BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

Olaplex Holdings Inc (NASDAQ:OLPX) presented its first quarter 2025 financial results on May 8, revealing a mixed performance characterized by declining profitability but growth in its specialty retail channel. Despite reporting an earnings per share miss, with diluted EPS of $0.00 compared to $0.01 in the prior year period, the company’s stock rose 2.26% to $1.36 following the presentation, suggesting investors were encouraged by revenue figures that exceeded analyst expectations.

The premium hair care brand continues to navigate a challenging market environment while implementing its strategic initiatives centered around its "Bonds and Beyond" framework. The company’s ability to grow its specialty retail segment by double digits provided a bright spot amid broader sales challenges.

Quarterly Performance Highlights

Olaplex reported Q1 2025 net sales of $97.0 million, representing a 1.9% decrease compared to the same period in 2024. The results revealed significant divergence in channel performance, with specialty retail growing 12.0% while professional and direct-to-consumer channels declined by 10.9% and 7.2%, respectively.

As shown in the following sales breakdown:

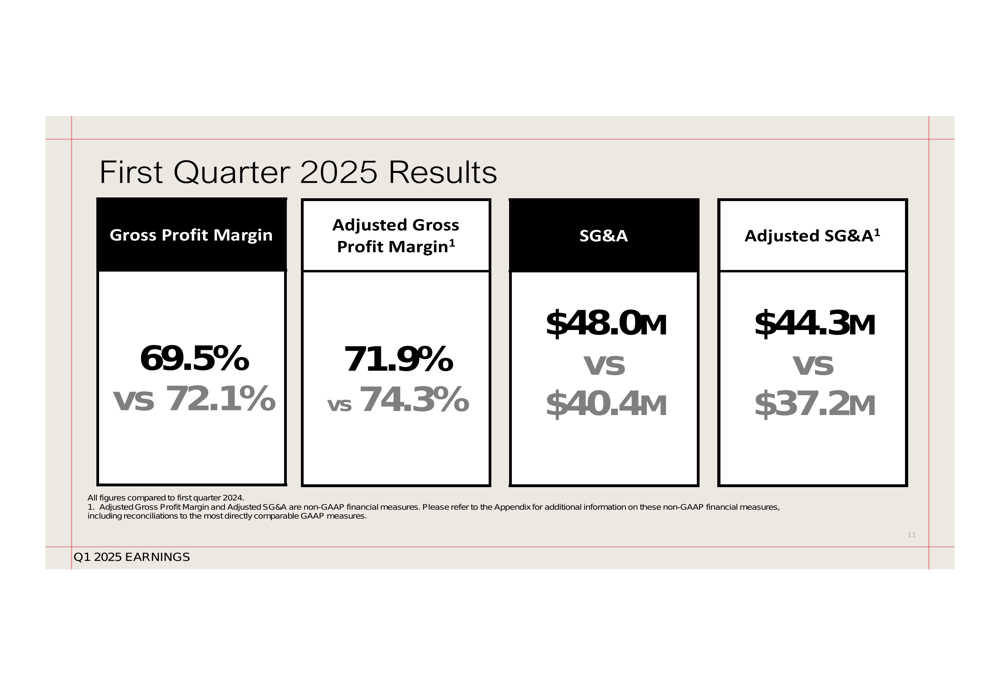

Profitability metrics showed more pronounced pressure, with gross profit margin declining to 69.5% from 72.1% in Q1 2024. On an adjusted basis, which excludes amortization of patented formulations, gross profit margin was 71.9%, down from 74.3% in the prior year period. The company also reported increased selling, general and administrative expenses, which rose to $48.0 million from $40.4 million.

The following slide details these profitability metrics:

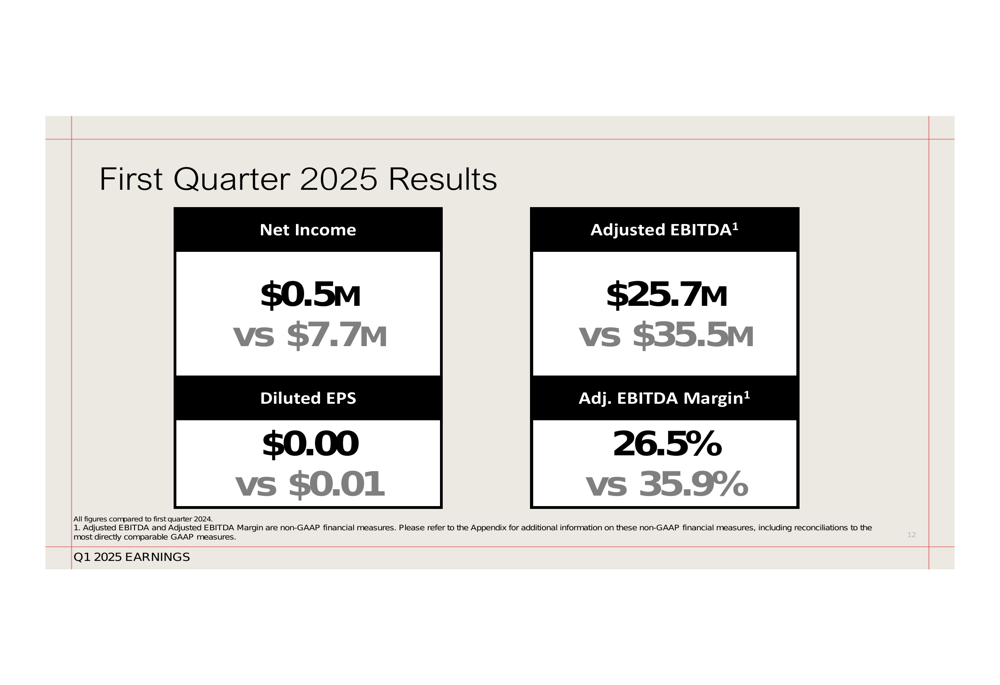

The combination of lower sales and higher operating expenses significantly impacted Olaplex’s bottom line. Net income fell to $0.5 million from $7.7 million in Q1 2024, while adjusted EBITDA decreased to $25.7 million from $35.5 million, with the corresponding margin contracting to 26.5% from 35.9%.

The following slide illustrates these profit metrics:

Financial Position

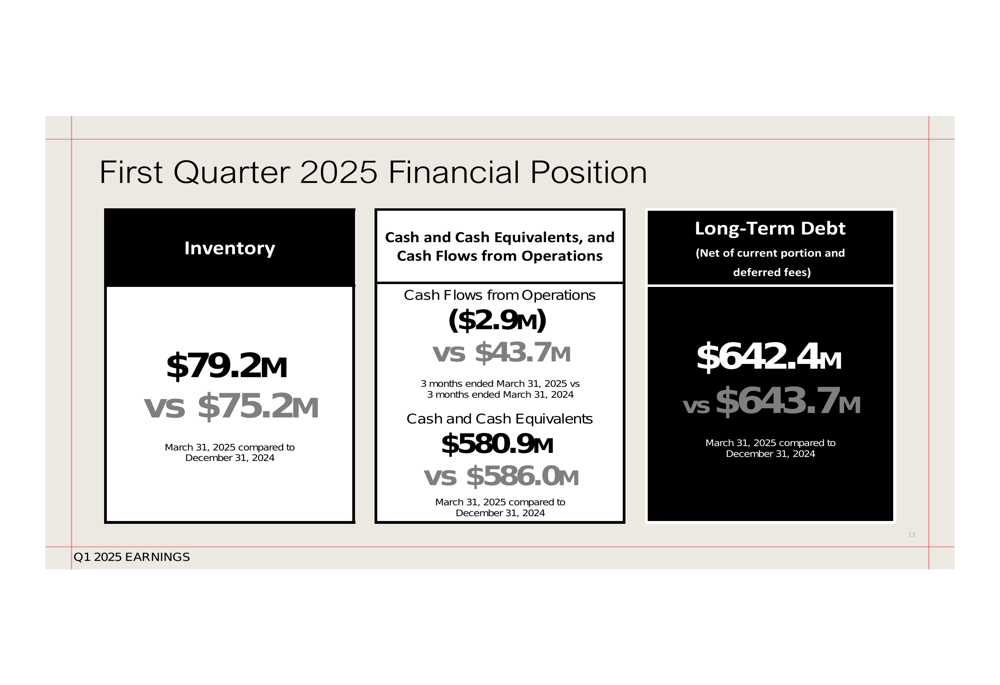

Despite the quarterly profit decline, Olaplex maintains a strong financial position with substantial cash reserves. As of March 31, 2025, the company reported $580.9 million in cash and cash equivalents, slightly down from $586.0 million at the end of 2024. Long-term debt stood at $642.4 million, marginally lower than the $643.7 million reported at year-end 2024.

The company’s cash flow from operations showed a significant shift, registering a negative $2.9 million for the first quarter of 2025 compared to a positive $43.7 million in the same period of 2024. Inventory levels increased slightly to $79.2 million from $75.2 million at the end of 2024.

