Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

OneMain Holdings Inc. (NYSE:OMF) presented its first quarter 2025 financial results on April 29, 2025, showing significant improvement across key metrics compared to both the previous quarter and the same period last year. The company, which positions itself as the lender of choice for nonprime consumers, reported diluted earnings per share (EPS) of $1.78, representing a 70% increase from $1.05 in Q4 2024 and a 38% improvement from $1.29 in Q1 2024.

The strong performance comes after a challenging 2024, which management had previously characterized as a "cyclical low in earnings." The latest results suggest OneMain is executing effectively on its recovery strategy, with shares trading at $49.15 as of the previous close, up 0.74% but still well below the company’s 52-week high of $58.90.

Quarterly Performance Highlights

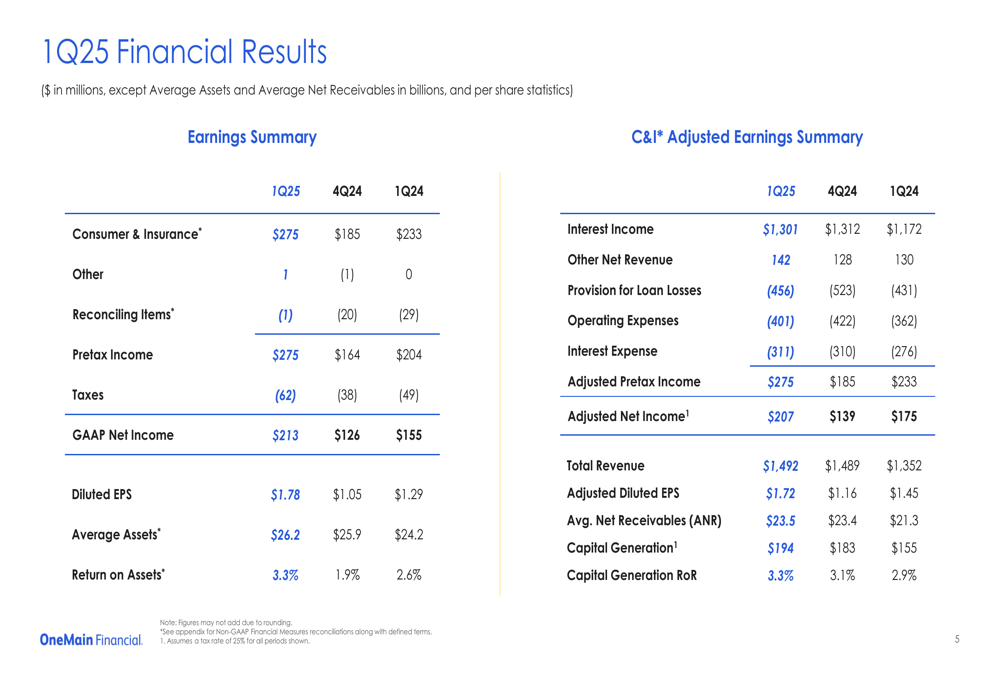

OneMain reported GAAP net income of $213 million for Q1 2025, a substantial increase from $126 million in Q4 2024 and $155 million in Q1 2024. The company’s Consumer & Insurance (C&I) segment generated total revenue of $1.5 billion, up 10% year-over-year.

