Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Omnicell Inc (NASDAQ:OMCL) shares surged 14.48% in premarket trading to $34.00 following the release of its Q2 2025 investor presentation on July 31, 2025. The medication management technology provider reported a 5% year-over-year revenue increase to $291 million, though its Non-GAAP EBITDA declined 4% compared to the same period last year. This positive market reaction marks a significant reversal from the 13.74% stock drop following Q1 results, suggesting investors are encouraged by the company’s strategic transformation toward recurring revenue streams.

Quarterly Performance Highlights

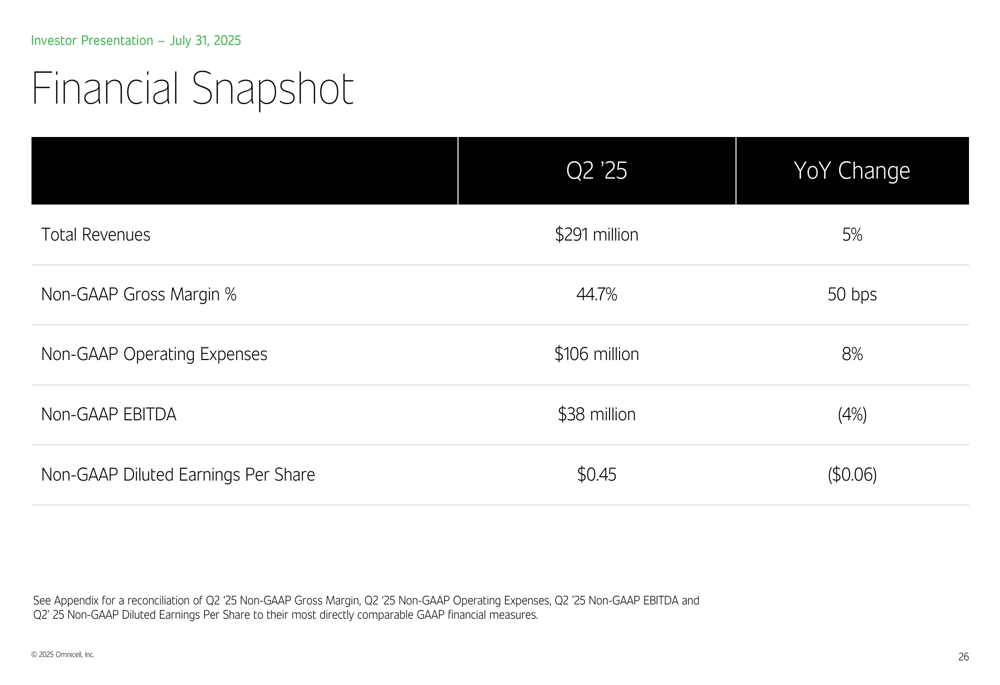

Omnicell’s Q2 2025 financial results showed mixed performance with revenue growth offset by a slight decline in profitability. The company achieved a 5% year-over-year revenue increase to $291 million, while Non-GAAP gross margin improved by 50 basis points to 44.7%. However, Non-GAAP EBITDA decreased 4% to $38 million, and Non-GAAP diluted earnings per share fell $0.06 to $0.45 compared to Q2 2024.

As shown in the following financial snapshot from the company’s presentation:

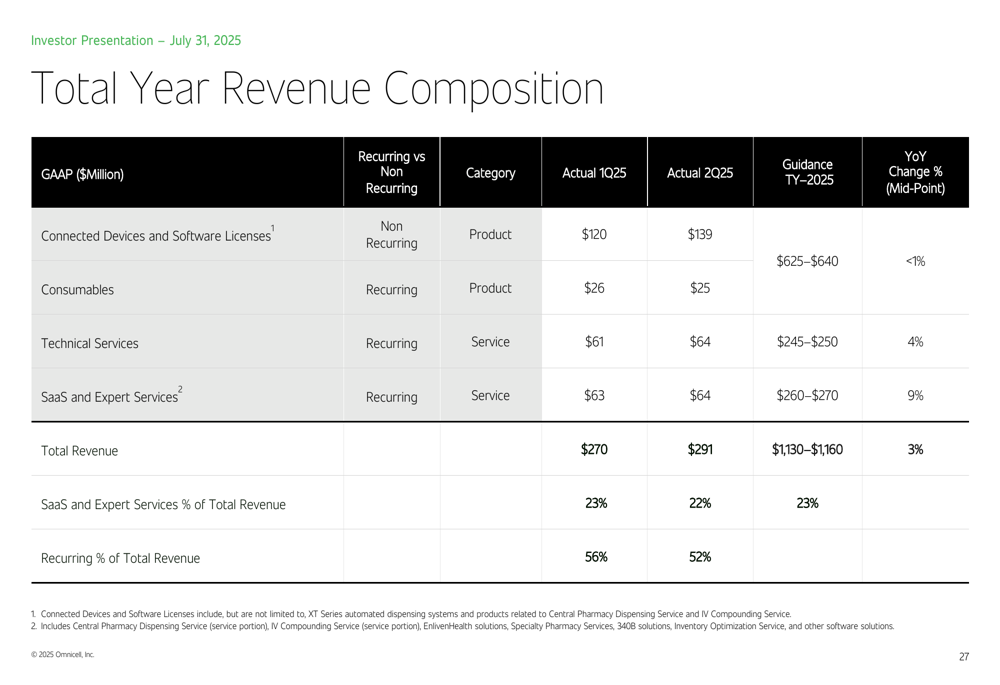

The revenue composition for 2025 reveals Omnicell’s continued shift toward recurring revenue streams. The company now categorizes its revenue into Connected Devices and Software (ETR:SOWGn) Licenses, Consumables, Technical Services, and SaaS and Expert Services. For the full year 2025, Omnicell expects Connected Devices and Software Licenses revenue of $625-$640 million (less than 1% YoY growth), while SaaS and Expert Services revenue is projected to reach $260-$270 million (9% YoY growth).

This revenue breakdown illustrates the company’s strategic pivot:

Strategic Initiatives

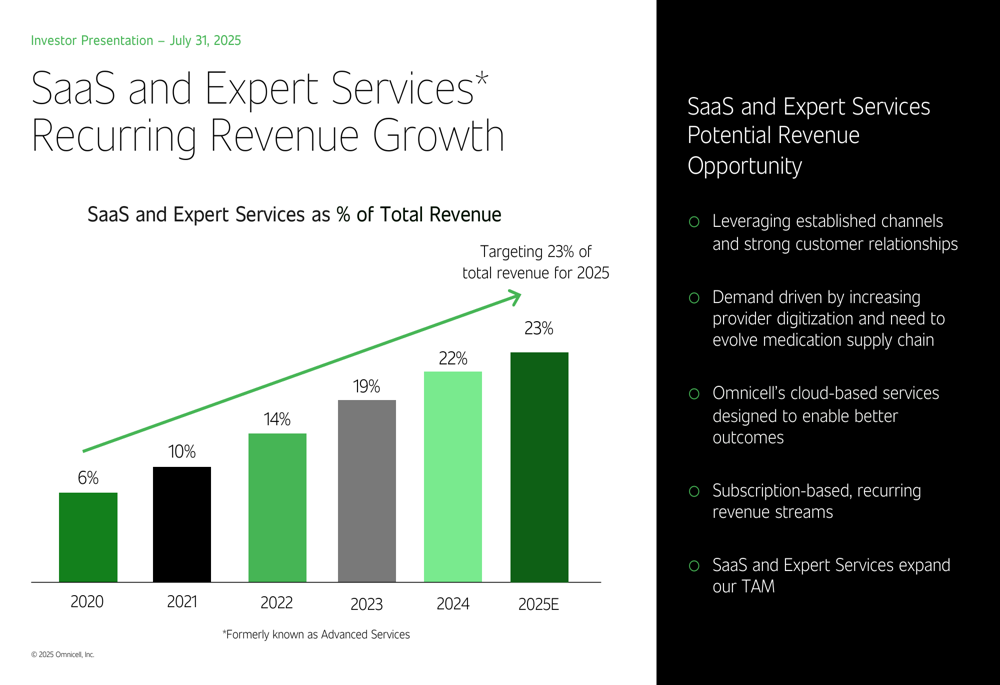

Omnicell’s presentation emphasized its transformation toward recurring revenue streams, particularly through SaaS and Expert Services. This category has grown dramatically from just 6% of total revenue in 2020 to a projected 23% in 2025, creating a more stable and predictable revenue base.

The following chart illustrates this strategic shift:

The company highlighted several investment strengths, including its established position serving more than half of the top 300 U.S. health systems and its 30-year track record in medication management. Omnicell’s product backlog stands at $647 million, with Annual Recurring Revenue reaching $580 million as of December 31, 2024, providing visibility into future revenue streams.

As shown in the company’s investment highlights:

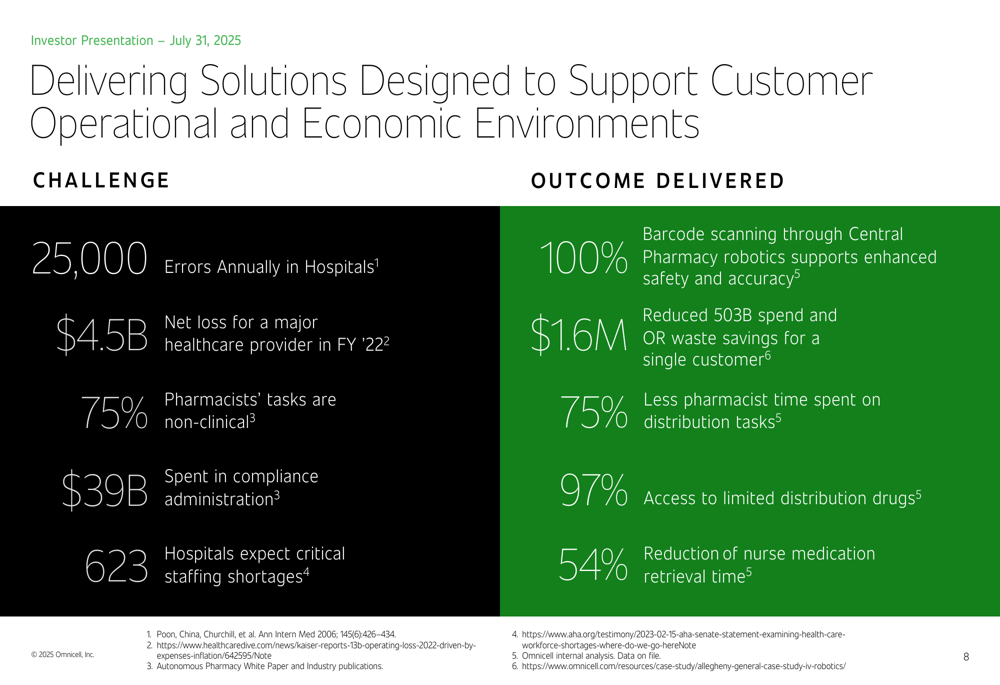

Omnicell’s value proposition centers on addressing critical healthcare challenges through automation and technology. The company claims its solutions can help reduce medication errors, decrease waste, improve regulatory compliance, and allow pharmacists to focus more on clinical activities rather than administrative tasks.

The following slide quantifies both the challenges faced by healthcare providers and the outcomes delivered by Omnicell’s solutions:

Innovation Pipeline

Omnicell’s presentation showcased several innovations launched in 2024 and planned for 2025. The 2024 innovations include XT Amplify (enhancing pharmacy and nursing efficiency), Central Med Automation Service (centralizing medication management), and OmniSphere (a cloud-native software platform).

