Intel stock spikes after report of possible US government stake

Introduction & Market Context

Novavax , Inc. (NASDAQ:NVAX) presented its second quarter 2025 financial results and operational highlights on August 6, 2025, revealing a strategic pivot toward partnership-driven revenue and aggressive cost-cutting measures. The vaccine developer’s shares rose 3.57% in premarket trading to $6.97, building on positive momentum following its strong first-quarter performance earlier this year.

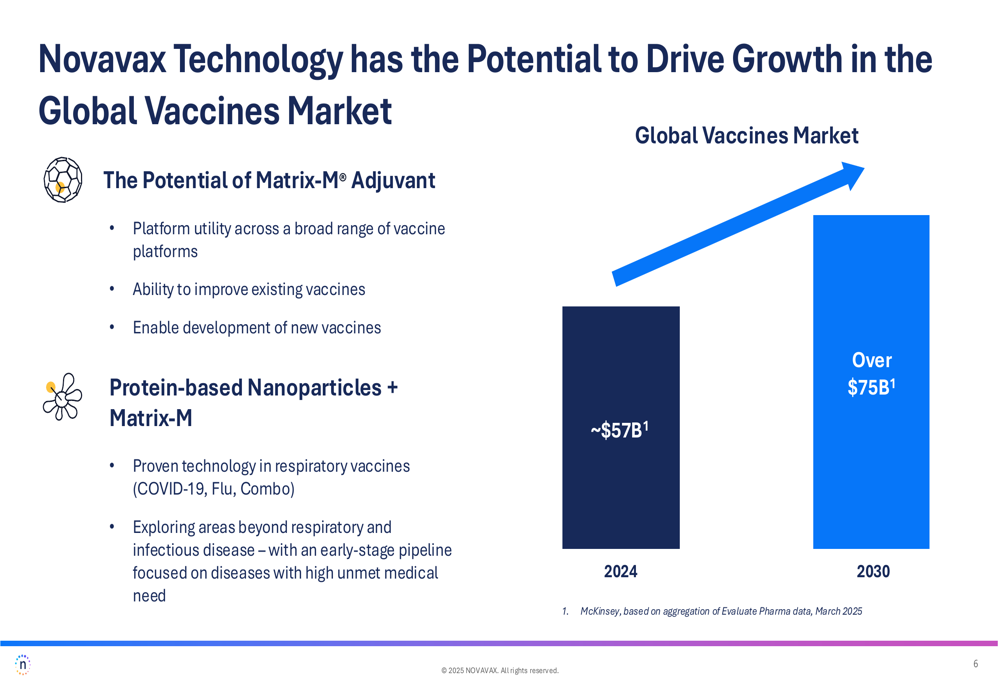

The presentation highlighted Novavax’s positioning within a growing global vaccines market, which is projected to expand from approximately $57 billion in 2024 to over $75 billion by 2030, according to McKinsey data cited by the company. Novavax is leveraging its protein-based technology platform and Matrix-M adjuvant to capitalize on this growth potential.

As shown in the following chart illustrating Novavax’s growth potential in the expanding vaccines market:

Quarterly Performance Highlights

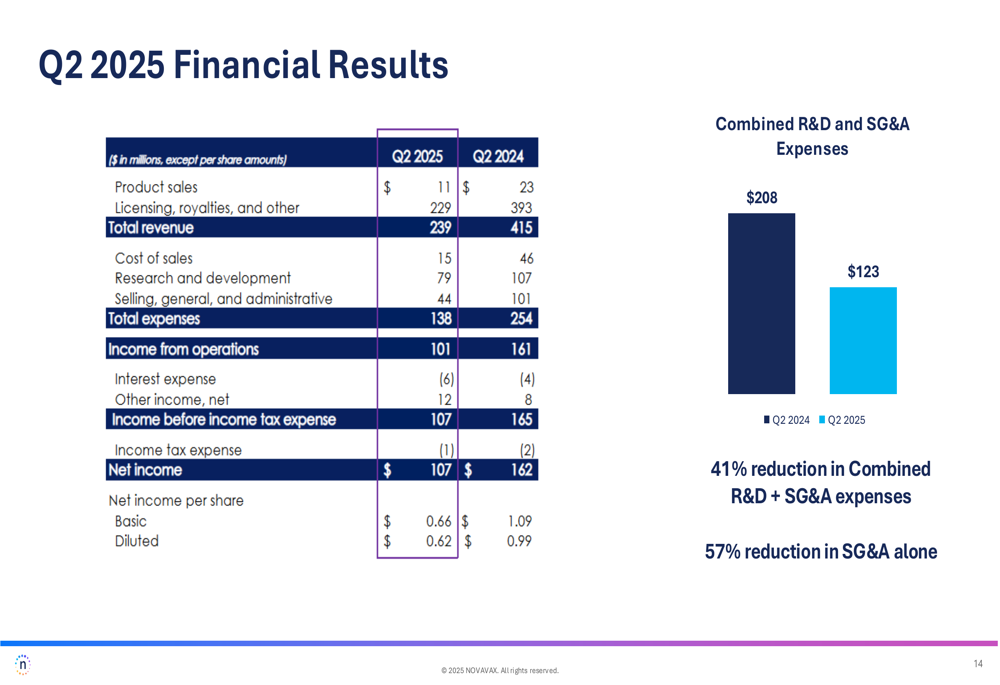

Novavax reported total revenue of $239 million for Q2 2025, compared to $415 million in the same period last year. Despite this revenue decline, the company achieved net income of $107 million, driven by milestone payments and significant reductions in operating expenses.

The financial results breakdown reveals a shift from product sales to licensing and partnership revenue:

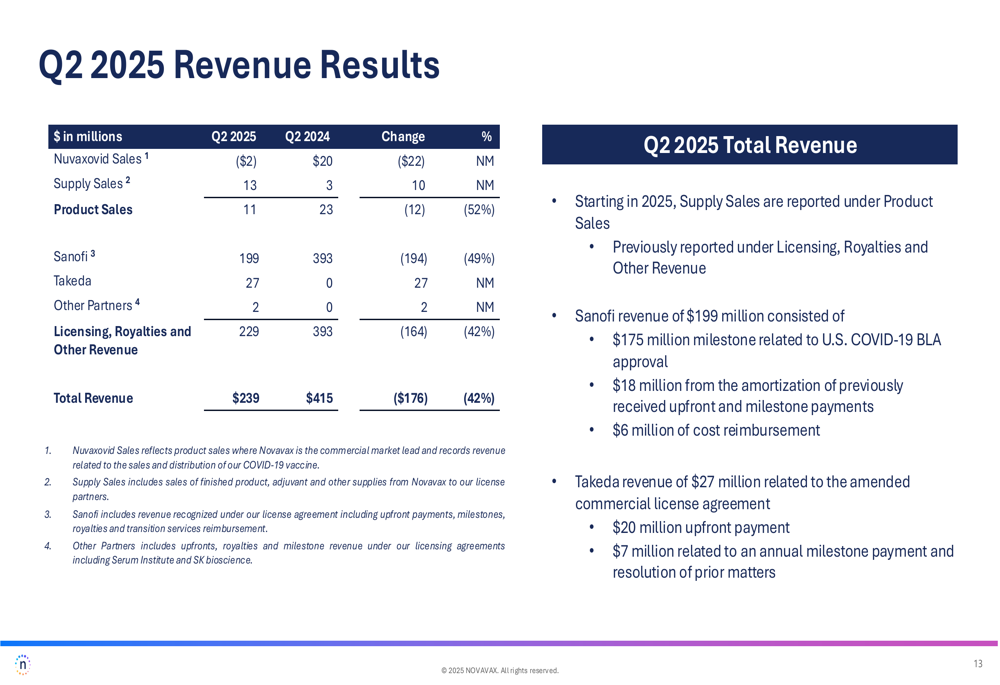

The company’s revenue composition has evolved significantly, with licensing, royalties, and other revenue accounting for $229 million of the total $239 million. This included a substantial $175 million milestone payment related to the U.S. FDA approval of Nuvaxovid in May 2025. Product sales contributed just $11 million during the quarter.

A detailed breakdown of the revenue sources shows:

Strategic Initiatives

Novavax outlined three strategic priorities for 2025, with partnerships playing a central role in the company’s business model. The Sanofi (NASDAQ:SNY) partnership remains the top priority, followed by enhancing existing partnerships and leveraging technology to forge new collaborations. The third priority focuses on advancing the company’s technology platform and early-stage pipeline.

The following slide illustrates these strategic priorities:

The partnership with Sanofi is expected to yield up to $50 million in milestone payments in Q4 2025, providing additional revenue visibility for the remainder of the year. This relationship, along with other collaborations like the one with Takeda (which contributed $27 million in Q2 revenue), underscores Novavax’s shift toward a partnership-driven business model.

