US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Oxford Square Capital Corp. (NASDAQ:OXSQ) released its first quarter 2025 financial results presentation on April 25, showing a continued decline in net asset value (NAV) despite maintaining stable investment income. The business development company, which focuses on debt and equity investments primarily in leveraged loans and CLO securities, faces ongoing challenges in balancing yield generation with portfolio quality.

The company’s stock was trading at $2.44 at the previous close, with premarket activity showing a slight increase of 0.37% to $2.45. Oxford Square continues to trade well below its 52-week high of $3.29 while maintaining its consistent quarterly distribution of $0.105 per share.

Quarterly Performance Highlights

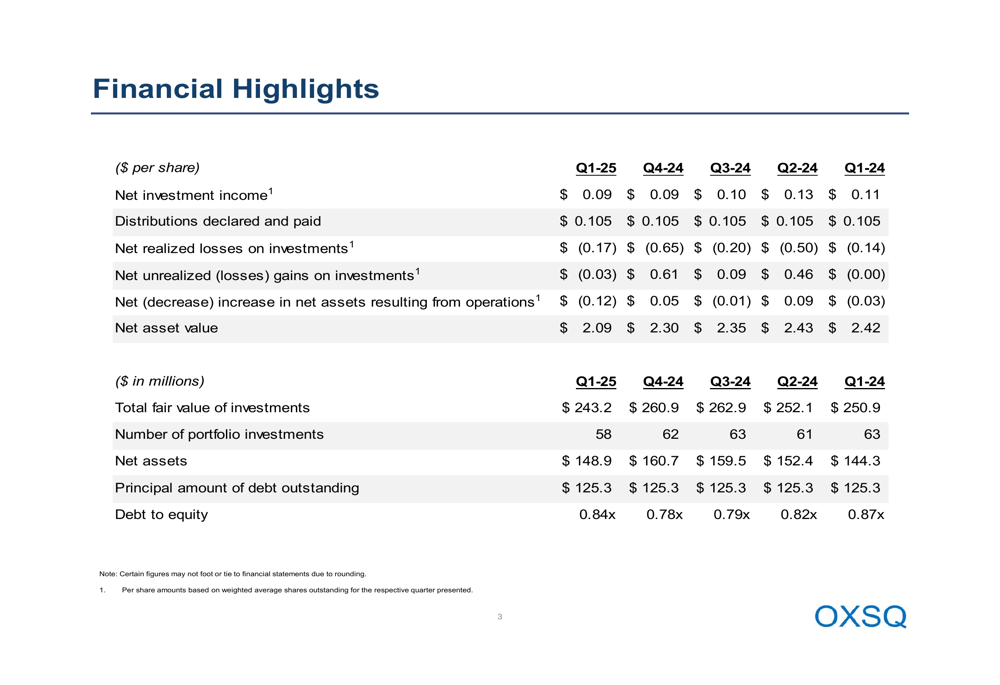

Oxford Square reported net investment income of $0.09 per share for Q1 2025, unchanged from the previous quarter but down from $0.11 per share in the same quarter last year. The company maintained its quarterly distribution of $0.105 per share, continuing its track record of consistent dividend payments.

However, net asset value per share declined to $2.09 as of March 31, 2025, a significant drop from $2.30 at the end of 2024 and $2.42 a year ago. This 9.1% quarter-over-quarter NAV decline was primarily driven by net realized losses of $0.17 per share and net unrealized losses of $0.03 per share.

As shown in the following financial highlights table, the company has experienced a consistent downward trend in NAV over the past five quarters:

Total (EPA:TTEF) investments at fair value decreased to $243.2 million at the end of Q1 2025, down from $260.9 million in the previous quarter. The number of portfolio investments also decreased to 58 from 62 in the previous quarter.

