Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

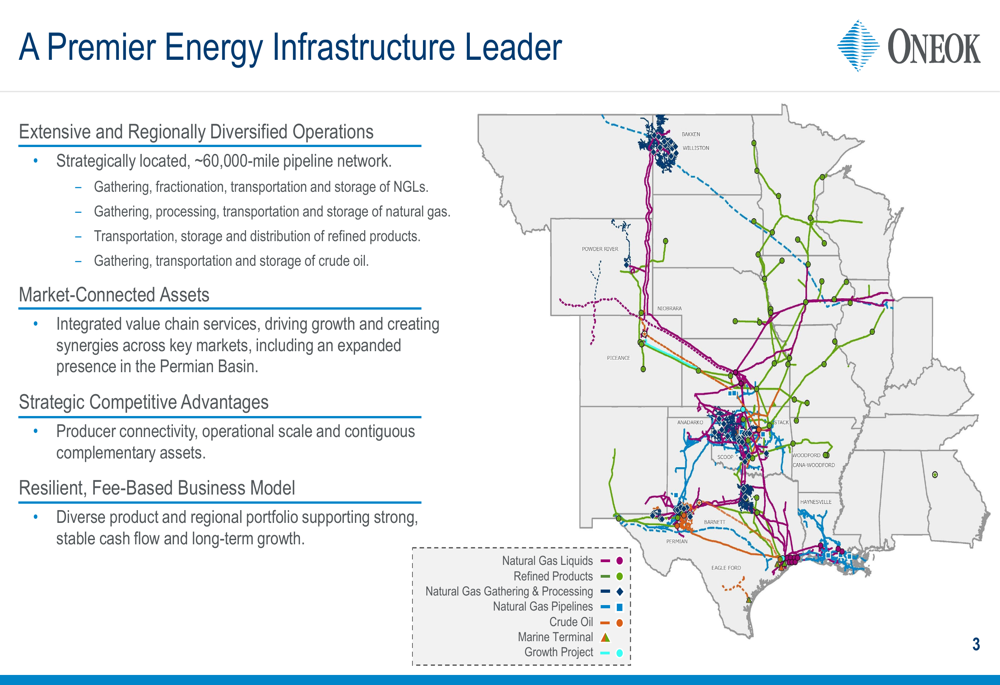

ONEOK Inc. (NYSE:OKE), a premier energy infrastructure leader with approximately 60,000 miles of pipeline network, presented its second quarter 2025 results on August 5, 2025, showcasing robust sequential growth across all business segments. The company’s integrated and diversified operations span multiple products and geographies, including the Permian, Anadarko, and Rocky Mountain regions, positioning it well to capitalize on growing industrial demand from data centers, LNG facilities, and ammonia plants.

As shown in the following infrastructure map, ONEOK’s extensive network provides strategic competitive advantages through producer connectivity and operational scale:

Quarterly Performance Highlights

ONEOK reported a net income of $853 million for Q2 2025, representing a substantial 23% increase from the $691 million reported in Q1 2025. Adjusted EBITDA reached $1.981 billion, up 12% from $1.775 billion in the previous quarter. The company also declared a quarterly dividend of $1.03 per share ($4.12 annualized) while strengthening its balance sheet by repaying nearly $600 million in senior notes.

The following chart breaks down Q2 2025 adjusted EBITDA by segment, illustrating the company’s diversified revenue streams:

This strong quarterly performance was driven by significant volume increases across all segments: NGL volumes increased by 18%, refined products volumes grew by 7%, and natural gas processed volumes rose by 6% compared to the first quarter.