Financial Analysis

A key highlight of Novavax’s Q2 results was the substantial reduction in operating expenses, which decreased by 41% compared to Q2 2024. Combined R&D and SG&A expenses fell from $208 million in Q2 2024 to $123 million in Q2 2025. This cost discipline contributed significantly to the company’s profitability despite lower revenue.

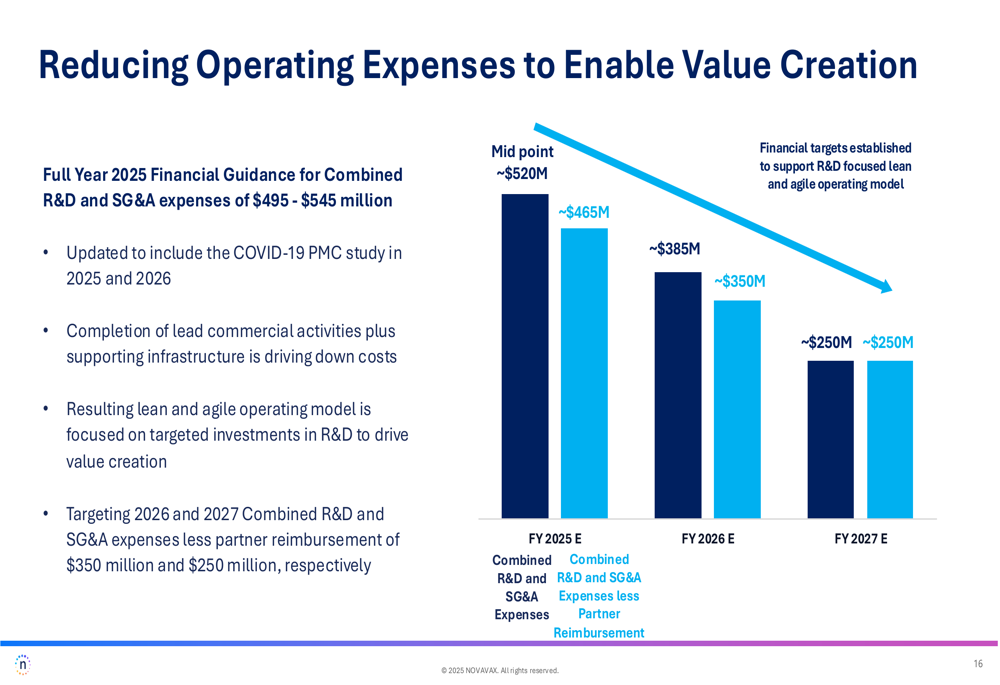

The company’s expense reduction trajectory is clearly illustrated in the following slide:

Novavax ended the quarter with a strong financial position, reporting combined cash and accounts receivable of $854 million, consisting of $628 million in cash and $226 million in accounts receivable. This represents a solid foundation as the company continues its strategic transformation.

The company updated its full-year 2025 financial guidance for combined R&D and SG&A expenses to $495-545 million, which includes costs associated with the COVID-19 post-marketing commitment (PMC) study required by the FDA. This study is expected to cost between $70-90 million, with approximately $55 million to be reimbursed.

Pipeline and R&D Updates

Novavax’s presentation highlighted promising developments in its vaccine pipeline, particularly for its combination influenza-COVID (CIC) and standalone influenza vaccines. New T-cell response data showed numerically higher responses compared to competitor products, suggesting potential for broader and longer-lasting immunity.