Portfolio Composition and Strategy

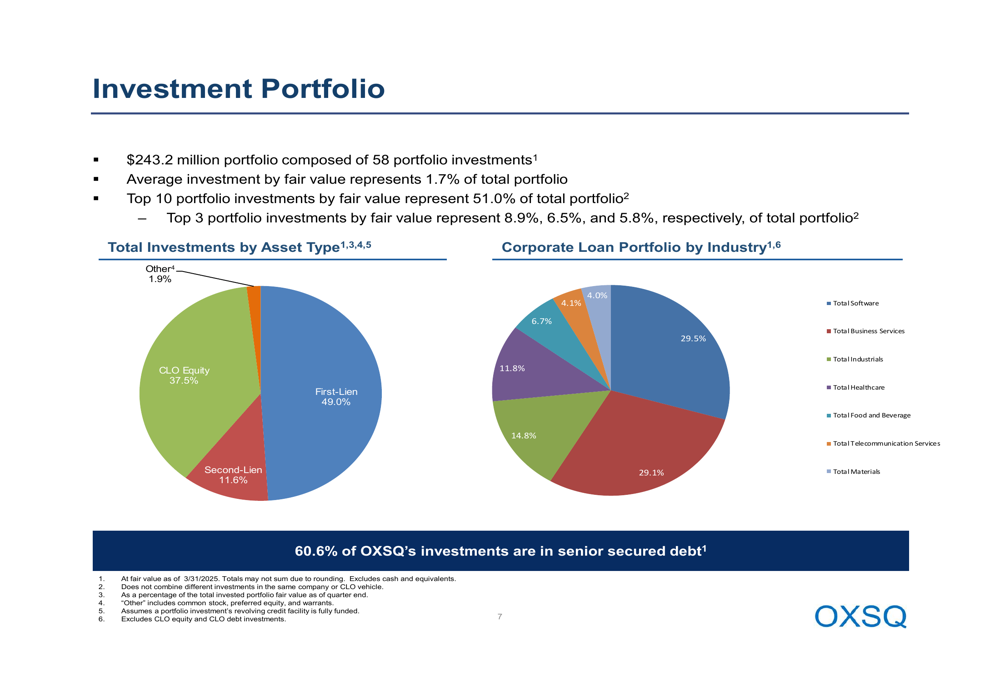

Oxford Square continues to shift its portfolio composition toward first-lien secured debt, which now represents 49% of total investments, up from 47% in the previous quarter and a significant increase from 35% a year ago. This strategic shift comes at the expense of second-lien secured debt, which declined to 12% of the portfolio from 29% a year ago.

The company’s CLO equity investments remained relatively stable at 38% of the portfolio compared to 34% a year ago. This balanced approach reflects management’s strategy to maintain yield while improving the overall risk profile of the portfolio.

The following chart illustrates the company’s current investment portfolio composition:

The corporate loan portfolio shows significant concentration in business services (29.5%), software (29.1%), and healthcare (14.8%), highlighting the company’s focus on these sectors. The top 10 portfolio investments by fair value represent 51.0% of the total portfolio, with the top three investments accounting for 8.9%, 6.5%, and 5.8%, respectively.

Investment Activity and Yields

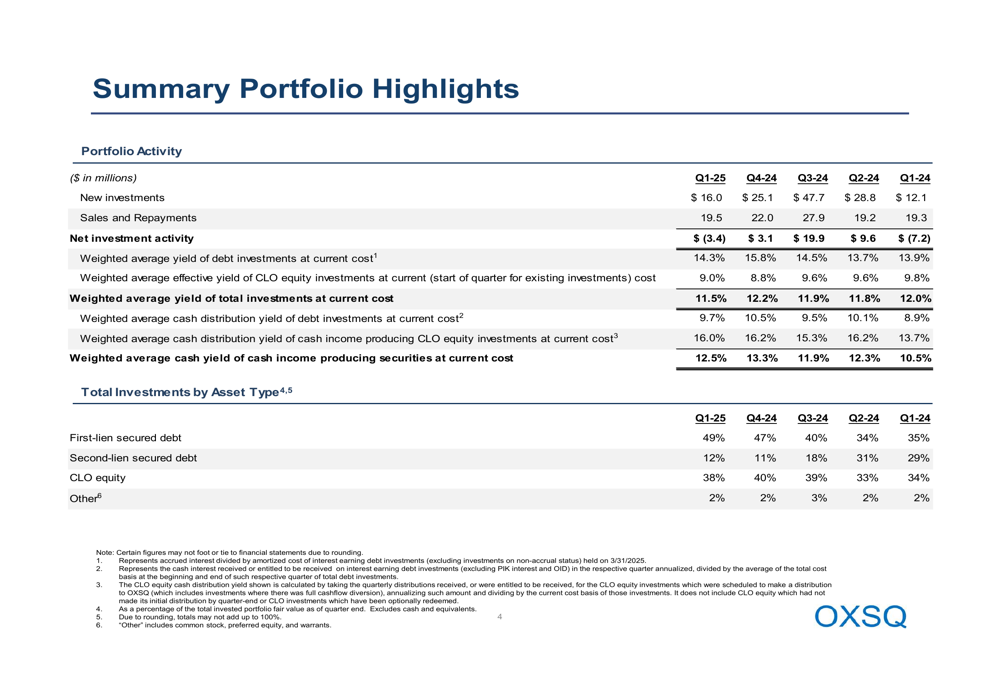

Oxford Square reported $16.0 million in new investments during Q1 2025, a decrease from $25.1 million in the previous quarter. Sales and repayments totaled $19.5 million, resulting in negative net investment activity of $(3.4) million for the quarter, compared to positive net investment activity of $3.1 million in Q4 2024.

