S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

Orexo AB (STO:ORX) presented its Q2 2025 interim report on July 16, 2025, revealing a challenging quarter marked by currency headwinds and one-time expenses. The Swedish pharmaceutical company’s stock dropped 8.54% following the presentation, with shares trading at SEK 18.6, down from the previous close of SEK 20.3.

Despite the negative market reaction, Orexo maintained its full-year guidance, emphasizing progress in its product pipeline and continued optimization of its Zubsolv business. The company faces a complex market environment with geopolitical uncertainties and evolving U.S. healthcare policies affecting its predominantly U.S.-focused business.

Quarterly Performance Highlights

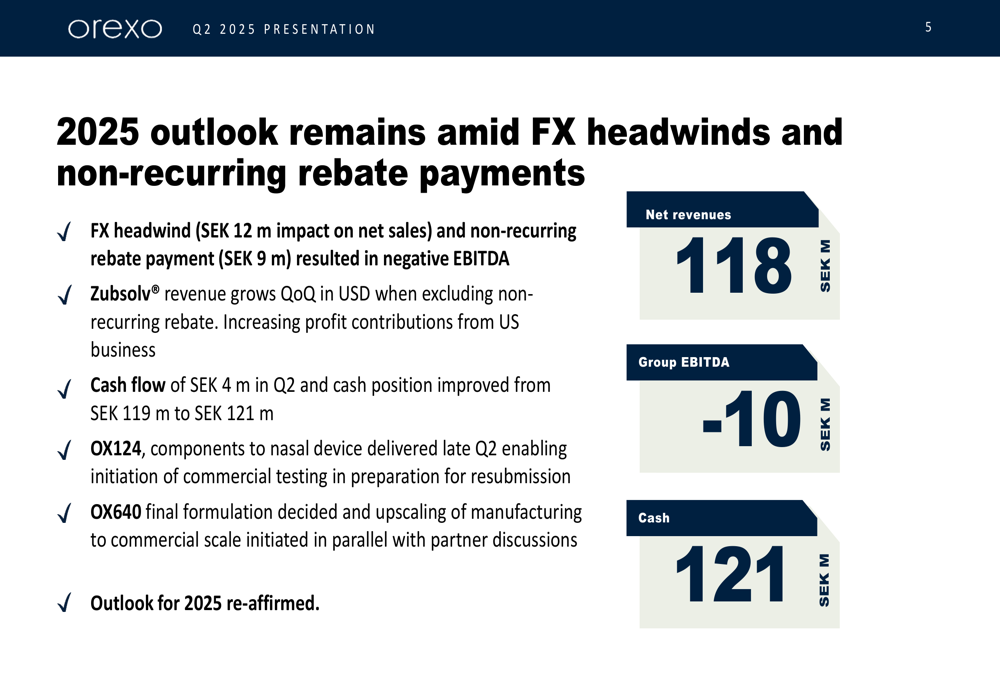

