Stock market today: S&P 500 falls as job cuts stoke economic fears, tech stutters

OneMain Holdings Inc (NYSE:OMF) released its third quarter 2025 financial results on October 31, 2025, showcasing robust performance across key metrics. The company, which positions itself as a leading lender for nonprime consumers, reported significant earnings growth, improved credit metrics, and continued expansion of its newer product offerings.

Quarterly Performance Highlights

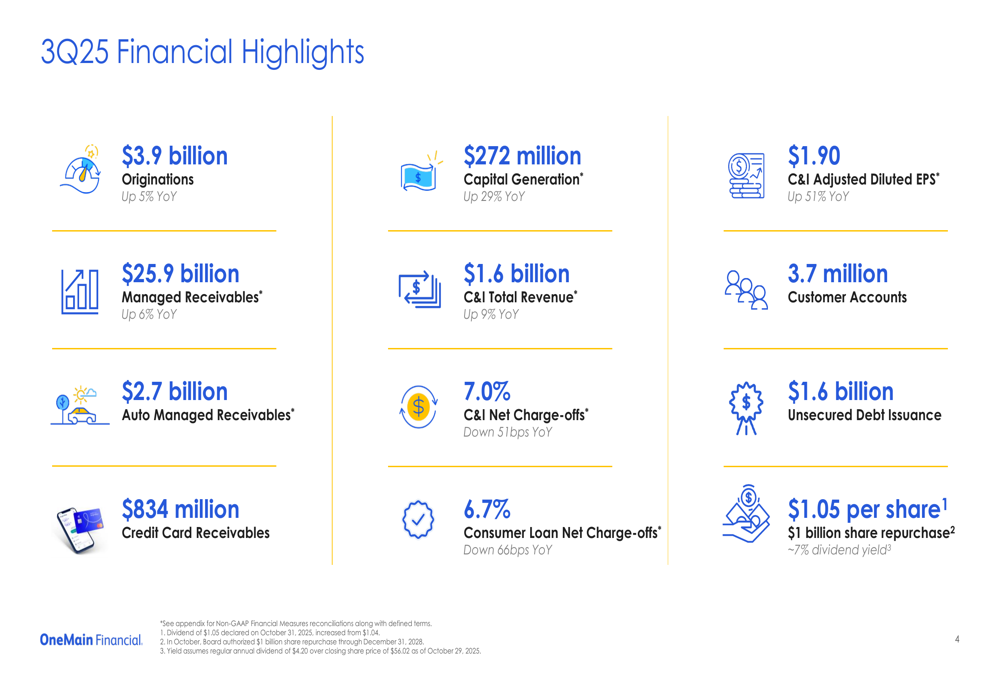

OneMain delivered strong financial results in Q3 2025, with adjusted diluted earnings per share reaching $1.90, representing a 51% increase year-over-year and significantly exceeding analyst expectations of $1.61. The company reported $1.6 billion in total revenue, up 9% compared to the same period last year.

The company’s originations remained strong at $3.9 billion, a 5% increase from Q3 2024, while managed receivables grew to $25.9 billion, up 6% year-over-year. Capital generation, a key metric for the company, increased by 29% year-over-year to $272 million.

As shown in the following comprehensive financial highlights slide, OneMain demonstrated growth across multiple dimensions:

