Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Otis Worldwide Corp (NYSE:OTIS) shares plunged more than 10% in premarket trading after the elevator and escalator manufacturer released its Q2 2025 earnings presentation on July 23, revealing mixed results that highlighted stark contrasts between its business segments.

Introduction & Market Context

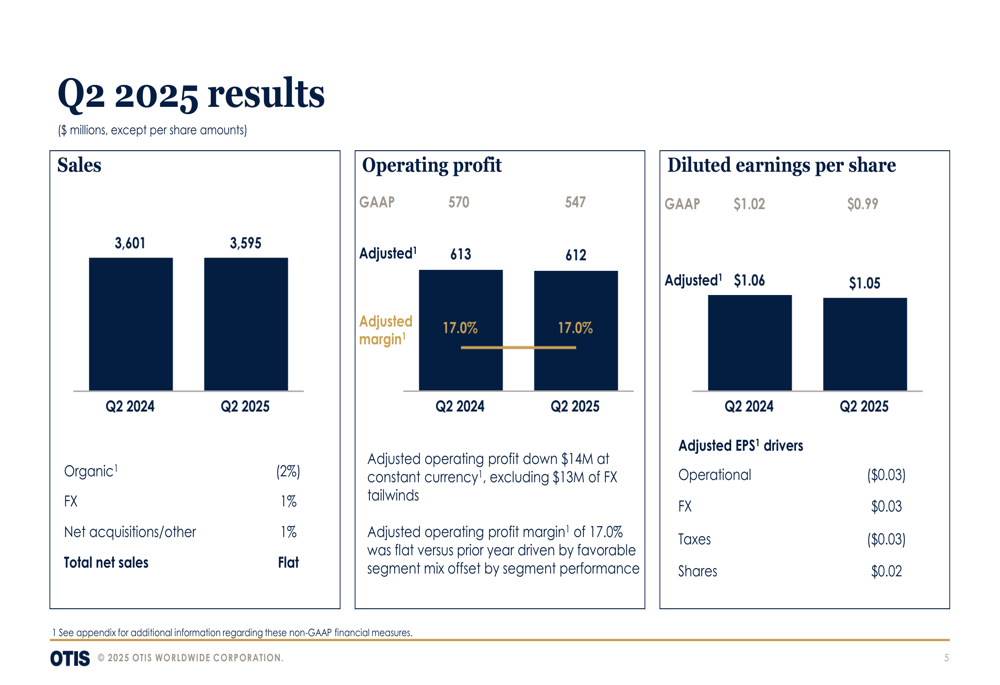

The company reported flat overall sales of $3.595 billion compared to $3.601 billion in Q2 2024, with adjusted earnings per share slightly declining to $1.05 from $1.06 a year earlier. While Otis maintained its full-year adjusted EPS guidance of $4.00 to $4.10, investors appeared concerned about significant weakness in the company’s New Equipment segment, particularly in China.

As shown in the following quarterly results overview, Otis delivered flat sales despite organic sales declining 2%, offset by favorable foreign exchange and acquisition impacts:

