September looms as a risk month for stocks, Yardeni says

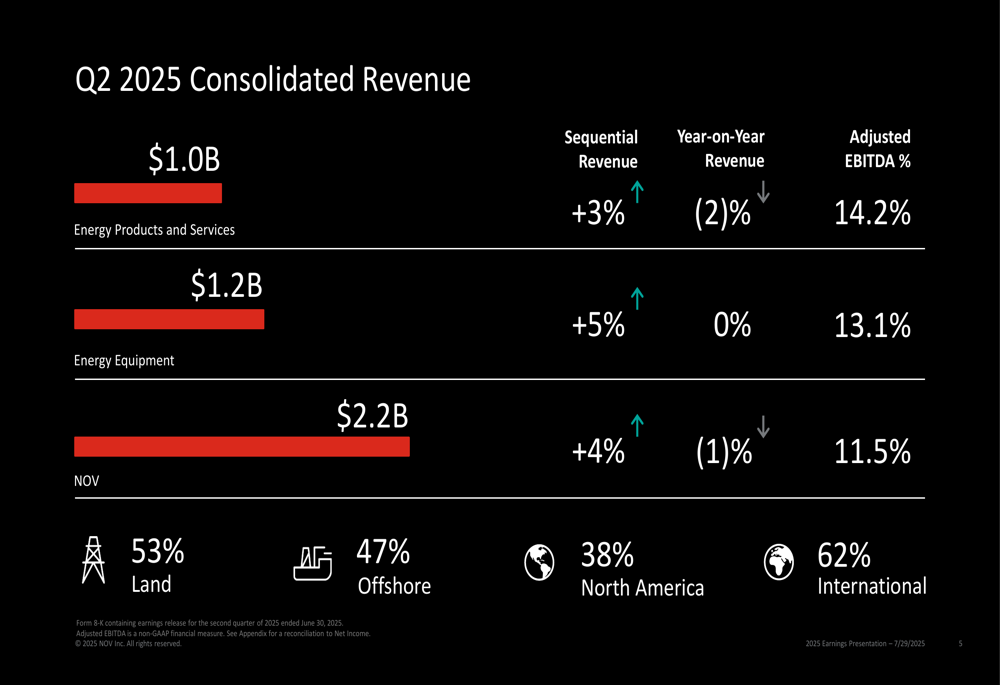

NOV Inc. (NYSE:NOV) shares plunged over 7% in early trading following the release of its second quarter 2025 earnings presentation on July 29, as investors reacted to concerning forward indicators despite modest sequential revenue growth. The oilfield equipment and technology provider reported consolidated revenue of $2.2 billion, representing a 4% sequential increase but a 1% year-over-year decline.

Quarterly Performance Highlights

NOV delivered mixed results across its two main business segments. The company achieved an overall adjusted EBITDA margin of 11.5%, with its Energy Products and Services segment generating $1.0 billion in revenue (+3% sequentially, -2% year-over-year) and its Energy Equipment segment posting $1.2 billion (+5% sequentially, flat year-over-year).

The company’s geographical revenue mix reflects its strategic pivot toward international and offshore markets, with North America representing only 38% of revenue while international markets accounted for 62%. Similarly, offshore operations contributed 47% of revenue compared to 53% from land-based activities.

However, the most concerning metric for investors appears to be the dramatic 57% year-over-year decline in new orders, which totaled just $420 million in the quarter. This resulted in a book-to-bill ratio of only 66%, suggesting potential revenue challenges in future quarters as the company works through its existing backlog.

Detailed Financial Analysis

The Energy Products and Services segment faced several headwinds during the quarter. Management noted that profitability was impacted by "a less favorable sales mix, tariffs, and charges in Latin America." This segment’s adjusted EBITDA margin contracted to 14.2%, representing a 40 basis point sequential decline and a substantial 330 basis point year-over-year drop.

