FOMC minutes; Delta, PepsiCo to report; gold retreats - what’s moving markets

Italian fashion retailer OVS SPA (BIT:OVS) reported strong financial results for the first half of 2025, with significant growth in profitability and continued sales momentum. The company announced its results on September 17, 2025, highlighting a 31.7% increase in net income and solid performance across key metrics.

Quarterly Performance Highlights

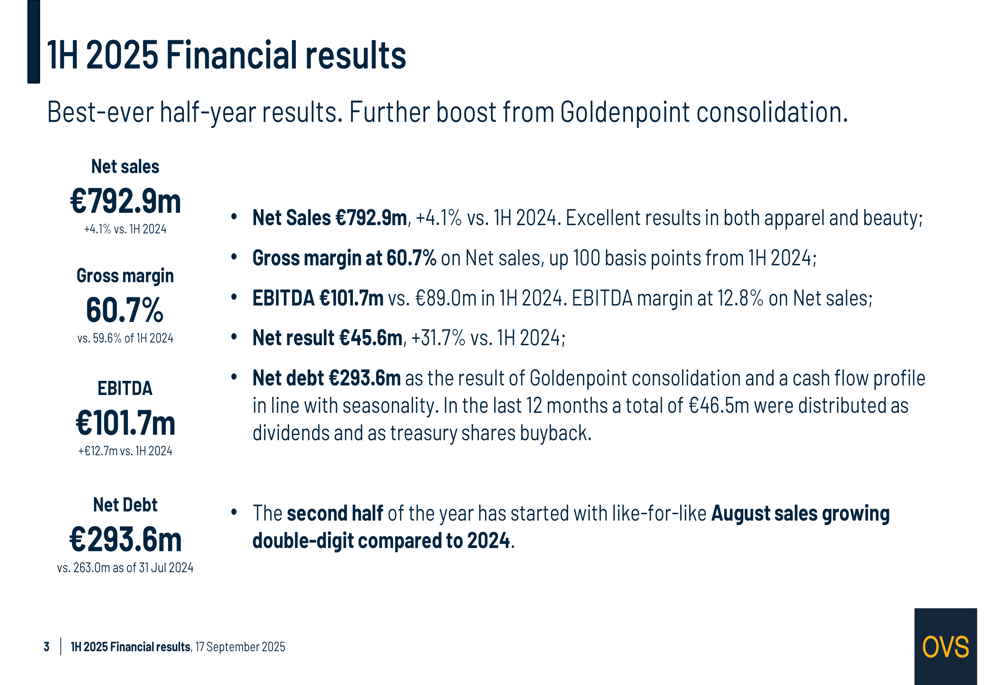

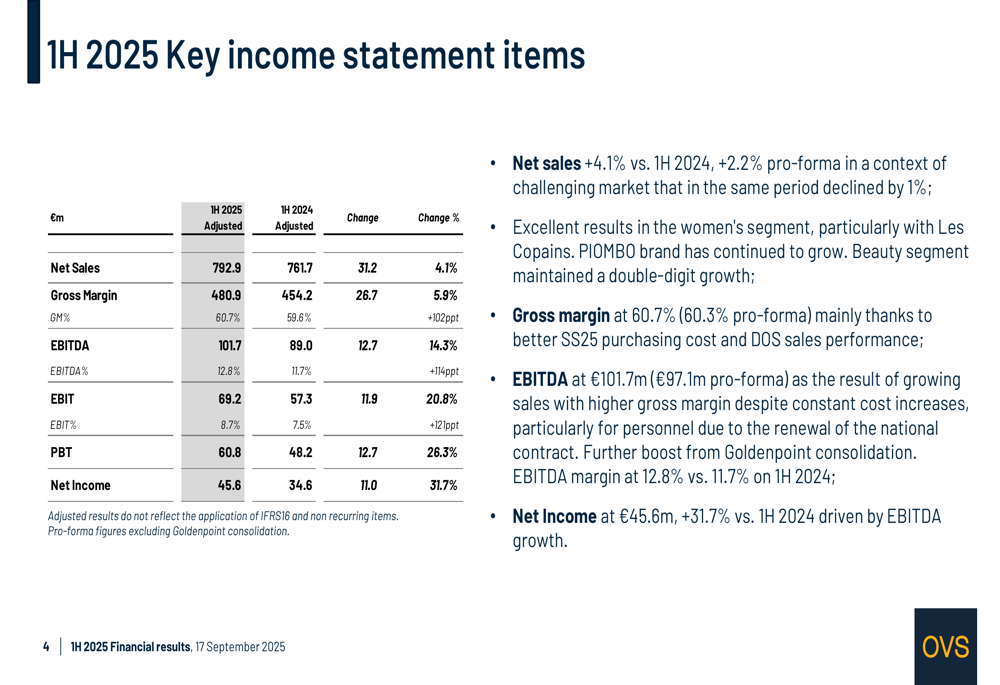

OVS delivered robust financial performance in the first half of 2025, with net sales reaching €792.9 million, representing a 4.1% increase compared to the same period last year. The company’s gross margin expanded by 100 basis points to 60.7%, while EBITDA grew by 14.3% to €101.7 million.

The company’s net income showed the most impressive growth, surging 31.7% to €45.6 million compared to €34.6 million in the first half of 2024. This strong bottom-line performance demonstrates OVS’s ability to effectively manage costs while growing sales.

