Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Ontex Group (BR:EBR:ONTEX) reported disappointing first-half 2025 results on July 16, revealing a 4% year-over-year decline in revenue and significant pressure on profitability. The market reacted negatively to the presentation, with shares falling 11.14% to €6.54, approaching the company’s 52-week low of €6.47.

The personal hygiene products manufacturer faced multiple headwinds during the period, including weaker demand in Europe and North America, customer inventory adjustments, and supply chain disruptions. These challenges forced the company to revise its full-year outlook downward, though management expressed confidence in a second-half recovery.

Quarterly Performance Highlights

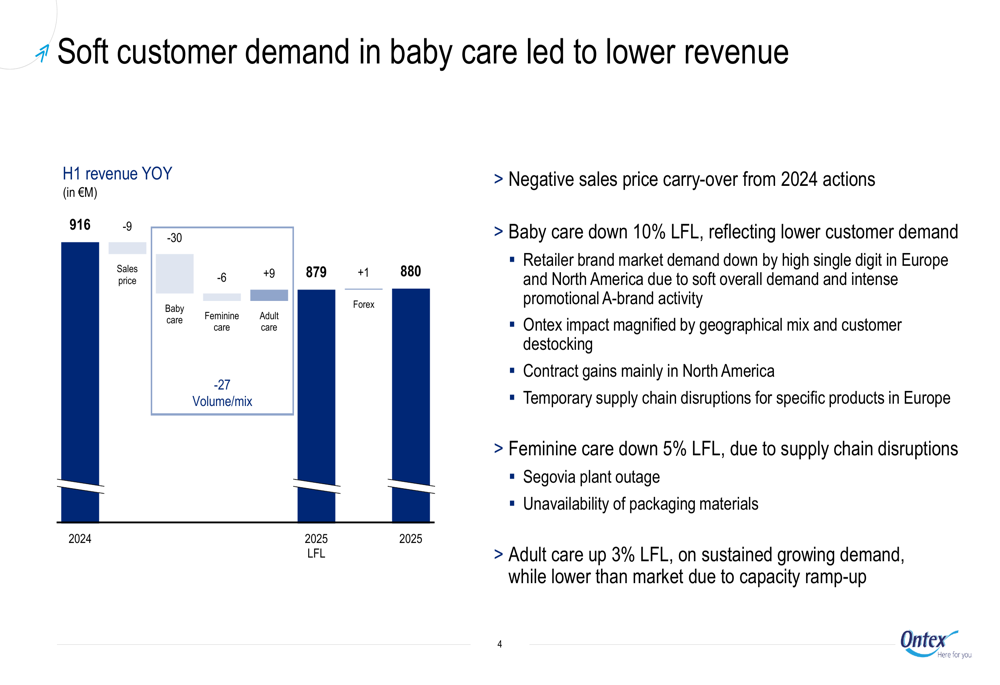

Ontex reported H1 2025 revenue of €880 million, down 4.0% like-for-like compared to the same period last year. The decline was primarily driven by negative price carry-over from 2024 actions and volume decreases in key segments.

As shown in the following revenue breakdown:

Baby care was particularly hard hit, declining 10% like-for-like due to lower customer demand. Feminine care dropped 5% like-for-like, attributed to supply chain disruptions. The adult care segment provided the only bright spot, growing 3% like-for-like on sustained demand, though growth was constrained by capacity ramp-up issues.