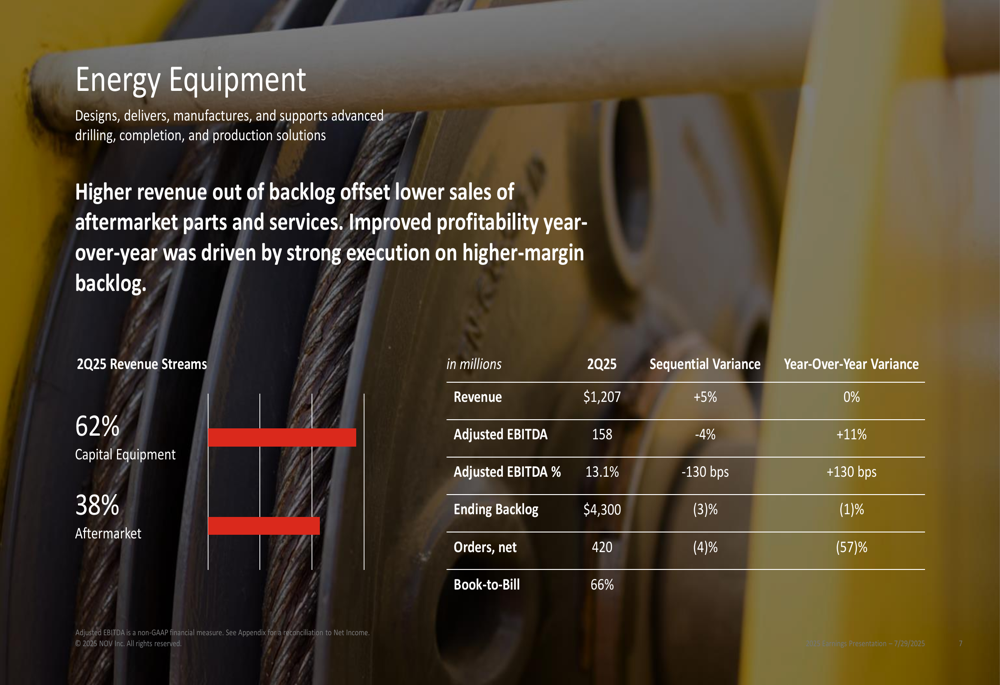

By contrast, the Energy Equipment segment showed improved profitability year-over-year, with adjusted EBITDA margin expanding 130 basis points to 13.1% compared to Q2 2024. Management attributed this improvement to "strong execution on higher-margin backlog." However, the segment’s backlog declined 3% sequentially to $4.3 billion, and the sharp drop in new orders raises questions about future revenue stability.

The financial results align with patterns identified in NOV’s previous quarter, when the company missed EPS expectations. According to the Q1 earnings call, NOV had anticipated tariff impacts of $8-10 million in Q2, with these costs expected to increase to approximately $15 million per quarter going forward.

Strategic Initiatives

Despite market challenges, NOV highlighted several significant achievements during the quarter, including:

- A multi-year contract for instrumentation and digital services with a major U.S. land drilling contractor

- A contract to deliver a Submerged Swivel and Yoke system for an FLNG (OL:FLNG) project in Argentina

- Installation of four high-profile automation packages on offshore rigs, including one with the ATOM RTX™ robotic system that reported nearly 99% utilization