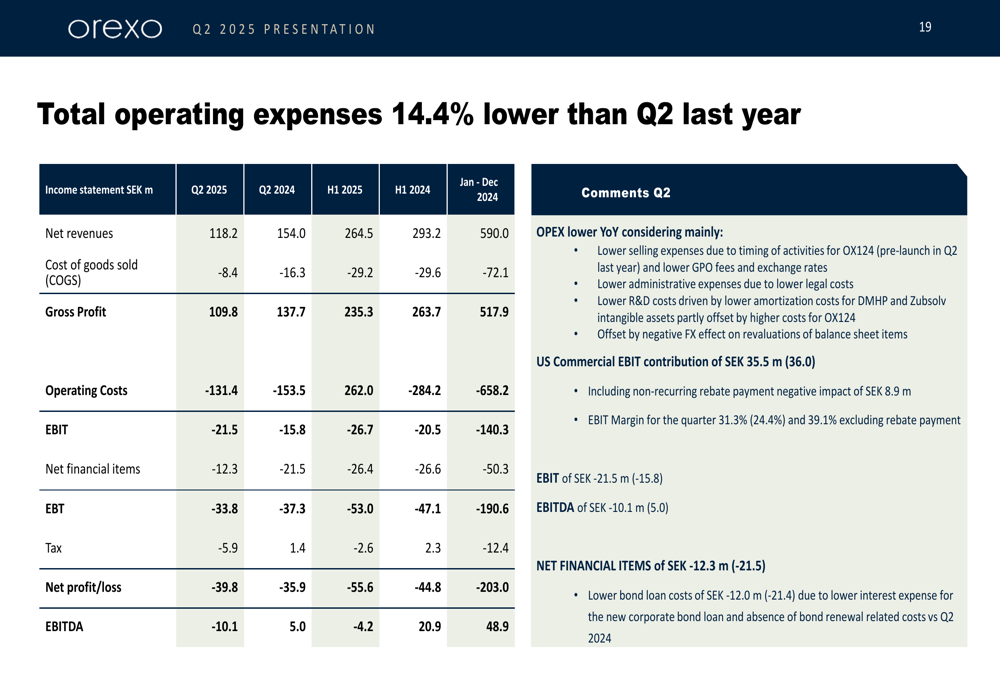

Orexo reported net revenues of SEK 118 million for Q2 2025, with the quarter’s performance significantly impacted by foreign exchange headwinds (SEK 12 million) and a non-recurring rebate payment (SEK 9 million). These factors resulted in a negative EBITDA of SEK 10 million, a notable decline from the positive EBITDA of SEK 5.9 million reported in Q1 2025.

As shown in the key highlights from the presentation:

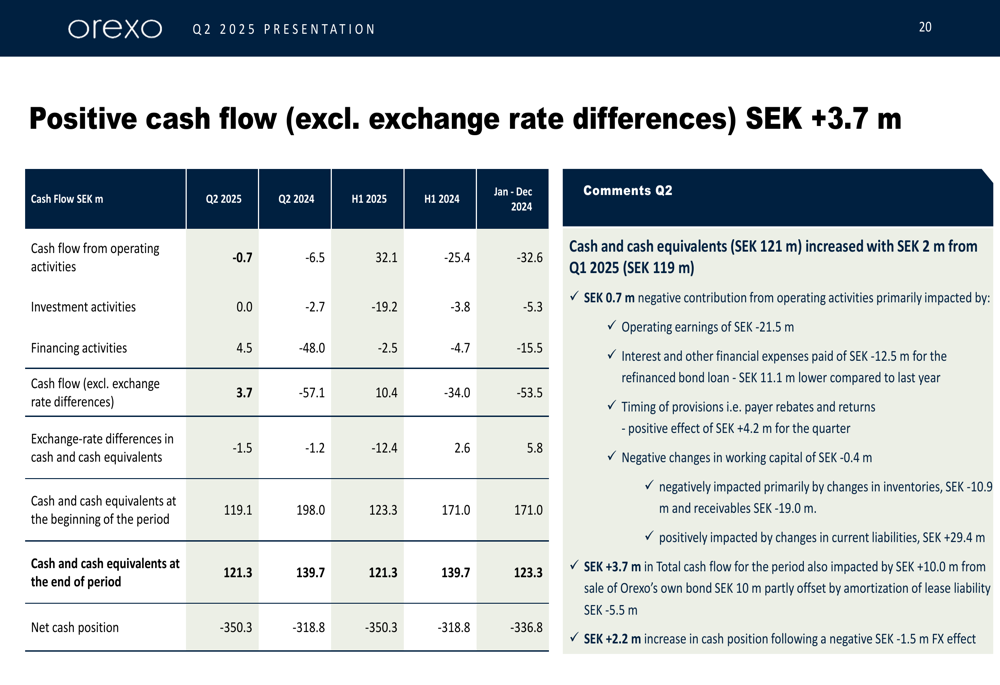

The company’s cash position improved slightly from SEK 119 million to SEK 121 million, with a positive cash flow of SEK 4 million in Q2. This modest improvement in cash position demonstrates the company’s ability to manage its finances despite the challenging quarter.