The weighted average yield of debt investments at current cost decreased to 14.3% in Q1 2025 from 15.8% in the previous quarter. Similarly, the weighted average yield of total investments declined to 11.5% from 12.2% in Q4 2024.

The following table details the company’s investment activity and yield trends over the past five quarters:

The weighted average cash distribution yield of cash income-producing securities was 12.5% in Q1 2025, down from 13.3% in Q4 2024 but up from 10.5% a year ago, indicating some volatility in the income-generating capacity of the portfolio.

Credit Quality and Risk Management

Oxford Square has made significant progress in reducing non-accrual investments. Total non-accrual investments at cost decreased to $16.1 million in Q1 2025, a substantial improvement from $71.2 million a year ago and down from $18.5 million in the previous quarter. At fair value, non-accrual investments stood at $3.9 million, down from $5.1 million in Q4 2024.

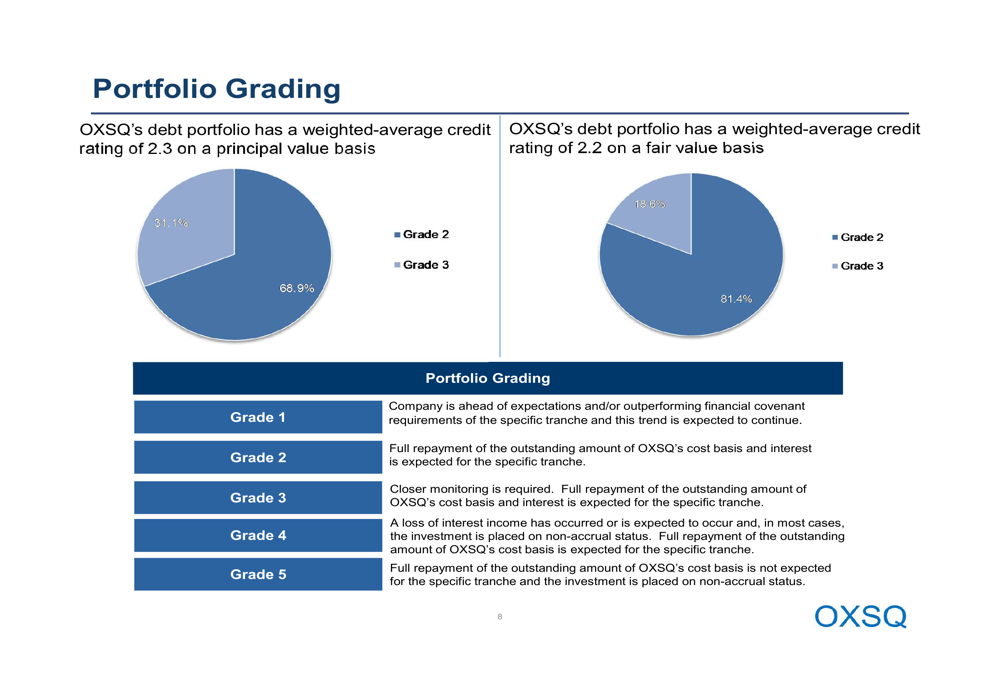

The company’s portfolio grading shows that 81.4% of investments by fair value are rated Grade 3, indicating that "closer monitoring is required" but "full repayment of OXSQ’s cost basis and interest is expected." The remaining 18.6% are rated Grade 2, suggesting these investments are performing according to expectations.