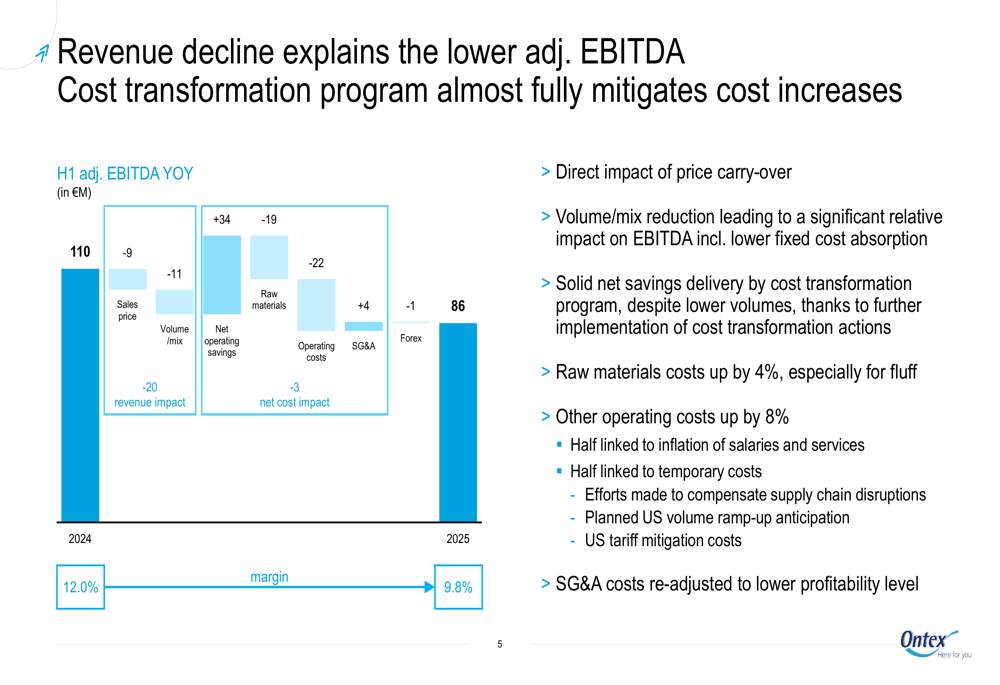

Profitability metrics showed significant deterioration, with adjusted EBITDA margin falling 2.2 percentage points year-over-year to 9.8%. This represents a continuation of the negative trend observed in Q1 2025, when the company reported an EBITDA margin above 11%.

The following chart illustrates the factors contributing to the EBITDA decline:

Raw material costs increased by 4%, particularly for fluff pulp, while other operating costs rose by 8%. These increases, combined with lower volumes and reduced fixed cost absorption, significantly impacted profitability despite ongoing cost transformation efforts.

Detailed Financial Analysis

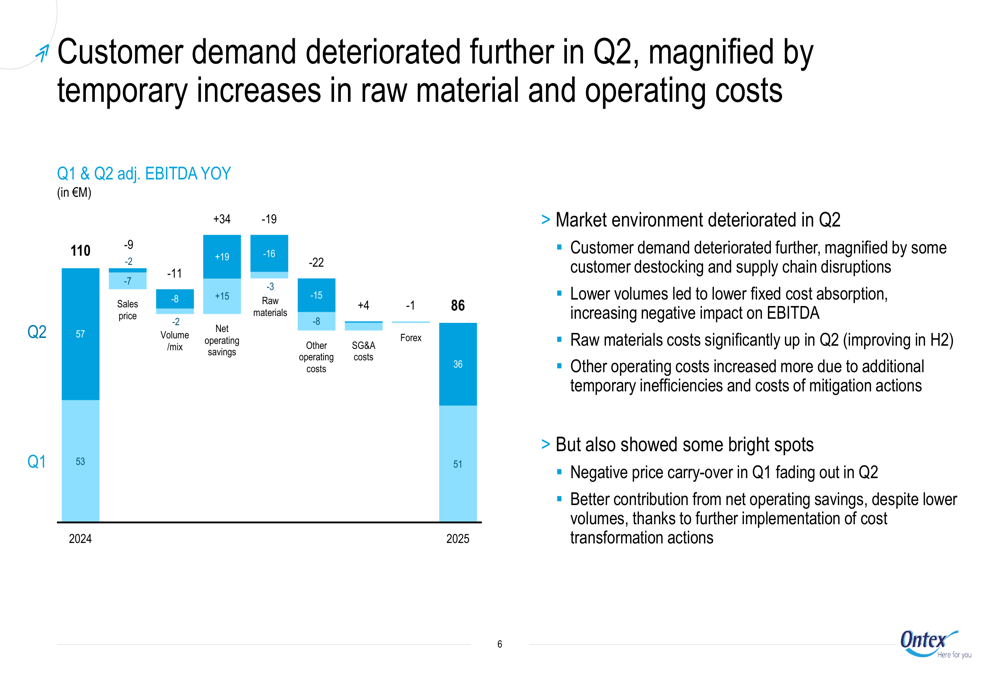

A closer examination of quarterly performance reveals that market conditions worsened as the half progressed. The company’s presentation highlighted that the negative price carry-over effect from Q1 began fading in Q2, but this positive development was offset by deteriorating market conditions.

