IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

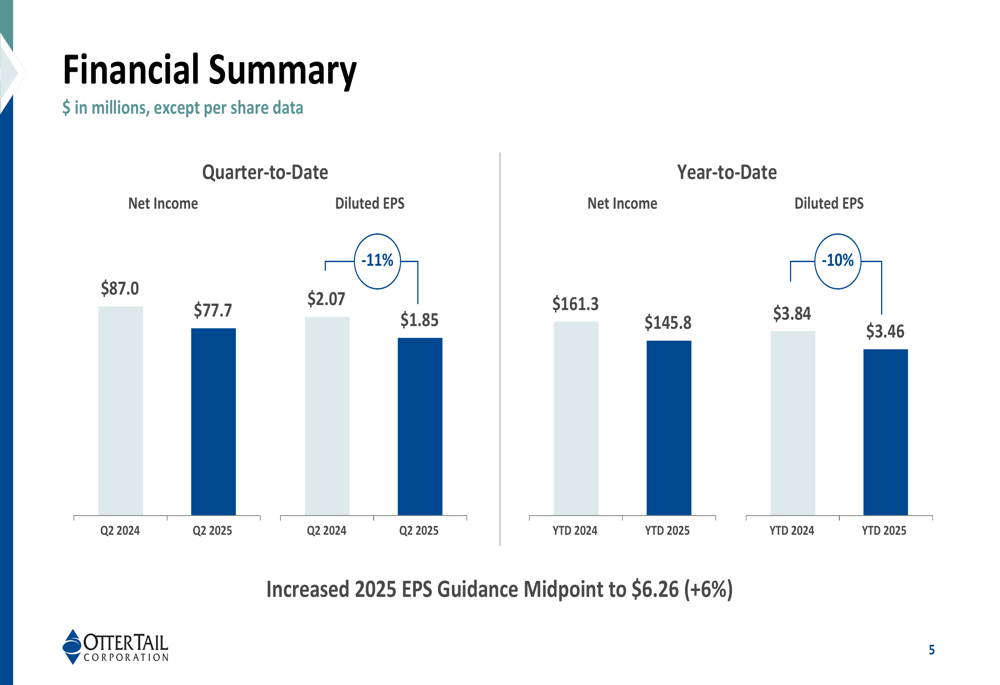

Otter Tail Corporation (NASDAQ:OTTR) released its second quarter 2025 earnings presentation on August 5, showing mixed results across its business segments but raising its full-year guidance. The company reported diluted earnings per share (EPS) of $1.85, down 11% from $2.07 in the same quarter last year, but exceeding analysts’ expectations of $1.72. Following the announcement, Otter Tail’s stock rose 6.14% to close at $76.22.