Quarterly Performance Highlights

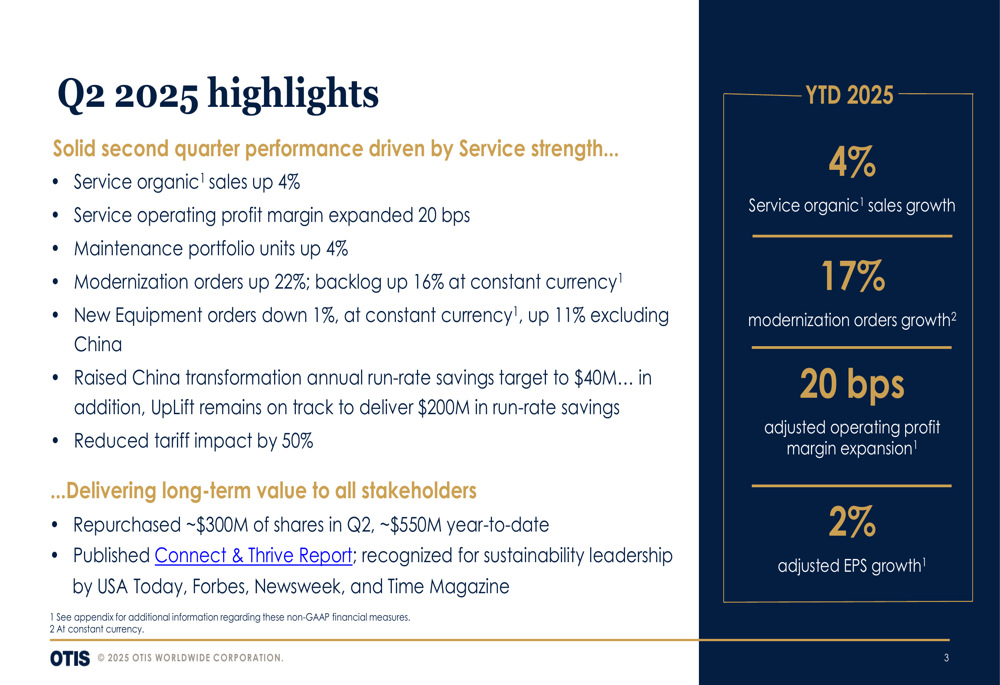

Otis characterized its second quarter as a "solid performance driven by Service strength," with service organic sales growing 4% and service operating profit margin expanding 20 basis points. The company’s maintenance portfolio units increased 4%, while modernization orders surged 22% with backlog up 16% at constant currency.

However, these positive developments were overshadowed by challenges in the New Equipment segment, where orders declined 1% overall, though they increased 11% when excluding China. The company highlighted its progress in reducing tariff impact by 50% and advancing its cost-saving initiatives.

The following slide illustrates the key highlights from the quarter:

Segment Analysis

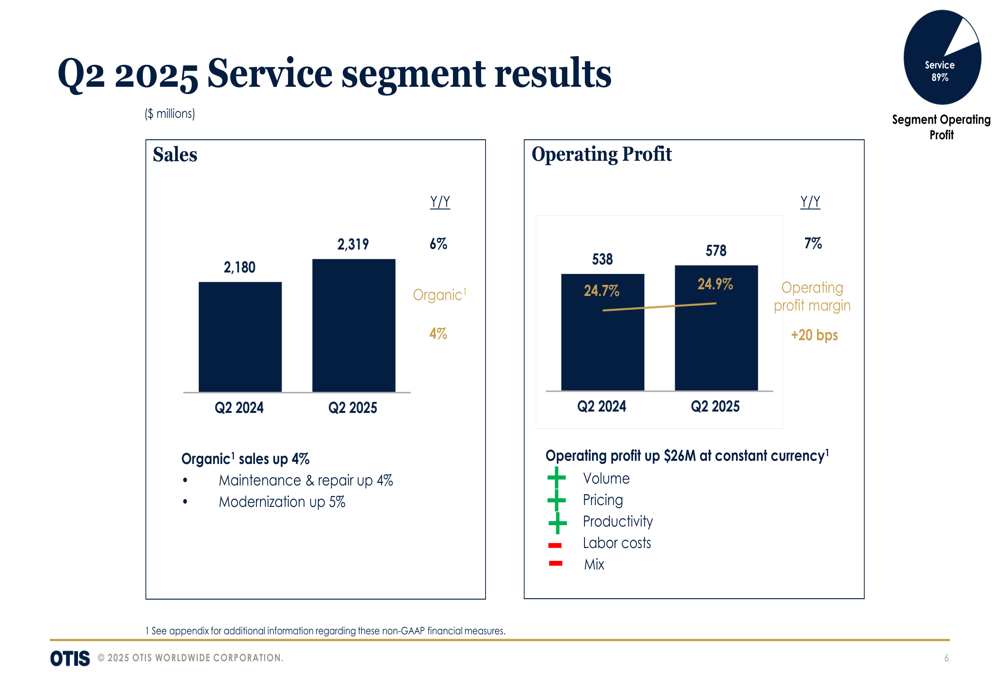

The stark contrast between Otis’s business segments was evident in the detailed financial breakdowns. The Service segment, which represents 89% of the company’s operating profit, delivered strong results with sales up 6% year-over-year to $2.319 billion and operating profit increasing 7% to $578 million. Service operating profit margin expanded 20 basis points to 24.9%.

