Gold prices hover near 6-week high amid softer dollar, Fed rate cut bets

Introduction & Market Context

Polish energy giant ORLEN Group (WSE:PKN) presented its first quarter 2025 financial results on May 22, demonstrating remarkable resilience in a challenging macro environment. Despite facing headwinds from lower oil prices and refining margins, the company reported a 40% year-over-year increase in EBITDA LIFO, showcasing the strength of its diversified business model.

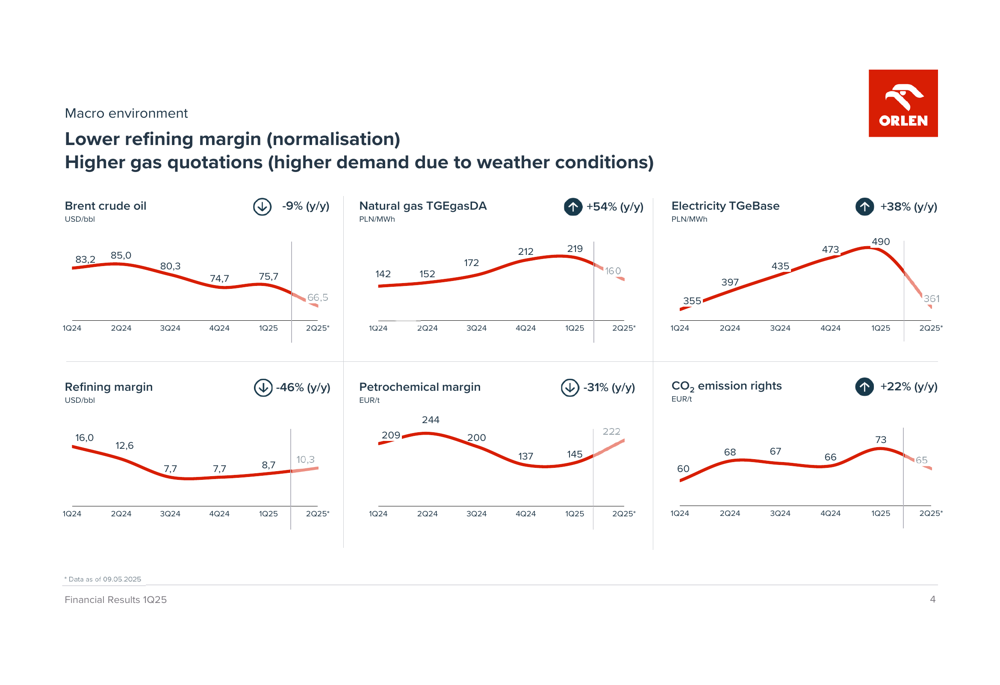

The quarter was characterized by significant market volatility, with Brent crude prices falling to $75.7 per barrel from $83.2 in Q1 2024, while natural gas prices surged over 54% and electricity prices jumped nearly 38%. This divergent commodity price environment created both challenges and opportunities across ORLEN’s business segments.

