Investor caution ahead of Nvidia earnings "understandable," Barclays says

Introduction & Market Context

Ontex Group (EURONEXT:EBR:ONTEX) shares plunged nearly 12% on April 30, 2025, after the personal hygiene products manufacturer reported a 2.8% like-for-like revenue decline in its first quarter results presentation. Despite the quarterly setback, the company maintained its full-year outlook, citing expected improvements in the coming quarters amid a challenging market environment characterized by geopolitical tensions and inflation fears.

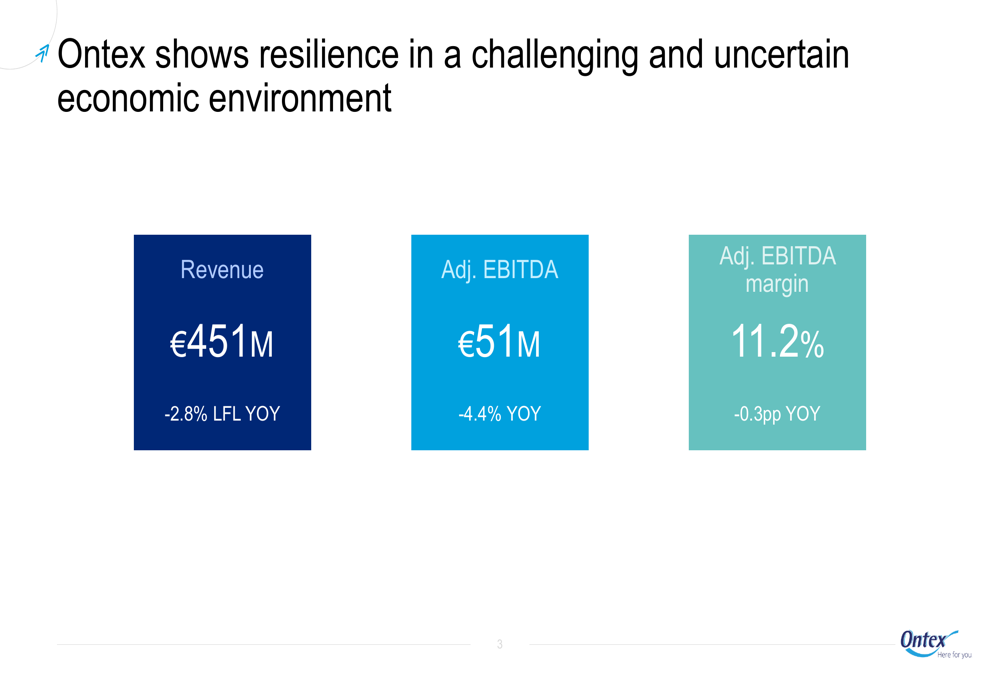

The Belgium-based manufacturer reported Q1 2025 revenue of €451 million and adjusted EBITDA of €51 million, representing year-over-year declines of 2.8% and 4.4% respectively. These results mark a reversal from the company’s stronger performance in Q4 2024, when it achieved 3.5% like-for-like revenue growth and a 28% increase in adjusted EBITDA.

Quarterly Performance Highlights

Ontex’s Q1 2025 performance reflects ongoing market challenges, with the company’s adjusted EBITDA margin slightly contracting to 11.2%, down 0.3 percentage points year-over-year. The company attributed this performance to a combination of lower volumes in Europe, price decreases, and increased operating costs.

As shown in the following financial highlights chart, the company’s key metrics all showed year-over-year declines:

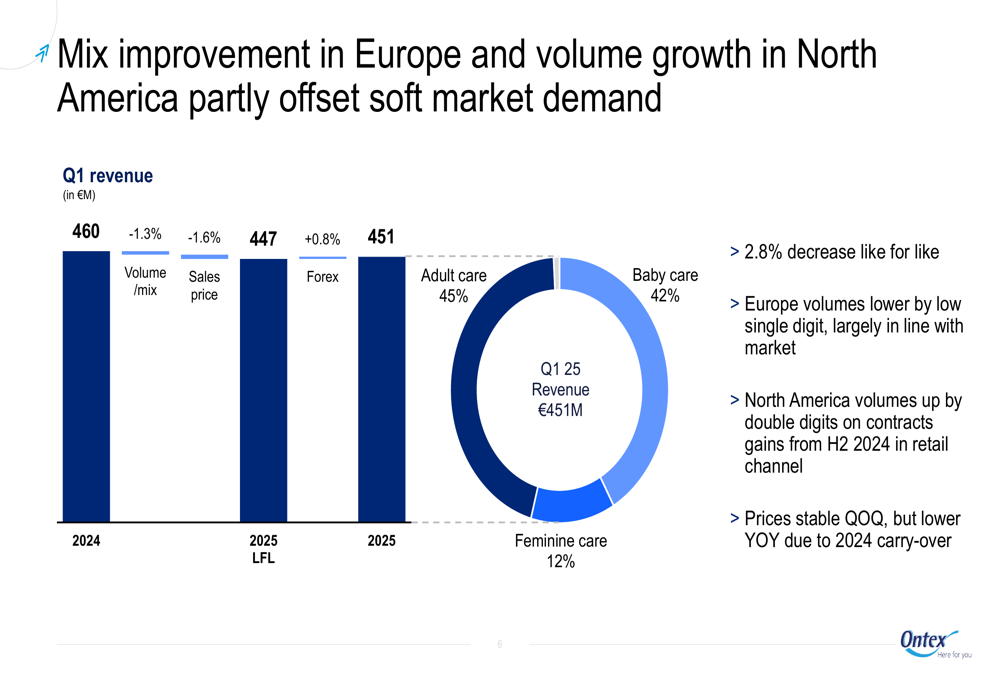

The revenue analysis reveals that adult care continues to be Ontex’s largest segment, representing 45% of total revenue, followed by baby care at 42% and feminine care at 12%. Volume mix decreased by 1.3%, while sales prices fell by 1.6%, partially offset by a 0.8% positive impact from foreign exchange.

The company’s performance varied significantly by region, with North American volumes growing by double digits due to new retail contracts gained in the second half of 2024, while European volumes declined by a low single digit, which management described as largely in line with the overall market.

The following revenue breakdown illustrates these dynamics:

Detailed Financial Analysis

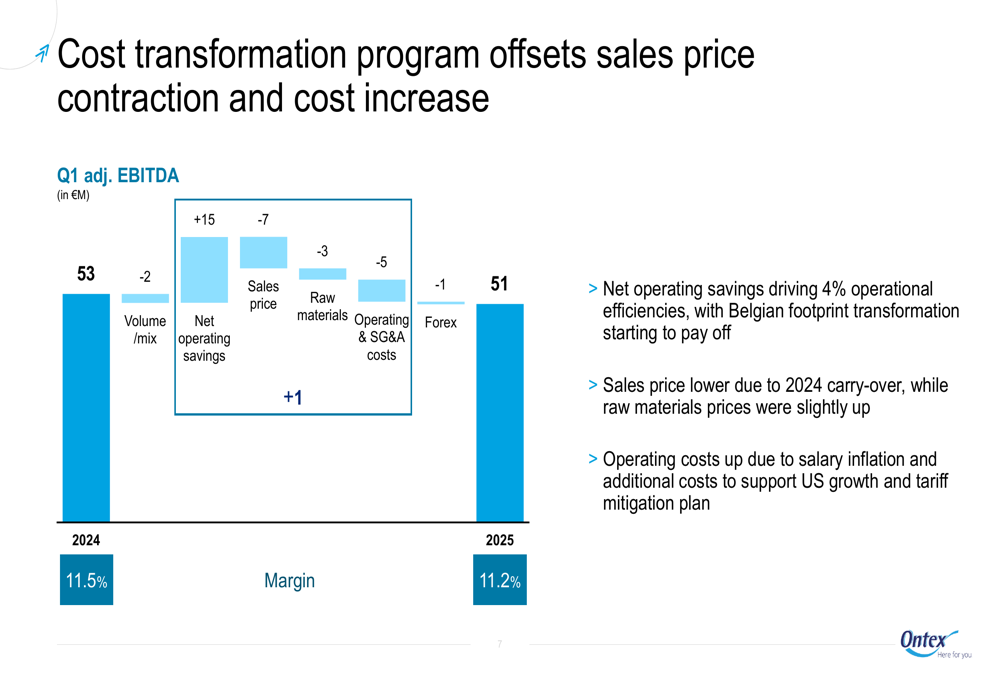

Ontex’s adjusted EBITDA bridge analysis provides insight into the factors affecting profitability. Despite achieving €15 million in net operating savings, these gains were more than offset by negative impacts from volume/mix (-€2M), sales price (-€7M), raw materials (-€3M), operating and SG&A costs (-€5M), and forex (-€1M).