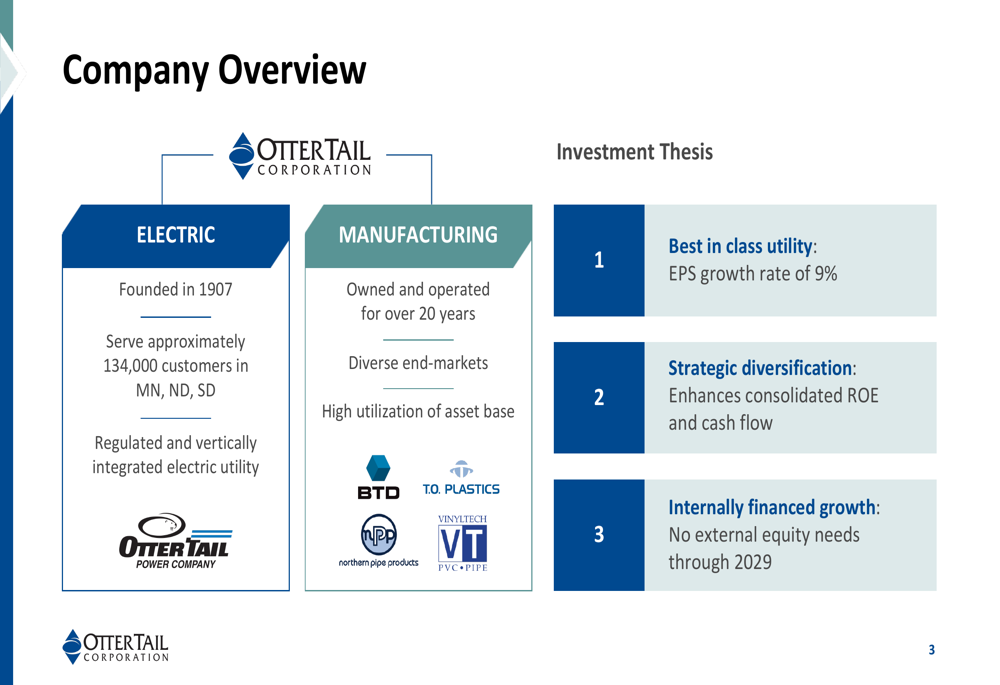

The company operates through two main segments: Electric (a regulated utility serving Minnesota, North Dakota, and South Dakota) and Manufacturing (which includes metal fabrication and plastics businesses). While the Electric segment showed modest growth, the Manufacturing and Plastics segments faced headwinds from pricing pressures and challenging market conditions.

As shown in the following company overview, Otter Tail presents itself as a diversified energy and manufacturing company with a strong investment thesis:

Quarterly Performance Highlights

Otter Tail reported Q2 2025 diluted EPS of $1.85, representing an 11% decrease from the prior year. Despite this decline, the company highlighted several positive developments, including regulatory approvals for solar projects, the filing of a South Dakota rate case, and the ramp-up of its BTD Georgia manufacturing facility.

The following financial summary shows the quarter-to-date and year-to-date performance:

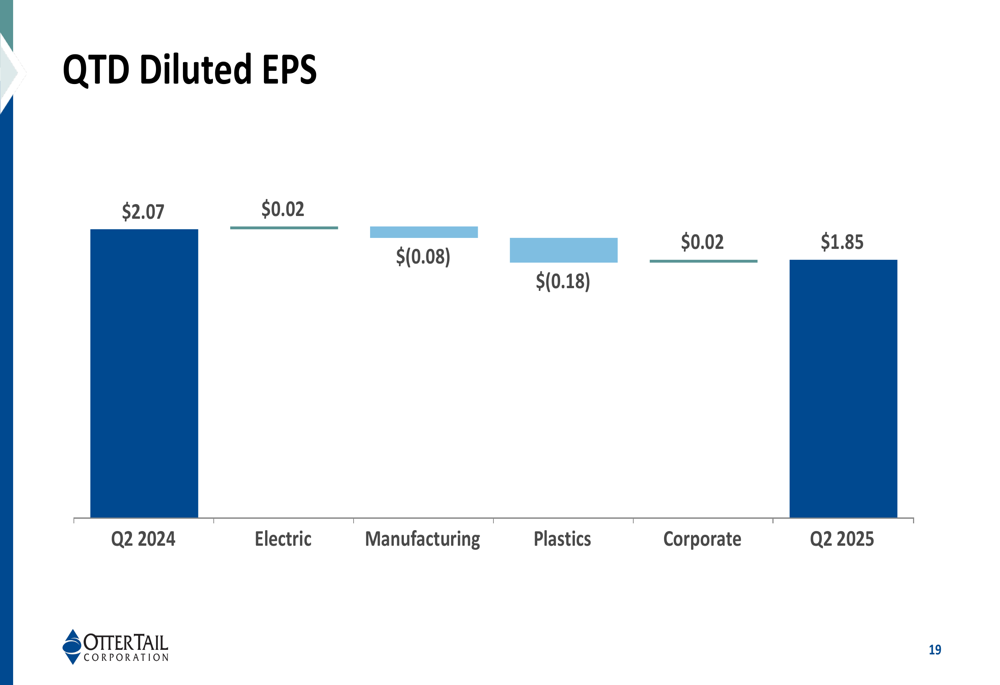

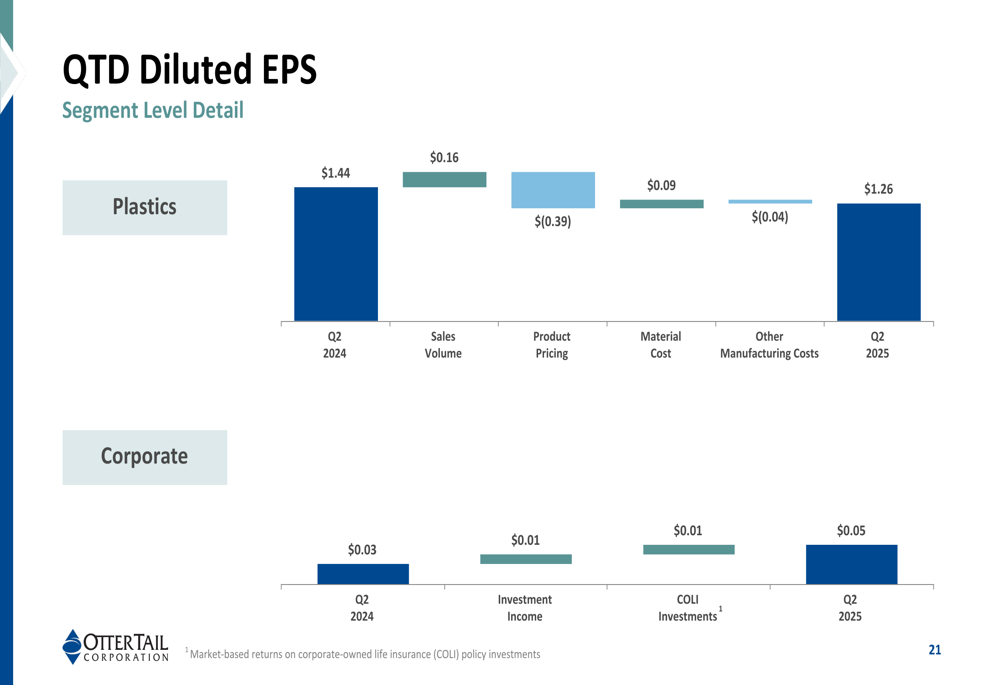

Breaking down the quarterly EPS performance by segment reveals where the changes occurred:

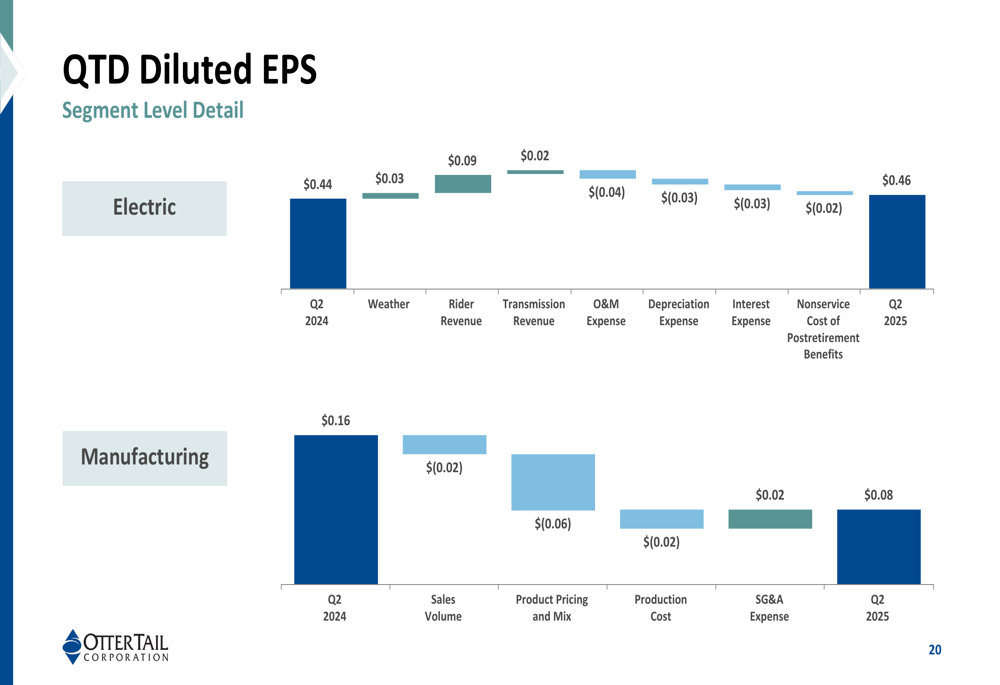

A deeper dive into the Electric segment shows modest growth despite higher expenses:

The Plastics segment, which historically has been a significant contributor to earnings, faced substantial pricing pressures that offset volume gains:

Segment Analysis

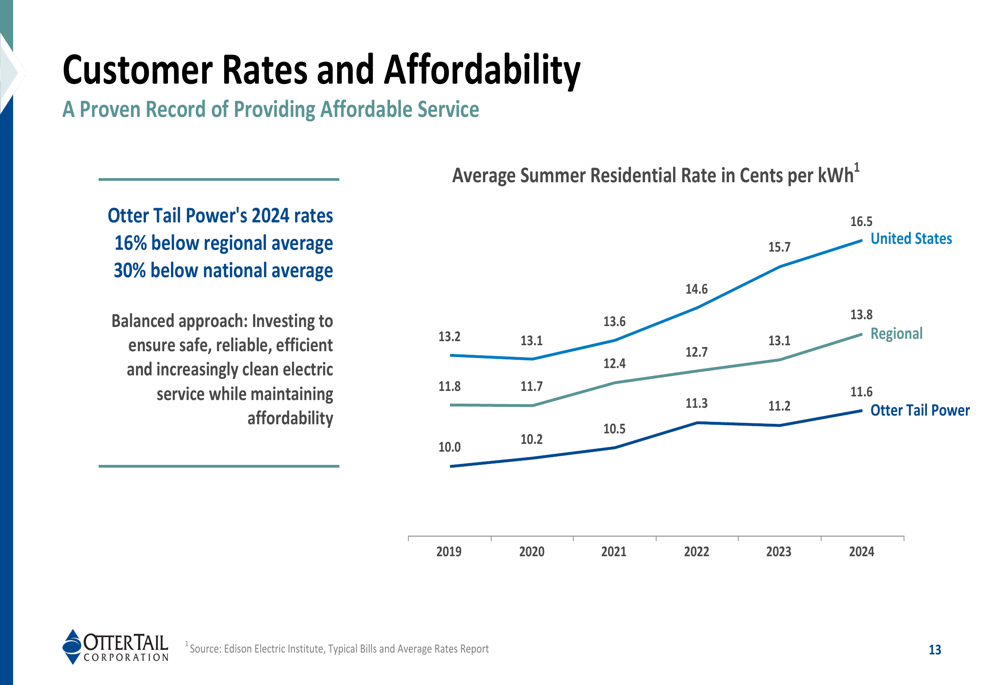

Otter Tail’s Electric segment continues to be a stable performer with a focus on renewable energy investments. The company highlighted its position as a low-cost provider, with 2024 rates 16% below the regional average and 30% below the national average. This competitive advantage positions the utility well for attracting large load customers such as data centers and cryptocurrency operations.

