Gold prices near $4,500/oz record high on rate cut bets, US tariff uncertainty

NRG Energy (NYSE:NRG) presented its second quarter 2025 earnings results on August 6, revealing mixed quarterly performance but strong year-to-date numbers. The company’s shares dropped 5.78% in premarket trading to $162.02, suggesting the results fell short of market expectations despite management’s optimistic outlook.

Executive Summary

NRG reported second quarter adjusted earnings per share of $1.73, an 8% increase year-over-year, while maintaining its full-year 2025 guidance. The company highlighted several strategic initiatives, including significant data center power agreements and an expanding virtual power plant program, which management believes will drive future growth.

"Strong Second Quarter Caps Robust First Half; Trending At the Upper End of 2025 Guidance Ranges," stated the company in its key messages slide, emphasizing its confidence in meeting full-year targets despite some quarterly headwinds.

As shown in the following key messages from the presentation:

Quarterly Performance Highlights

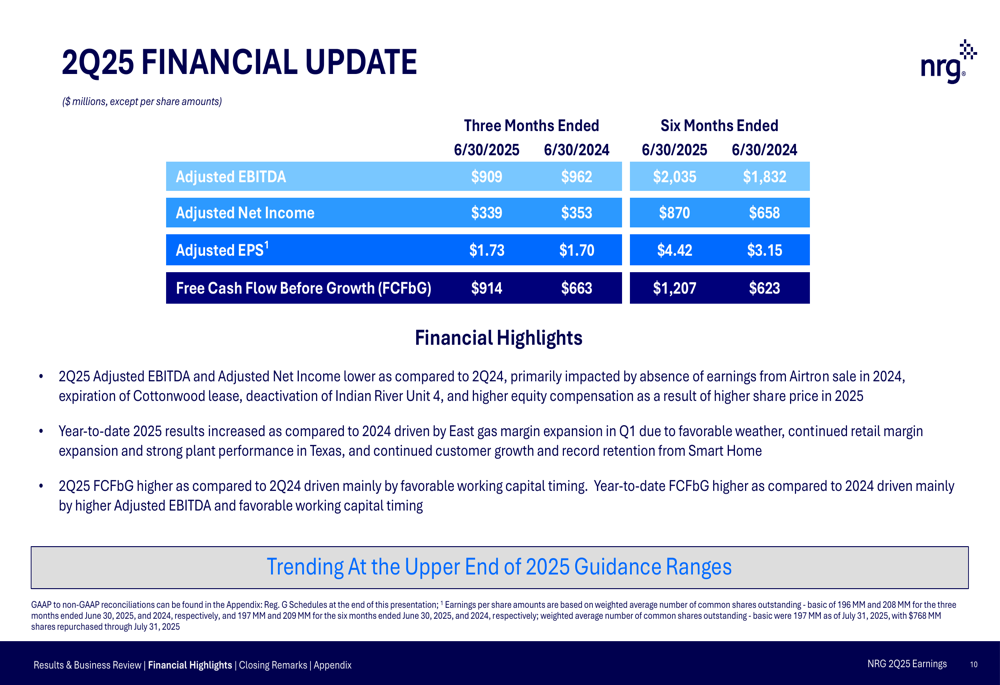

For Q2 2025, NRG posted adjusted EBITDA of $909 million and adjusted net income of $339 million, resulting in adjusted EPS of $1.73. While these quarterly figures represent a decrease compared to Q2 2024, the company’s year-to-date performance remains strong with adjusted EBITDA reaching $2.035 billion, up 11% year-over-year.

The company explained that the quarterly decline was primarily due to the absence of earnings from the Airtron sale in 2024, expiration of the Cottonwood lease, deactivation of Indian River Unit 4, and higher equity compensation resulting from increased share price in 2025.

The detailed financial results are illustrated in the following slide:

Despite the quarterly dip, NRG’s year-to-date 2025 results improved compared to 2024, driven by East gas margin expansion in Q1 due to favorable weather, continued retail margin expansion and strong plant performance in Texas, and continued customer growth and record retention from the Smart Home segment.

