Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

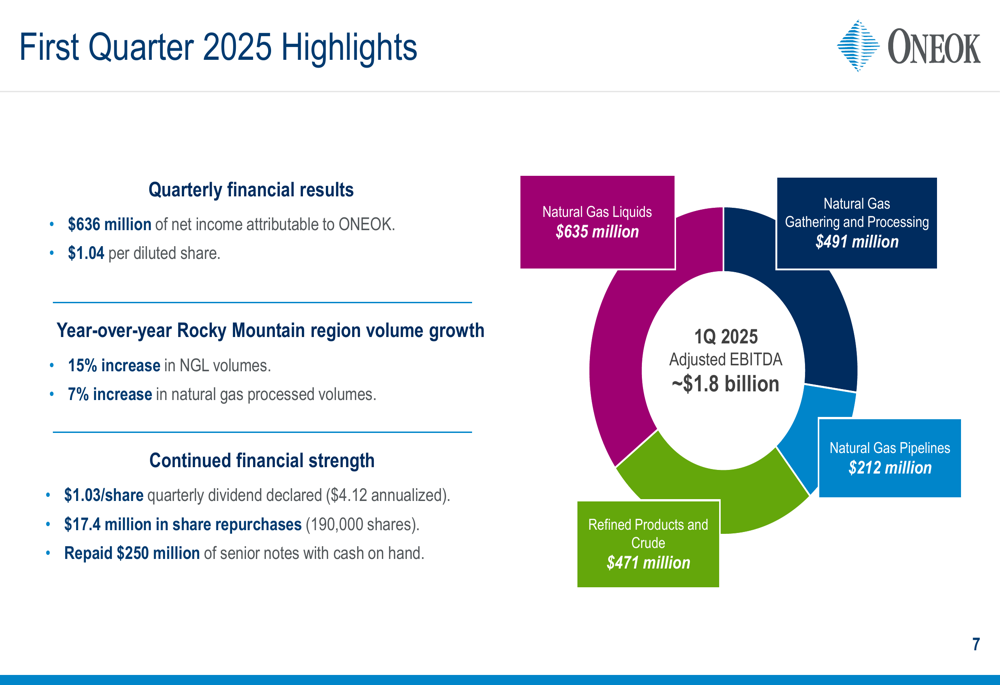

ONEOK Inc. (NYSE:OKE), a premier energy infrastructure company, reported first quarter 2025 net income of $636 million, or $1.04 per diluted share, according to its Q1 2025 presentation released on April 30. The company continues to demonstrate resilience and growth through its increasingly diversified business model spanning natural gas liquids, natural gas gathering and processing, and refined products and crude oil transportation.

The company has evolved from a primarily NGL-focused business to a more balanced energy infrastructure provider following strategic acquisitions, including Magellan, EnLink, and Medallion. This transformation has positioned ONEOK to capitalize on growing demand across multiple energy sectors while maintaining its 11-year streak of adjusted EBITDA growth.

Quarterly Performance Highlights

ONEOK reported first quarter 2025 adjusted EBITDA of approximately $1.8 billion, with contributions from all business segments. The company declared a quarterly dividend of $1.03 per share ($4.12 annualized) and repurchased 190,000 shares for $17.4 million during the quarter, demonstrating its commitment to shareholder returns while maintaining financial discipline.

The company also reported strong year-over-year volume growth in the Rocky Mountain region, with NGL volumes increasing 15% and natural gas processed volumes up 7%. Additionally, ONEOK repaid $250 million of senior notes with cash on hand, further strengthening its balance sheet.

As shown in the following chart of ONEOK’s adjusted EBITDA by segment for Q1 2025:

Business Segment Performance

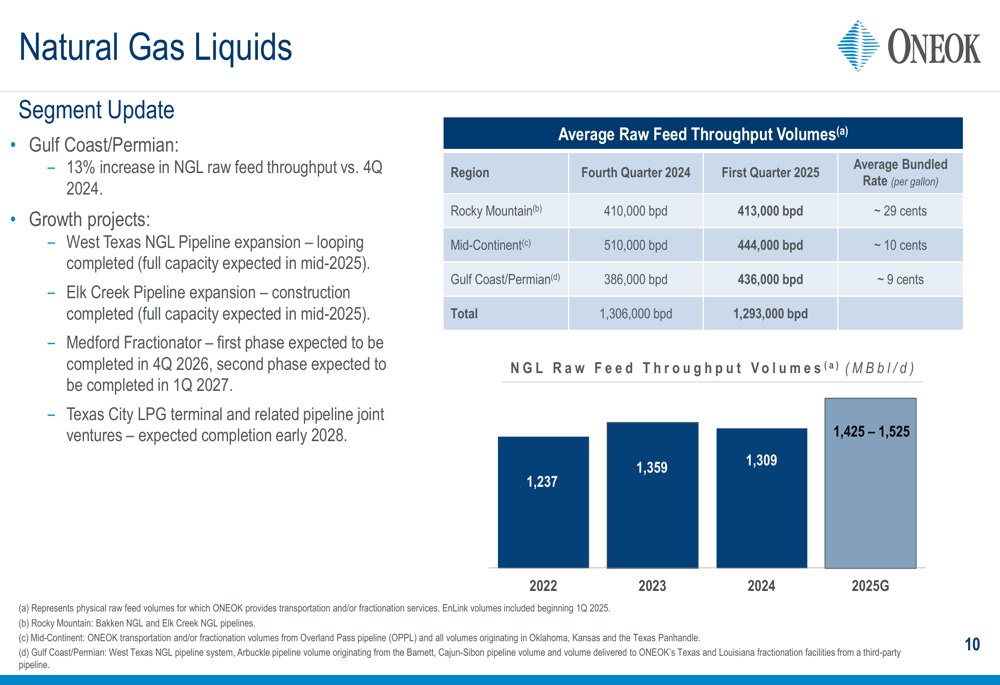

ONEOK’s Natural Gas Liquids segment generated $635 million in adjusted EBITDA during Q1 2025, though this represented a decrease from Q4 2024 primarily due to lower optimization and marketing earnings from purity NGLs held in inventory and lower volumes on the legacy ONEOK system. However, the Gulf Coast/Permian region showed strength with a 13% increase in NGL raw feed throughput compared to the previous quarter.

The Natural Gas Gathering and Processing segment contributed $491 million to Q1 adjusted EBITDA, benefiting from the EnLink acquisition and lower operating costs, though partially offset by lower volumes on the legacy ONEOK system due to winter weather. The segment’s processed volumes reached 5,250 MMcf/d in Q1 2025, significantly higher than the 2,342 MMcf/d in Q4 2024, largely due to the addition of EnLink and Permian Basin assets.

The following image illustrates ONEOK’s NGL raw feed throughput volumes and growth trajectory:

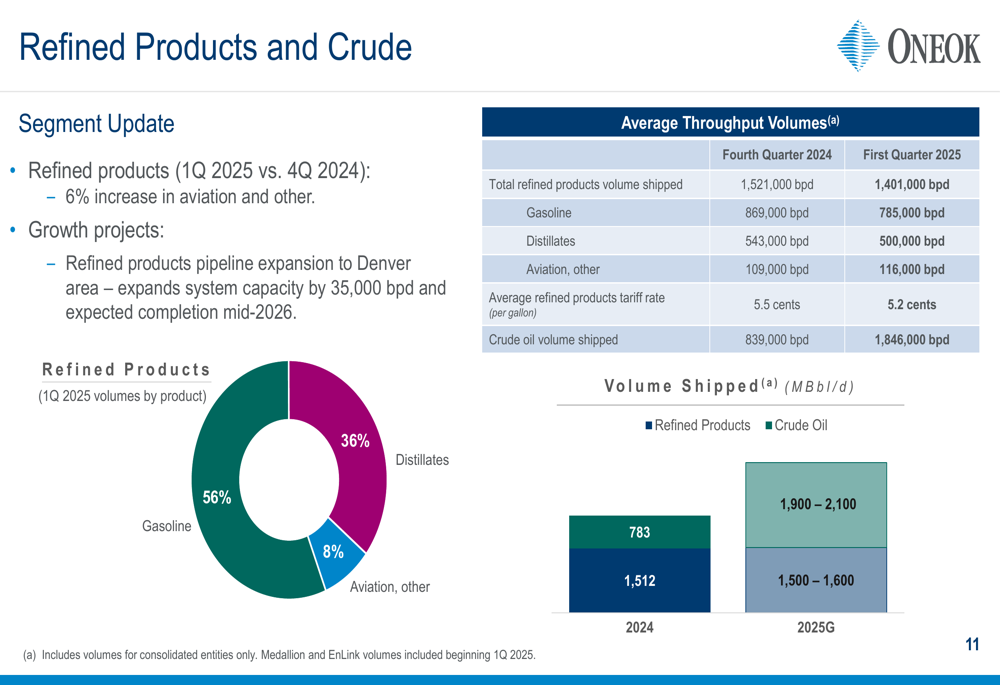

The Refined Products and Crude segment generated $471 million in adjusted EBITDA, experiencing a decrease from Q4 2024 primarily due to lower earnings from BridgeTex associated with non-recurring deferred revenue recognition in the fourth quarter, as well as lower seasonal volumes and rates on the refined products system. Crude oil volumes shipped increased dramatically to 1,846,000 bpd in Q1 2025 from 839,000 bpd in Q4 2024.

The segment’s product mix and volume trends are illustrated in the following chart:

Strategic Initiatives & Growth Projects

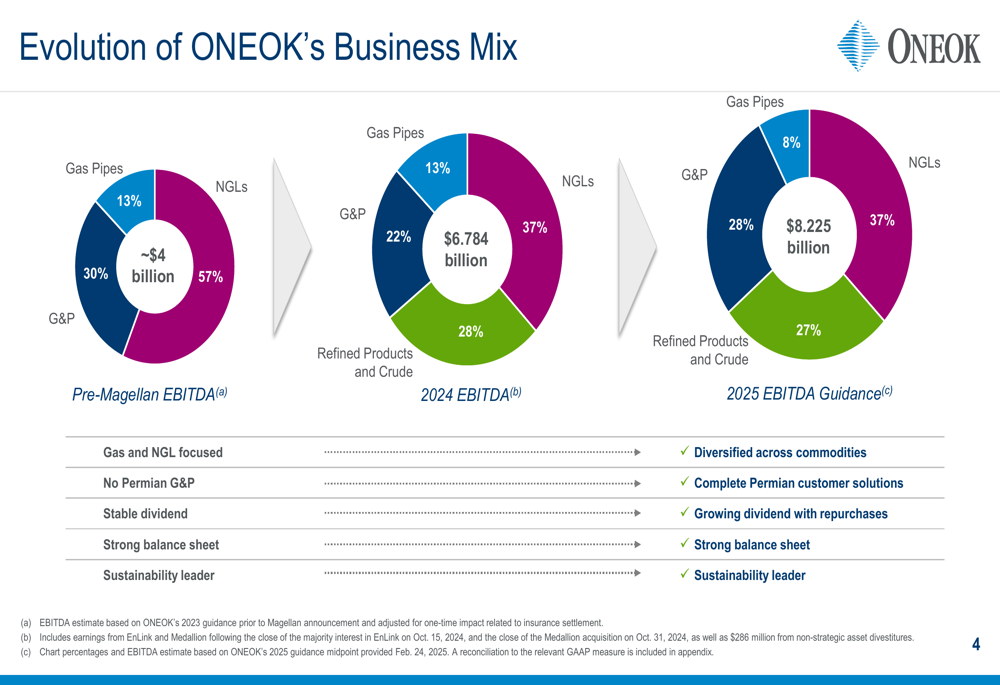

ONEOK’s business mix has evolved significantly, creating a more balanced and resilient portfolio. The company’s adjusted EBITDA is now distributed across four major segments: Natural Gas Liquids (37%), Natural Gas Gathering and Processing (28%), Refined Products and Crude (27%), and Natural Gas Pipelines (8%).