The following chart illustrates Otter Tail’s rate advantage compared to regional and national averages:

In the Manufacturing segment, Otter Tail reported mixed conditions across its end markets. The recreational vehicle market remains weak, while industrial and horticulture markets show strength. The company’s plastics business faced significant headwinds from declining PVC pipe prices, which fell 15% year-over-year in Q2. However, sales volumes increased by 11%, partially offsetting the price decline.

Strategic Initiatives & Capital Plan

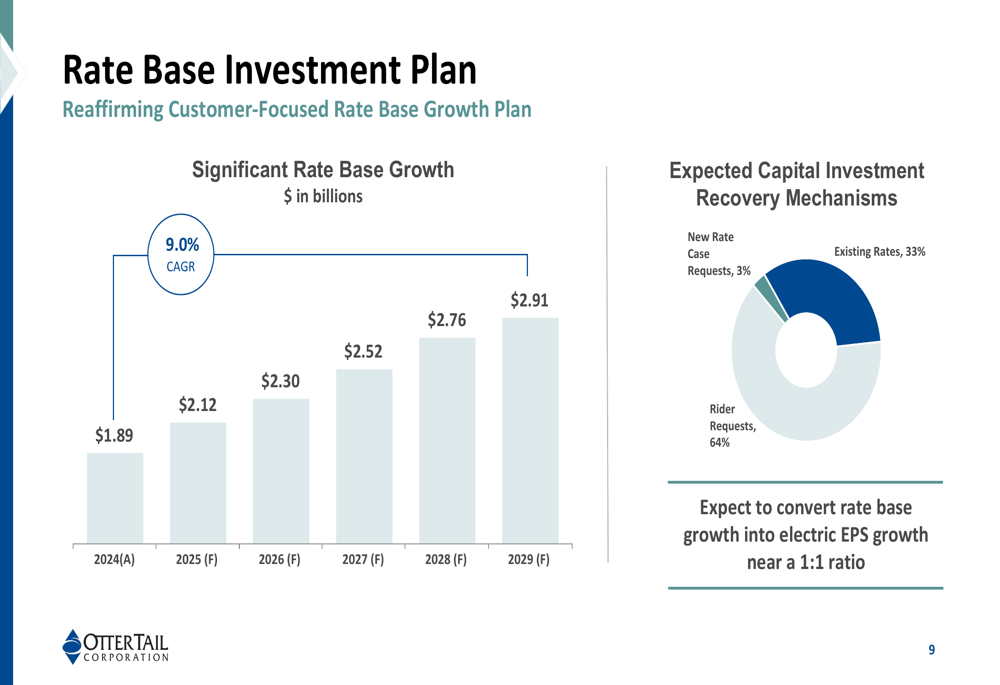

Otter Tail outlined an ambitious capital expenditure plan totaling $1.55 billion over the next five years, with the majority allocated to the Electric segment. The company expects its rate base to grow at a compound annual growth rate (CAGR) of 9.0% through 2029, as shown in the following chart:

Key projects include significant investments in renewable generation and transmission infrastructure. The company received regulatory approval for the Abercrombie Solar and Solway Solar projects, which collectively represent 345 MW of capacity. Additionally, Otter Tail is pursuing several major transmission projects through the MISO regional transmission organization.

In the Manufacturing segment, expansion projects at Vinyltech Corporation and BTD Georgia are progressing. The Vinyltech expansion will increase the Plastics segment’s production capacity by 15% through a multi-phase project, while the BTD Georgia facility is ramping up to full production capability with the potential to generate up to $35 million in incremental annual revenue.

