Crispr Therapeutics shares tumble after significant earnings miss

Introduction & Market Context

onsemi (NASDAQ:ON) shares fell over 5.6% in premarket trading Monday after the company released its Q2 2025 earnings presentation, despite reporting modest sequential revenue growth and meeting guidance targets. The semiconductor manufacturer posted revenue of $1.47 billion, up 2% quarter-over-quarter, as the company cited "signs of stabilization across end-markets" after a challenging period for the industry.

The presentation comes after onsemi’s stock has already declined significantly over the past six months, with shares down approximately 40% according to previous earnings reports. Despite the stock pressure, the company highlighted several positive developments, including doubled Silicon Carbide (SiC) revenue in China and expanded adoption of its Treo manufacturing platform.

Quarterly Performance Highlights

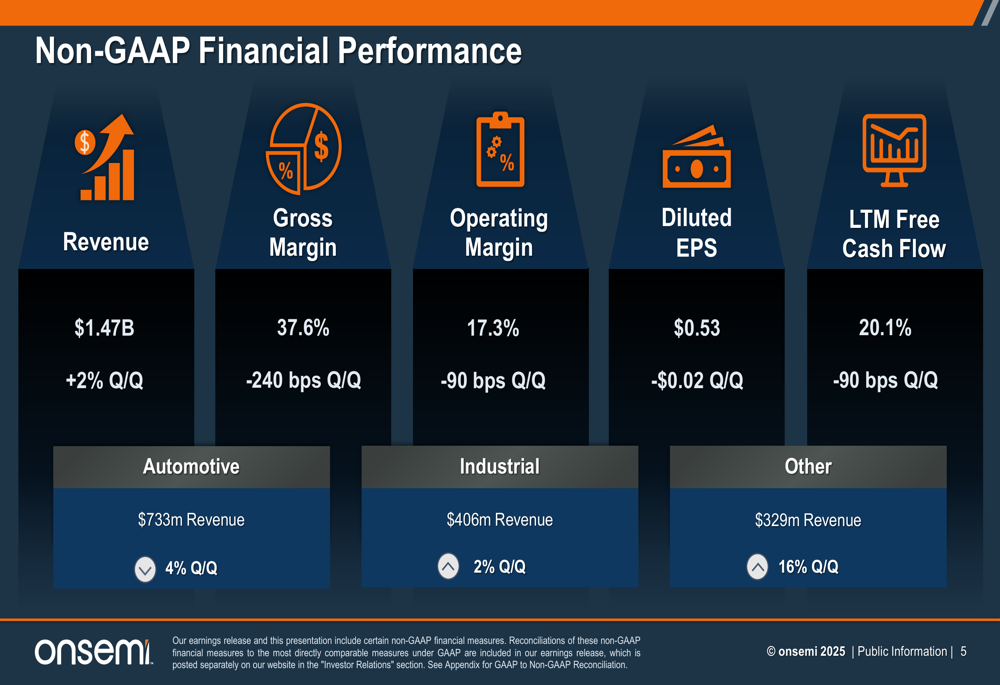

onsemi reported Q2 2025 revenue of $1.47 billion, representing a 2% sequential increase from Q1. However, gross margin declined 240 basis points quarter-over-quarter to 37.6%, while operating margin fell 90 basis points to 17.3%. Diluted earnings per share came in at $0.53, down $0.02 from the previous quarter.

As shown in the following financial performance overview:

The company’s automotive segment led revenue at $733 million (+4% Q/Q), followed by industrial at $406 million (+2% Q/Q), while the "Other" category showed the strongest growth at $329 million (+16% Q/Q). The long-term free cash flow margin stood at 20.1%, down 90 basis points quarter-over-quarter.