For 2025, the company previewed MedVision, a web-enabled software solution for outpatient clinic inventory management, and MedTrack-OR, an RFID-enabled drawer working with Omnicell’s Anesthesia Workstation to automatically track medications in operating rooms.

These innovations align with Omnicell’s "Autonomous Pharmacy" vision, which aims to replace manual, error-prone activities with automated processes to achieve zero medication errors, zero waste, and 100% regulatory compliance.

Forward-Looking Statements

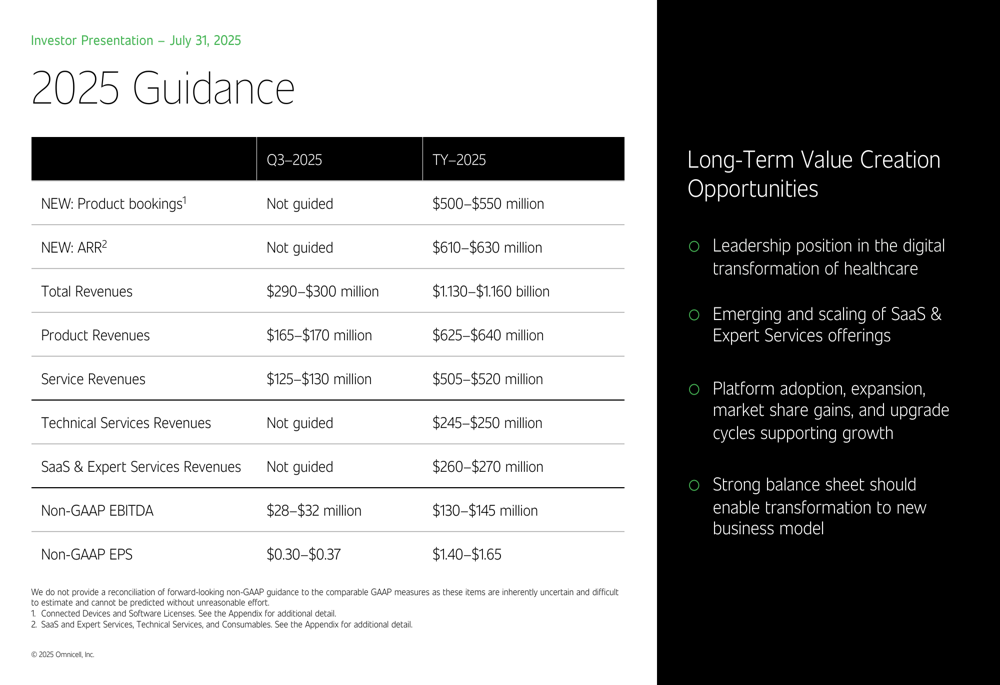

Omnicell provided detailed guidance for both Q3 and the full year 2025. For the full year, the company expects:

This guidance represents modest growth compared to 2024, with total revenues projected between $1.130-$1.160 billion. The company’s Non-GAAP EBITDA is expected to range from $130-$145 million, with Non-GAAP EPS between $1.40-$1.65.

Notably, these projections come after Omnicell mentioned in its Q1 earnings call that tariff impacts could affect Non-GAAP EBITDA by approximately $40 million in 2025, suggesting the company is navigating supply chain challenges while maintaining its growth trajectory.

Conclusion

Omnicell’s Q2 2025 presentation reveals a company in strategic transition, gradually shifting from a hardware-centric business model to one with a growing proportion of recurring revenue. While the 5% revenue growth and slight EBITDA decline show mixed short-term results, the market’s positive reaction suggests confidence in the company’s long-term strategy.

With a substantial product backlog, growing recurring revenue base, and continued innovation in medication management automation, Omnicell appears positioned to capitalize on healthcare providers’ increasing need for efficiency and error reduction. However, challenges remain, including tariff impacts and the need to maintain growth in an increasingly competitive healthcare technology landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.