As shown in the following comprehensive summary of financial results:

The detailed income statement reveals consistent growth across all profitability metrics, with EBIT increasing by 20.8% to €69.2 million and profit before tax growing by 26.3% to €60.8 million. The company noted that excellent results were seen in the women’s segment, while the PIOMBO brand continued to grow and the beauty segment maintained double-digit growth.

Detailed Financial Analysis

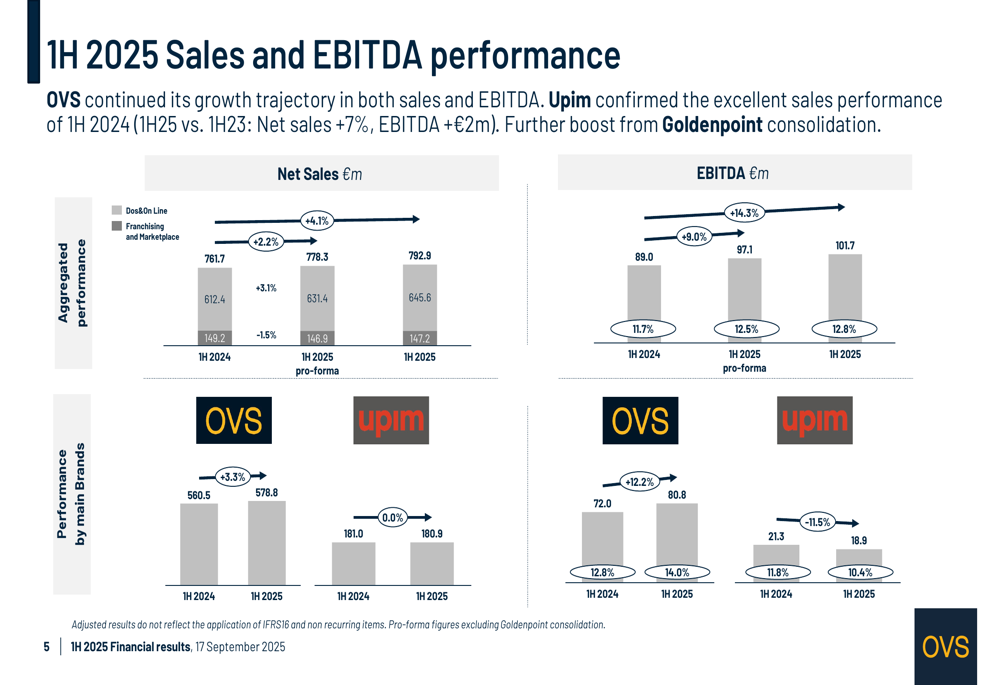

Breaking down performance by brand, OVS’s namesake brand showed solid growth with sales increasing by 3.3% and EBITDA rising by 12.2%. However, the Upim brand displayed mixed results with flat sales (0.0% growth) and an 11.5% decline in EBITDA. The company’s overall results were further boosted by the consolidation of Goldenpoint.