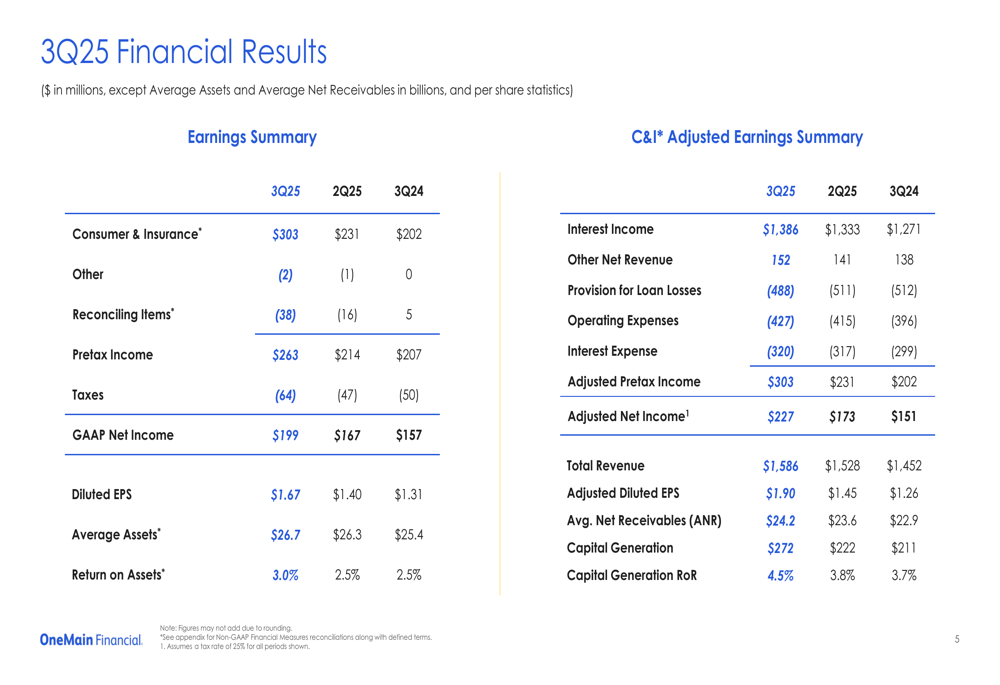

In the detailed earnings summary, the company reported GAAP net income of $199 million, up from $157 million in Q3 2024, representing a 27% increase. Return on assets improved to 3.0%, up from 2.5% in both the previous quarter and the same quarter last year.

Credit Performance & Portfolio Quality

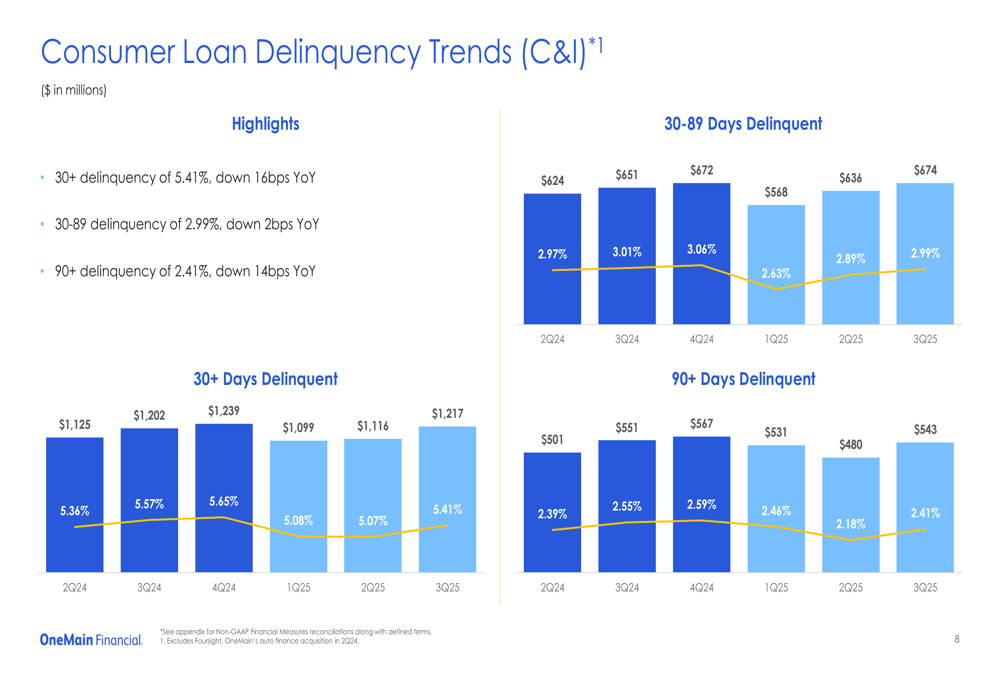

A notable aspect of OneMain’s Q3 performance was the improvement in credit metrics. Consumer loan net charge-offs decreased to 6.7%, down 66 basis points year-over-year, while overall C&I net charge-offs declined to 7.0%, a 51 basis point improvement from Q3 2024.

The company’s 30+ day delinquency rate decreased to 5.41%, down 16 basis points year-over-year, with particularly strong improvement in the 90+ day delinquency category, which declined 14 basis points to 2.41%.