This performance follows a particularly strong first quarter, where NRG had reported adjusted EPS of $2.68, significantly exceeding analyst expectations of $1.67, according to previous earnings reports.

Strategic Growth Initiatives

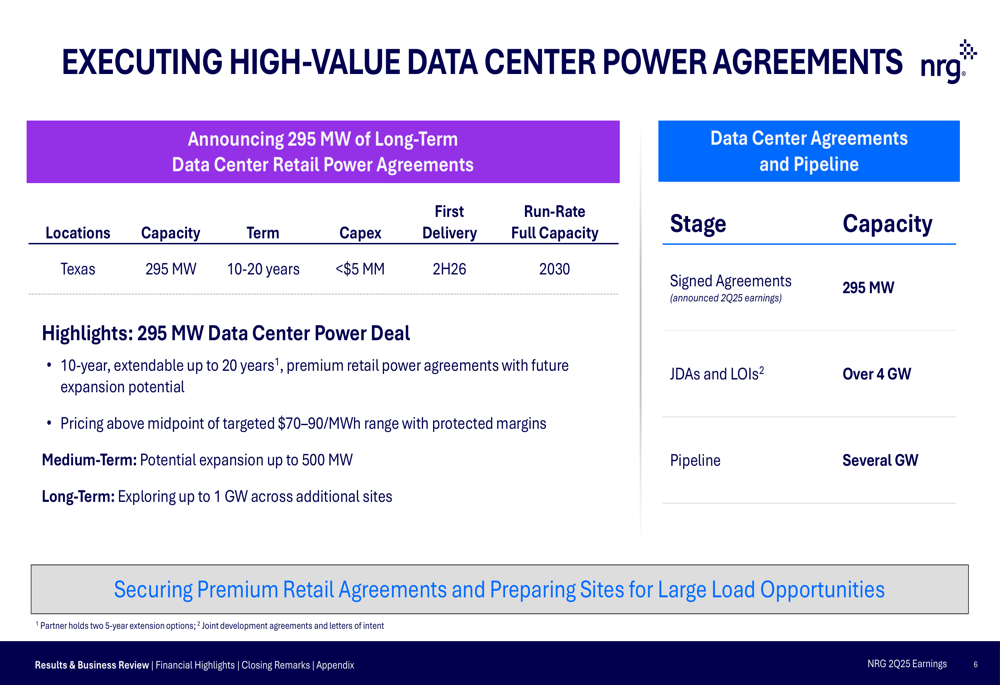

A major highlight of NRG’s presentation was the announcement of 295 MW of long-term data center retail power agreements, with terms ranging from 10-20 years. These agreements, set for first delivery in the second half of 2026, feature pricing in the $70-90/MWh range with protected margins and minimal capital expenditure requirements.

The data center agreements also come with significant expansion potential, with the company noting "potential expansion of 500 MW medium-term" and exploration of "up to 1 GW long-term." This strategic focus on the high-growth data center market represents an important pivot for NRG.

The details of these agreements are shown in the following slide:

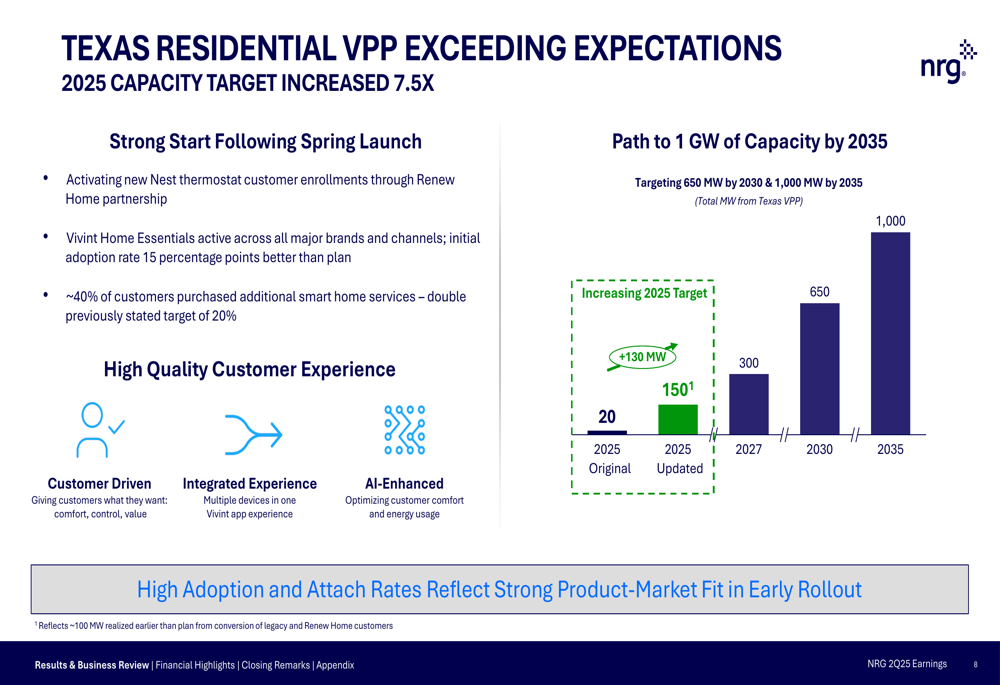

Another key growth initiative is NRG’s Texas Residential Virtual Power Plant (VPP), which is exceeding initial expectations. The company has increased its 2025 capacity target 7.5 times, from 20 MW to 150 MW, with ambitious goals of reaching 650 MW by 2030 and 1,000 MW by 2035.

The VPP program has shown strong customer adoption, with initial rates 15 percentage points better than planned, and approximately 40% of customers purchasing additional smart home services – double the company’s previously stated target of 20%.

The growth trajectory of the VPP initiative is illustrated here:

NRG also highlighted progress on its Texas Energy Fund Development Portfolio, with the T.H. Wharton 415 MW CT project moving forward after closing TEF financing and receiving the first loan disbursement. The project remains on track for a mid-2026 commercial operation date. Additional projects in the development pipeline include Cedar Bayou 5 (689 MW CCGT) and Greens Bayou 6 (443 MW CT), both targeted for 2028 completion.

Financial Outlook & Capital Allocation

NRG reaffirmed its 2025 guidance, projecting adjusted earnings per share of $6.75-$7.75, adjusted EBITDA of $3.725-$3.975 billion, and free cash flow before growth of $1.975-$2.225 billion. The company stated it is trending toward the upper end of these ranges.

