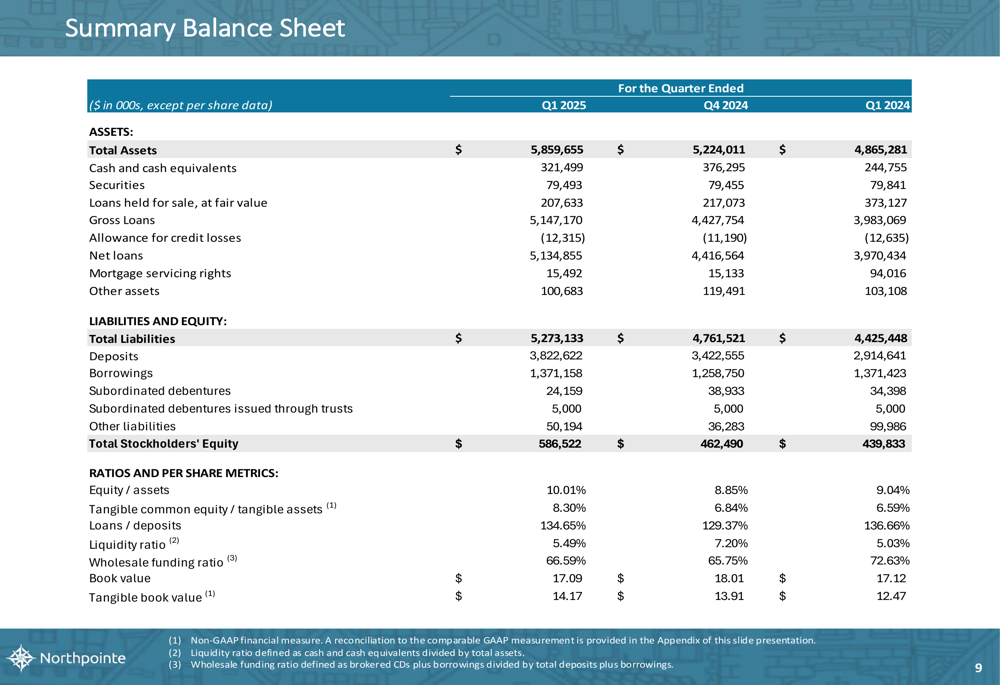

The balance sheet shows continued growth across key metrics. Total assets increased to $5.86 billion, with gross loans growing to $5.15 billion from $4.43 billion in the previous quarter. The equity to assets ratio improved to 10.01%, up from 8.85% in Q4 2024, while the tangible common equity to tangible assets ratio reached 8.30%.

The following slide provides a comprehensive view of the balance sheet:

Capital Position and Outlook

Northpointe maintains strong regulatory capital ratios, with the bank reporting a total capital to risk-weighted assets ratio of 12.16% and a CET1 capital ratio of 11.95%. At the holding company level, Northpointe Bancshares reported a total capital ratio of 12.74% and a CET1 ratio of 9.92%, all well above regulatory requirements.

The company’s strong capital position, combined with its specialized focus on mortgage banking and digital deposit gathering, positions it well for continued growth. The significant expansion of the Mortgage Purchase Program and the consistent growth in deposits suggest that Northpointe’s strategy is gaining traction in the marketplace.

While the company’s stock price has remained relatively stable, trading in the middle of its 52-week range, the substantial improvement in earnings and continued balance sheet growth could potentially lead to increased investor interest if these trends continue in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.