Financial Outlook & Guidance

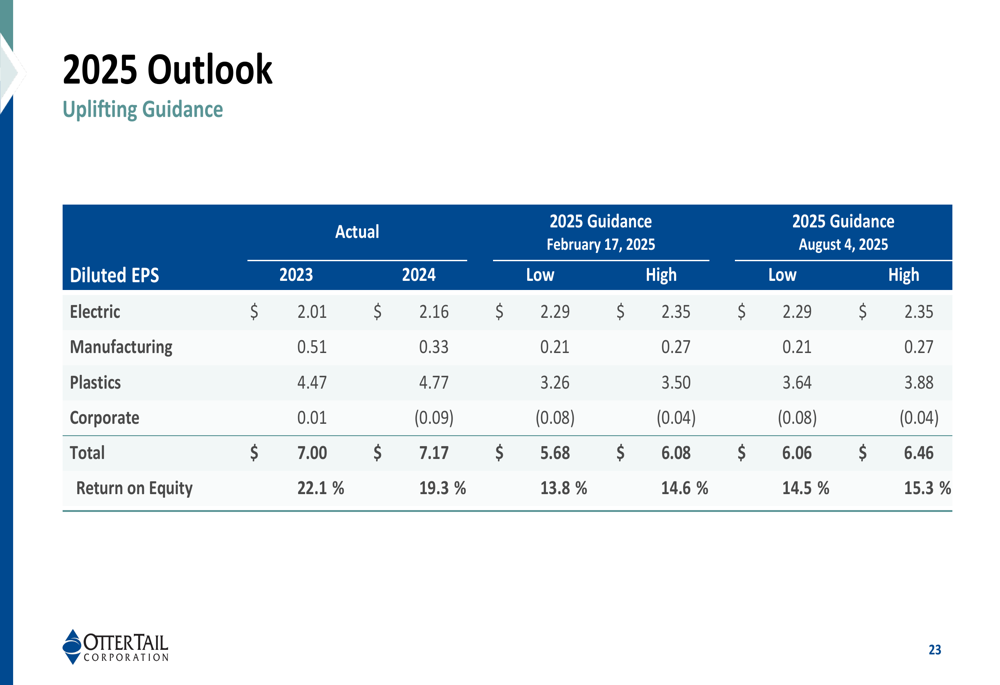

Despite the year-over-year decline in quarterly earnings, Otter Tail raised its full-year 2025 guidance, increasing the EPS range to $6.06-$6.46 from the previous $5.68-$6.08. This improved outlook primarily reflects better-than-expected performance in the Plastics segment.

The detailed 2025 outlook by segment shows:

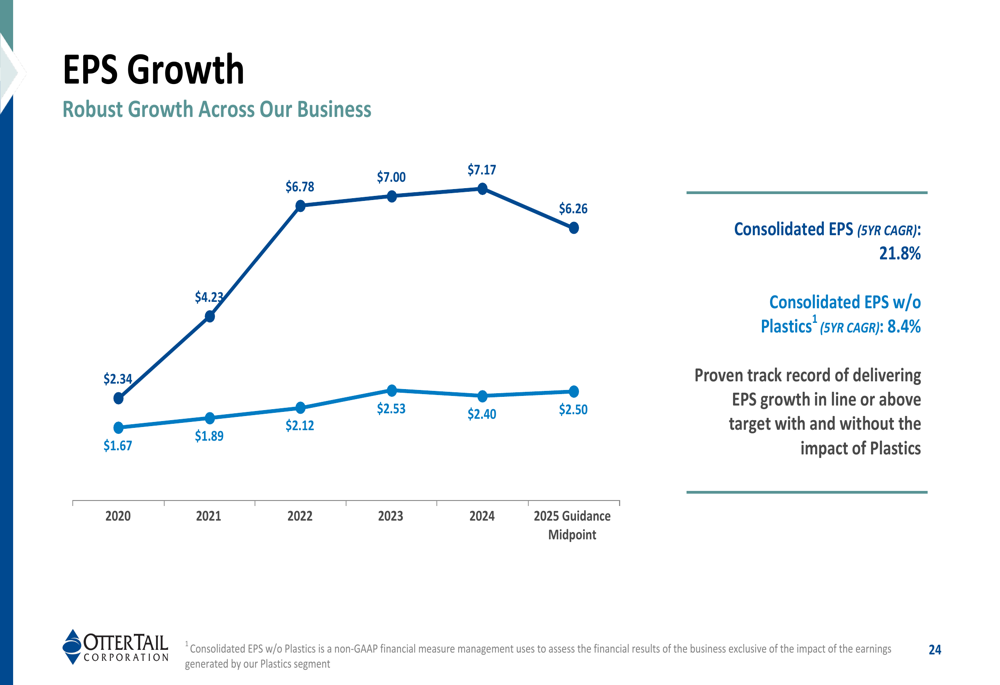

Otter Tail’s long-term EPS growth shows impressive results, particularly when including the contribution from the Plastics segment:

The company maintains a strong balance sheet with $307.2 million in cash and cash equivalents as of June 30, 2025. Otter Tail emphasized that its growth plans through 2029 can be internally financed without the need for equity issuance, which should be positive for existing shareholders.

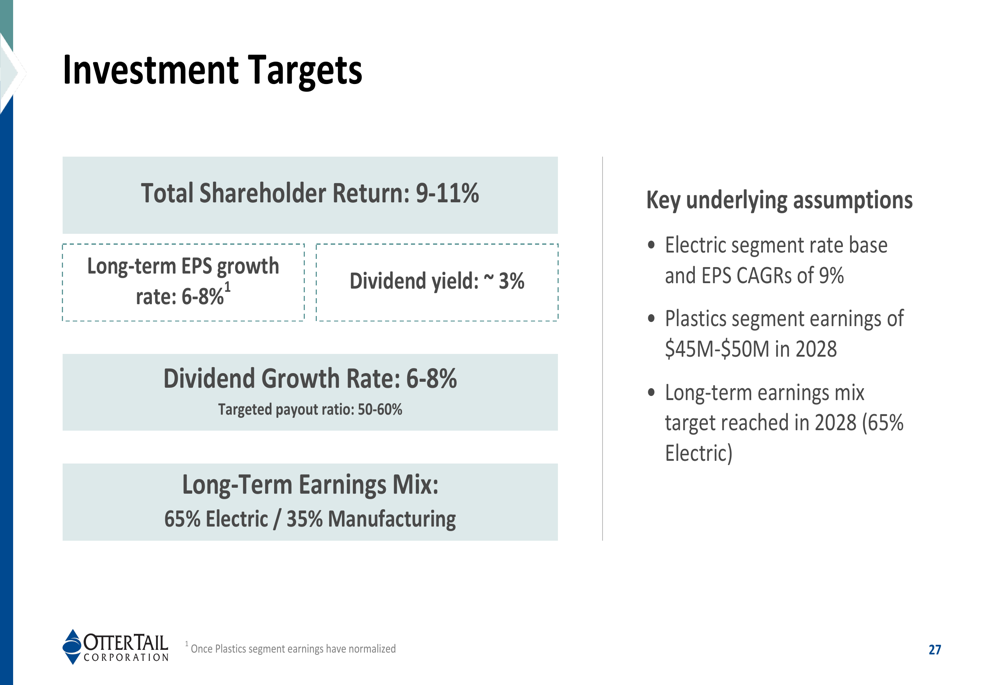

Looking further ahead, Otter Tail outlined its investment targets, including a total shareholder return of 9-11%, long-term EPS growth of 6-8%, and dividend growth of 6-8%. The company is targeting a long-term earnings mix of 65% from the Electric segment and 35% from Manufacturing by 2028.

According to CEO Chuck McFarlane, "We are pleased with our Q2 financial results as they outpaced our expectations." CFO Todd Walland added that the company’s "solid balance sheet helps to ensure we are well positioned to deliver on our customer-focused growth strategy."

With its combination of stable utility operations and manufacturing businesses, Otter Tail continues to navigate market challenges while positioning itself for long-term growth through strategic investments in renewable energy and manufacturing capacity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.