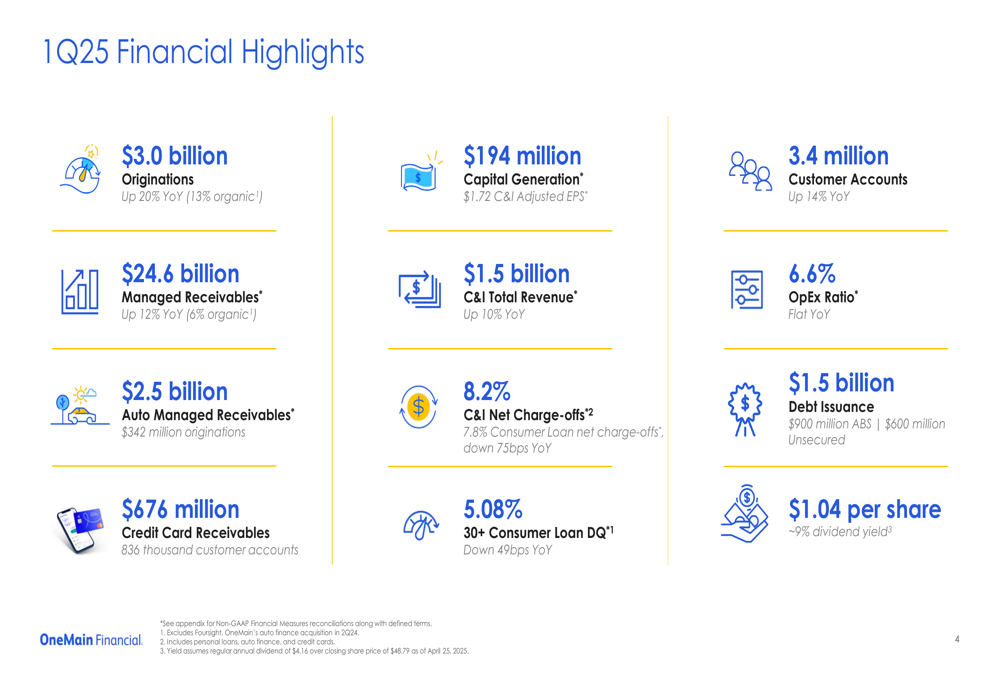

As shown in the following comprehensive overview of key financial metrics:

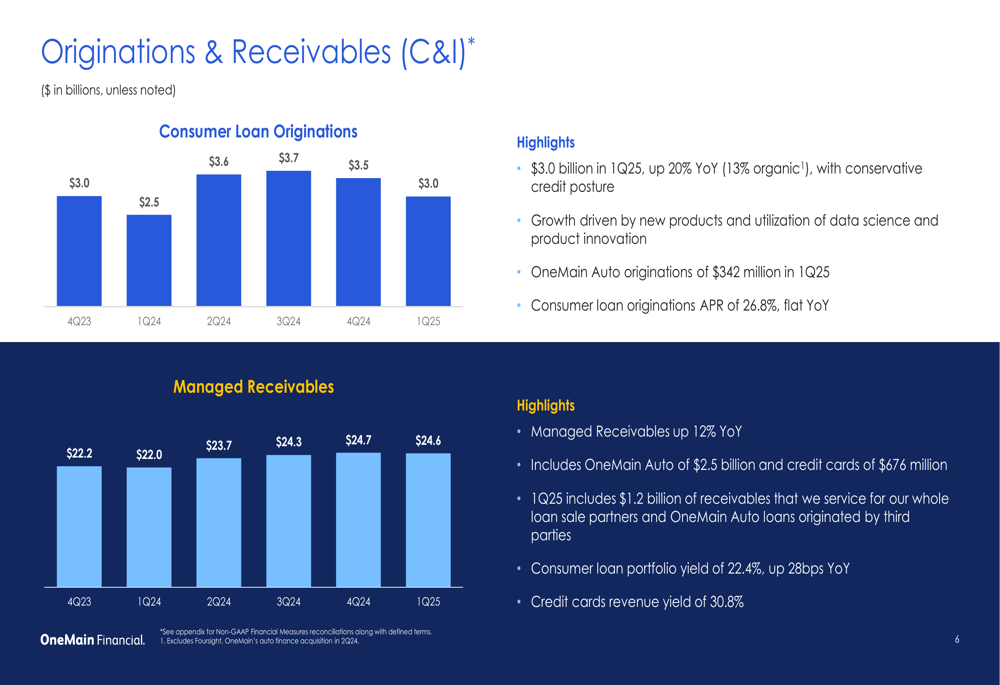

Loan originations reached $3.0 billion in the quarter, representing a 20% increase year-over-year (13% organic growth). Managed receivables grew to $24.6 billion, up 12% compared to Q1 2024, with 6% coming from organic growth. The company’s customer base expanded to 3.4 million accounts, a 14% increase from the previous year.

The detailed financial results summary further illustrates the company’s improving performance trajectory:

Capital generation for the quarter was $194 million, translating to $1.72 C&I Adjusted EPS. The company maintained its operating expense ratio at 6.6%, despite continued investments in the business and integration of recent acquisitions.