The service segment performance is illustrated in the following chart:

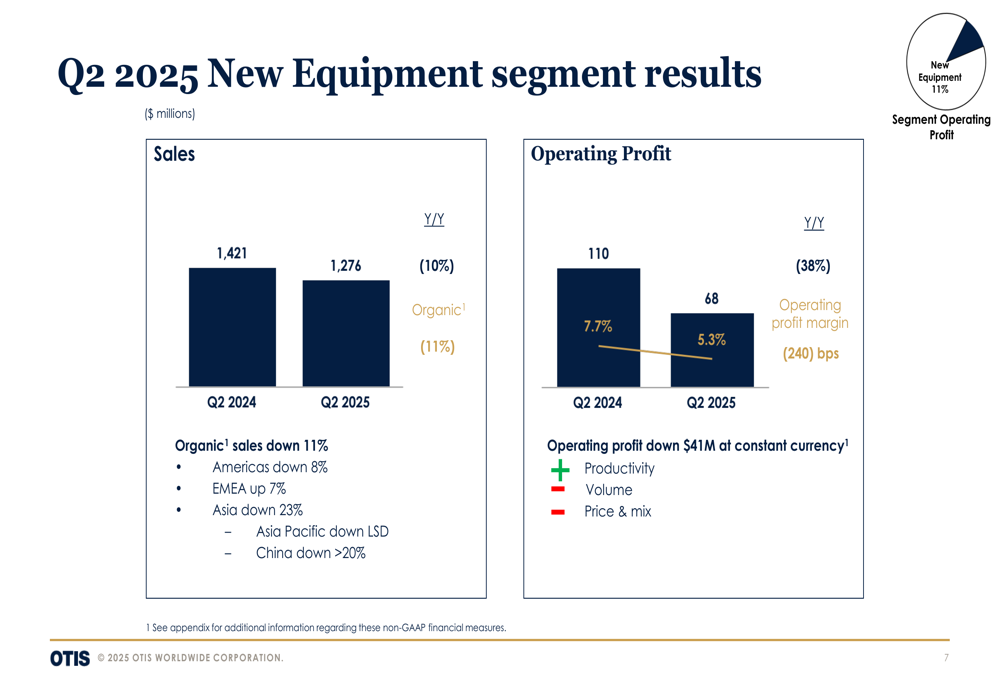

Meanwhile, the New Equipment segment faced significant headwinds, with sales declining 10% year-over-year to $1.276 billion and operating profit plummeting 38% to $68 million. The segment’s operating margin contracted sharply by 240 basis points to 5.3%. Particularly concerning was the performance in Asia, where organic sales fell 23%, with China down more than 20%.

The following slide details the New Equipment segment’s challenges:

The orders and backlog data further highlighted these divergent trends, with New Equipment orders down 1% overall but up 11% excluding China, while Modernization orders surged 22% across all regions:

Strategic Initiatives & Cost Savings

Otis emphasized its progress on strategic cost-saving initiatives, including the UpLift program and China transformation efforts. The company raised its China transformation annual run-rate savings target to $40 million, while the UpLift initiative remains on track to deliver $200 million in run-rate savings.