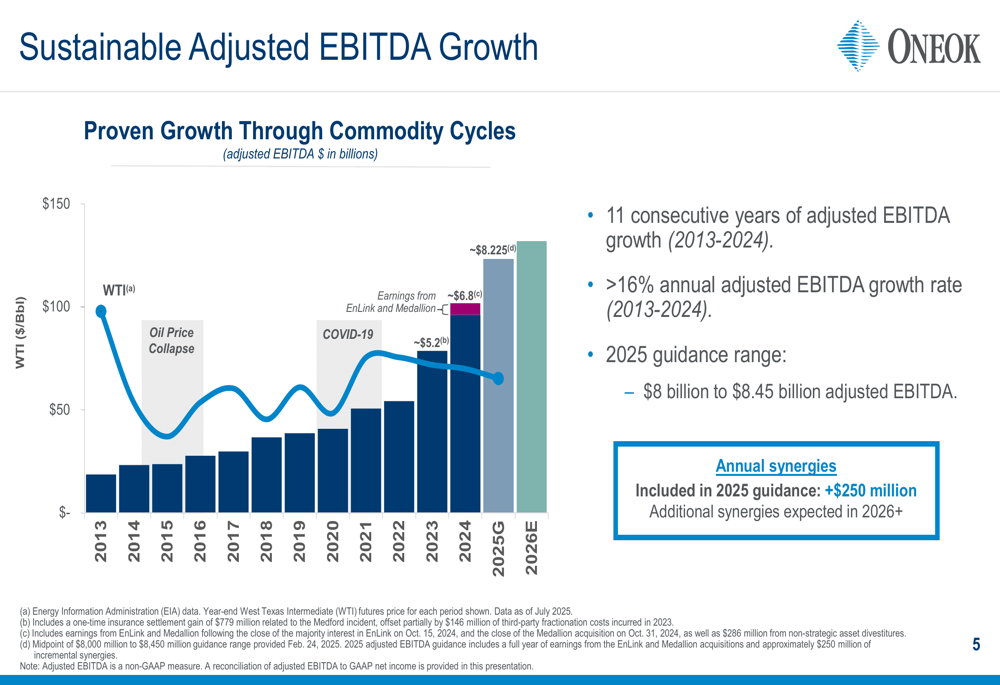

ONEOK’s financial results demonstrate its continued trajectory of sustainable growth, having achieved 11 consecutive years of adjusted EBITDA growth from 2013 to 2024, with an annual growth rate exceeding 16% during this period. The company’s 2025 guidance range for adjusted EBITDA is $8 billion to $8.45 billion, which includes annual synergies of $250 million, with additional synergies expected in 2026 and beyond.

The following chart illustrates ONEOK’s impressive adjusted EBITDA growth through various commodity cycles:

Segment Performance Analysis

Natural Gas Liquids

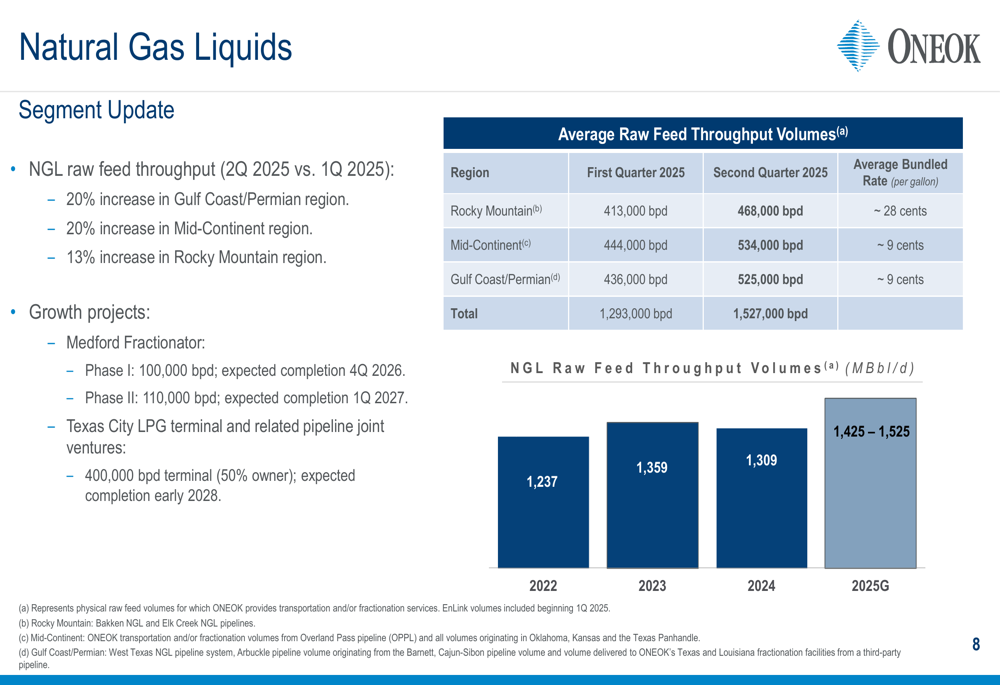

The Natural Gas Liquids segment saw significant volume increases in Q2 2025 compared to Q1 2025, with raw feed throughput rising 20% in both the Gulf Coast/Permian and Mid-Continent regions, and 13% in the Rocky Mountain region. Total (EPA:TTEF) NGL raw feed throughput reached 1,527,000 barrels per day in Q2, up from 1,293,000 barrels per day in Q1.

The segment’s adjusted EBITDA variances between Q1 and Q2 2025 included a $43 million increase in exchange services and an $8 million benefit from lower operating costs, partially offset by a $12 million decrease in transportation and storage.

The following chart details NGL throughput volumes by region and shows the company’s growth trajectory:

Refined Products and Crude

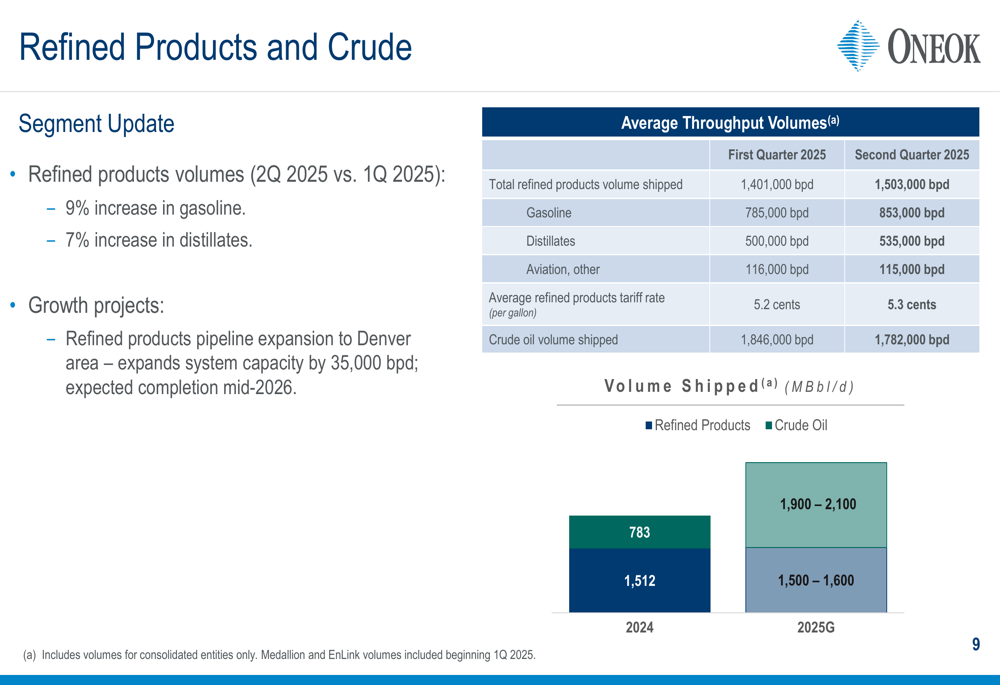

The Refined Products and Crude segment reported a 7% overall increase in refined products volumes in Q2 2025 compared to Q1, with gasoline volumes up 9% and distillates up 7%. Total refined products volume shipped reached 1,503,000 barrels per day in Q2, compared to 1,401,000 barrels per day in Q1.