The following chart illustrates these delinquency trends:

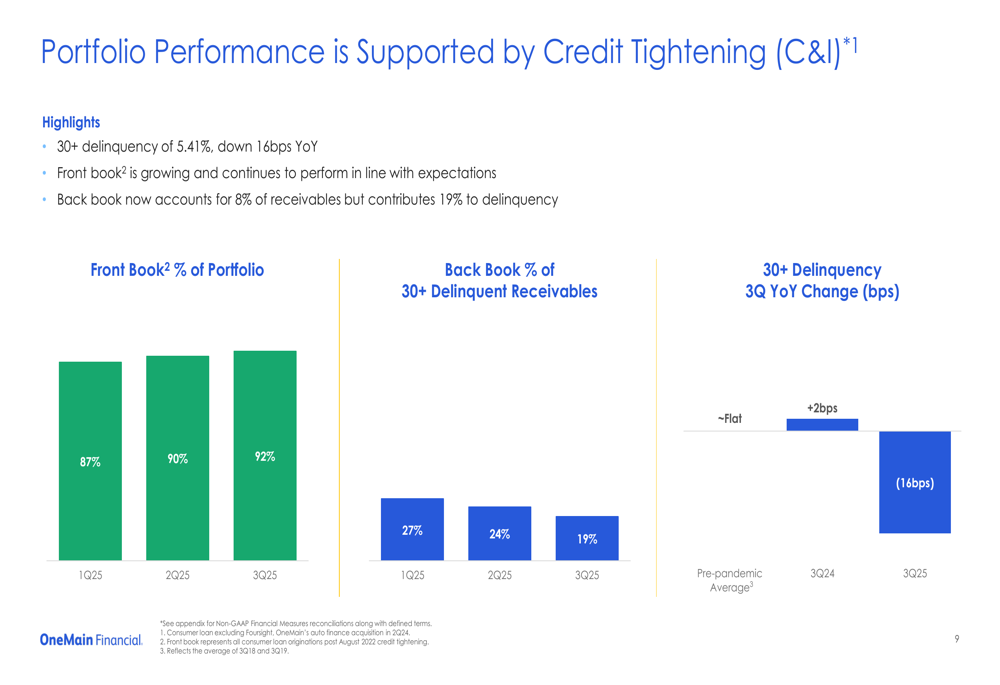

OneMain attributed the improving credit performance to its strategic credit tightening initiatives. The company noted that its "front book" of newer loans now comprises 92% of the portfolio but contributes only 81% to delinquencies, while the remaining "back book" accounts for 8% of receivables but 19% of delinquencies.

Despite the improving credit metrics, OneMain maintained its loss reserve coverage at 11.5%, unchanged year-over-year, demonstrating continued prudence in its approach to credit risk.

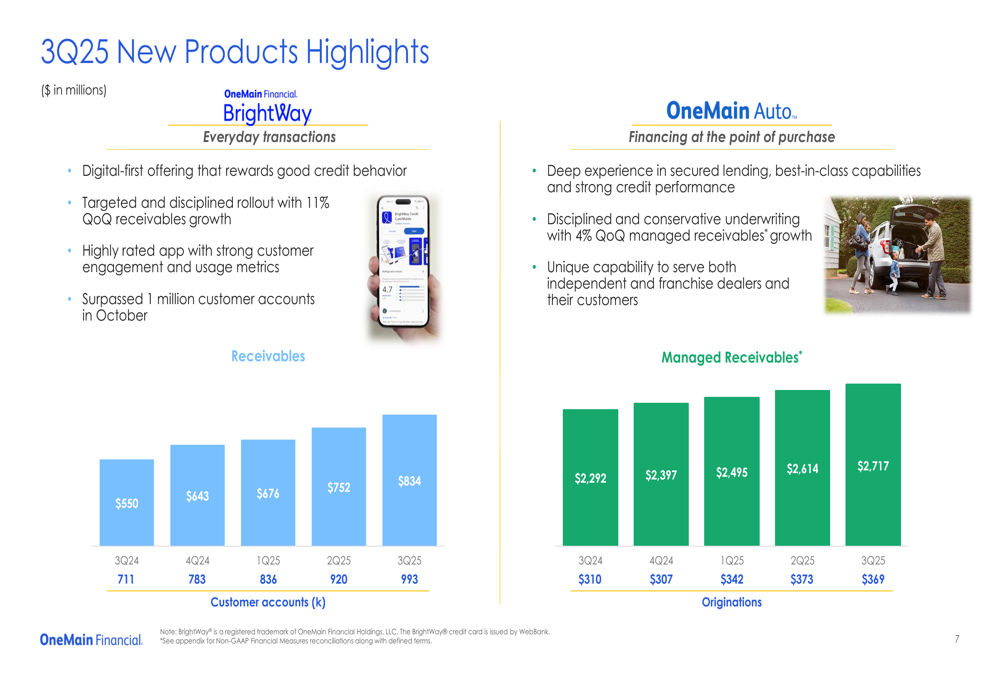

New Product Growth Initiatives

OneMain continued to make progress on its strategic diversification into new product categories. The BrightWay credit card business showed strong momentum, with receivables growing to $834 million, up 11% quarter-over-quarter and 52% year-over-year. The product reached a significant milestone in October, surpassing one million customer accounts.