Credit Quality Improvements

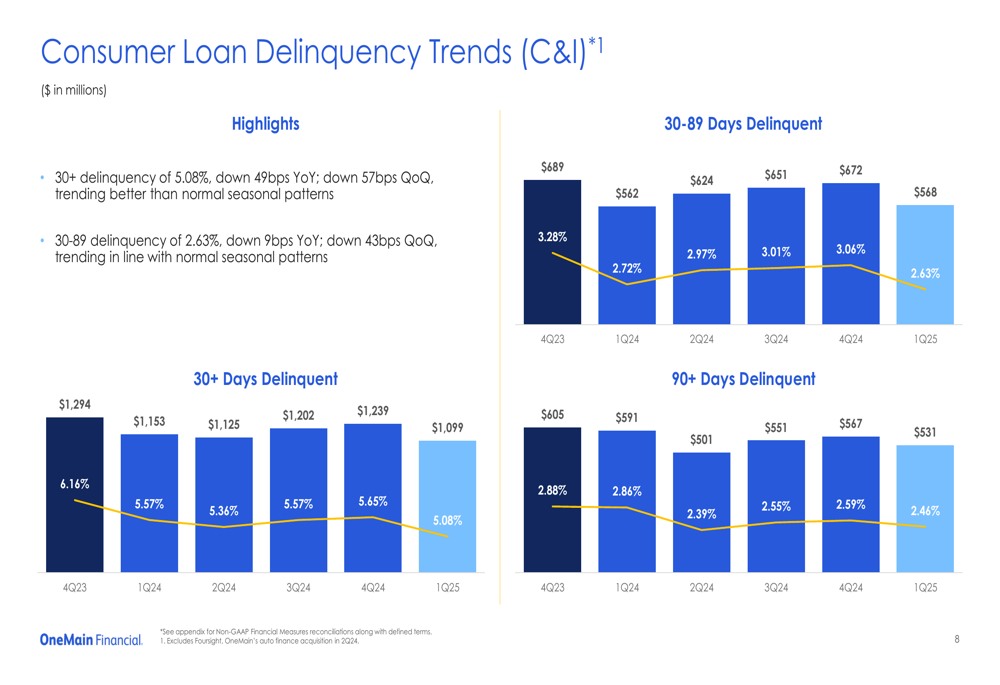

A key highlight of OneMain’s Q1 2025 results was the significant improvement in credit quality metrics. The 30+ day consumer loan delinquency rate decreased to 5.08%, down 49 basis points year-over-year and 57 basis points quarter-over-quarter, trending better than normal seasonal patterns.

The following chart illustrates the positive trend in delinquency rates:

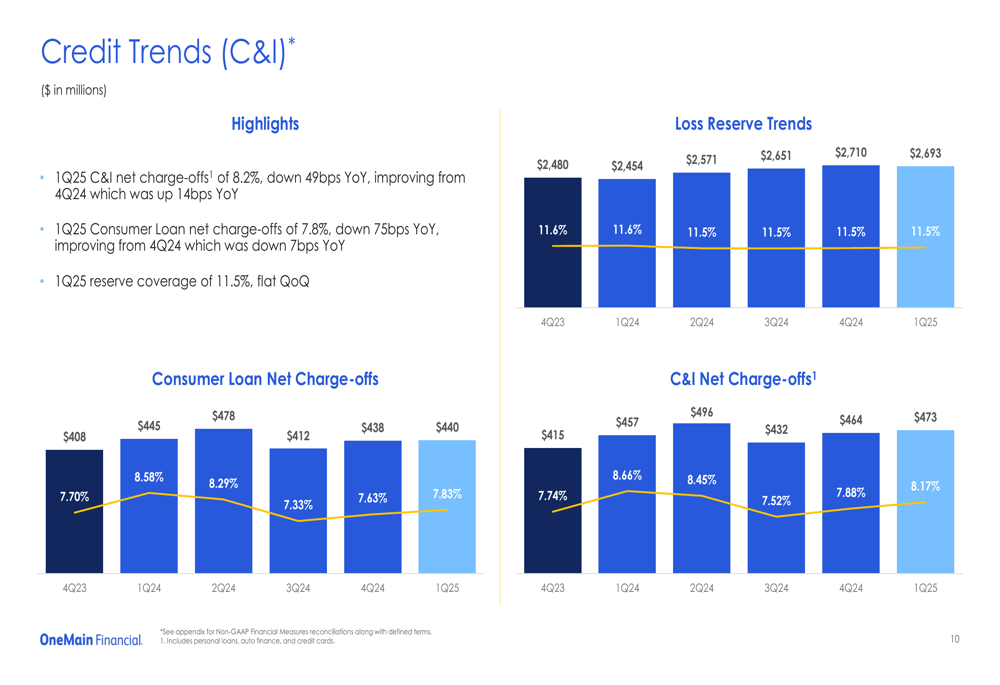

Net charge-offs in the C&I segment were 8.2% for Q1 2025, down 49 basis points year-over-year, while consumer loan net charge-offs specifically improved to 7.8%, down 75 basis points from Q1 2024. The company maintained its loss reserve coverage at 11.5% of receivables, unchanged from the previous quarter.

