Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Olaplex Holdings Inc (NASDAQ:OLPX) presented its second quarter 2025 earnings results on August 7, 2025, revealing a mixed performance with revenue growth but declining profitability. The premium hair care brand’s stock rose 3.19% to $1.46 during regular trading, with an additional 0.71% gain in pre-market activity, suggesting investors were cautiously optimistic about the company’s long-term transformation strategy despite near-term profitability challenges.

The results come as Olaplex continues to execute its "Bonds and Beyond" strategy, focusing on hair health and brand engagement while navigating significant channel shifts in its business model.

Quarterly Performance Highlights

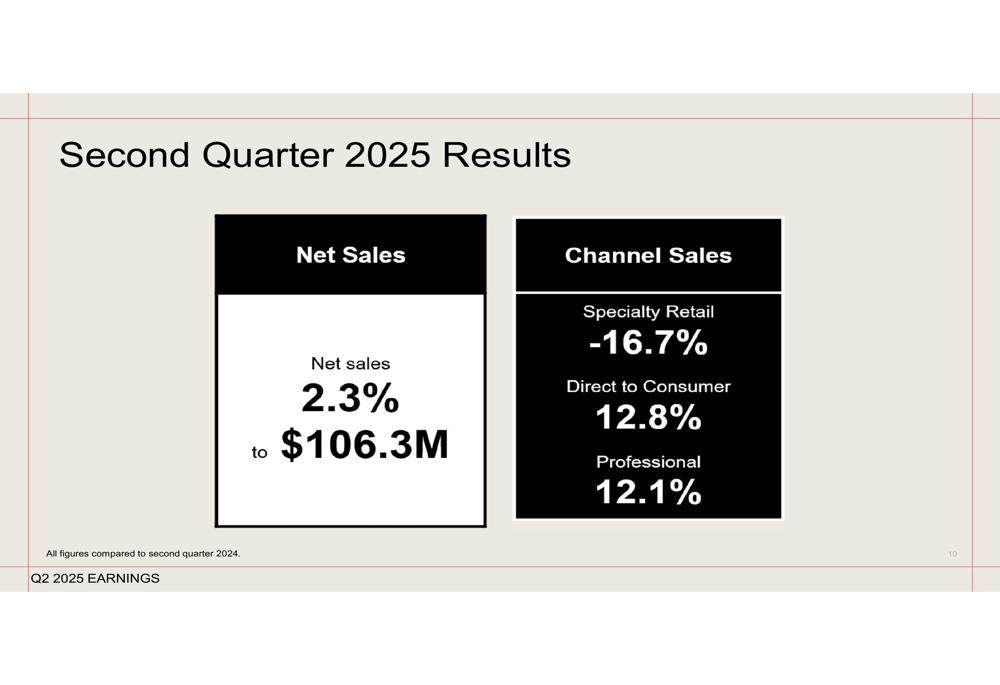

Olaplex reported Q2 2025 net sales of $106.3 million, representing a 2.3% increase compared to the same period in 2024. This marks a reversal from the 1.9% year-over-year decline reported in Q1 2025, suggesting the company’s strategic initiatives may be gaining traction.

However, the sales performance varied significantly across distribution channels. The company experienced a substantial 16.7% decline in specialty retail sales, while direct-to-consumer and professional channels showed strong growth of 12.8% and 12.1%, respectively. This represents a notable shift from Q1 2025, when specialty retail was the only growing channel.

As shown in the following quarterly sales breakdown:

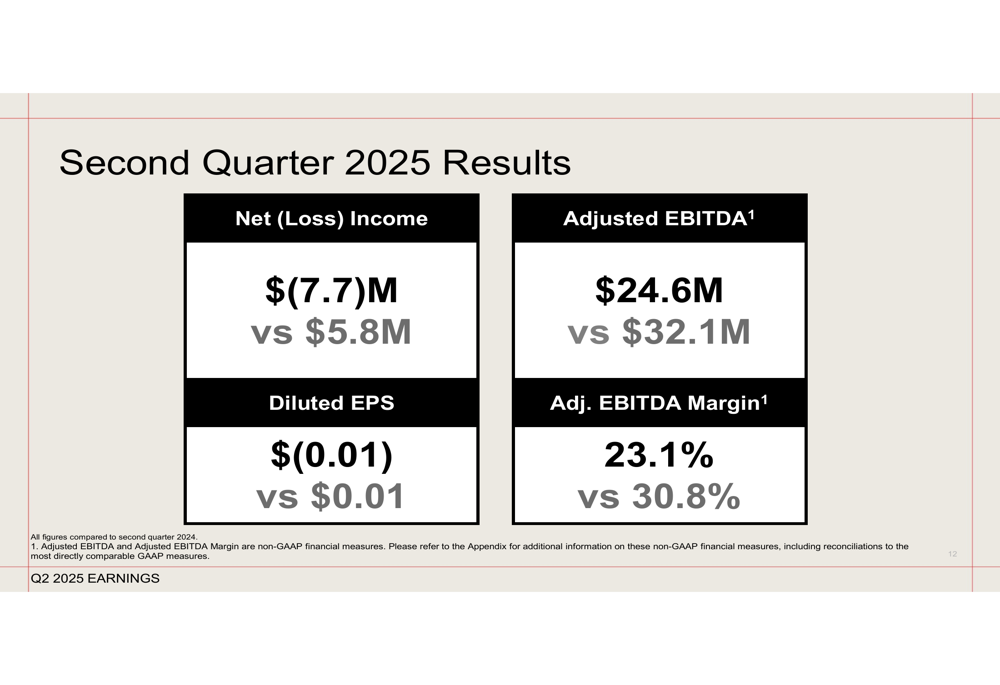

Despite the revenue growth, Olaplex’s bottom line deteriorated significantly. The company reported a net loss of $7.7 million, compared to a net income of $5.8 million in Q2 2024. Diluted earnings per share turned negative at $(0.01), down from $0.01 in the prior-year period. Adjusted EBITDA declined to $24.6 million from $32.1 million, with the adjusted EBITDA margin contracting to 23.1% from 30.8%.

The following slide illustrates these profitability metrics:

Detailed Financial Analysis

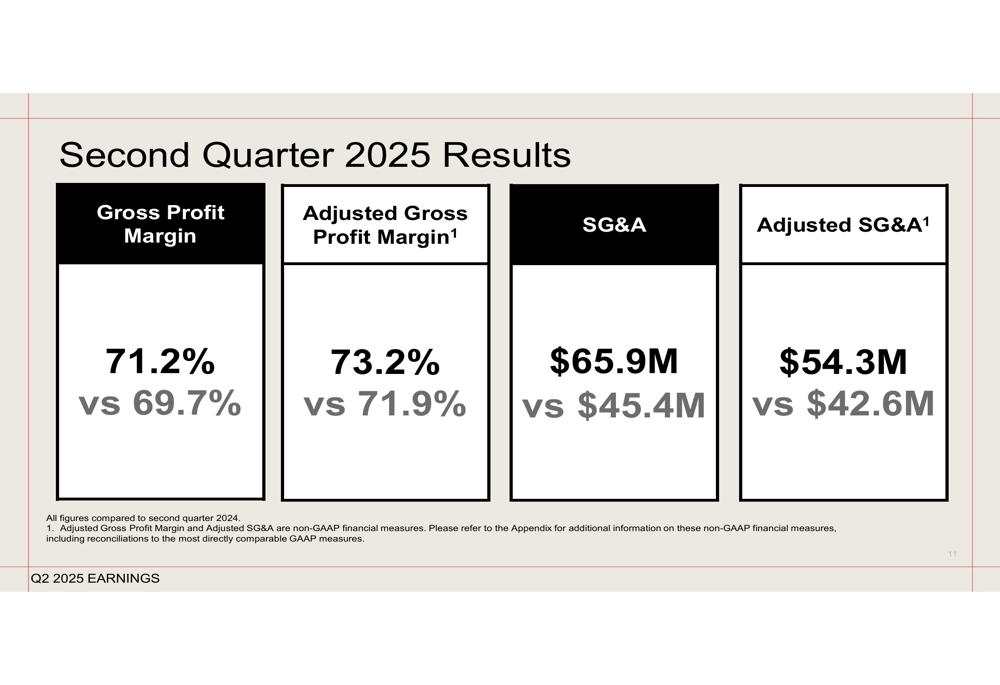

Olaplex’s gross profit margin improved to 71.2% from 69.7% in Q2 2024, while adjusted gross profit margin increased to 73.2% from 71.9%. However, this improvement was more than offset by a substantial increase in selling, general, and administrative expenses, which rose to $65.9 million from $45.4 million in the prior-year period. Even on an adjusted basis, SG&A expenses increased to $54.3 million from $42.6 million.