Strategic Initiatives

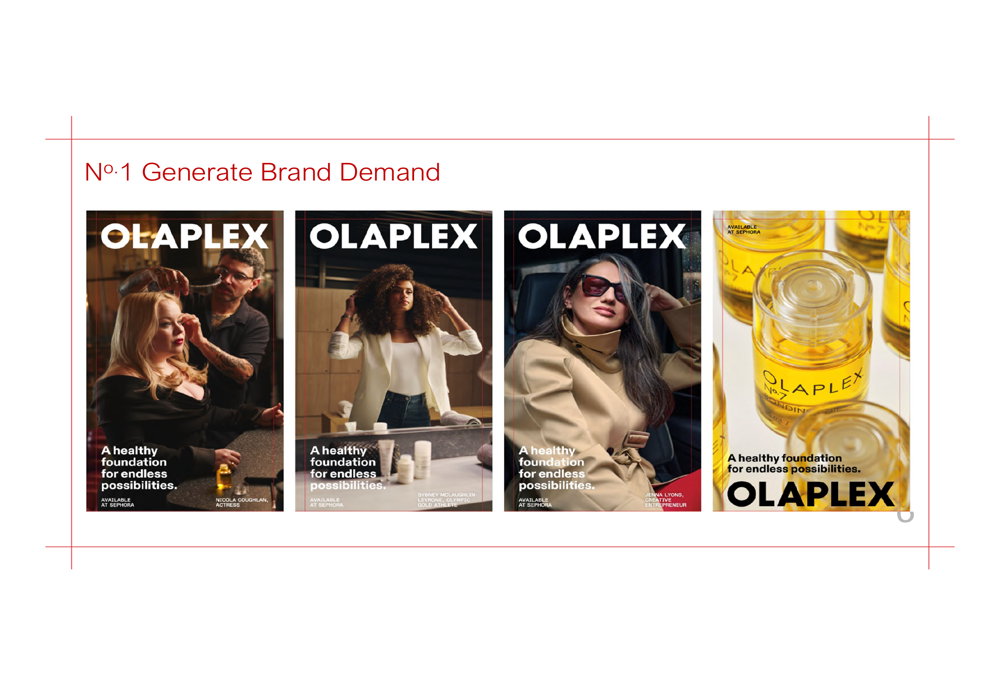

CEO Amanda Baldwin outlined the company’s strategic focus for 2025, centered around the "Bonds and Beyond" framework, which consists of three key pillars: generating brand demand, harnessing innovation, and executing with excellence.

To drive brand demand, Olaplex has expanded its celebrity partnerships, featuring Nicola Coughlan, Sydney McLaughlin-Levrone, and Jenna Lyons in its marketing campaigns. These partnerships aim to reinforce the brand’s positioning around "a healthy foundation for endless possibilities" and expand its reach across diverse consumer segments.