The buprenorphine/naloxone market, where Orexo’s lead product Zubsolv competes, showed continued growth with a 4% year-over-year increase and 2% quarter-over-quarter growth. The commercial segment showed particularly strong growth at 11% year-over-year, while the Medicaid segment growth stagnated at 1% and the cash segment declined by 11%.

Product Pipeline Updates

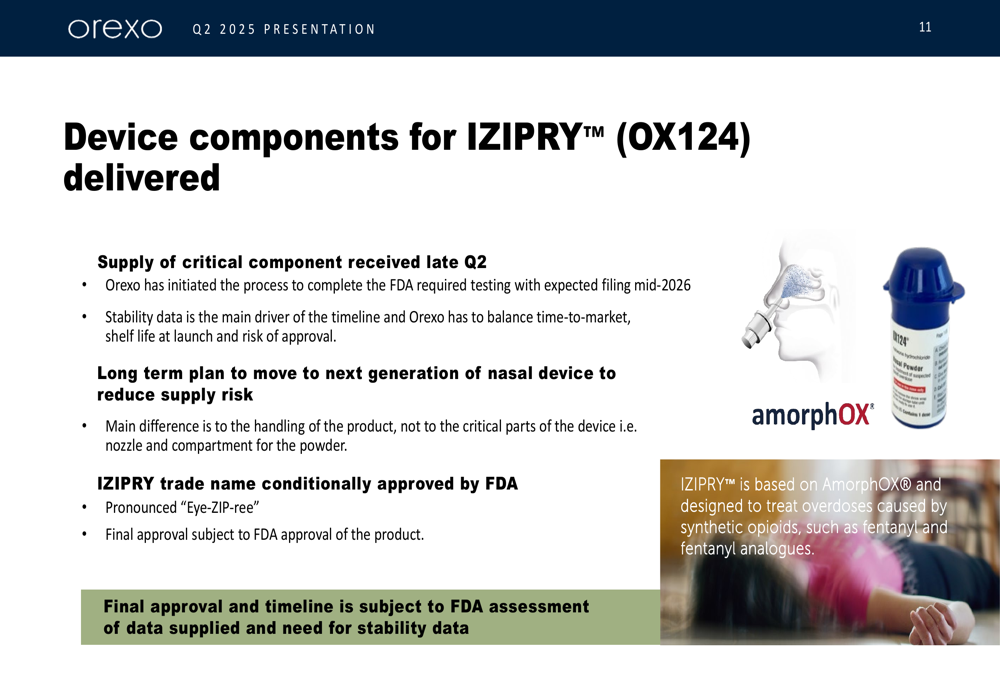

Orexo made significant progress with its product pipeline during the quarter, particularly with its IZIPRY (OX124) naloxone rescue medication and OX640 adrenaline rescue treatment.

For IZIPRY, the company received critical device components late in Q2, enabling the initiation of FDA-required testing with an expected filing by mid-2026. The FDA has conditionally approved the IZIPRY trade name for this product.

As illustrated in the presentation:

The company’s OX640 adrenaline product also reached important milestones, with the final formulation decided and manufacturing upscaling to commercial scale initiated. Orexo indicated that existing manufacturing capacity is capable of supporting the launch and initial global distribution, with additional capacity under construction for commercial use in H1 2026.

Partnering discussions for OX640 are ongoing in parallel with manufacturing upscaling, representing a potential value driver for the company. Orexo compared the market opportunity for OX640 to that of Narcan, which grew from less than $5 million in sales in 2015 to over $130 million by Q3 2021.