The following slide details these profitability and expense metrics:

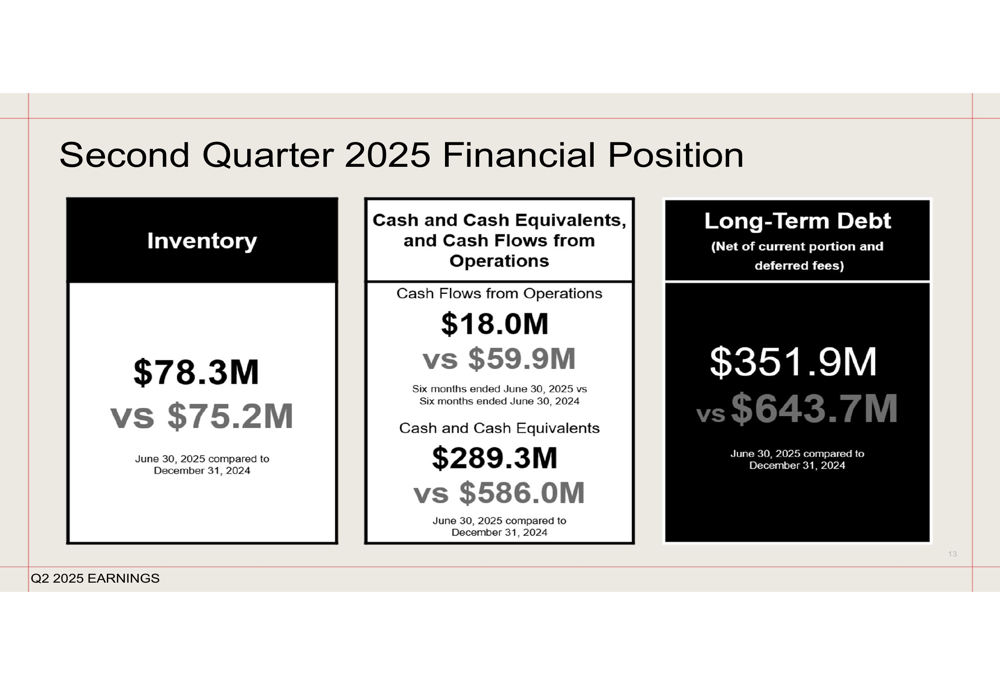

The company’s balance sheet showed significant changes compared to December 31, 2024. Cash and cash equivalents decreased substantially to $289.3 million from $586.0 million, while long-term debt was reduced to $351.9 million from $643.7 million. This suggests that Olaplex has used a significant portion of its cash reserves to pay down debt, continuing the debt reduction strategy mentioned in Q1 2025 when the company paid down $300 million in debt.

Cash flows from operations for the first six months of 2025 totaled $18.0 million, a substantial decrease from $59.9 million in the same period of 2024, reflecting the company’s increased investments and lower profitability.

The following slide provides details on the company’s financial position:

Strategic Initiatives

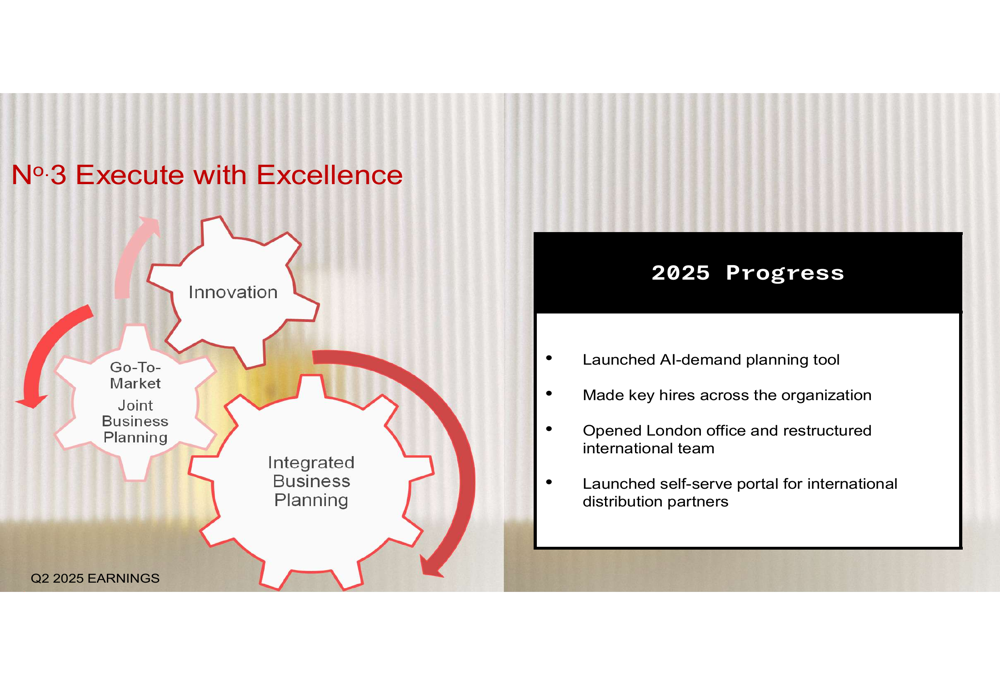

Olaplex’s presentation highlighted three key strategic focus areas for 2025: generating brand demand, harnessing innovation, and executing with excellence. These initiatives form the foundation of the company’s transformation strategy.