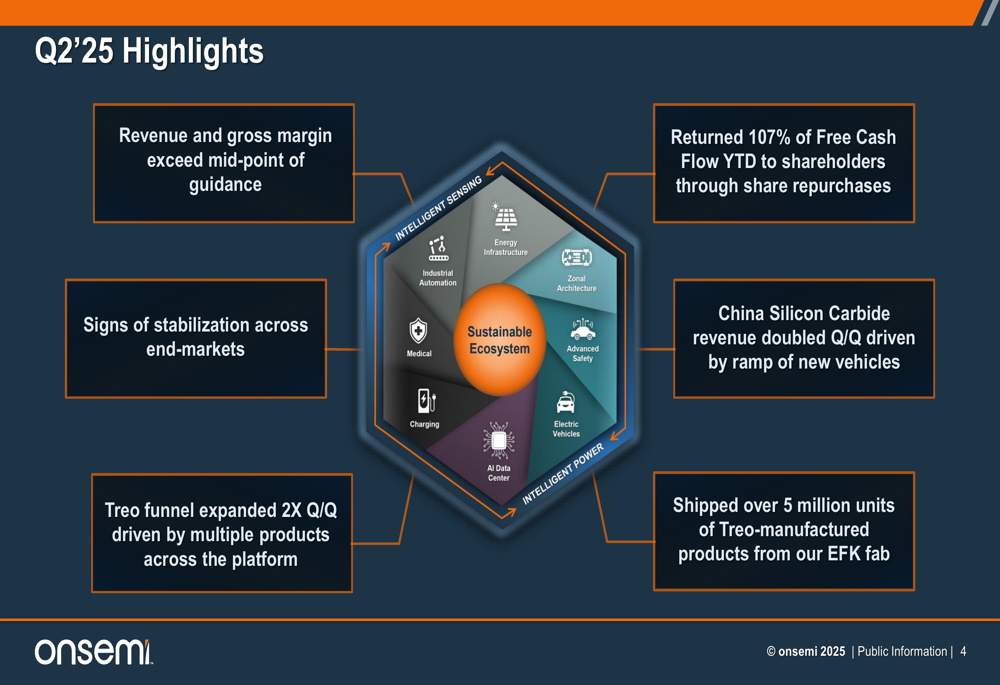

Among the quarter’s key highlights, onsemi emphasized the doubling of China Silicon Carbide revenue, driven by new vehicle production ramps, and the shipment of over 5 million Treo-manufactured units from its East Fishkill facility. The company also returned 107% of free cash flow year-to-date to shareholders through share repurchases.

The following slide illustrates these achievements alongside the company’s strategic focus areas:

Strategic Initiatives

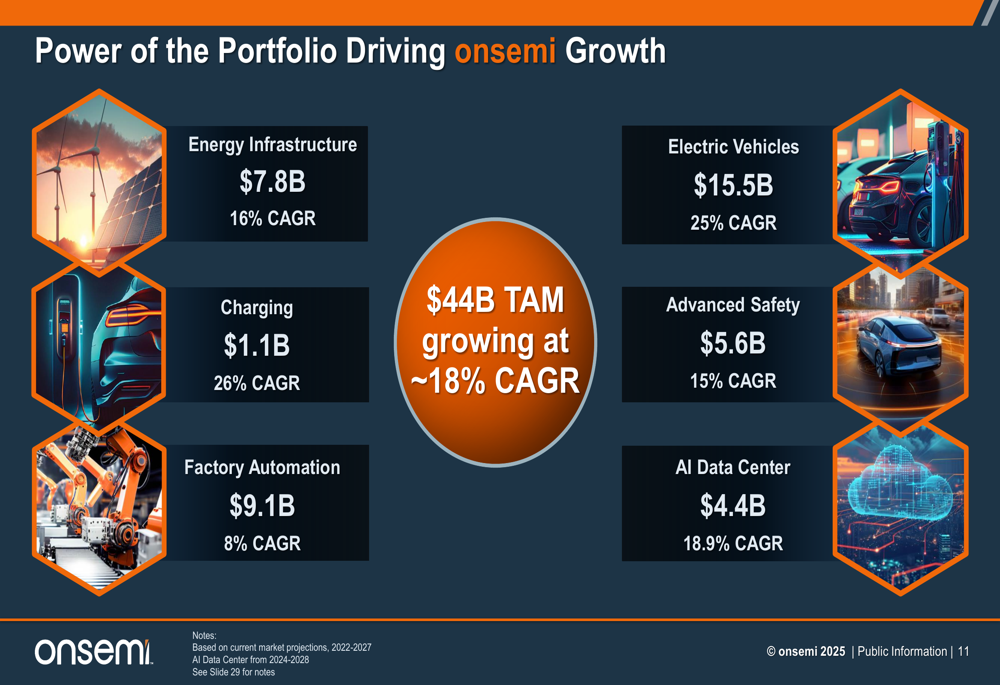

onsemi continues to position itself as a leader in high-growth semiconductor markets, targeting a total addressable market of $44 billion growing at approximately 18% CAGR. The company’s strategy centers on intelligent power and sensing technologies for automotive, industrial, and emerging applications.

The presentation highlighted onsemi’s ambition to capture 35-40% of the Silicon Carbide market, leveraging its end-to-end supply chain and comprehensive product portfolio. This focus appears to be gaining traction, particularly in China’s electric vehicle market where the company reported doubled quarterly revenue.