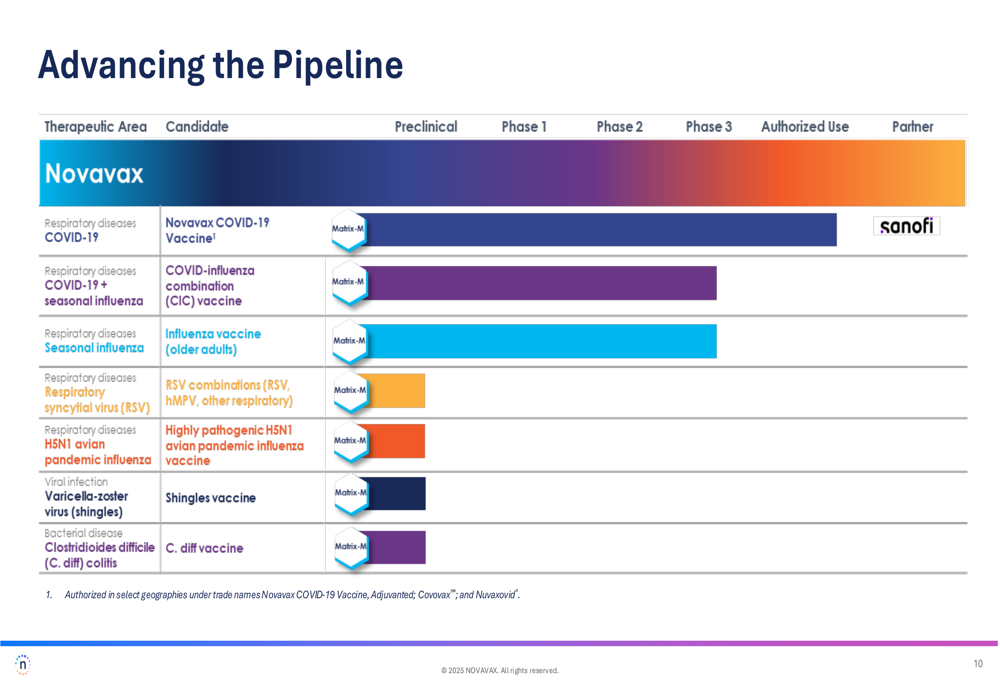

The company’s comprehensive pipeline spans multiple therapeutic areas, including COVID-19, seasonal influenza, RSV, pandemic influenza, shingles, and C. diff colitis, with candidates at various stages of development:

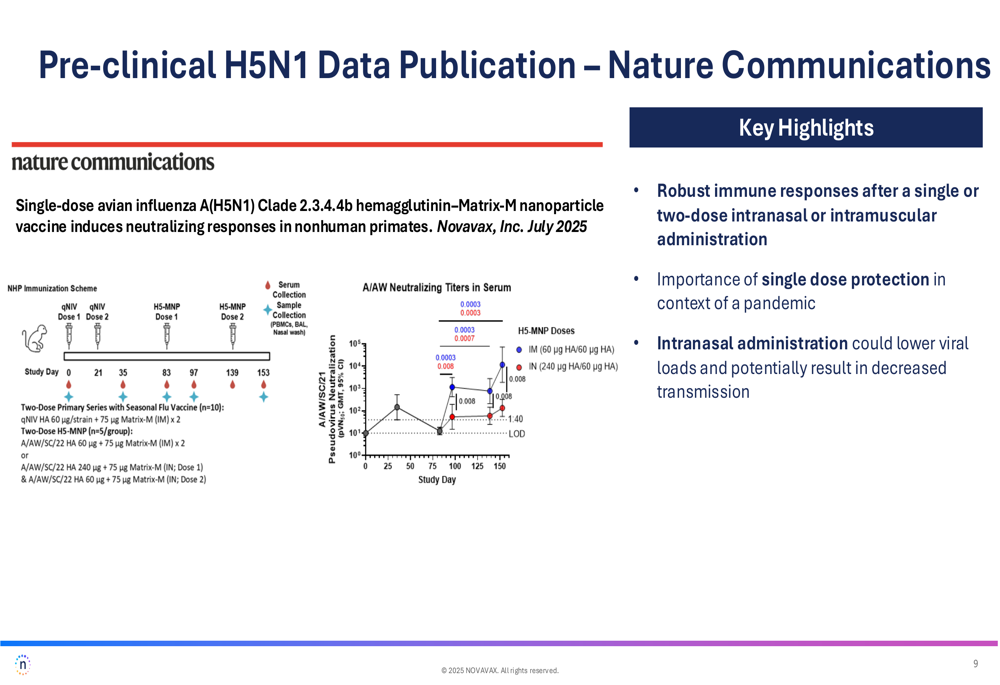

Scientific validation of Novavax’s technology platform was reinforced by a recent publication in Nature Communications regarding preclinical H5N1 data, which demonstrated robust immune responses after single or two-dose administration:

Forward-Looking Statements

Looking ahead, Novavax reaffirmed its revenue framework for 2025, with total expected revenue of $975 million to $1.025 billion. This includes anticipated milestone payments from partnerships and ongoing product sales.

The company’s cost-cutting initiatives are projected to continue, with combined R&D and SG&A expenses expected to decrease from approximately $520 million in FY2025 to around $250 million by FY2027. This aligns with statements from the Q1 earnings call, where management indicated a target of achieving non-GAAP profitability by 2027.

Novavax’s strategic focus on partnerships, cost discipline, and targeted pipeline development positions the company to leverage its protein-based technology platform and Matrix-M adjuvant across an expanding range of applications in the growing global vaccines market. While the transition from direct product sales to a partnership model has resulted in revenue fluctuations, the improved cost structure and milestone-driven revenue streams appear to be creating a more sustainable financial foundation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.