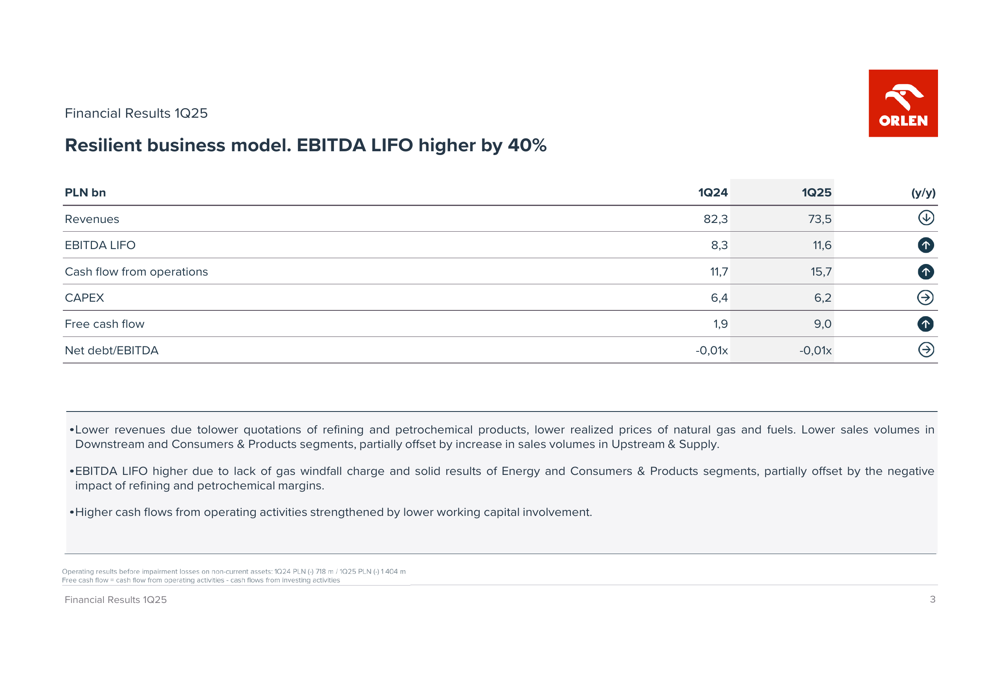

As shown in the following chart of key financial metrics, ORLEN delivered strong bottom-line growth despite a revenue decline:

Quarterly Performance Highlights

ORLEN’s EBITDA LIFO reached 11.6 billion PLN in Q1 2025, up 40% from 8.3 billion PLN in the same period last year. This impressive growth came despite a 10.7% decline in revenues to 73.5 billion PLN. The company’s cash flow from operations increased by 34% to 15.7 billion PLN, while free cash flow surged to 9.0 billion PLN from 1.9 billion PLN a year earlier.

The company’s performance was achieved against a backdrop of mixed macro indicators, with declining oil prices and refining margins offset by higher natural gas and electricity prices.

The following chart illustrates these key macro environment indicators:

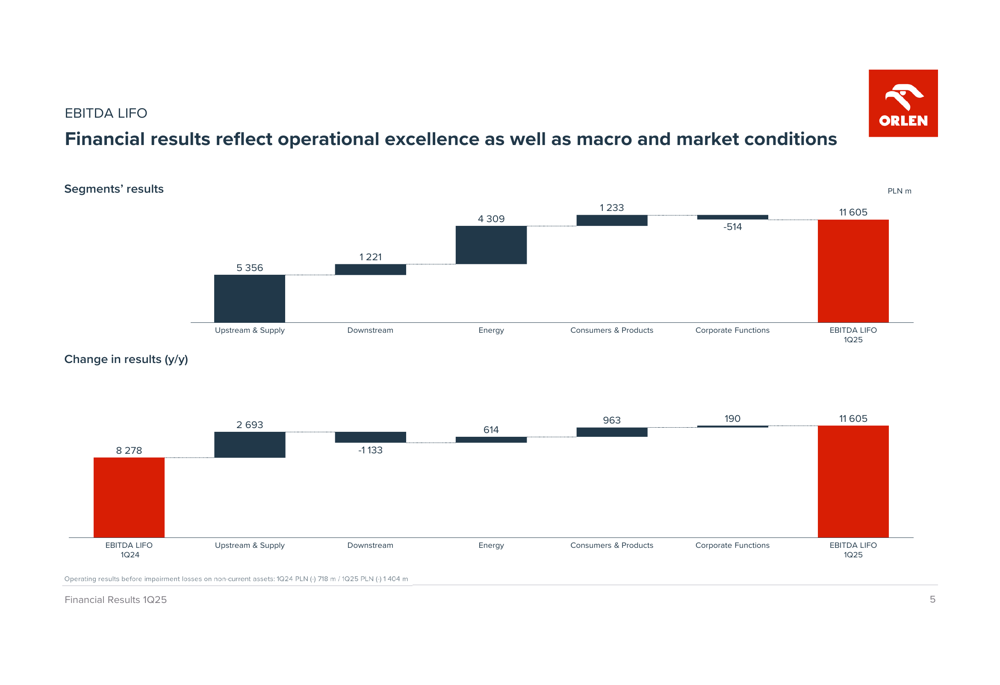

ORLEN’s segment performance showed significant divergence, with Upstream & Supply and Consumers & Products posting strong growth, while Downstream faced challenges from normalizing refining margins and lower petrochemical demand.