The quarterly EBITDA comparison shows this progression:

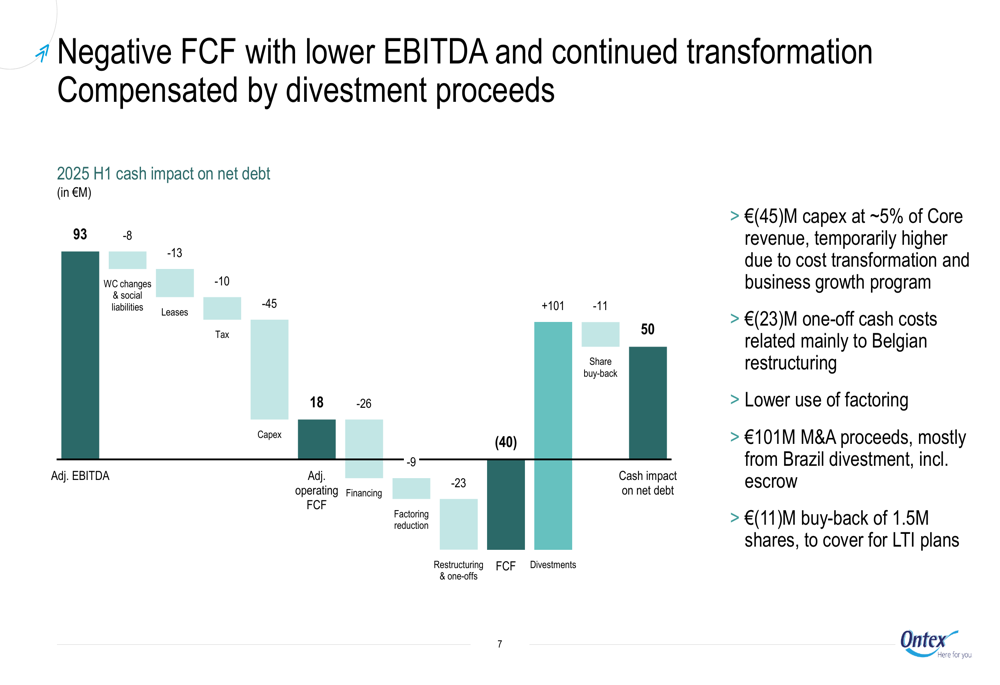

Free cash flow after interest turned negative at €(40) million, compared to a positive €43 million in H1 2024. This decline was driven by lower EBITDA, higher capital expenditures, and one-off cash costs related primarily to Belgian restructuring.

The following cash flow analysis provides more detail:

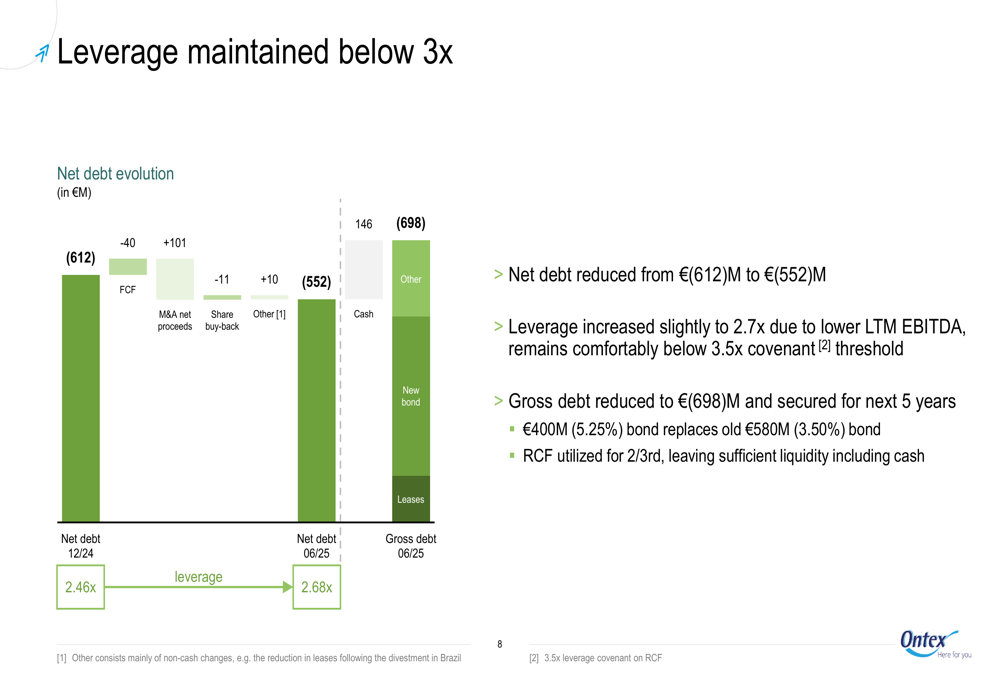

Despite cash flow challenges, Ontex made progress in reducing its net debt from €612 million to €552 million, largely due to proceeds from divestments, particularly its Brazilian operations. However, leverage increased slightly to 2.7x (from 2.5x at the end of 2024) due to lower LTM EBITDA, though it remains below the 3.5x covenant threshold.

