Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Executive Summary

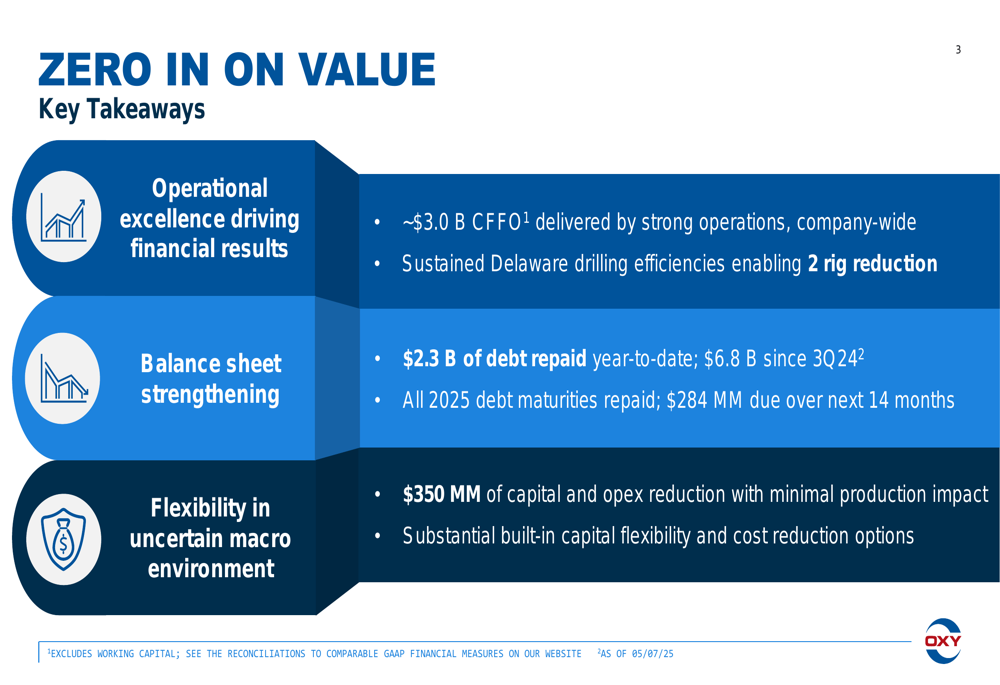

Occidental Petroleum Corporation (NYSE:OXY) delivered strong first quarter 2025 results, generating approximately $3.0 billion in cash flow from operations and $1.2 billion in free cash flow, according to the company’s May 8, 2025, earnings presentation. The quarter was marked by significant debt reduction progress, with $2.3 billion repaid year-to-date and operational efficiencies enabling capital reductions while maintaining production guidance.