The segment breakdown of EBITDA LIFO reveals these contrasting performances:

Segment Performance Analysis

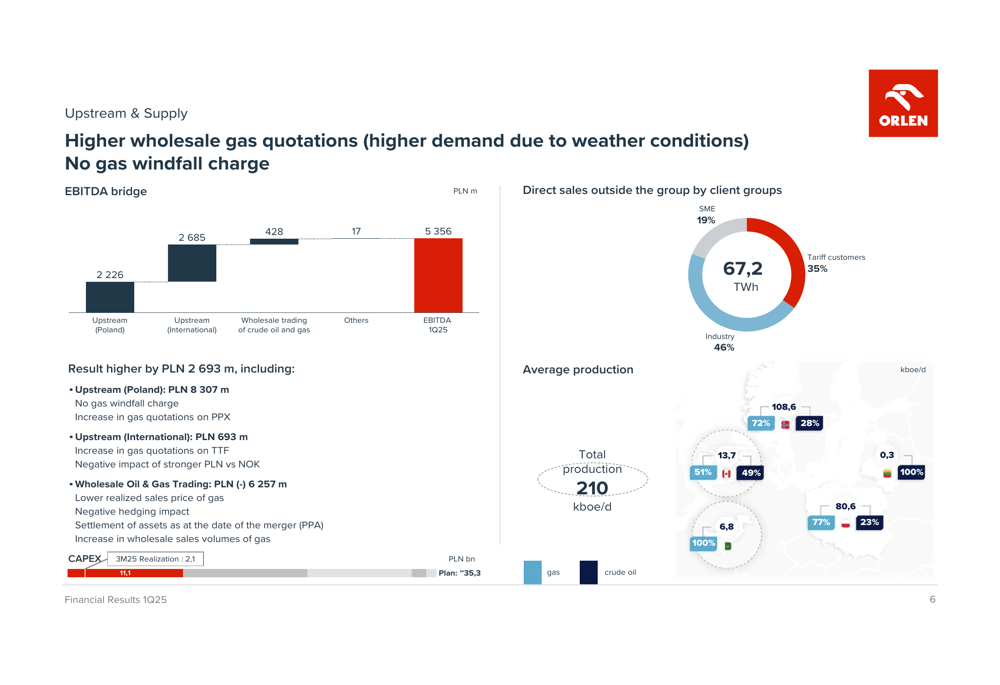

The Upstream & Supply segment was the standout performer, with EBITDA more than doubling to 5.36 billion PLN from 2.66 billion PLN in Q1 2024. This growth was primarily driven by favorable gas quotations on PPX and TTF, partially offset by the negative impact of a stronger PLN against the Norwegian krone. The segment maintained stable production at 210 kboe/d.

As illustrated in the following segment breakdown:

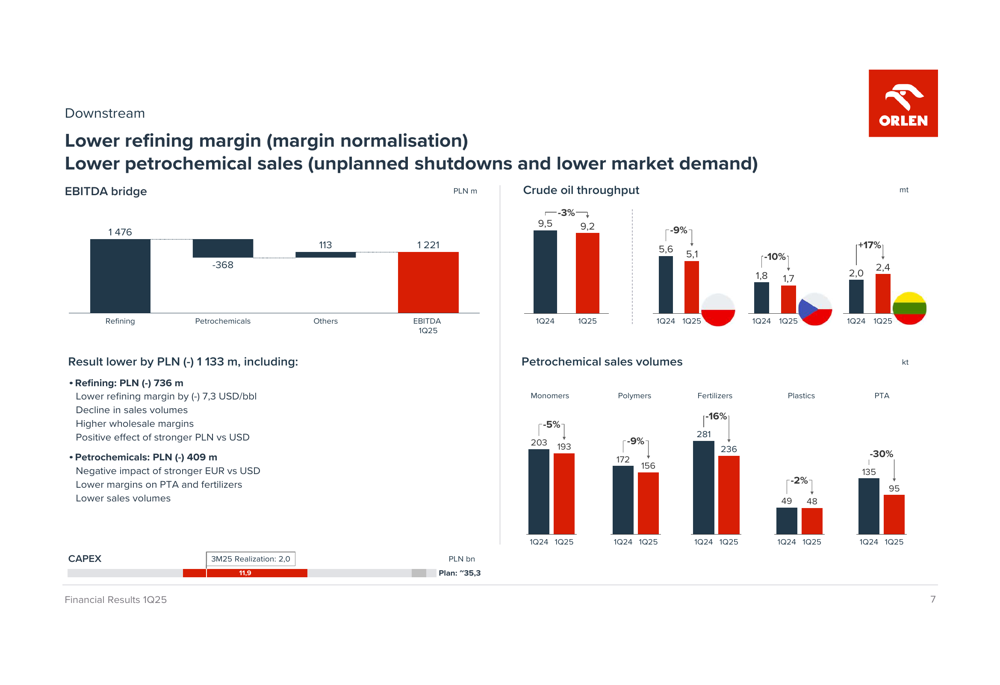

The Downstream segment faced significant headwinds, with EBITDA declining by nearly 50% to 1.22 billion PLN. This was attributed to normalizing refining margins after the exceptional levels seen in previous periods, as well as lower petrochemical sales due to unplanned shutdowns and weaker market demand. Crude oil throughput decreased by 3% to 9.2 million tons.

The following chart details the Downstream segment’s performance:

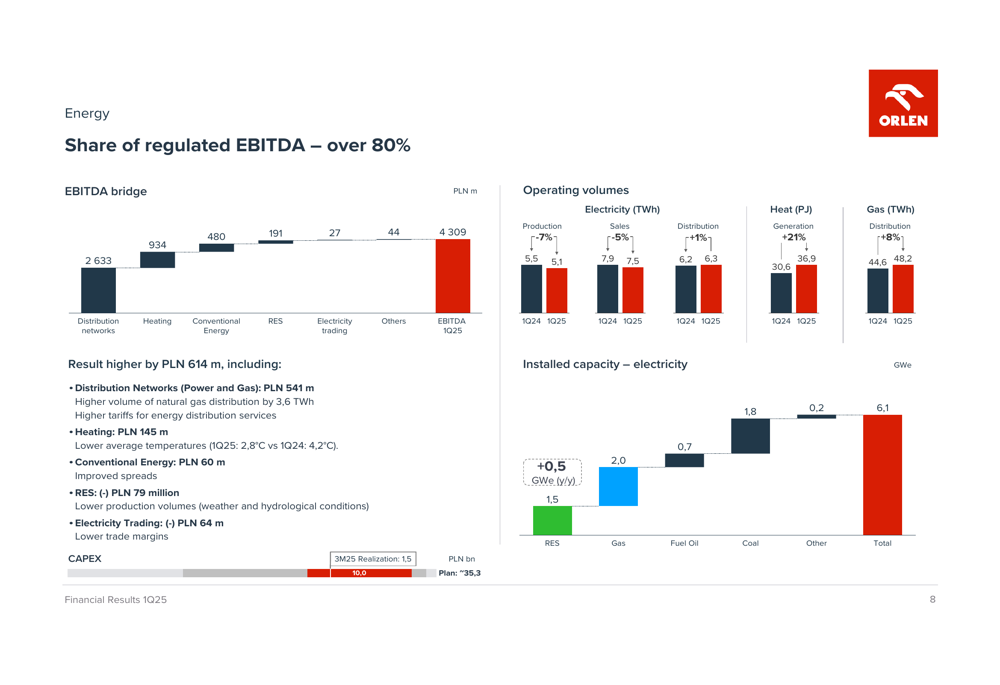

The Energy segment delivered solid growth, with EBITDA increasing by 17% to 4.31 billion PLN. Notably, over 80% of this segment’s EBITDA comes from regulated activities, providing stability amid market volatility. The segment’s performance was supported by strong distribution networks and heating operations.