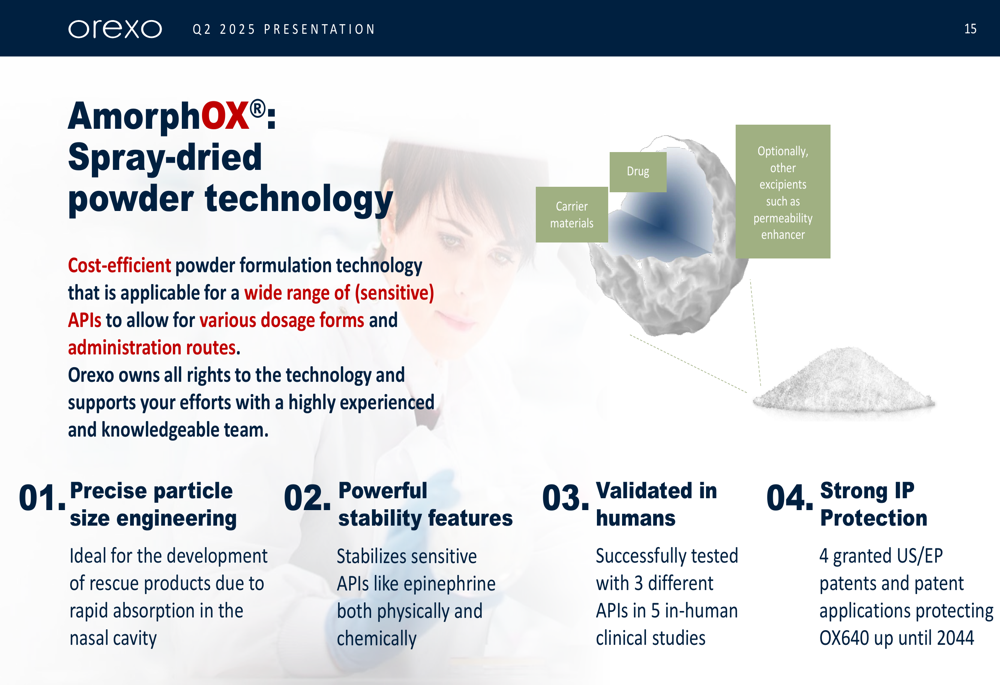

The company’s proprietary AmorphOX technology platform, which underpins these development programs, offers several advantages including cost-efficient powder formulation, precise particle size engineering, and strong stability features. This technology has been validated in humans and has strong IP protection.

Financial Analysis

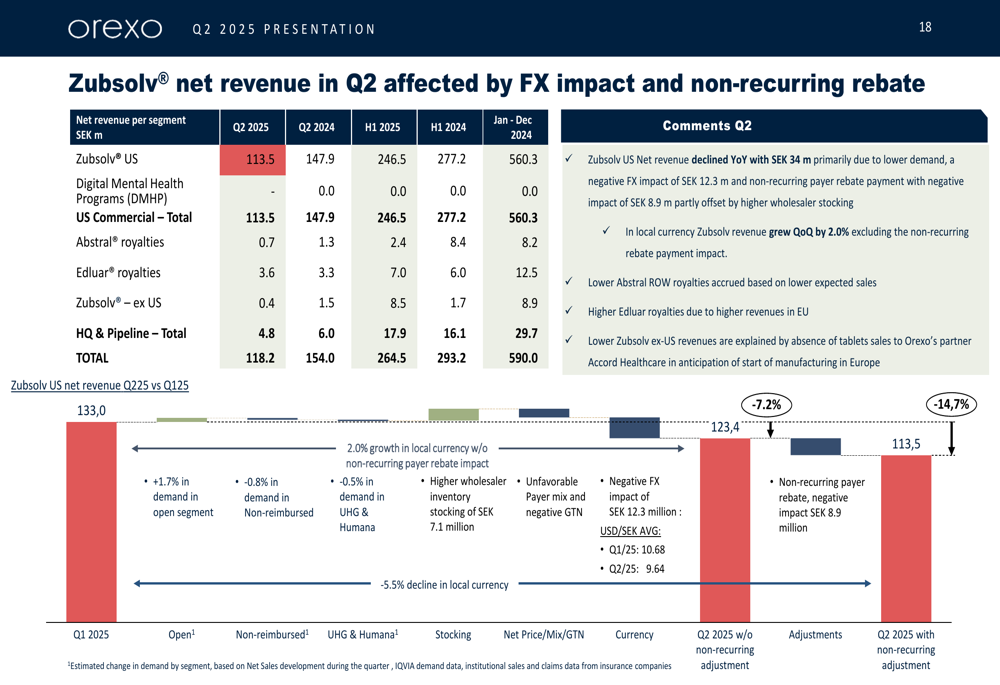

Zubsolv remains Orexo’s primary revenue driver, with net revenue of SEK 113.5 million in Q2. When excluding the non-recurring rebate payment impact, Zubsolv revenue grew quarter-over-quarter by 2.0% in local currency.