The following EBITDA bridge visualization shows how these factors contributed to the overall decline:

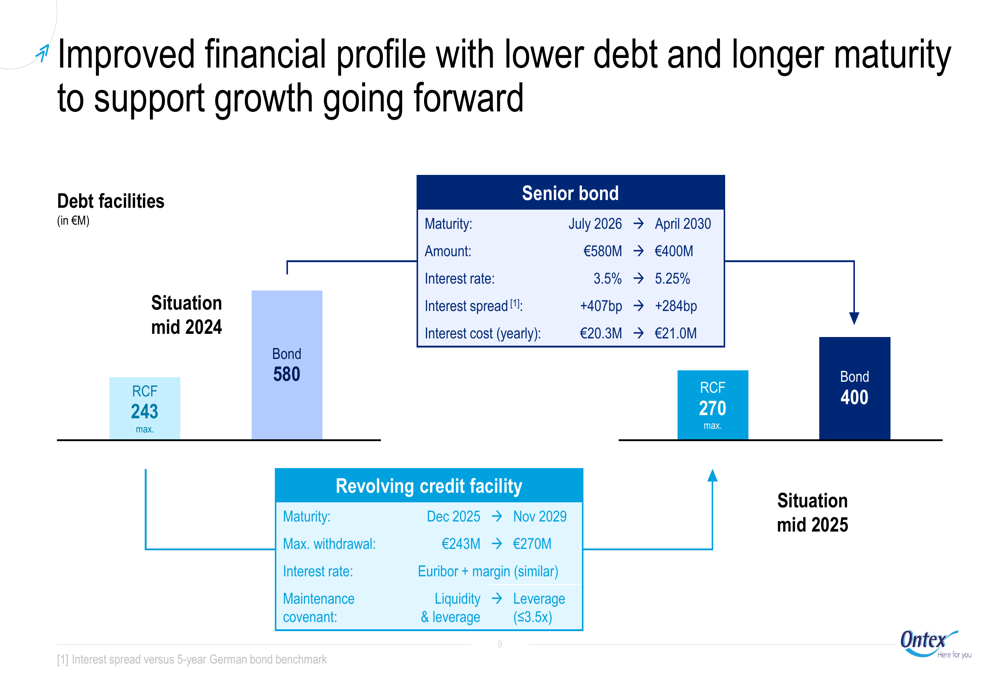

The company’s net financial debt stood at €656 million at the end of Q1 2025, with a leverage ratio of 2.7x. Management expects this ratio to improve to approximately 2.5x following the completion of the Brazilian divestment. The temporary increase in debt was attributed to higher inventories related to US tariff mitigation actions, restructuring expenses, and €10 million spent on share buybacks.

Ontex has significantly improved its debt profile, replacing a €580 million bond maturing in 2026 with a new €400 million bond maturing in 2030. The company also secured a larger revolving credit facility of €270 million, extending its maturity from December 2025 to November 2029.

The following chart illustrates the company’s improved financial profile:

Strategic Initiatives

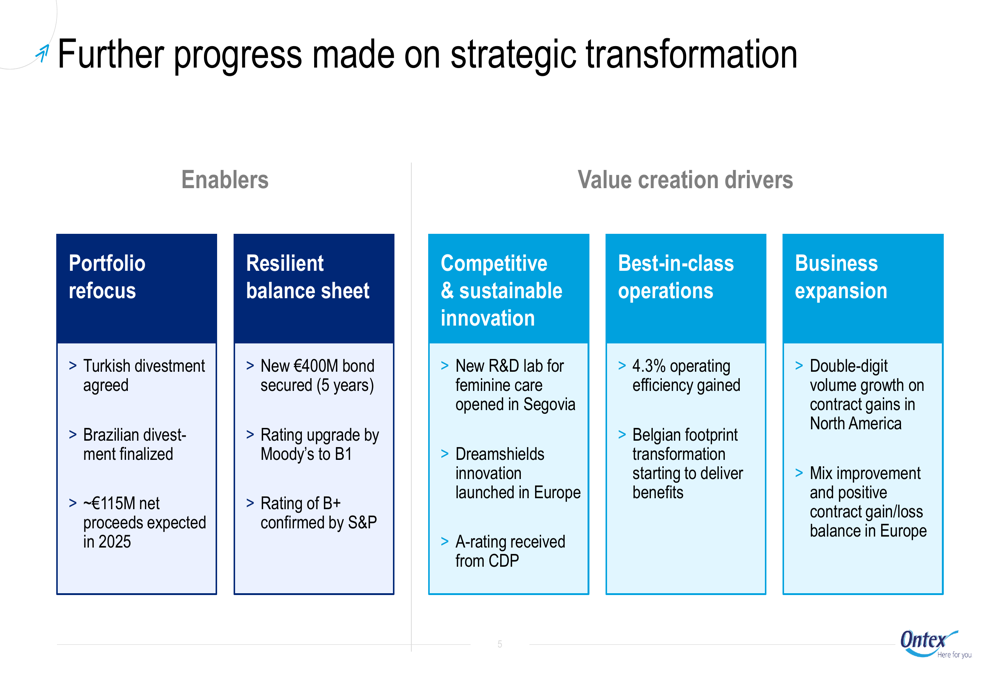

Despite the challenging quarter, Ontex continues to make progress on its strategic transformation. The company has agreed to divest its Turkish operations and finalized the sale of its Brazilian business, with expected net proceeds of approximately €115 million in 2025. These divestments align with Ontex’s portfolio refocus strategy.

The company highlighted several value creation drivers, including competitive and sustainable innovation, operational improvements, and business expansion. Notable achievements include opening a new R&D lab for feminine care in Segovia, launching Dreamshields innovation in Europe, and receiving an A-rating from CDP for environmental leadership.

The following chart outlines the company’s strategic transformation progress:

Operational efficiency improved by 4.3%, with the Belgian footprint transformation beginning to deliver benefits. In North America, the company achieved double-digit volume growth on contract gains, while in Europe, it reported mix improvement and a positive contract gain/loss balance.

Forward-Looking Statements

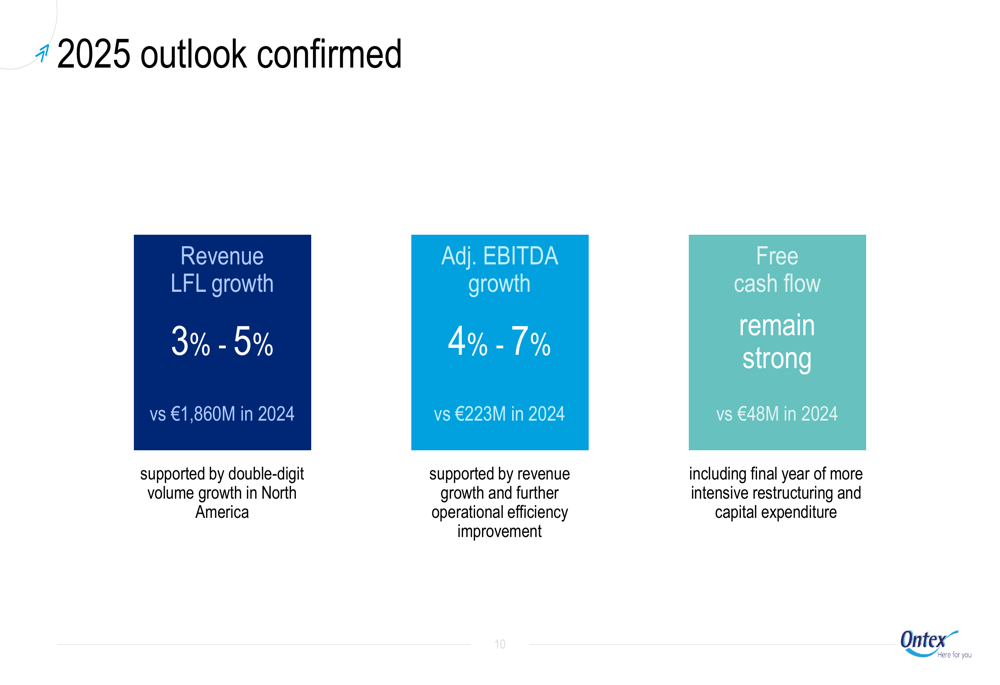

Despite the Q1 setback, Ontex confirmed its full-year 2025 outlook, projecting like-for-like revenue growth of 3-5% compared to €1,860 million in 2024, and adjusted EBITDA growth of 4-7% versus €223 million in 2024. Management also expects free cash flow to remain strong compared to the €48 million generated in 2024.

The company’s optimistic outlook is supported by anticipated double-digit volume growth in North America and further operational efficiency improvements. Management noted that 2025 represents the final year of intensive restructuring and capital expenditure.

The following slide details the company’s 2025 outlook:

Ontex expressed confidence in its ability to navigate the current geopolitical uncertainties, citing good resilience, focus on business expansion and innovation, new major contracts starting in Q3, and structural cost transformation savings. However, investors appeared skeptical, as evidenced by the sharp decline in the company’s stock price following the presentation.

The disconnect between Ontex’s maintained positive outlook and the market’s negative reaction suggests investors may be concerned about the company’s ability to reverse the Q1 decline and achieve its full-year targets in the face of persistent market challenges and economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.