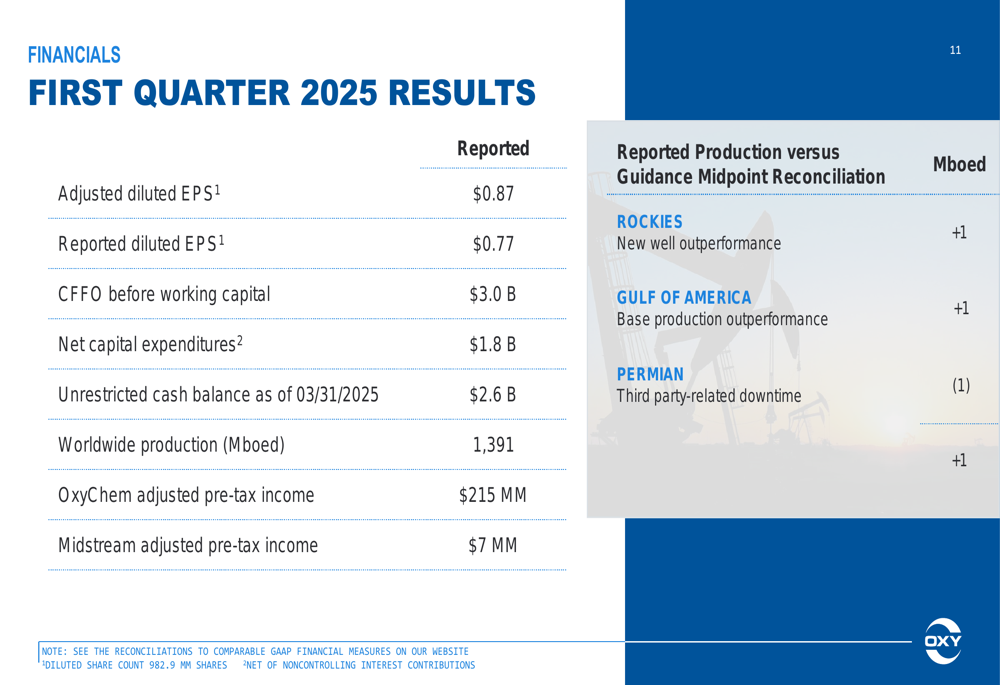

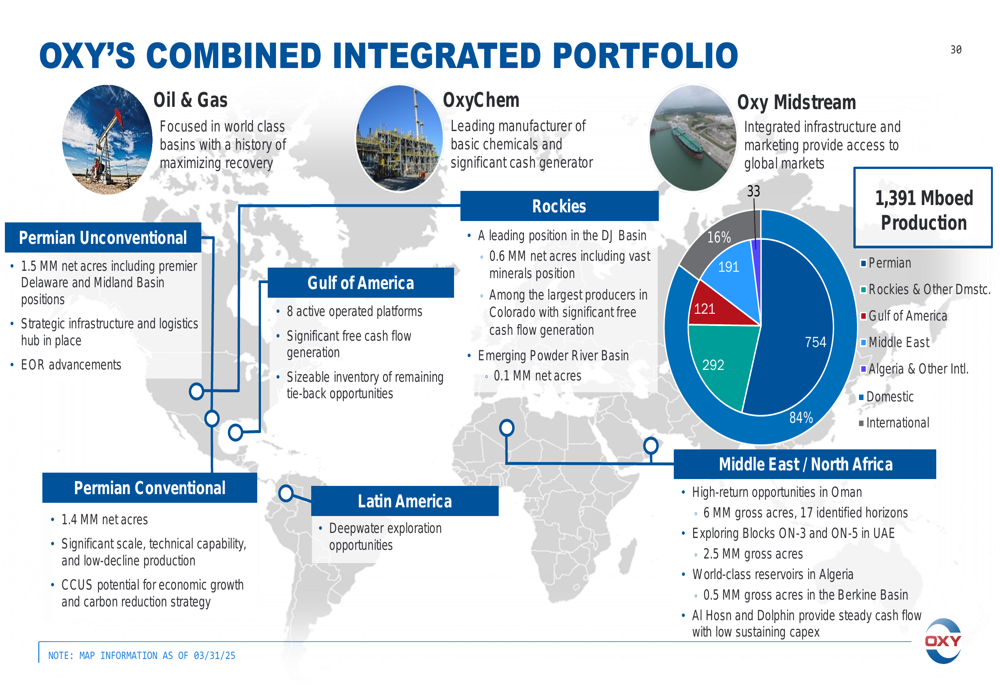

The company reported adjusted diluted earnings per share of $0.87 and total production of 1,391 thousand barrels of oil equivalent per day (Mboed). Occidental’s chemical segment outperformed expectations with $215 million in adjusted pre-tax income, contributing to the company’s solid quarterly performance.

As shown in the following summary of key takeaways from the quarter:

Financial Performance

Occidental’s first quarter 2025 financial results demonstrated the company’s ability to generate substantial cash flow while continuing to strengthen its balance sheet. The company reported adjusted diluted EPS of $0.87 and reported diluted EPS of $0.77, supported by strong operational performance across its business segments.

Total (EPA:TTEF) company production reached 1,391 Mboed, slightly above the midpoint of guidance, with the Permian Basin contributing 754 Mboed, or approximately 54% of total production. The company’s chemical segment (OxyChem) delivered $215 million in adjusted pre-tax income, while the midstream segment contributed $7 million.

The detailed financial results for the first quarter are illustrated below:

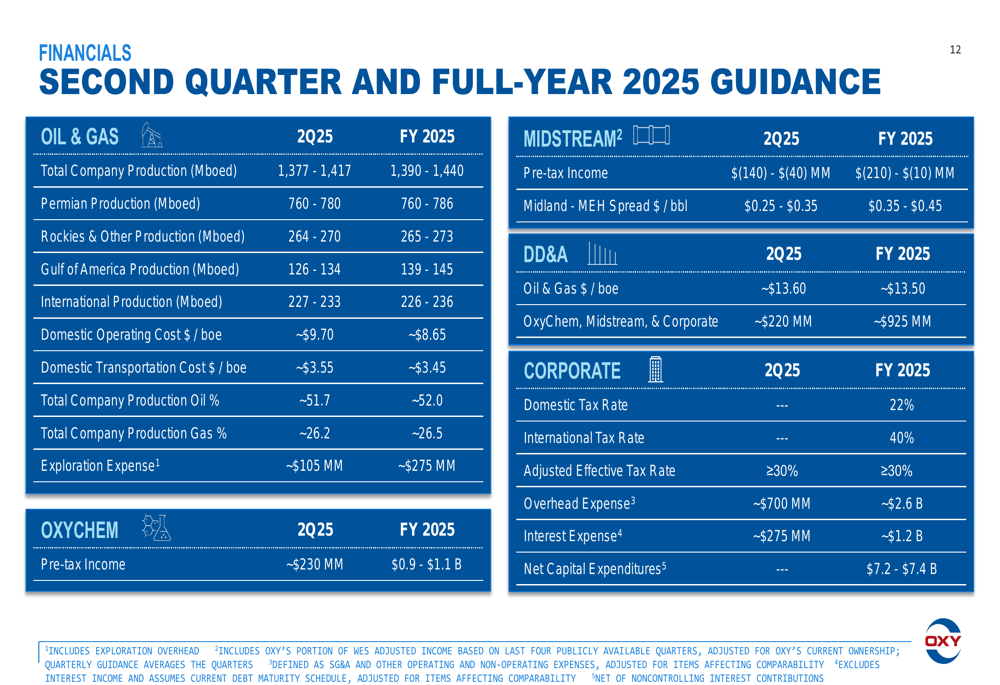

Looking ahead, Occidental provided guidance for the second quarter and full year 2025. For Q2, the company expects total production between 1,377 and 1,417 Mboed, with full-year production guidance of 1,390 to 1,440 Mboed. OxyChem is projected to generate approximately $230 million in pre-tax income for Q2 and between $0.9 billion and $1.1 billion for the full year.

Debt Reduction Progress

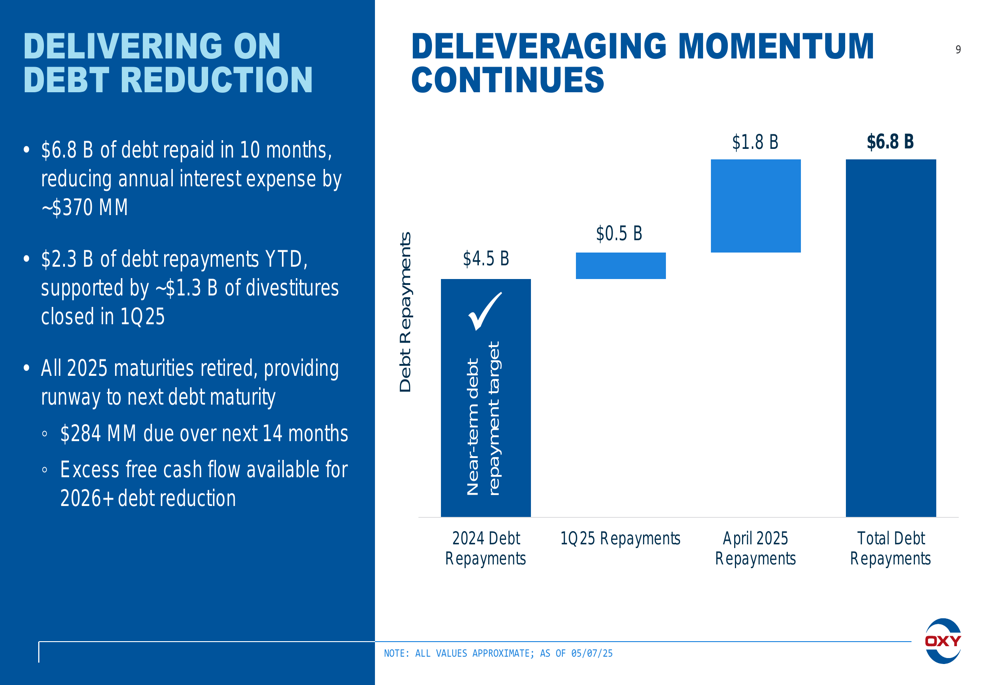

A cornerstone of Occidental’s strategy has been aggressive debt reduction, which continued in the first quarter of 2025. The company has repaid $6.8 billion of debt in the past 10 months, including $2.3 billion year-to-date as of May 7, 2025. This deleveraging effort has reduced annual interest expense by approximately $370 million.