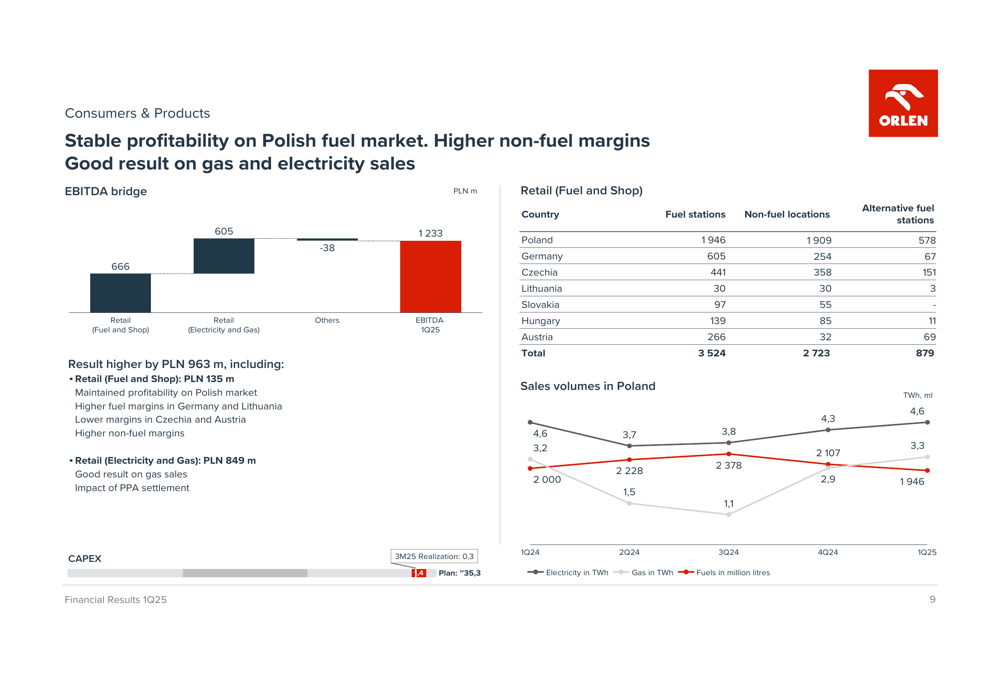

The Consumers & Products segment showed remarkable growth, with EBITDA more than quadrupling to 1.23 billion PLN from 270 million PLN in Q1 2024. This was driven by stable profitability in the Polish fuel market and higher non-fuel margins. The company continues to expand its retail network and alternative fuel stations across Central Europe.