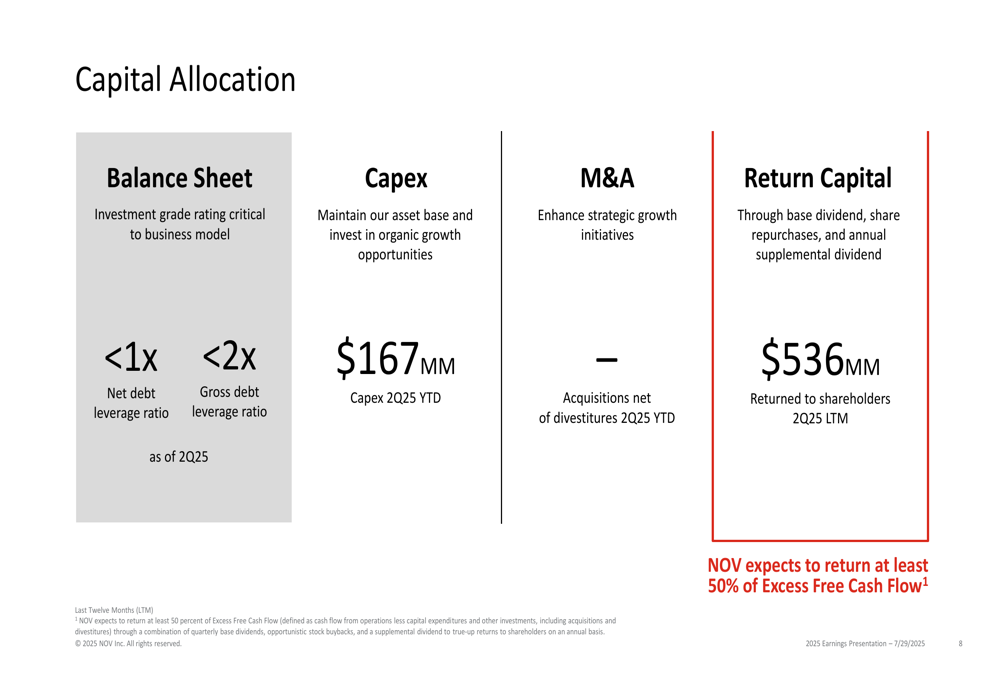

The company’s capital allocation strategy remains focused on maintaining an investment grade rating while returning capital to shareholders. NOV has targeted a net debt leverage ratio below 1x and a gross debt leverage ratio below 2x. The company returned $536 million to shareholders over the last twelve months through dividends and share repurchases.

NOV emphasized its commitment to returning at least 50% of excess free cash flow to shareholders through a combination of dividends, buybacks, and supplemental dividends, highlighting its confidence in long-term cash generation despite near-term market challenges.

Forward-Looking Statements

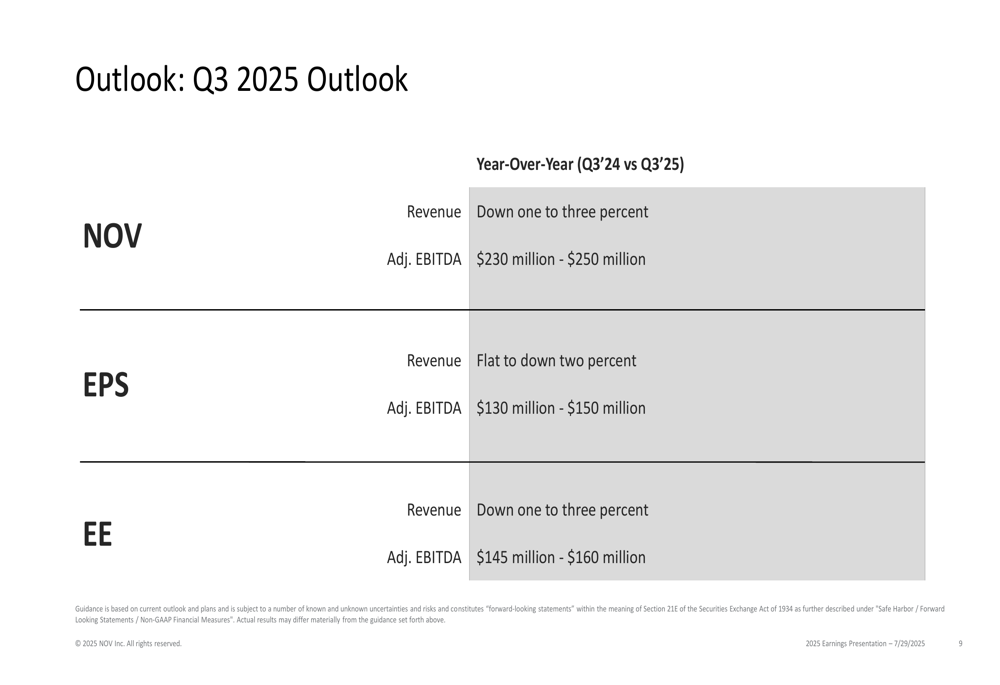

NOV’s outlook for the third quarter likely contributed to the negative market reaction. The company projects consolidated revenue to decline 1-3% year-over-year in Q3 2025, with adjusted EBITDA expected between $230-250 million.

Both operating segments are expected to see revenue contraction, with Energy Products and Services projected to be flat to down 2% year-over-year and Energy Equipment anticipated to decline 1-3%. This outlook suggests continued challenges in NOV’s core markets, particularly given the significant drop in new orders.

The guidance aligns with cautions expressed during the Q1 earnings call, where CEO Clay Williams noted the significance of U.S. shale developments while acknowledging industry challenges. The continued shift toward international and offshore markets appears to be a strategic response to declining North American drilling activity.

With a current stock price of $13.15 in pre-market trading, NOV shares have fallen significantly from their 52-week high of $21.20, though they remain above the 52-week low of $10.84. Investors appear concerned about the company’s ability to maintain revenue and profitability in the face of declining orders and ongoing market challenges, despite NOV’s technological leadership and strong position in offshore and international markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.