The net debt evolution is illustrated here:

Forward-Looking Statements

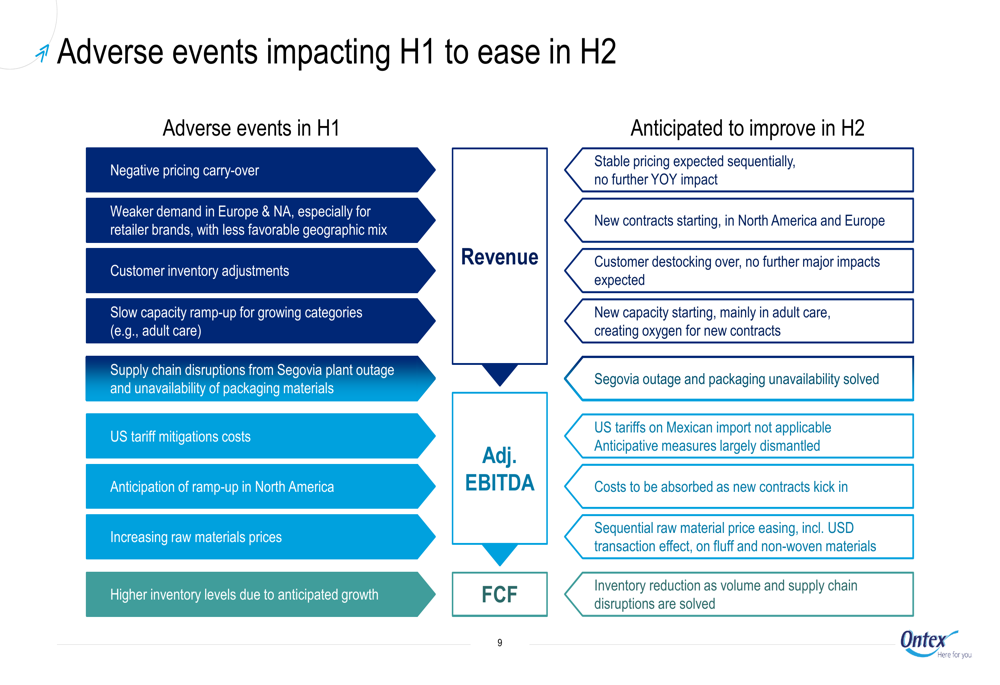

Ontex management expressed optimism for the second half of 2025, suggesting that many of the adverse events impacting H1 results would ease. The company anticipates volume-driven revenue growth of 5-9% like-for-like in H2, with sales prices expected to remain largely stable.

The following slide outlines factors expected to improve in H2:

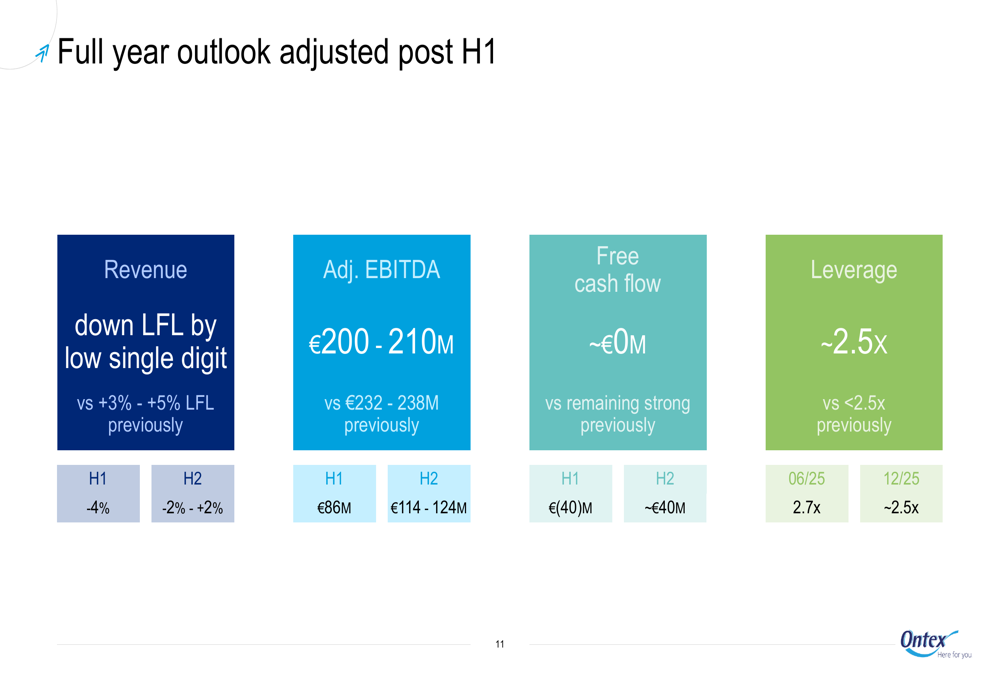

Based on first-half performance and second-half expectations, Ontex has adjusted its full-year outlook:

The revised guidance projects a low single-digit decline in like-for-like revenue for the full year, adjusted EBITDA of €200-210 million, free cash flow of approximately €0 million, and leverage of around 2.5x. This represents a significant downgrade from the guidance provided in the Q1 earnings call, which had targeted revenue growth of 3-5% and EBITDA growth of 4-7% for 2024.

Strategic Initiatives

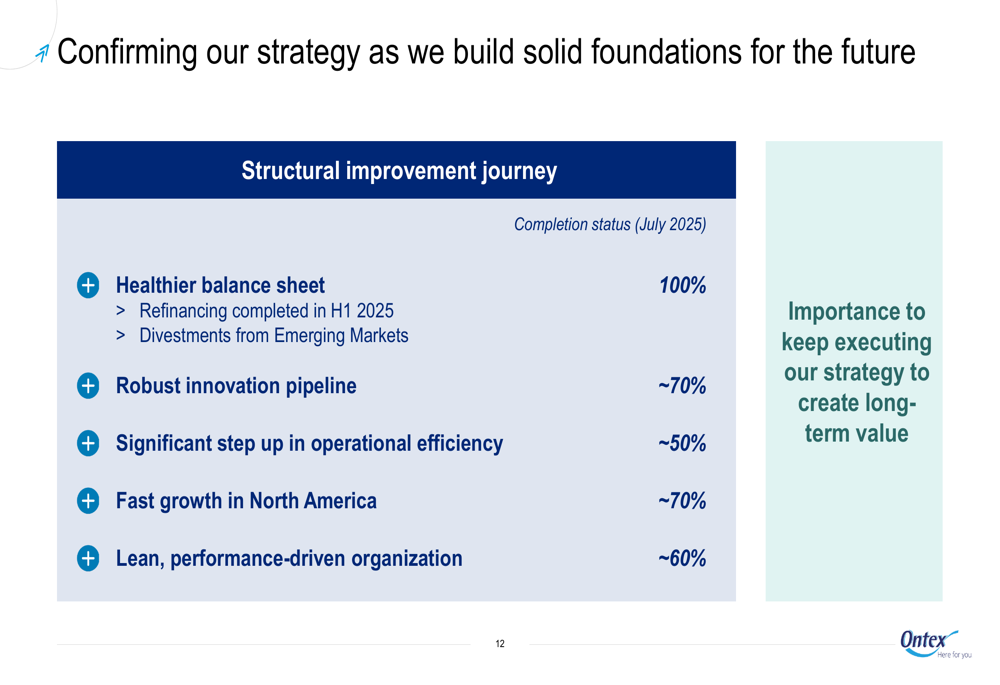

Despite current challenges, Ontex continues to make progress on its structural improvement initiatives. The company highlighted several areas of advancement, including a healthier balance sheet (100% complete), a robust innovation pipeline (70% complete), and significant steps in operational efficiency (50% complete).

The progress on strategic initiatives is summarized here:

The company’s growth strategy in North America is approximately 70% complete, while efforts to create a lean, performance-driven organization are about 60% complete. These initiatives are expected to support the anticipated second-half recovery and position the company for improved performance in 2026.

Ontex has also made strategic divestments, including its Brazilian operations, which contributed €101 million in M&A proceeds. These moves align with the company’s strategy to streamline operations and focus on core markets, similar to the divestment of its Turkish business mentioned in previous earnings reports.

As Ontex navigates through a challenging 2025, investors will be closely watching whether the anticipated second-half recovery materializes and whether the company can deliver on its revised guidance while continuing to advance its strategic transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.