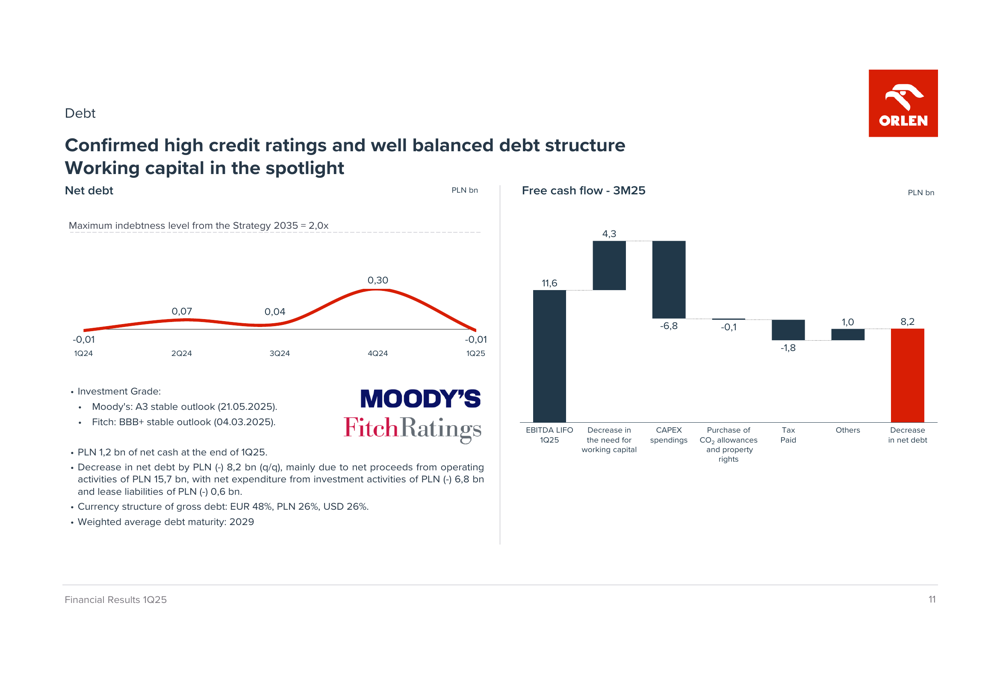

Financial Position & Cash Flow

ORLEN maintained a strong financial position with essentially zero net debt (net debt/EBITDA ratio of -0.01x), providing significant financial flexibility for future investments. The company’s investment grade credit ratings were confirmed by both Moody’s and Fitch.

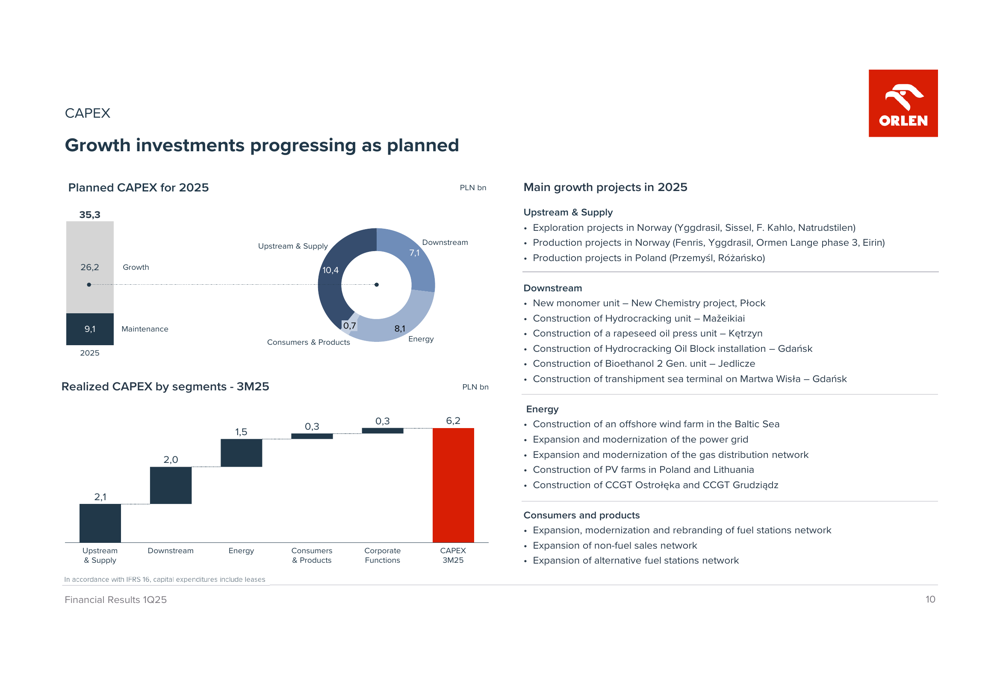

Capital expenditure (CAPEX) for Q1 2025 reached 6.2 billion PLN, slightly below the 6.4 billion PLN spent in Q1 2024. The company’s growth investments are progressing as planned across all segments, with particular focus on upstream assets, downstream projects, and energy infrastructure.