The credit trends chart below shows the stabilization of charge-offs and reserves:

Management attributed the improving credit performance to their credit tightening initiatives, with the "front book" (loans originated after credit tightening) now comprising 87% of the portfolio while contributing only 73% of delinquent receivables. The "back book" (pre-tightening loans) accounts for just 13% of receivables but 27% of delinquencies.

Product Diversification Strategy

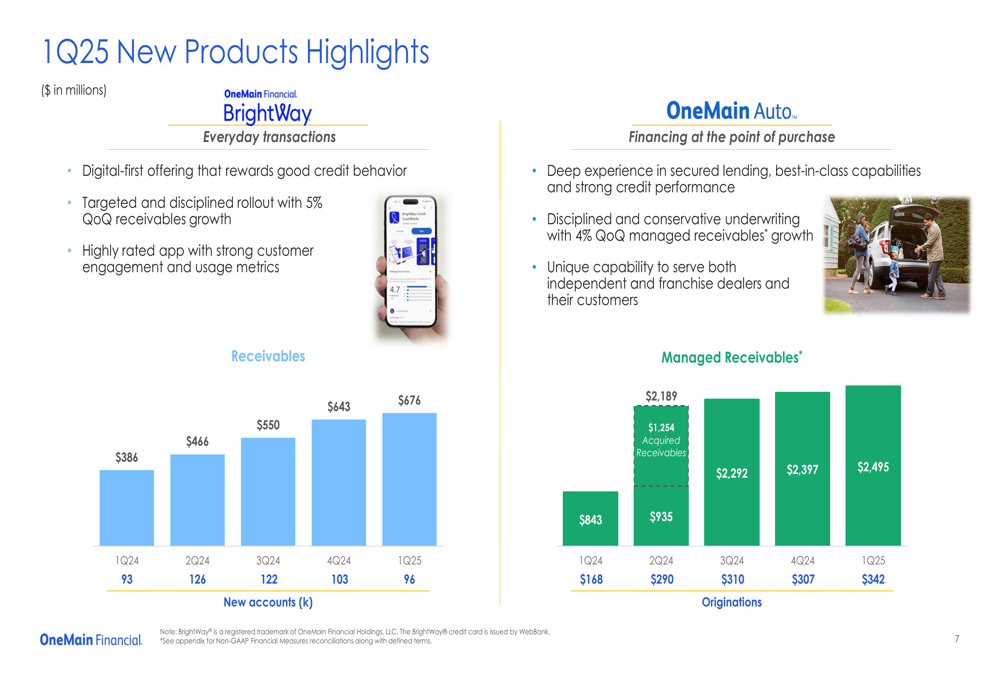

OneMain continues to execute on its diversification strategy beyond traditional personal loans. The company reported strong growth in its newer product lines, including auto financing and credit cards.

As illustrated in the following originations and receivables chart:

Auto managed receivables reached $2.5 billion with $342 million in originations during Q1 2025, representing continued growth in this segment. Meanwhile, credit card receivables under the BrightWay brand grew to $676 million with 836,000 customer accounts.

The detailed breakdown of new product performance demonstrates the success of these initiatives:

BrightWay credit card receivables grew 5% quarter-over-quarter and 75% year-over-year, with a revenue yield of 30.8%. OneMain Auto showed 4% quarter-over-quarter growth in managed receivables, with originations increasing to $342 million in Q1 2025 compared to $168 million in Q1 2024.

