Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Oportun Financial Corp (NASDAQ:OPRT) released its first quarter 2025 earnings presentation on May 8, 2025, highlighting its second consecutive quarter of GAAP profitability as the company continues to benefit from strategic shifts implemented over the past year. The financial technology company, which provides inclusive, affordable financial services to hardworking people, saw its stock rise 1.63% in aftermarket trading to $6.25, building on a 10.61% gain during regular trading hours.

The Q1 results reinforce the turnaround narrative that began in Q4 2024, when CEO Raul Vasquez stated the company had "turned the corner in improving financial performance." That momentum has continued into 2025, with significant year-over-year improvements across key financial and operational metrics.

Quarterly Performance Highlights

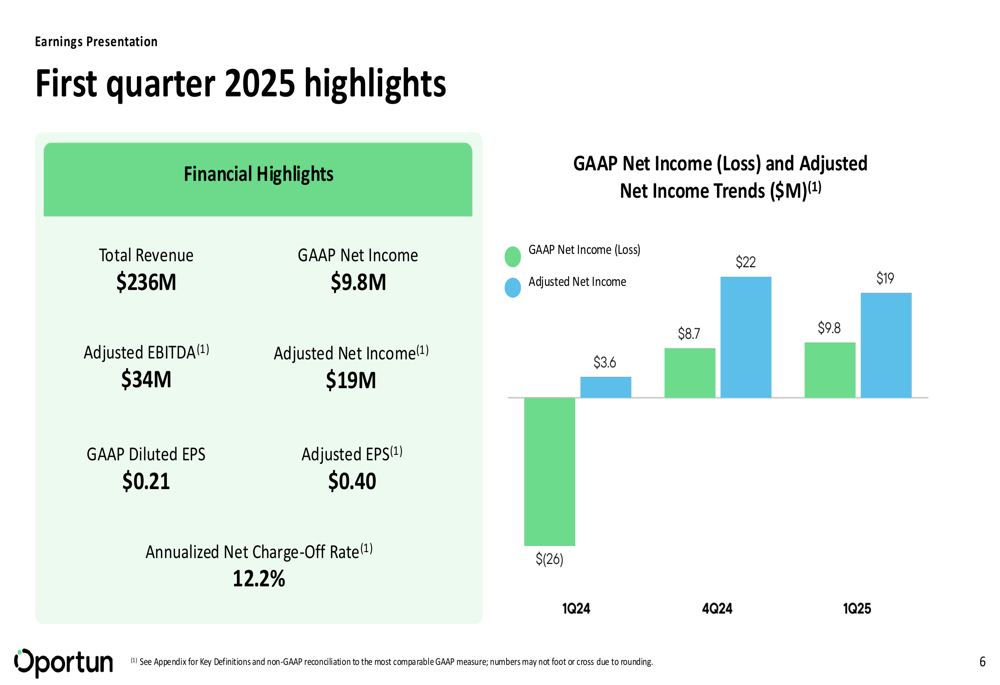

Oportun reported GAAP net income of $9.8 million ($0.21 per share) for Q1 2025, representing a substantial $36 million improvement from the $26 million loss in Q1 2024. The company’s adjusted net income reached $19 million, translating to adjusted earnings per share of $0.40, compared to just $0.09 in the same period last year.

The company exceeded its guidance across all key metrics for the quarter. Total (EPA:TTEF) revenue reached $236 million, surpassing the guidance range of $225-230 million. The annualized net charge-off rate came in at 12.2%, better than the guided 12.3%, while adjusted EBITDA of $34 million significantly outperformed the $18-22 million guidance.

As shown in the following chart of quarterly financial highlights and net income trends:

Adjusted EBITDA saw a remarkable year-over-year increase from $1.9 million in Q1 2024 to $34 million in Q1 2025. This improvement was driven by both revenue growth and substantial reductions in operating expenses, which declined 15% year-over-year to $92.7 million.

The company’s return on equity metrics also showed significant improvement, with GAAP ROE reaching 11.0% and adjusted ROE hitting 21.0%, compared to just 3.7% in Q1 2024. This performance improvement is illustrated in the following comparison:

Credit Quality Improvements

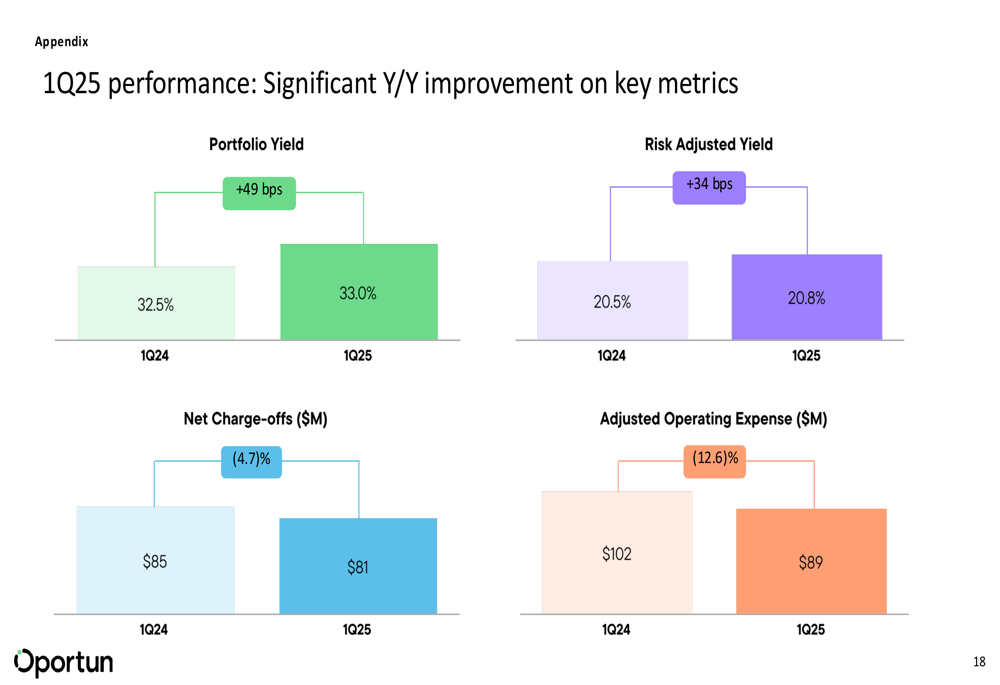

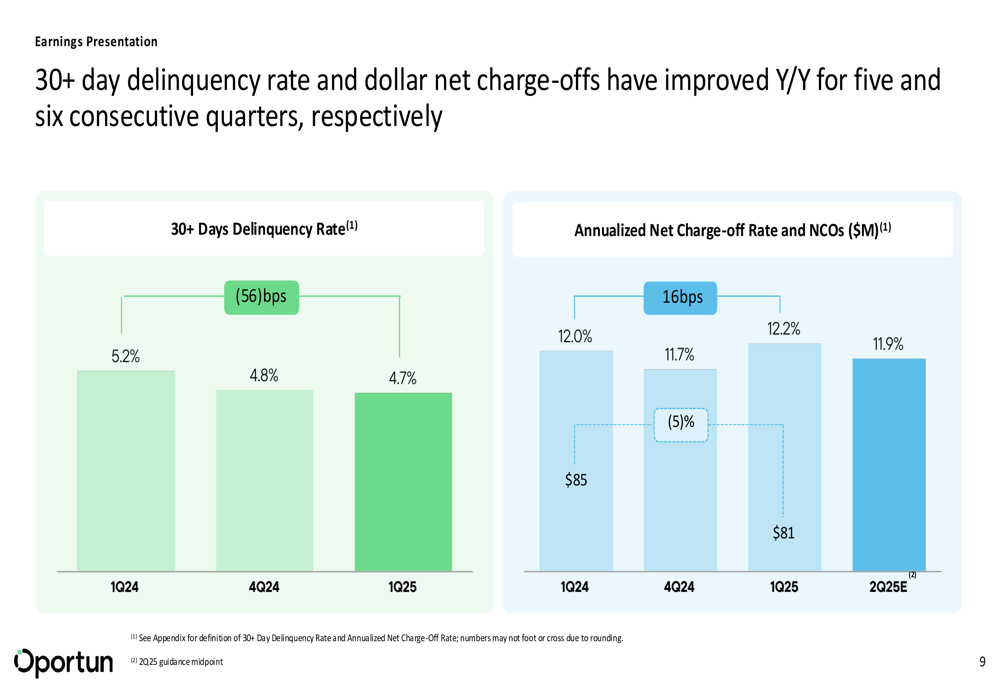

A key driver of Oportun’s improved financial performance has been the steady enhancement in credit quality. The 30+ day delinquency rate decreased to 4.7% in Q1 2025, down 56 basis points from 5.2% in Q1 2024. Similarly, dollar net charge-offs declined 5% year-over-year to $81 million.