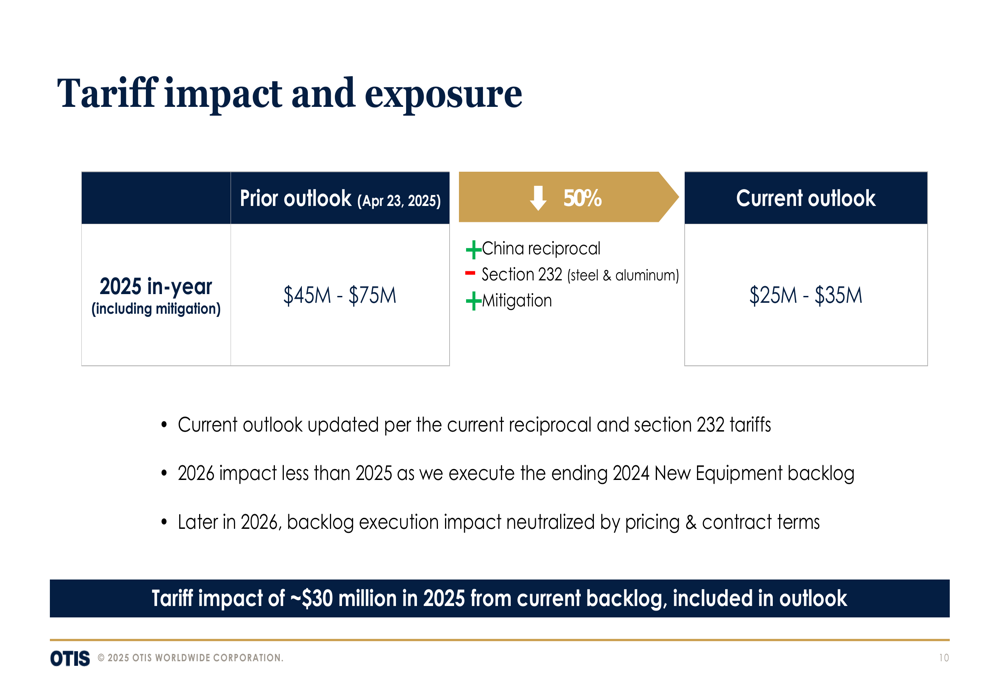

The company also highlighted its success in mitigating tariff impacts, reducing the expected 2025 impact from $45-$75 million to $25-$35 million, representing a 50% reduction. This improvement was attributed to changes in China reciprocal tariffs, Section 232 tariffs on steel and aluminum, and various mitigation strategies.

As shown in the following slide, Otis expects the tariff impact to diminish further in 2026:

Outlook & Guidance

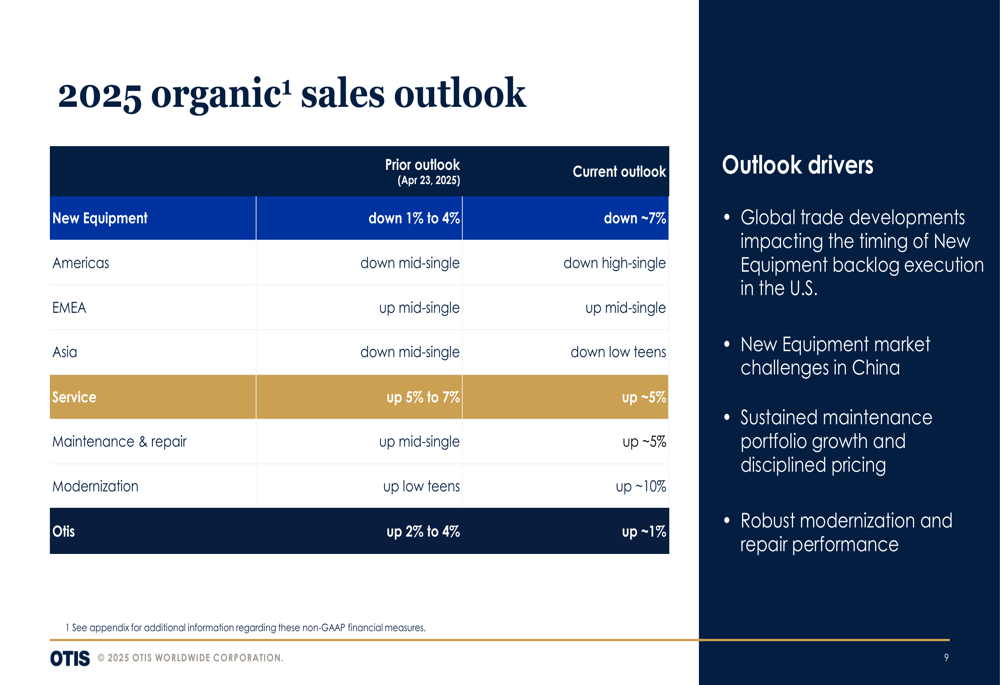

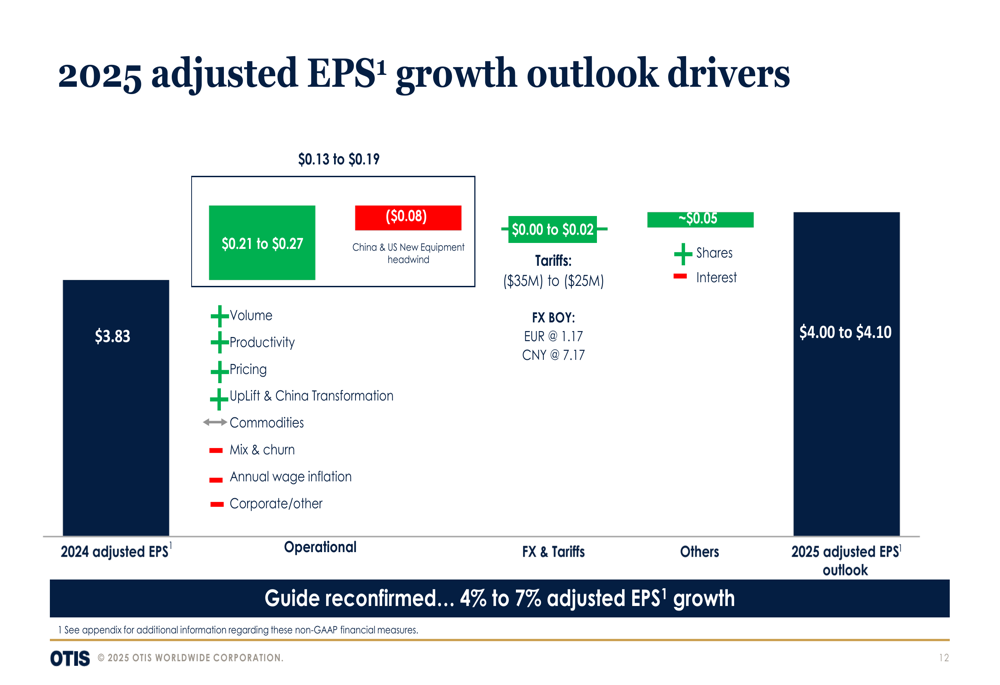

Despite the challenges in the New Equipment segment, Otis maintained its 2025 adjusted EPS guidance of $4.00 to $4.10, representing growth of 4% to 7% compared to 2024. However, the company revised its organic sales growth outlook downward to approximately 1%, compared to the previous guidance of 2% to 4%.

The company’s updated industry outlook anticipates global new equipment unit growth to decline mid-single digits, with particularly weak performance in Asia (down high single digits) and the Americas (down low single digits). Meanwhile, the global installed base is expected to grow at mid-single digits, supporting the service business.

The following slide details Otis’s revised organic sales outlook by region and segment:

The company also provided a breakdown of the drivers behind its 2025 adjusted EPS growth outlook:

Investor Reaction

The market’s negative reaction to Otis’s Q2 results was evident in the premarket trading, with shares falling 10.05% to $90.84. This significant decline suggests investors were disappointed by the weakness in the New Equipment segment, particularly in China, and the downward revision to organic sales growth expectations.

The stock’s movement represents a substantial pullback from its 52-week high of $106.83, though it remains above the 52-week low of $89.70. Prior to this earnings release, Otis shares had been performing relatively well, closing at $100.99 on July 22, up 2.53% for the day.

While Otis continues to emphasize the strength and resilience of its Service business, which generates the vast majority of its operating profit, the market appears concerned about the company’s ability to navigate the challenging global new equipment market, particularly given the significant headwinds in China. The company’s ability to execute on its cost-saving initiatives and successfully mitigate tariff impacts will likely be key factors in determining whether it can deliver on its full-year earnings guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.