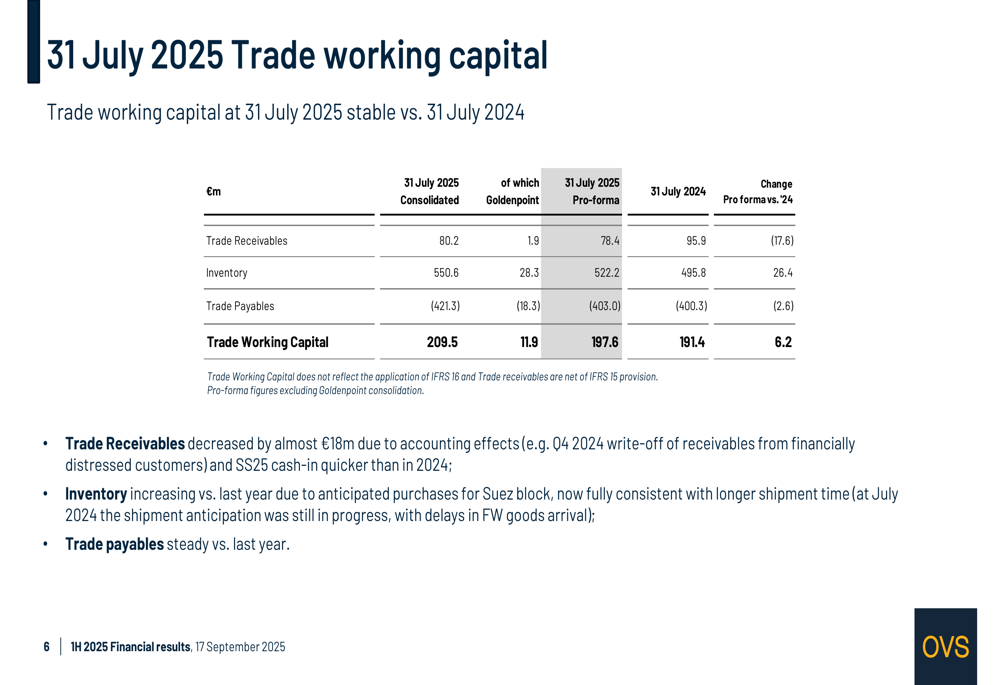

The company’s trade working capital increased to €209.5 million as of July 31, 2025, compared to €191.4 million a year earlier. This change was primarily driven by higher inventory levels (€550.6 million vs. €495.8 million), which the company attributed to anticipated purchases. Trade receivables decreased to €80.2 million from €95.9 million, while trade payables increased slightly to €421.3 million from €400.3 million.

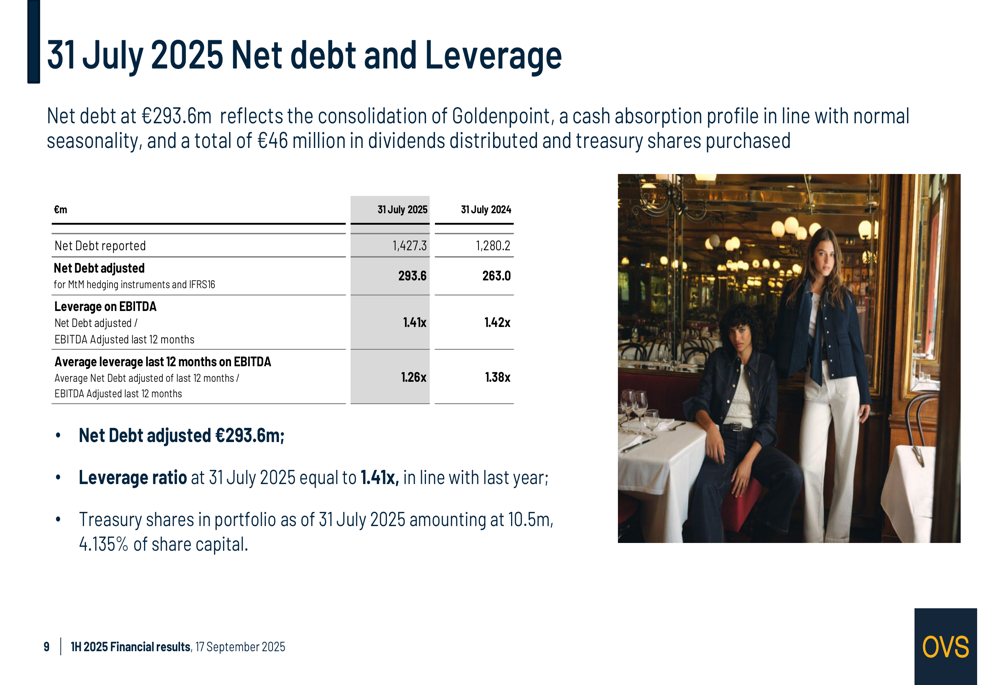

OVS’s net debt stood at €293.6 million as of July 31, 2025, with a leverage ratio of 1.41x, which the company noted was in line with the previous year. The debt position reflects the consolidation of Goldenpoint and approximately €46 million in dividends distributed and treasury shares purchased. As of the reporting date, OVS held 10.5 million treasury shares, representing 4.135% of its share capital.