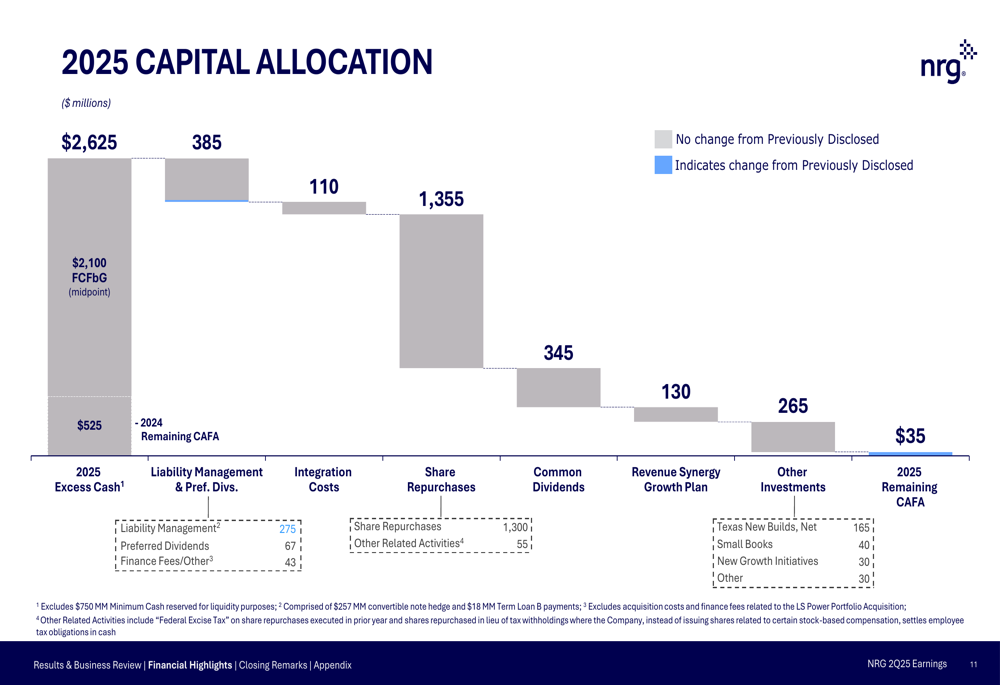

The company’s 2025 capital allocation plan totals $2.625 billion, with the largest portion ($1.3 billion) dedicated to share repurchases. Other allocations include common dividends ($345 million), liability management and preferred dividends ($275 million), and various growth investments.

The breakdown of NRG’s capital allocation strategy is shown in this slide:

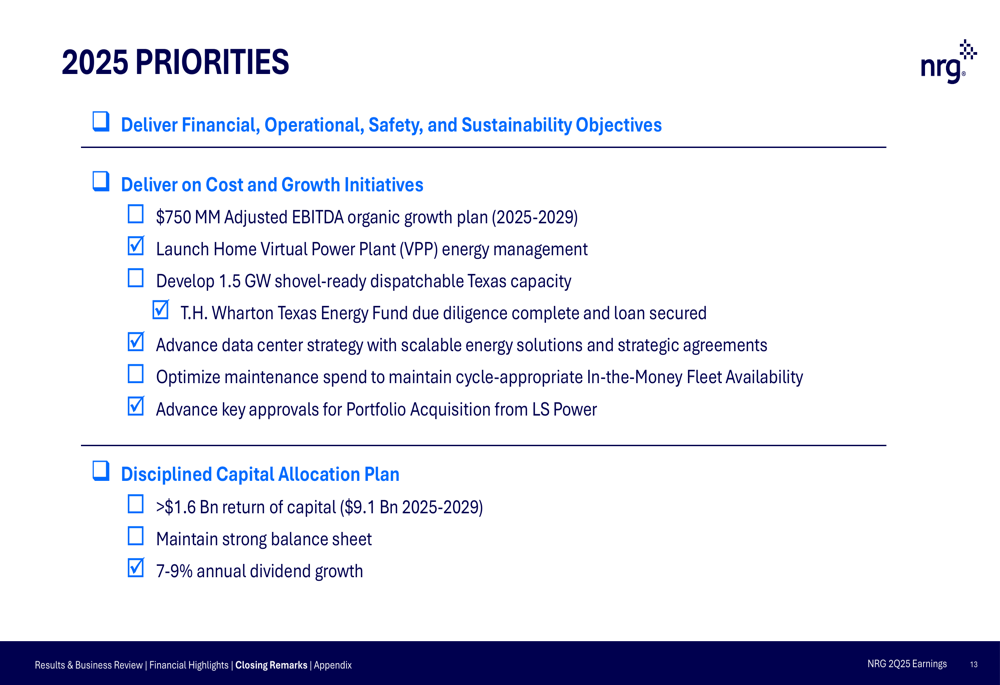

NRG also outlined its 2025 priorities, focusing on delivering financial, operational, safety, and sustainability objectives; executing cost and growth initiatives; and maintaining disciplined capital allocation. The company emphasized its commitment to returning capital to shareholders while maintaining a strong balance sheet and growing its annual dividend.

Market Reaction & Conclusion

Despite the company’s positive framing of results and reaffirmed guidance, NRG shares were down 5.78% in premarket trading following the earnings presentation, suggesting investors may have expected stronger quarterly performance or more aggressive growth projections.

The stock had been performing well prior to this report, trading near $171.96 at the previous close, not far from its 52-week high of $175.96. The company’s market capitalization stood at approximately $28.62 billion before the earnings announcement.

NRG’s mixed quarterly results highlight the challenges of balancing short-term performance with long-term strategic initiatives. While the company faces some headwinds in quarterly comparisons, its focus on high-growth areas like data centers and virtual power plants, combined with its Texas Energy Fund development projects, positions it to potentially capitalize on evolving energy market trends.

Investors will likely be watching closely to see if NRG can execute on its ambitious growth plans while delivering on its financial guidance for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.