The company’s credit improvement strategy is clearly illustrated in the following chart showing delinquency and charge-off trends:

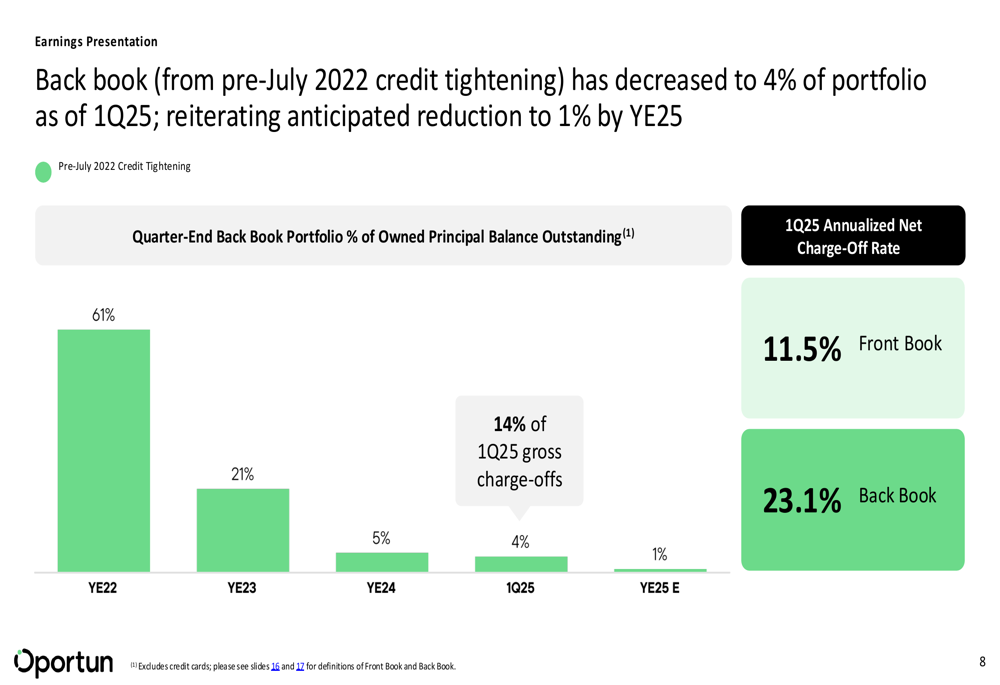

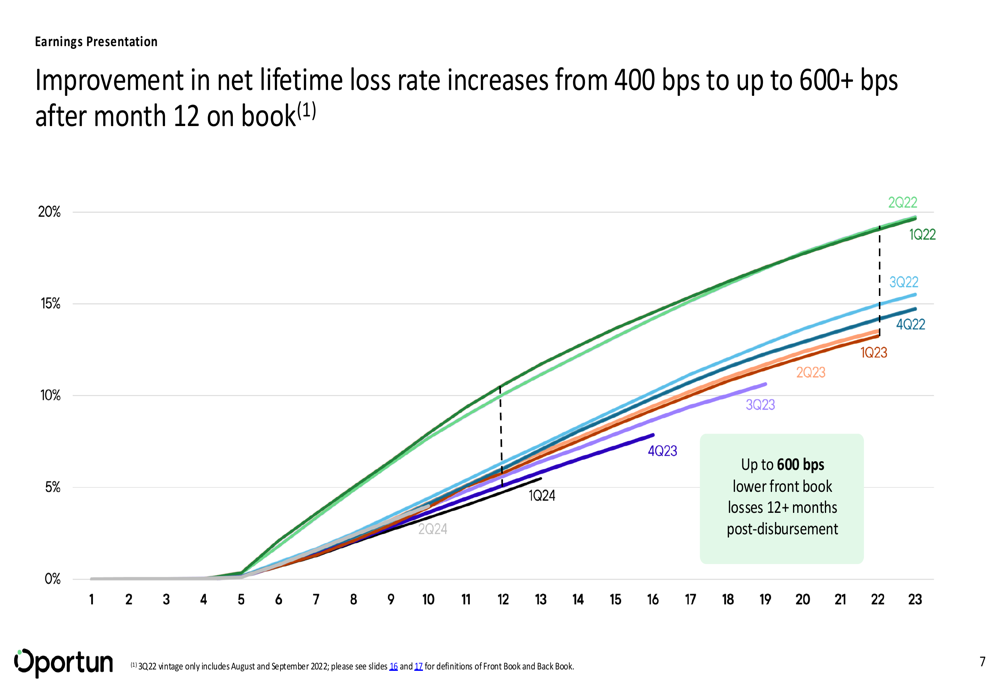

A significant component of Oportun’s credit quality improvement has been the ongoing reduction of its "back book" – loans originated before July 2022, which have substantially higher loss rates. As shown in the following chart, the back book has been reduced from 61% of the owned principal balance at the end of 2022 to just 4% in Q1 2025, with a target of 1% by year-end 2025:

The difference in performance between newer and older vintages is striking, with the Q1 2025 annualized net charge-off rate for the front book at 11.5%, compared to 23.1% for the back book. This improvement in loan vintage performance is further illustrated in the following chart showing the net lifetime loss rate by loan cohort:

Strategic Initiatives

Oportun’s presentation highlighted three strategic priorities that are driving its improved performance: improving credit outcomes, strengthening business economics, and identifying high-quality originations.