The detailed financial breakdown shows:

Total (EPA:TTEF) operating expenses were SEK 131.4 million, resulting in an EBIT of negative SEK 21.5 million. Despite these challenges, the company has continued to optimize its Zubsolv business, reducing selling and administrative expenses by 27% and increasing the EBIT margin to 39%.

Cash flow analysis reveals that despite the negative EBITDA, Orexo managed to maintain stable cash reserves:

Forward Outlook

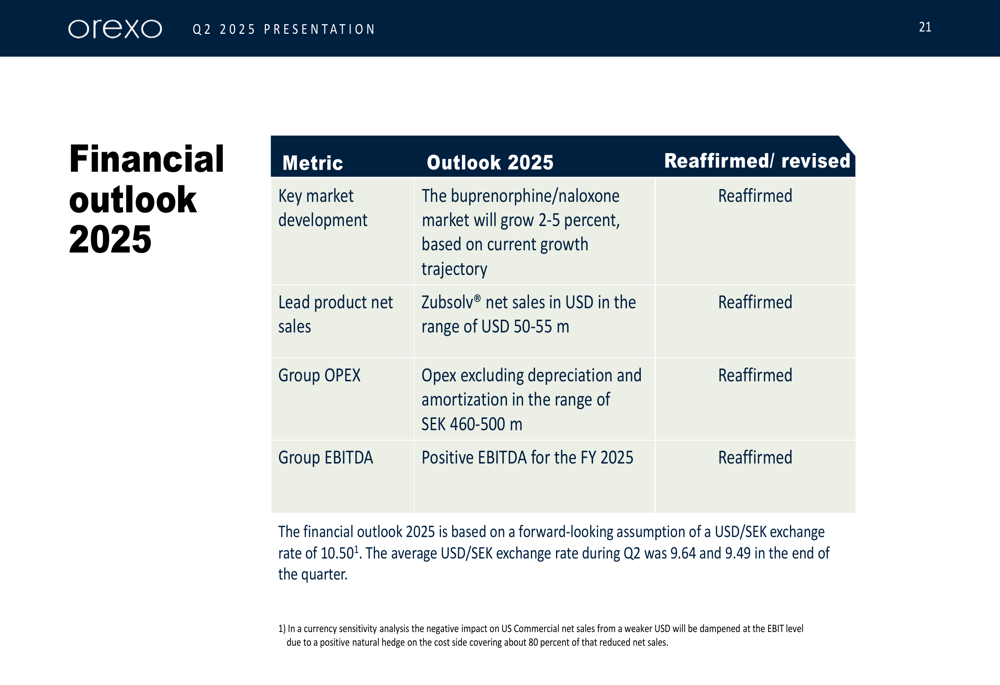

Orexo reaffirmed its financial outlook for 2025 despite the Q2 challenges. The company expects the buprenorphine/naloxone market to grow by 2-5% and projects Zubsolv net sales in the range of USD 50-55 million. Group operating expenses are expected to be between SEK 460-500 million, with positive EBITDA for the full year.

This outlook suggests management’s confidence in recovering from the temporary setbacks experienced in Q2. The company’s strategy focuses on three main areas: growing revenues and profit contributions from existing products, improving access to treatment, and capitalizing on the AmorphOX technology platform.

The company also noted an ongoing investigation by U.S. authorities that began in July 2020, representing a potential regulatory risk that investors should monitor.

Analyst Perspectives

While the Q2 results fell short of expectations, with negative EBITDA contrasting with the positive EBITDA of SEK 5.9 million reported in Q1, Orexo’s maintained guidance suggests the company views these challenges as temporary. The continued investment in pipeline products indicates confidence in future growth opportunities beyond the current Zubsolv business.

The market reaction reflects investor concerns about the immediate financial performance, but the company’s progress with its pipeline products and technology platform may offer longer-term value. Investors will likely focus on whether Orexo can return to positive EBITDA in the coming quarters and meet its full-year guidance while advancing its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.