Strategic Initiatives

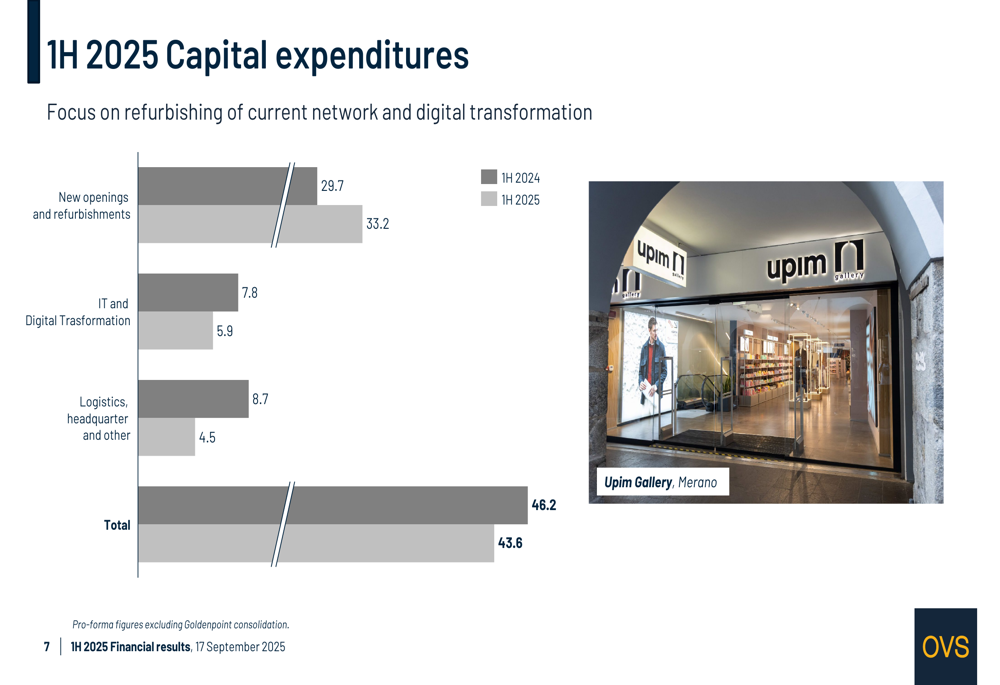

Capital expenditures for the first half of 2025 totaled €43.6 million, slightly down from €46.2 million in the same period last year. The majority of this investment (€33.2 million) was directed toward new openings and refurbishments, with additional spending on IT and digital transformation (€5.9 million) and logistics, headquarters, and other initiatives (€4.5 million).

The company continues to focus on refurbishing its current network and advancing its digital transformation efforts. OVS highlighted the Upim Gallery in Merano as an example of its store improvement initiatives.