Notably, Occidental has retired all 2025 debt maturities, with only $284 million due over the next 14 months. This provides significant financial flexibility and positions the company to continue allocating excess free cash flow toward further debt reduction.

The following chart illustrates Occidental’s debt reduction progress:

The company’s cash flow priorities for 2025 continue to focus on maintaining its production base, supporting a sustainable and growing dividend, and allocating excess cash flow to debt reduction to rebalance enterprise value in favor of common shareholders.

Operational Efficiencies

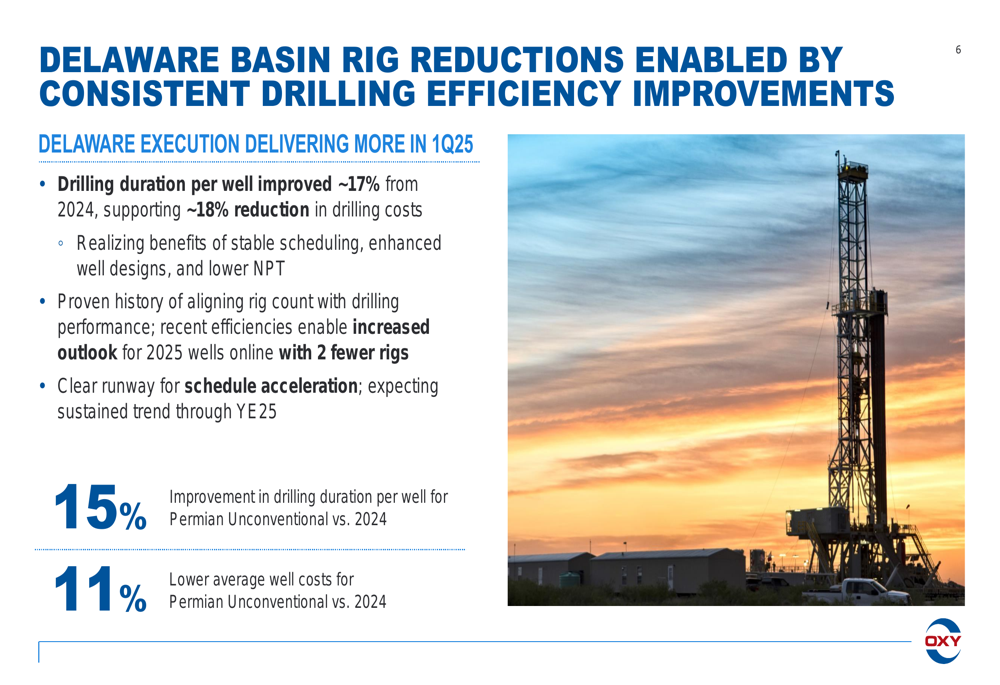

Operational excellence, particularly in the Delaware Basin, has been a key driver of Occidental’s financial performance. The company reported significant efficiency improvements in drilling operations, with drilling duration per well improved by approximately 17% from 2024, supporting an 18% reduction in drilling costs.

These efficiency gains have enabled Occidental to reduce its rig count in the Delaware Basin while maintaining production targets. The company expects to achieve a 15% improvement in drilling duration per well for Permian Unconventional operations versus 2024 and 11% lower average well costs.

The following slide details the Delaware Basin efficiency improvements:

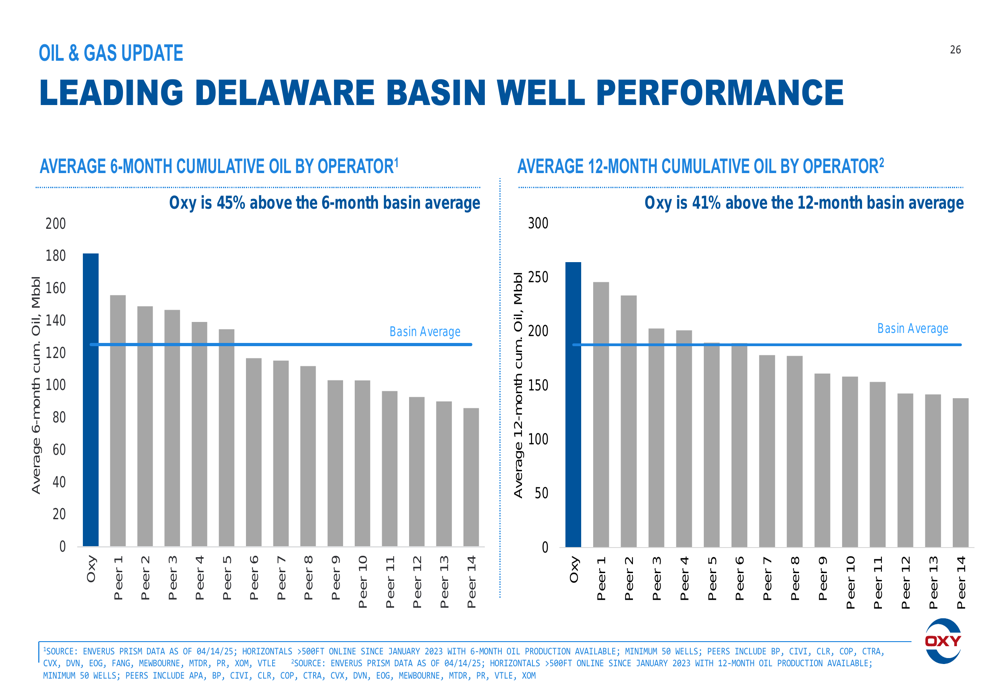

Occidental’s well performance in the Delaware Basin continues to outpace industry averages, with wells delivering 45% above the 6-month basin average and 41% above the 12-month basin average for cumulative oil production.

Strategic Initiatives

Occidental highlighted several strategic initiatives aimed at enhancing long-term value. In Oman, the company is in advanced negotiations for a contract extension of Block 53 (Mukhaizna) to 2050, which could deliver significant value and potentially grow resources by more than 800 million gross barrels. Additionally, a North Oman gas and condensate discovery with estimated resources in place exceeding 250 million barrels of oil equivalent presents another growth opportunity.

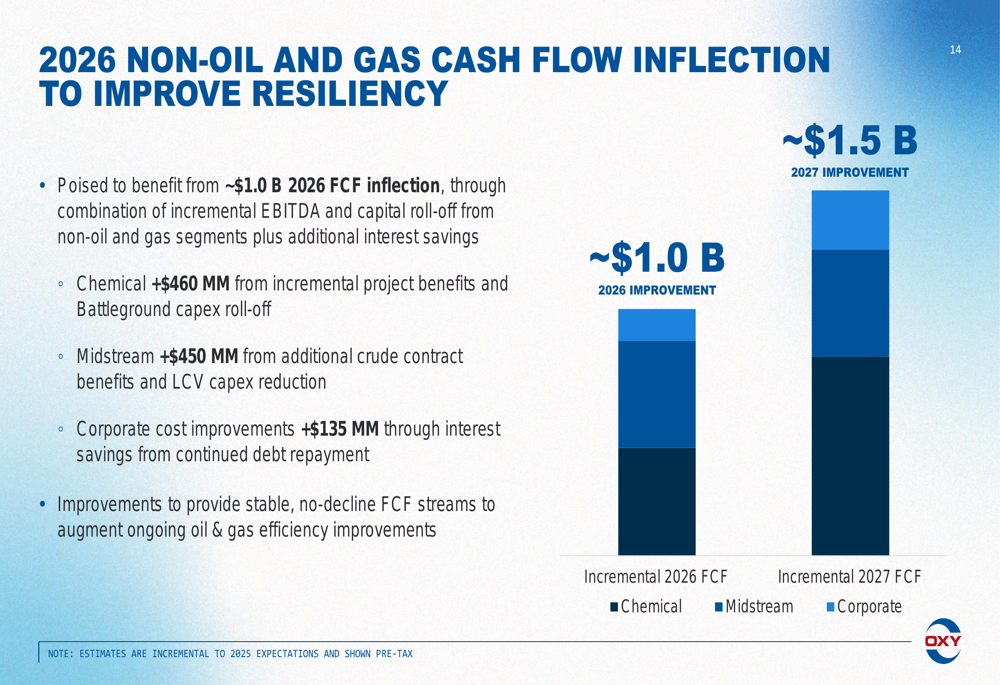

The company is also positioning itself for a significant cash flow inflection from non-oil and gas businesses in 2026. Occidental expects approximately $1.0 billion in incremental free cash flow in 2026, growing to $1.5 billion in 2027, through a combination of incremental EBITDA and capital roll-off from non-oil and gas segments plus additional interest savings.