This segment saw substantial adjusted EBITDA improvements, including a $64 million increase in optimization and marketing, a $34 million increase in transportation and storage, and a $7 million benefit from lower operating costs. These gains were partially offset by a $14 million decrease in adjusted EBITDA from unconsolidated affiliates.

The following chart shows the breakdown of throughput volumes by product type:

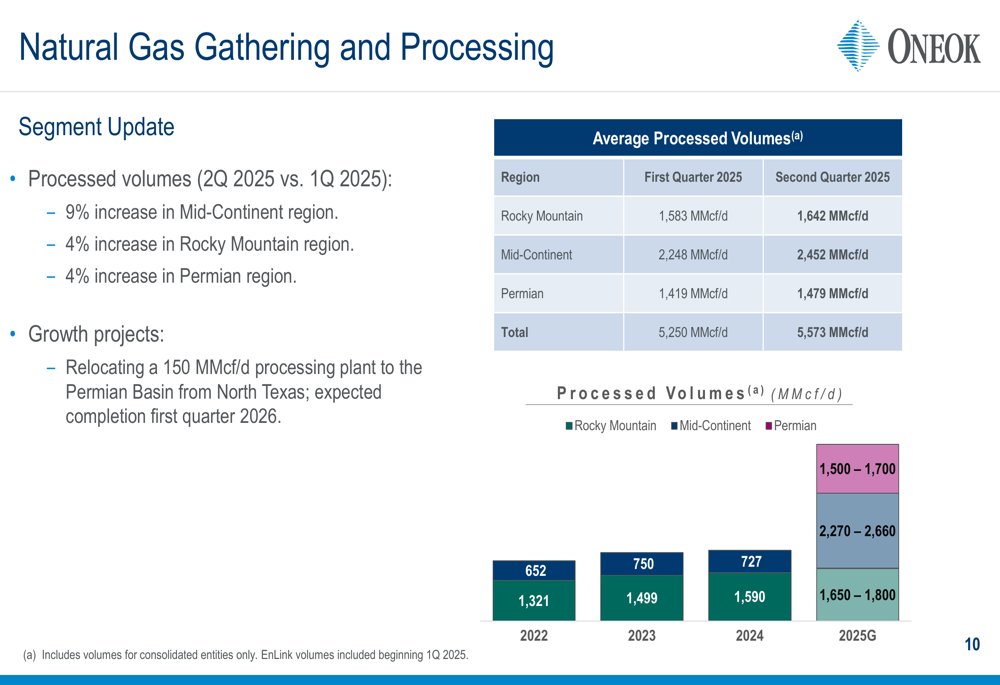

Natural Gas Gathering and Processing

The Natural Gas Gathering and Processing segment reported processed volumes of 5,573 MMcf/d in Q2 2025, a 6% increase from 5,250 MMcf/d in Q1. By region, processed volumes increased 9% in the Mid-Continent, 4% in the Rocky Mountain, and 4% in the Permian.

Adjusted EBITDA variances for this segment included a $51 million increase from higher volumes and a $21 million benefit from lower operating costs, partially offset by a $23 million decrease due to lower realized natural gas prices.

The following chart illustrates processed volumes by region:

Strategic Growth Initiatives

ONEOK is advancing several strategic growth projects to expand its capacity and enhance its market position:

1. Medford Fractionator: A two-phase expansion with Phase I (100,000 bpd) expected in Q4 2026 and Phase II (110,000 bpd) in Q1 2027

2. Texas City LPG terminal: A 400,000 bpd facility scheduled for completion in early 2028

3. Refined products pipeline expansion to the Denver area: Adding 35,000 bpd of capacity with expected completion by mid-2026

4. Relocation of a 150 MMcf/d processing plant from North Texas to the Permian Basin, expected to be completed in Q1 2026