Similarly, the OneMain Auto business demonstrated steady growth, with managed receivables increasing to $2.7 billion, up 4% quarter-over-quarter and 19% year-over-year. The company emphasized its disciplined and conservative underwriting approach in this segment.

The following slide details the performance of these new product initiatives:

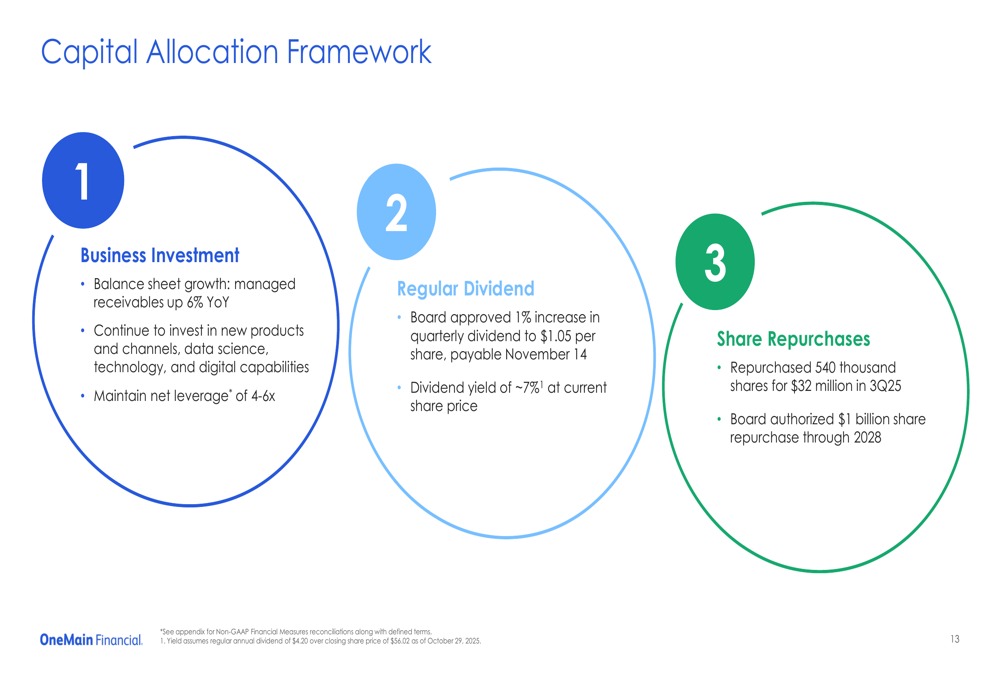

Capital Allocation & Shareholder Returns

OneMain enhanced its shareholder return program in Q3, with the board approving a 1% increase in the quarterly dividend to $1.05 per share, representing a yield of approximately 7% at current share prices. Additionally, the board authorized a new $1 billion share repurchase program through 2028.

During the quarter, the company repurchased 540,000 shares for $32 million. OneMain also strengthened its balance sheet by issuing $750 million in unsecured bonds at 6.13% due 2030 and $800 million at 6.50% due 2033, using part of the proceeds to redeem higher-cost debt.

The company’s capital allocation framework prioritizes business investment, regular dividends, and share repurchases, as illustrated in the following slide:

Forward Guidance & Strategic Priorities

OneMain updated its 2025 strategic priorities, narrowing its managed receivables growth guidance to 6-8% (from the previous 5-8%) and projecting revenue growth of approximately 9%, at the high end of its original 6-8% range. The company maintained its net charge-off guidance of 7.5-7.8% and operating expense ratio target of approximately 6.6%.

In the earnings call, CEO Doug Shulman emphasized the company’s long-term strategy, stating, "We built our business for the long run with best-in-class credit management and a fortress balance sheet." CFO Jenny Osterhout noted that the company continues to evaluate strategic opportunities.

The market responded positively to OneMain’s results, with the stock rising 5.11% in pre-market trading to $58.60, approaching its 52-week high of $63.25. This performance continues the company’s trend of exceeding market expectations, with the Q3 EPS representing an 18.01% positive surprise compared to analyst forecasts.

As OneMain continues to execute on its vision of being the lender of choice for nonprime consumers, its diversified product strategy and improving credit performance position the company for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.