This strategic diversification is illustrated in the following chart:

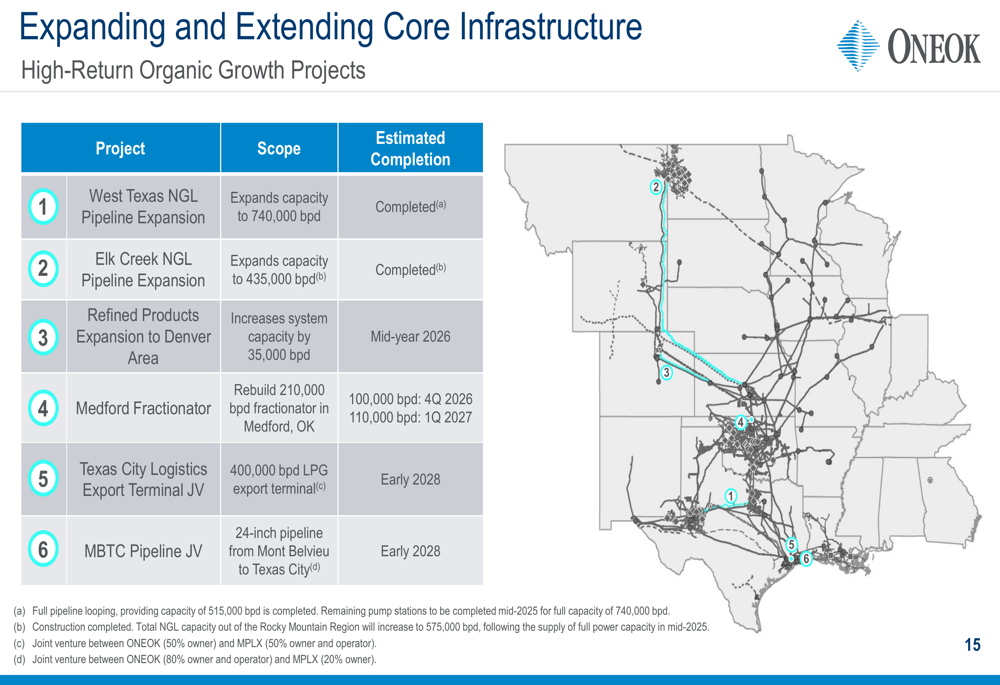

The company is executing several major infrastructure expansion projects to support continued growth:

1. West Texas NGL Pipeline expansion (completed) - Expands capacity to 740,000 bpd

2. Elk Creek NGL Pipeline expansion (completed) - Expands capacity to 435,000 bpd

3. Refined Products Expansion to Denver Area (expected mid-2026) - Increases system capacity by 35,000 bpd

4. Medford Fractionator (expected Q4 2026/Q1 2027) - 210,000 bpd fractionator in Medford, OK

5. Texas City Logistics Export Terminal JV (expected early 2028) - 400,000 bpd LPG export terminal

These strategic expansions are visualized in the following infrastructure map:

ONEOK is also strategically positioning itself to capitalize on growing industrial demand for natural gas, particularly from data centers, LNG export facilities, and ammonia plants. The company’s natural gas pipeline assets are directly connected to major LNG and industrial customers, with approximately 30 potential power plant expansion projects across its footprint representing over 4 Bcf/d of potential demand.