The company is focusing on better aligning loan amounts by risk levels and leveraging additional data to enhance its V12 credit model. This has resulted in five consecutive quarters of year-over-year improvement in 30+ day delinquency rates and six consecutive quarters of improvement in dollar net charge-offs.

Oportun is also placing greater emphasis on secured personal loans, which grew 59% year-over-year in Q1 2025. These loans have demonstrated approximately 500 basis points lower net charge-off rates compared to unsecured loans. Additionally, referral-driven originations grew 352% year-over-year to $35 million.

The company’s disciplined credit stance is supported by strong member stability metrics. For loans originated in Q1 2025, 100% of applicants had their income verified, with a median gross income of approximately $50,000. Borrowers demonstrated employment stability (5.2 years on average with the same employer) and residential stability (5.7 years on average at the same residence).

Forward-Looking Guidance

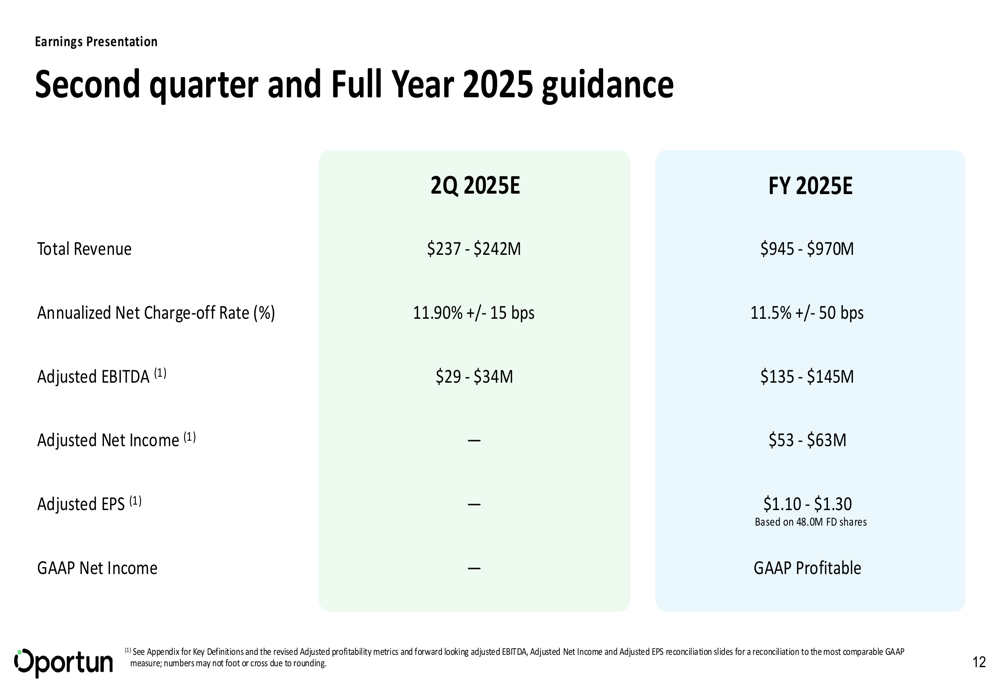

Oportun provided guidance for both the second quarter and full year 2025, projecting continued improvement in financial performance. For Q2 2025, the company expects:

- Total revenue of $237-242 million

- Annualized net charge-off rate of 11.90% (±15 basis points)

- Adjusted EBITDA of $29-34 million

For the full year 2025, Oportun reiterated its expectations for:

- Total revenue of $945-970 million

- Annualized net charge-off rate of 11.5% (±50 basis points), representing a 50 basis point improvement year-over-year at the midpoint

- Adjusted EBITDA of $135-145 million

- Adjusted net income of $53-63 million

- Adjusted EPS of $1.10-1.30, reflecting 53-81% growth year-over-year

- GAAP profitability for the full year

The detailed guidance is presented in the following chart:

The company also provided an interesting analysis of how the net charge-off rate is affected by the average daily principal balance (ADPB). If the ADPB had remained flat year-over-year instead of declining 5%, the Q1 2025 NCO rate would have been approximately 30 basis points lower at 11.4% instead of 12.2%. This suggests that as the company returns to growth, NCO rates could improve further.

Conclusion

Oportun’s Q1 2025 earnings presentation demonstrates that the company’s strategic shift toward higher-quality originations and operational efficiency is yielding tangible results. With two consecutive quarters of GAAP profitability, improving credit metrics, and strong forward guidance, the company appears to be successfully executing its turnaround strategy.

The reduction of the higher-risk back book portfolio, growth in secured personal loans, and enhanced underwriting capabilities position Oportun for continued improvement in 2025. While macroeconomic pressures and competition in the financial sector remain challenges, the company’s focus on serving stable, underbanked consumers with improving unit economics provides a foundation for sustainable growth.

Investors will be watching closely to see if Oportun can maintain this positive momentum throughout 2025 and deliver on its guidance for continued profitability and credit quality improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.