The following chart illustrates ORLEN’s CAPEX allocation and major growth projects:

Free cash flow generation was particularly strong at 9.0 billion PLN for the quarter, benefiting from robust EBITDA and a decrease in working capital requirements. This strong cash generation supports ORLEN’s ability to fund its ambitious investment program while maintaining financial discipline.

Forward-Looking Statements

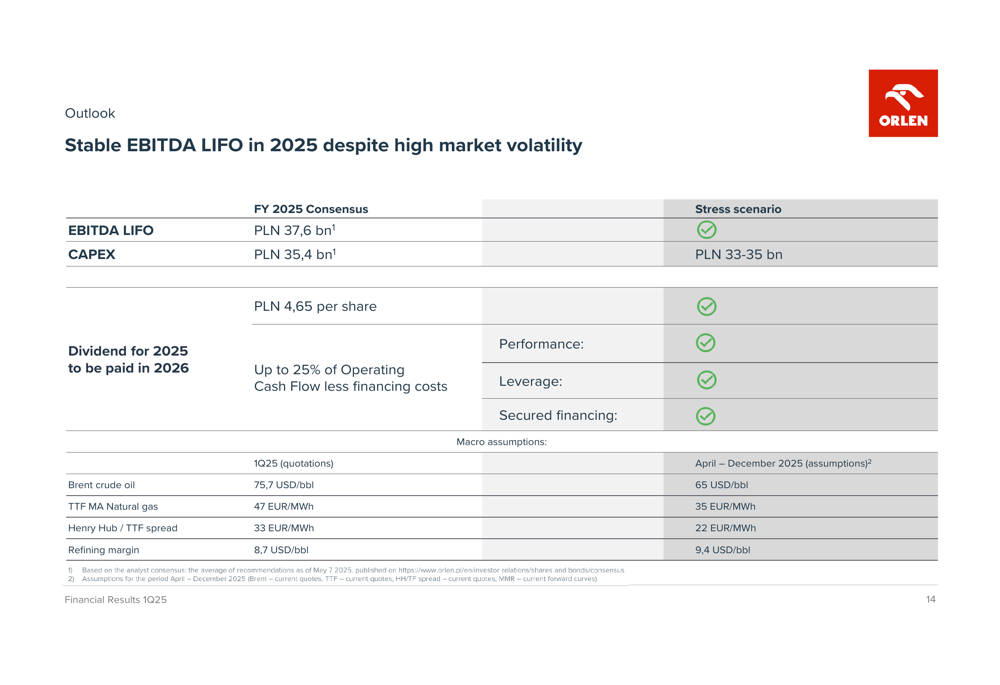

Looking ahead, ORLEN expects stable EBITDA LIFO for full-year 2025 despite continued market volatility. The company anticipates Brent crude prices to remain around $75-80 per barrel, with refining margins in the high single digits. Natural gas and electricity prices are expected to remain elevated compared to 2024 levels.

The following outlook details ORLEN’s expectations for 2025:

For the full year 2025, ORLEN has provided both consensus and stress scenario projections. Under the consensus scenario, the company expects EBITDA LIFO of approximately 45 billion PLN, CAPEX of 32 billion PLN, and dividends of 6 billion PLN. The stress scenario, which assumes lower oil prices and refining margins, projects EBITDA LIFO of 40 billion PLN.

ORLEN is also implementing a new segmental structure in line with its Strategy 2035, dividing operations into Upstream, Gas, Refining, Petrochemicals, Retail, and Energy segments. This reorganization aims to enhance transparency and strategic focus across the company’s diverse business portfolio.

In conclusion, ORLEN’s Q1 2025 results demonstrate the company’s ability to navigate a volatile energy market environment while delivering strong financial performance. The diversified business model has proven resilient, with strength in Upstream & Supply and Consumers & Products offsetting challenges in the Downstream segment. With zero net debt and strong cash flow generation, ORLEN is well-positioned to execute its strategic growth initiatives while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.