Financial Outlook

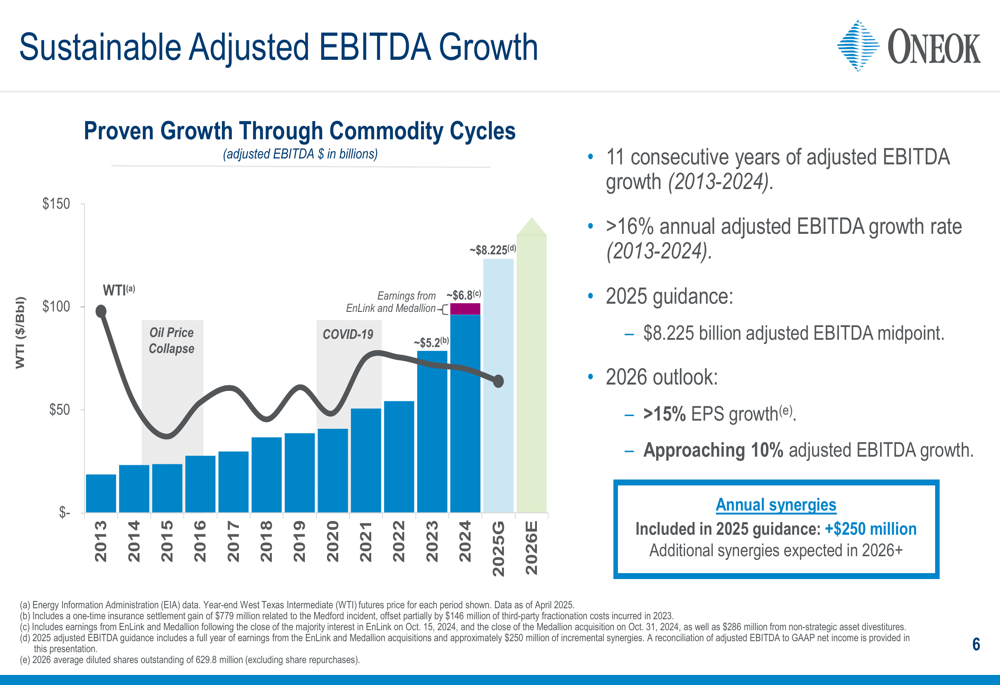

ONEOK has demonstrated consistent adjusted EBITDA growth for 11 consecutive years (2013-2024), with a compound annual growth rate exceeding 16%. The company’s 2025 guidance projects adjusted EBITDA of $8.225 billion (midpoint), with 2026 expectations of more than 15% EPS growth and approaching 10% adjusted EBITDA growth.

The following chart illustrates ONEOK’s impressive track record of adjusted EBITDA growth through various market cycles:

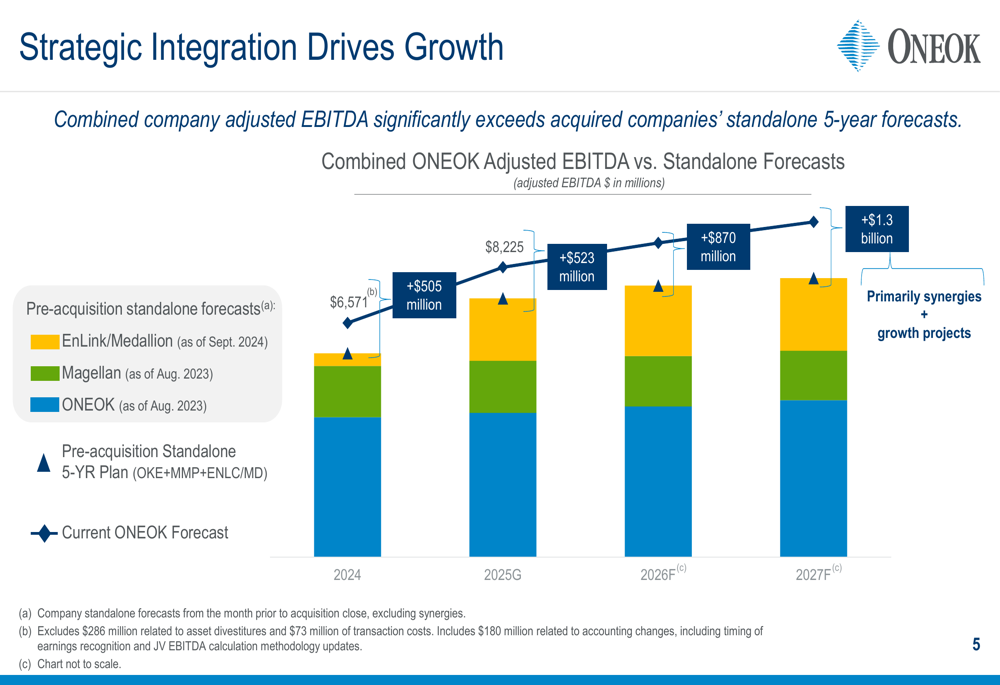

The company’s strategic integrations are driving significant growth beyond what the individual companies could have achieved independently. The combined adjusted EBITDA forecast substantially exceeds the standalone forecasts of the acquired companies, with synergies of approximately $250 million included in 2025 guidance and additional synergies expected in 2026 and beyond.

This synergy-driven growth is visualized in the following chart:

ONEOK’s continued focus on strategic integration, infrastructure expansion, and diversification across multiple energy sectors positions the company for sustainable growth while maintaining the financial strength to return capital to shareholders through dividends and share repurchases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.