The following slide details the company’s targeted growth markets and their respective potential:

Another key strategic initiative is the Treo manufacturing platform, which onsemi credits with driving gross margin expansion. The platform delivers "disruptive, high value" products with up to 70% gross margins, according to the presentation. The company has shipped over 5 million Treo-manufactured units and expects the platform to replace existing products over multiple years, contributing to margin improvement.

As illustrated in this slide on the Treo platform’s benefits:

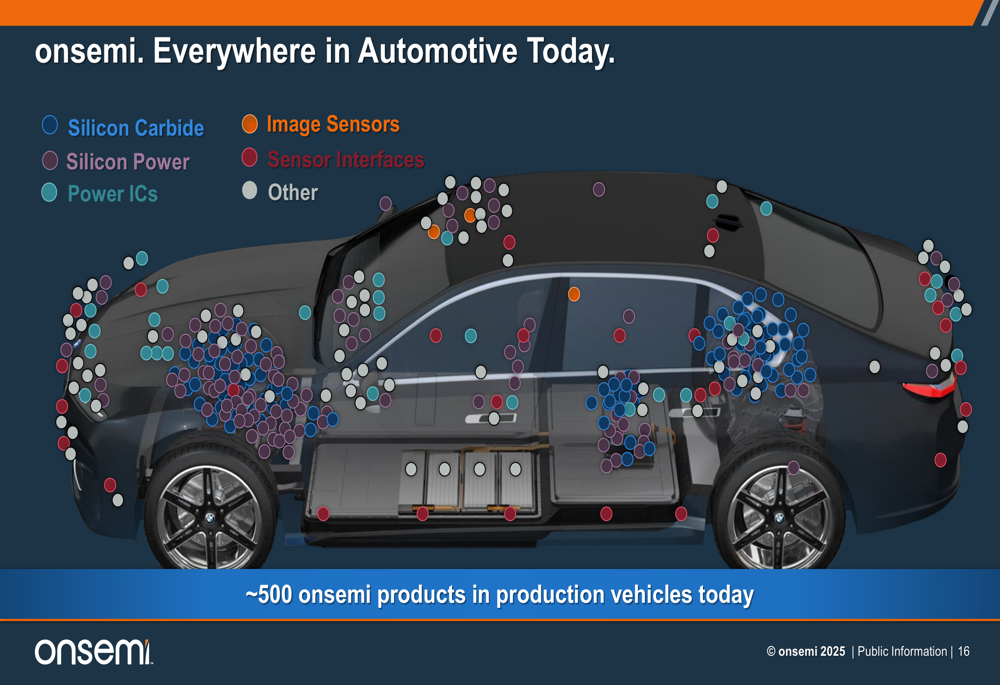

The company also emphasized its strong position in automotive applications, with approximately 500 onsemi products in production vehicles today across categories including Silicon Carbide, Silicon Power, Power ICs, Image Sensors, and Sensor Interfaces.

The following diagram shows onsemi’s extensive automotive product integration:

Forward-Looking Statements

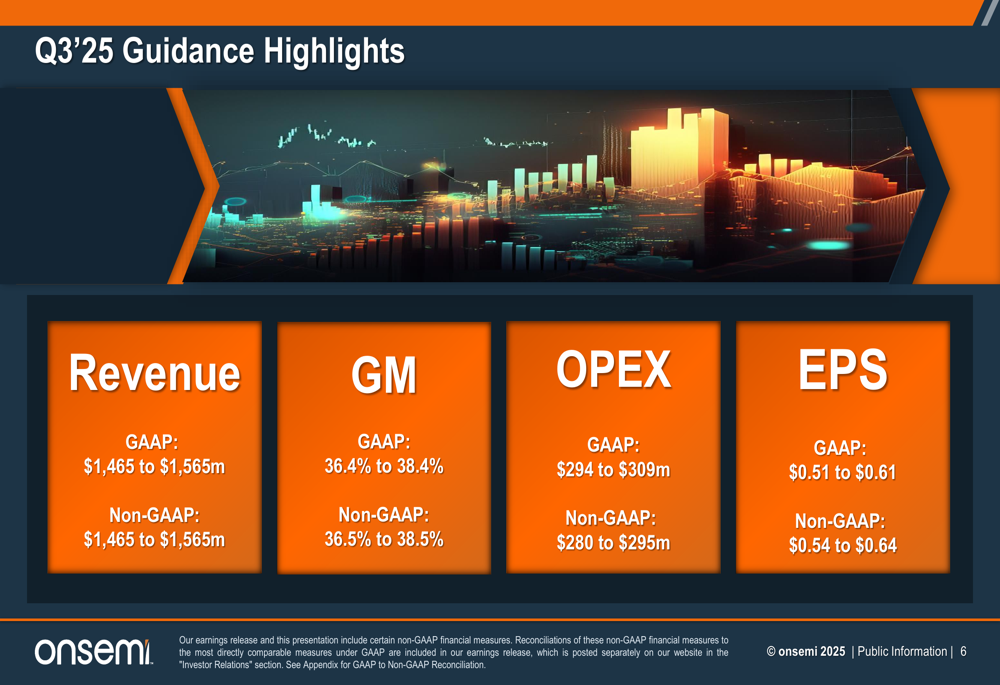

For Q3 2025, onsemi provided revenue guidance of $1,465 to $1,565 million and non-GAAP gross margin guidance of 36.5% to 38.5%. The company expects non-GAAP earnings per share between $0.54 and $0.64.

The Q3 guidance details are shown in this slide:

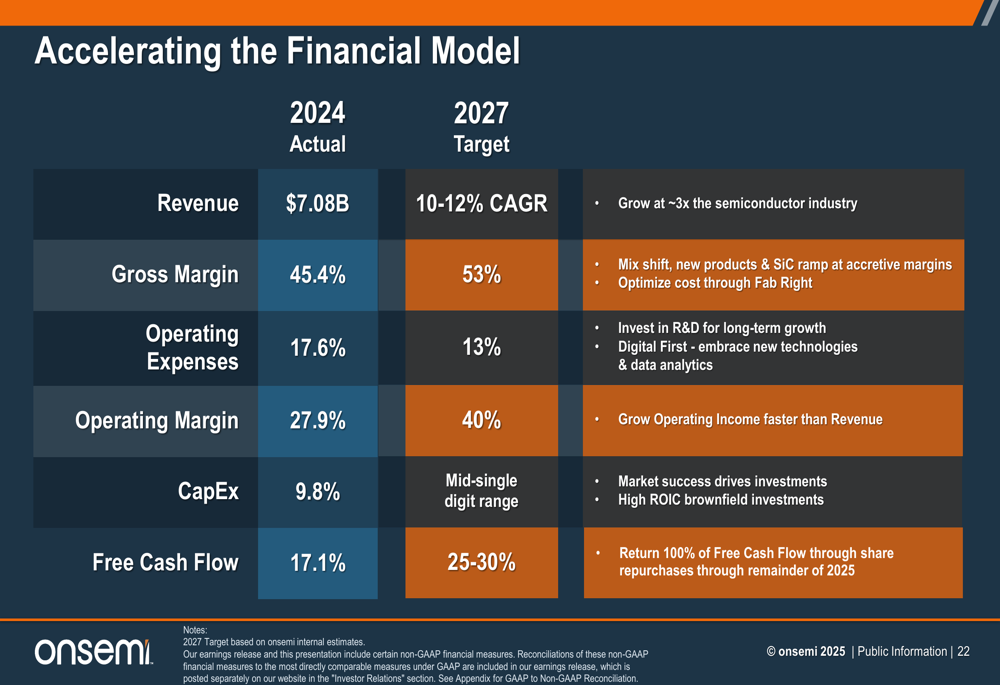

Looking further ahead, onsemi outlined ambitious targets for 2027, including revenue growth at a 10-12% CAGR (approximately three times the semiconductor industry average), gross margin expansion to 53% (from 45.4% in 2024), and operating margin improvement to 40% (from 27.9% in 2024). The company also aims to increase its free cash flow margin to 25-30% by 2027.

These long-term financial targets are detailed in the following slide:

The company reiterated its commitment to return 100% of free cash flow to shareholders through share repurchases through the remainder of 2025, continuing its focus on shareholder returns.

Conclusion

onsemi’s Q2 2025 presentation portrays a company navigating a challenging semiconductor market with modest sequential growth and signs of stabilization. While facing some margin pressure in the near term, the company remains focused on its long-term strategy centered on Silicon Carbide technology, the Treo manufacturing platform, and high-growth markets including electric vehicles, energy infrastructure, and AI data centers.

The doubling of China Silicon Carbide revenue represents a bright spot amid otherwise modest growth, suggesting the company’s strategic investments in this area are beginning to yield results. However, investors appear concerned about the pace of recovery and margin trajectory, as reflected in the premarket stock decline following the presentation.

As onsemi works toward its ambitious 2027 financial targets, the company’s ability to execute on its Silicon Carbide strategy and successfully transition to higher-margin Treo products will likely determine whether it can achieve the significant margin expansion and above-market growth it has projected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.