Balance Sheet & Capital Allocation

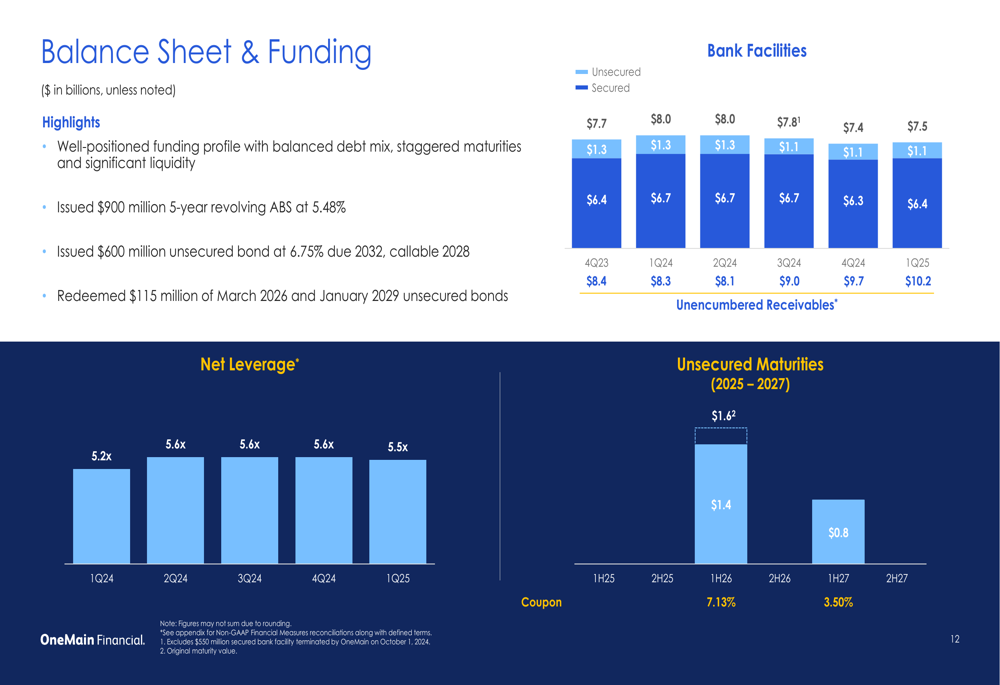

OneMain maintained a strong balance sheet with a well-structured funding profile. The company issued $1.5 billion in debt during the quarter, including $900 million in asset-backed securities (ABS) at 5.48% and $600 million in unsecured bonds at 6.75% due 2032 (callable in 2028).

The following chart illustrates the company’s balanced funding mix:

The company’s capital allocation framework prioritizes business investment, regular dividends, and share repurchases. OneMain declared a quarterly dividend of $1.04 per share, representing an approximately 9% yield at the current share price. Additionally, the company repurchased 323,000 shares for $16 million during the quarter.

Forward-Looking Statements

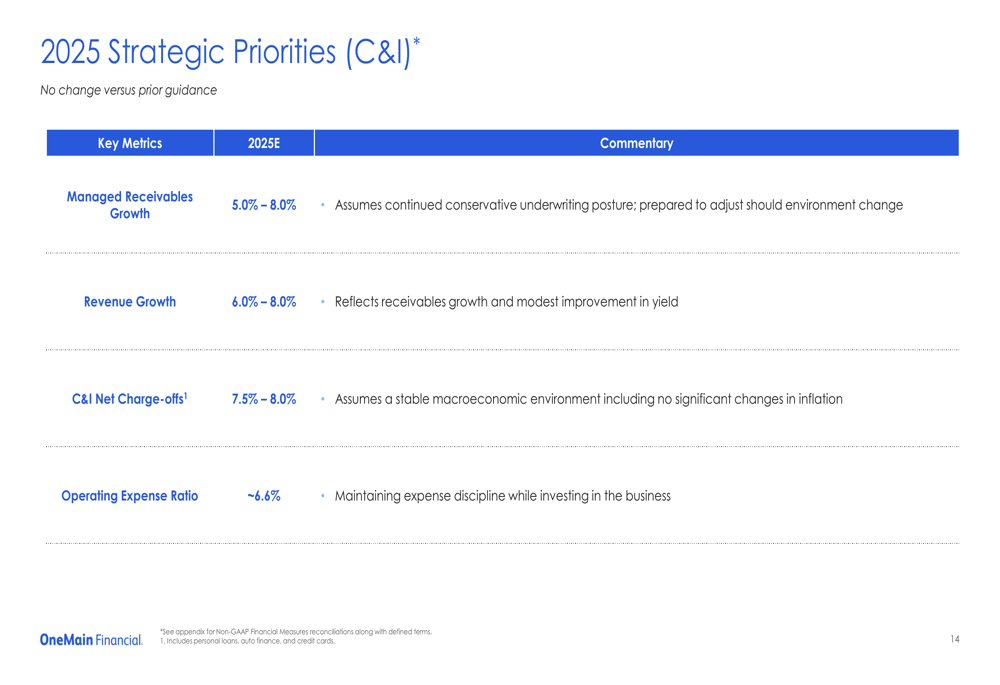

Looking ahead to the remainder of 2025, OneMain outlined its strategic priorities with specific guidance metrics:

The company expects managed receivables growth of 5-8% and revenue growth of 6-8% for the full year 2025. Net charge-offs are projected to range between 7.5-8.0%, assuming a stable macroeconomic environment. The operating expense ratio is expected to remain at approximately 6.6% as the company maintains expense discipline while continuing to invest in the business.

These projections align with management’s previous statements that 2024 represented a cyclical low point, with an upward trajectory in earnings and capital generation expected in 2025 and beyond. The improving credit metrics and growing diversification into new product lines provide a foundation for this optimistic outlook, though the company remains cautious about potential macroeconomic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.