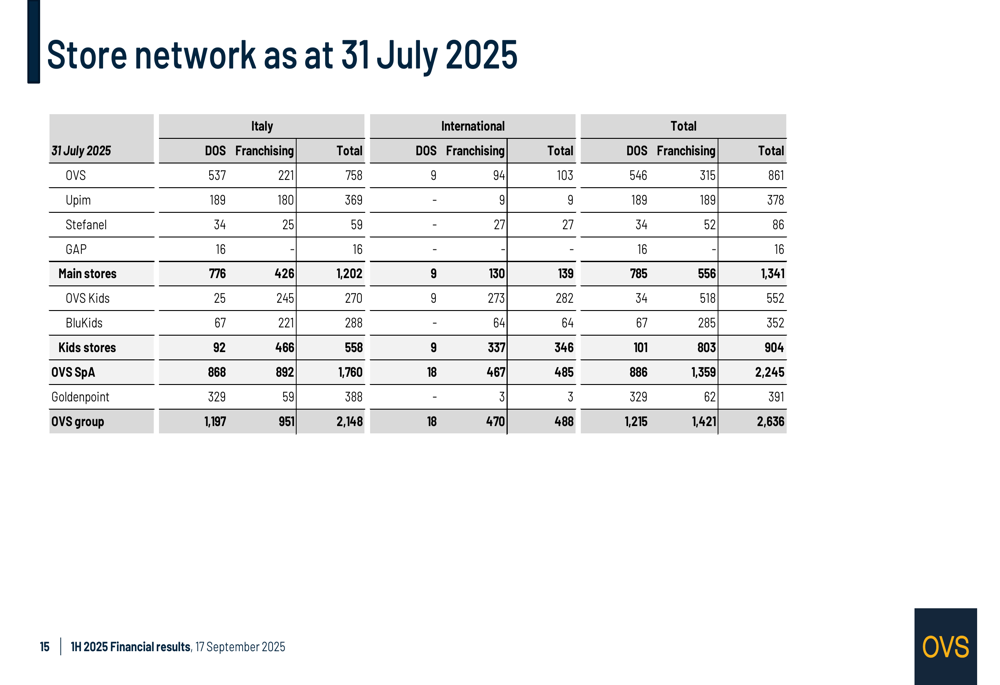

OVS has maintained a robust store network, with a total of 861 OVS stores and 378 Upim stores as of July 31, 2025. In Italy, the company operates 537 directly owned OVS stores and 221 franchised locations, along with 189 directly owned Upim stores and 180 franchised locations. Internationally, OVS has 9 directly owned stores and 94 franchised locations.

Forward-Looking Statements

OVS reported a strong start to the second half of the year, with August sales recording a double-digit increase compared to 2024. The company also noted that September is achieving good results in comparison with previous years, reinforcing management’s confidence in meeting full-year growth expectations.

The company highlighted the success of three city-center Upim stores with a new format in Lecce, Merano, and Biella, which are registering very high absolute values and exceeding management’s best expectations.

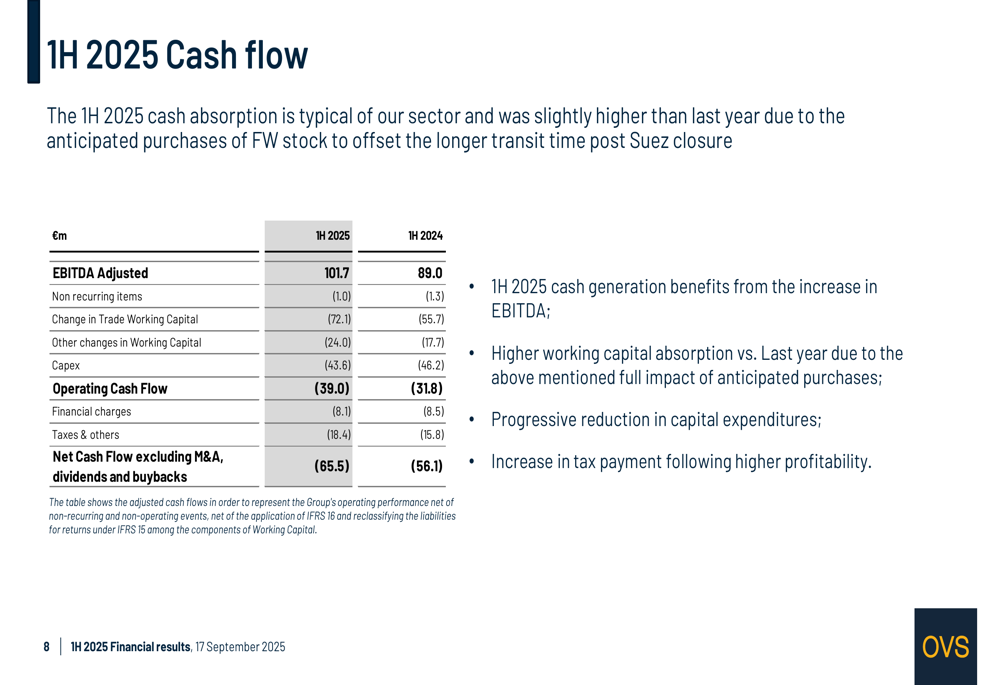

Cash flow for the first half of 2025 showed typical seasonal absorption, slightly higher than the previous year due to anticipated purchases of fall/winter stock to offset longer transit times following the Suez Canal closure. The company emphasized that its cash generation benefited from the increase in EBITDA and noted a progressive reduction in capital expenditures.

OVS’s performance in the first half of 2025 represents a significant improvement from the first quarter, when the company reported slightly weaker-than-expected sales and a slight decline in EBITDA. The strong results for the half-year period, coupled with positive momentum in August and September, suggest that OVS has successfully navigated the challenges faced earlier in the year and is well-positioned for continued growth in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.