As illustrated in the company’s strategic framework:

On the innovation front, Olaplex introduced several new products, including Olaplex Nº-0.5 Scalp Longevity Treatment, Olaplex No.4 FINE Bond Maintenance Shampoo, and Olaplex No.5 FINE Bond Maintenance Conditioner. These additions aim to expand the company’s product portfolio and address specific consumer needs.

The company also reported progress on operational excellence initiatives, including the launch of an AI-demand planning tool, key hires across the organization, opening a London office with restructured international team, and the launch of a self-serve portal for international distribution partners.

As shown in the execution strategy slide:

CEO Amanda Baldwin, who was appointed earlier this year, emphasized the company’s focus on long-term transformation while navigating near-term challenges. The significant increase in SG&A expenses suggests substantial investments in marketing, innovation, and organizational capabilities to support future growth.

Forward-Looking Statements

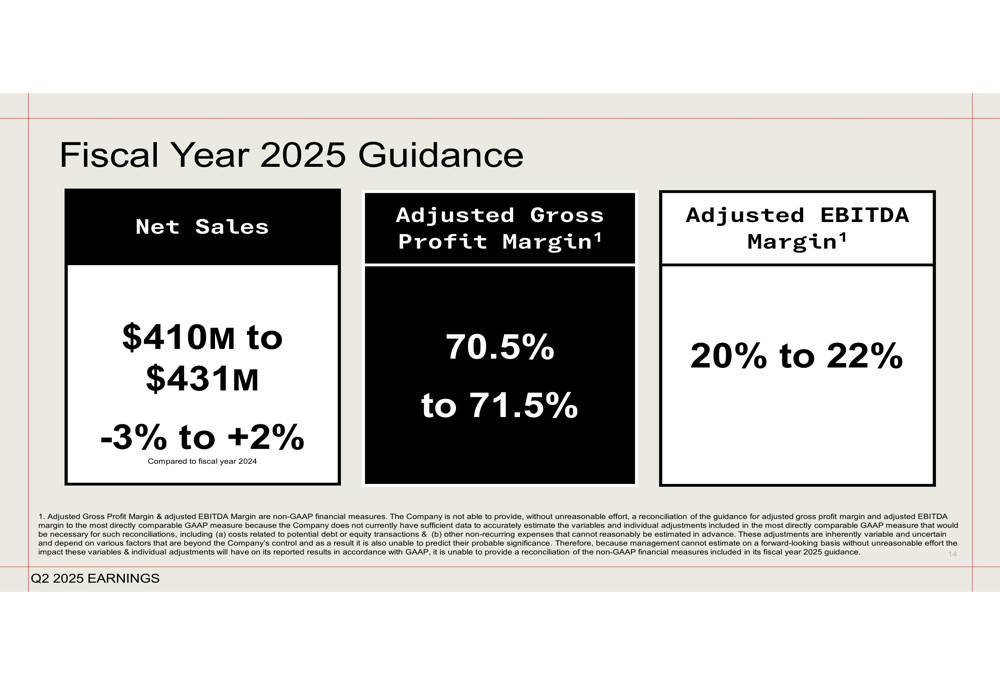

Despite the mixed quarterly results, Olaplex maintained its fiscal year 2025 guidance, projecting net sales between $410 million and $431 million, representing a range of -3% to +2% compared to fiscal year 2024. The company expects adjusted gross profit margin between 70.5% and 71.5% and adjusted EBITDA margin of 20% to 22%.

The following slide details the company’s full-year guidance:

This guidance suggests that Olaplex anticipates continued challenges in the second half of 2025, with full-year sales potentially declining despite the positive Q2 results. The projected adjusted EBITDA margin of 20-22% also represents a significant contraction from the 23.1% reported in Q2 and the 30.8% from Q2 2024, indicating that the company expects continued pressure on profitability as it invests in its transformation initiatives.

As Olaplex continues to navigate its strategic transformation, investors will be watching closely to see if the revenue growth momentum can be maintained while the company works to address profitability challenges and optimize its channel mix in the competitive premium hair care market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.