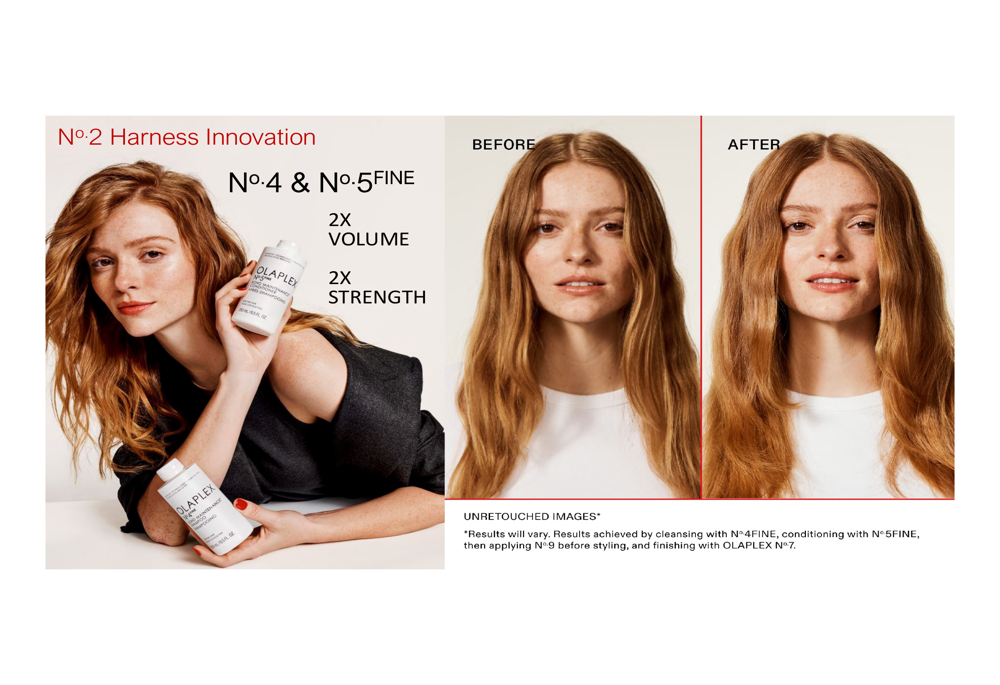

On the innovation front, the company highlighted its N°4 and N°5 FINE products, which promise "2X Volume" and "2X Strength." The presentation included before and after images demonstrating the products’ effects, part of Olaplex’s strategy to expand its product portfolio beyond its core bond-building technology.

Forward-Looking Statements

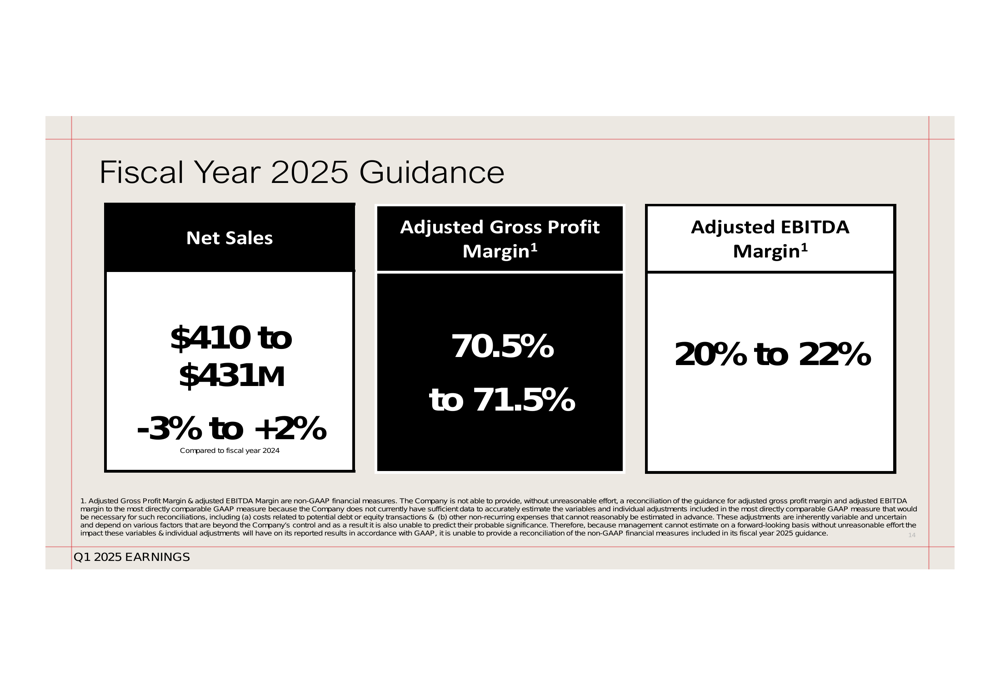

Despite the mixed Q1 results, Olaplex maintained its full-year 2025 guidance. The company expects net sales between $410 million and $431 million, representing a range from a 3% decline to a 2% increase compared to fiscal year 2024. Management also projects adjusted gross profit margins between 70.5% and 71.5%, and adjusted EBITDA margins of 20% to 22%.

During the earnings call, CEO Amanda Baldwin emphasized the resilience of the beauty category while acknowledging the company’s ongoing transformation. "Beauty is a resilient category," Baldwin stated, adding, "We’re in the middle of a transformation, and we’re really focused on our long-term goals."

CFO Catherine Dunleavy highlighted the company’s financial flexibility, noting, "We have the flexibility to invest straight through in turbulence," underscoring Olaplex’s commitment to maintaining strategic investments despite short-term challenges.

Analyst Perspectives

The market’s positive reaction to Olaplex’s results suggests investors are focusing on the company’s revenue performance rather than its profitability challenges. According to available data, analysts maintain a moderate outlook on the stock, with price targets ranging from $1.20 to $4.00.

Key risks identified include the continued decline in professional and direct-to-consumer channels, potential macroeconomic pressures affecting consumer spending, and increasing competition in the prestige hair care segment. However, the strong performance in specialty retail provides evidence that the company’s strategic initiatives may be gaining traction in certain distribution channels.

As Olaplex continues its transformation journey, investors will be watching closely for signs of stabilization in its challenged channels and for the company’s ability to translate its strategic initiatives into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.