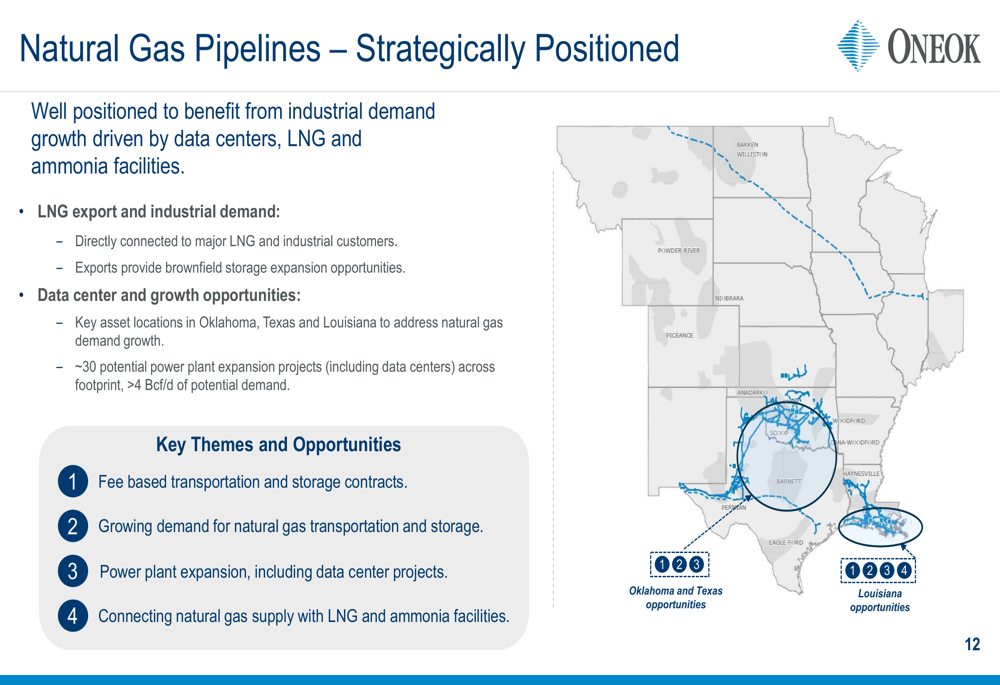

The company is also strategically positioned to benefit from industrial demand growth, particularly from data centers, LNG facilities, and ammonia plants. Its natural gas pipeline network offers opportunities for brownfield storage expansion and connections to major customers.

As shown in the following map, ONEOK’s natural gas pipeline infrastructure is well-positioned to capitalize on growing demand in key regions:

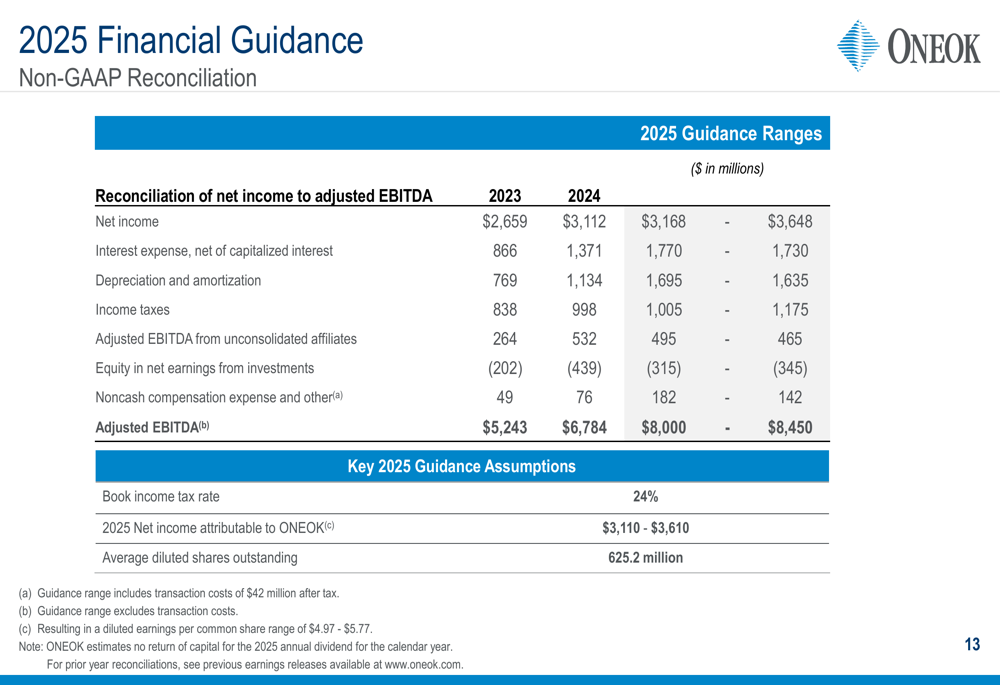

Financial Outlook and Guidance

ONEOK provided a detailed reconciliation of its 2025 financial guidance, projecting net income between $3,168 million and $3,648 million and adjusted EBITDA between $8,000 million and $8,450 million. This represents significant growth compared to 2024’s net income of $3,112 million and adjusted EBITDA of $6,784 million.

The following table provides a comprehensive breakdown of ONEOK’s financial guidance and reconciliation:

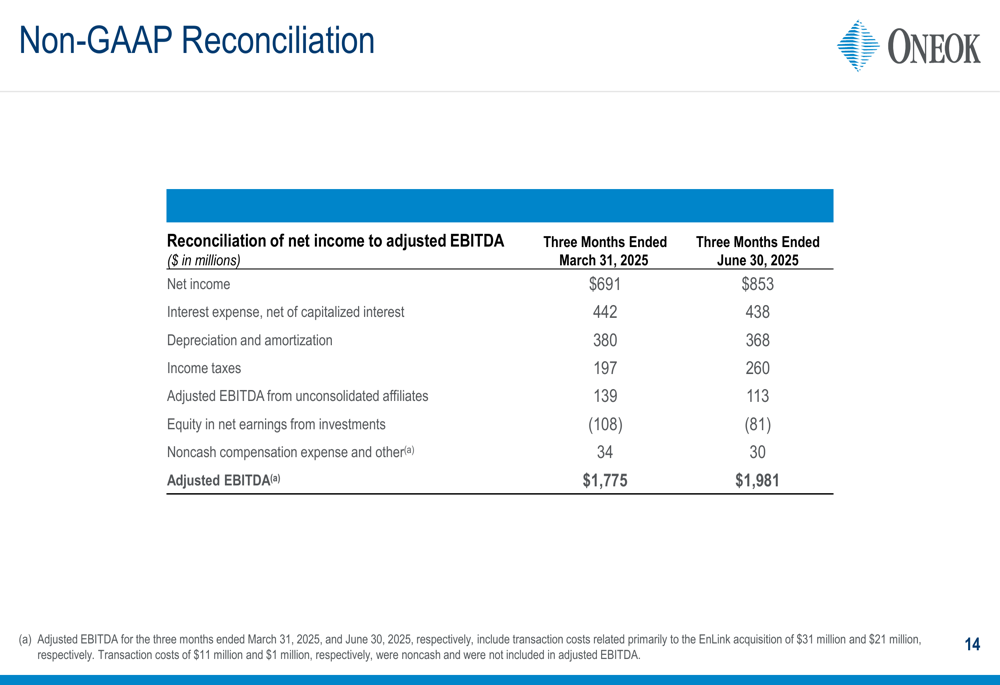

For Q2 2025, the company reported net income of $853 million, interest expense of $438 million, depreciation and amortization of $368 million, and income taxes of $260 million, resulting in adjusted EBITDA of $1,981 million. This represents substantial improvement over Q1 2025’s adjusted EBITDA of $1,775 million.

The detailed quarterly reconciliation is presented in the following table:

ONEOK’s strong financial performance, coupled with its strategic growth initiatives and market-connected assets, positions the company well for continued success in the evolving energy landscape. The company’s fee-based business model provides resilience through commodity cycles, while its diversified operations across multiple products and geographies offer both stability and growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.