As illustrated in the following chart:

In the chemicals segment, Occidental’s OxyChem subsidiary continues to maintain a market-leading position as the second-largest merchant caustic soda seller in the world and the fourth-largest VCM producer. The Battleground modernization and expansion project is progressing, with expected completion contributing to improved margins and higher product volumes.

Capital Allocation and Guidance

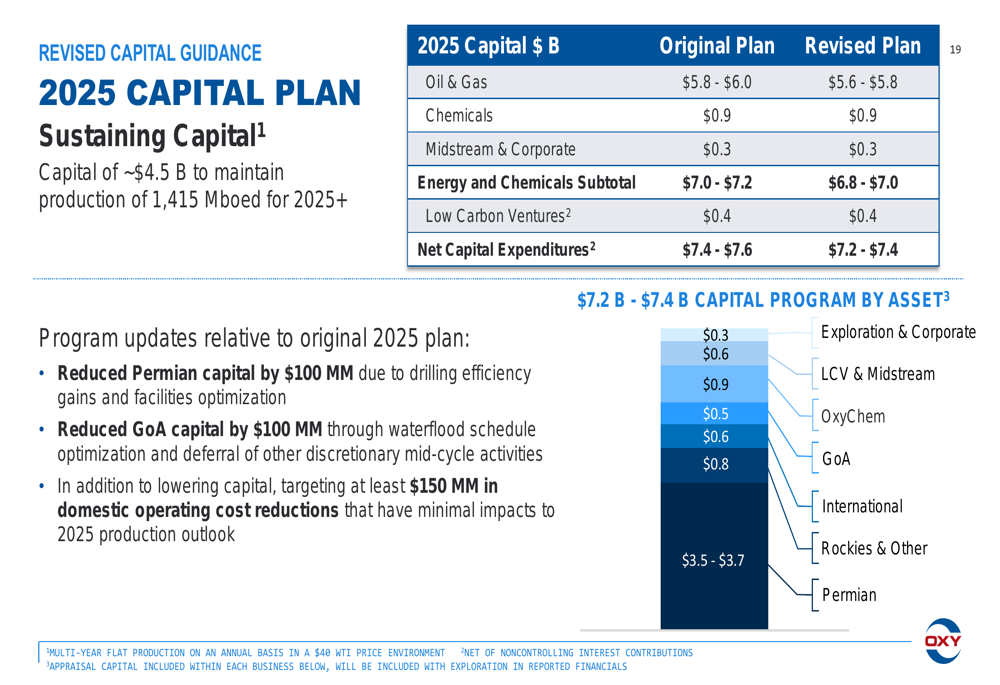

In response to the uncertain macro environment, Occidental has revised its 2025 capital guidance, reducing planned expenditures by $200 million while maintaining production targets. The company reduced Permian capital by $100 million due to drilling efficiency gains and facilities optimization, and Gulf of America capital by $100 million through waterflood schedule optimization and deferral of discretionary mid-cycle activities.

Additionally, Occidental is targeting at least $150 million in domestic operating cost reductions with minimal impacts to 2025 production outlook. The revised capital plan is detailed below:

The company’s diversified portfolio spans multiple basins and business segments, providing operational flexibility and resilience. Occidental holds 9.2 million net total U.S. acres, making it one of the largest U.S. acreage holders, with significant positions in the Permian Basin, Rockies, Gulf of America, and international assets.

Forward-Looking Statements

Looking ahead, Occidental is focused on operational excellence and innovation to drive continued performance improvements. The company has approximately 13 years of high-quality, low-breakeven development locations with breakevens below $60 per barrel at current pace, providing a deep inventory for future development.

The 2026 cash flow inflection from non-oil and gas businesses is expected to provide stable, no-decline free cash flow streams to augment ongoing oil and gas efficiency improvements. This diversification of cash flow sources should enhance the company’s resilience to oil price volatility.

Occidental’s stock closed at $39.01 on May 7, 2025, down 0.69% for the day, according to the provided fundamentals data. The stock is trading closer to its 52-week low of $34.78 than its high of $64.76, potentially reflecting broader market concerns about the energy sector despite the company’s solid operational performance.

In conclusion, Occidental’s first quarter 2025 results demonstrate the company’s commitment to operational excellence, debt reduction, and strategic positioning for long-term value creation. The combination of strong cash flow generation, significant deleveraging progress, and operational efficiencies provides a solid foundation for future growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.