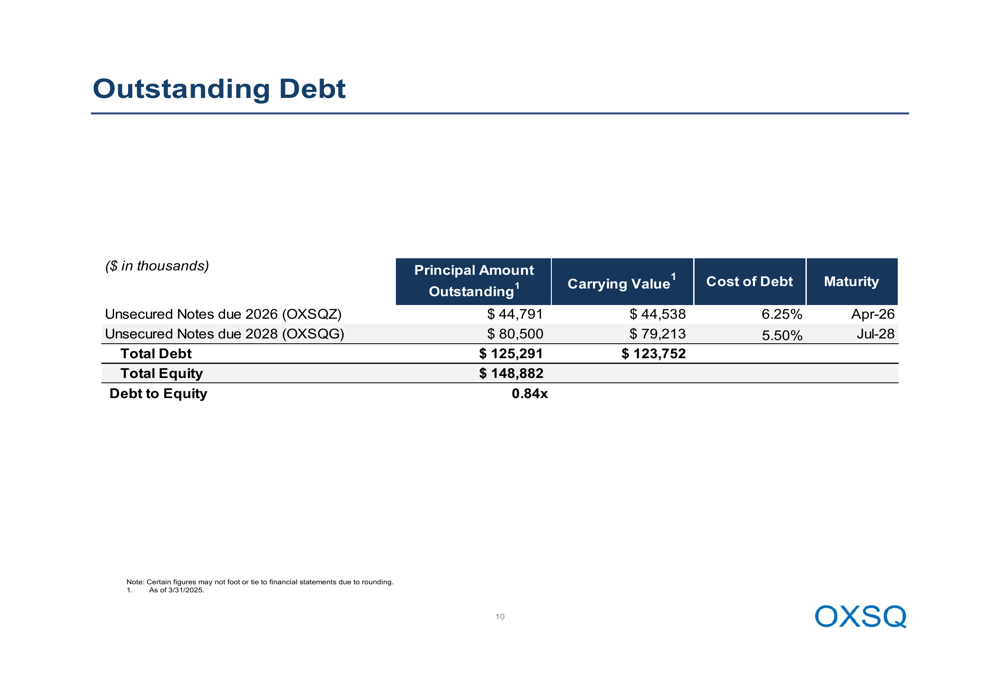

The debt-to-equity ratio increased slightly to 0.84x from 0.78x in the previous quarter, remaining within the company’s historical range. Oxford Square’s outstanding debt consists of $44.8 million in unsecured notes due in April 2026 with a cost of 6.25% and $80.5 million in unsecured notes due in July 2028 with a cost of 5.50%.

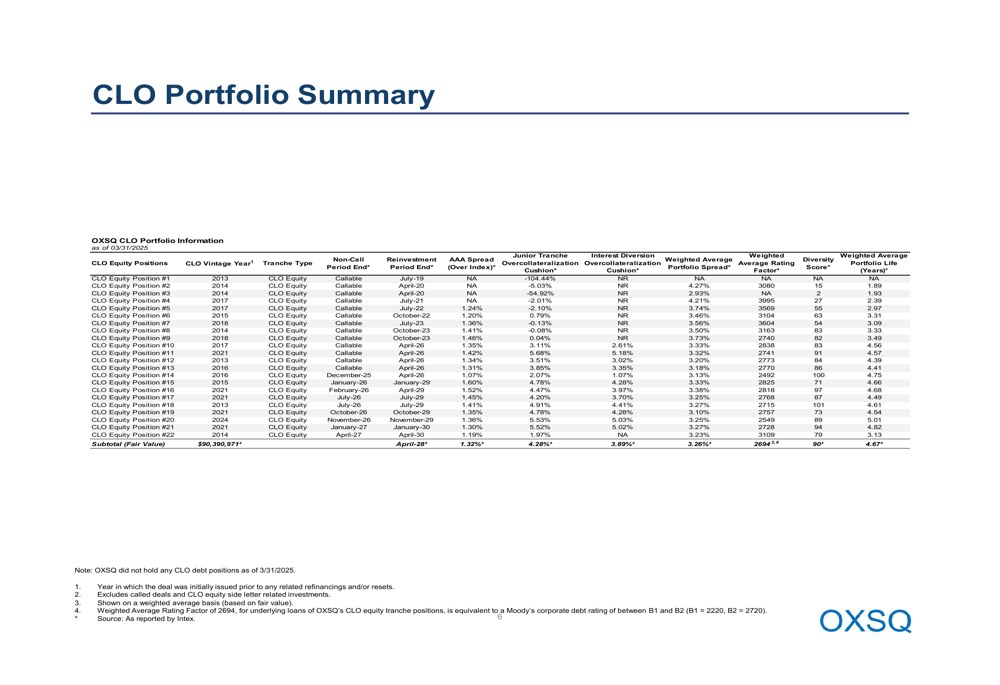

CLO Portfolio Performance

CLO equity investments continue to be a significant component of Oxford Square’s portfolio. The company’s CLO equity investments that have made initial distributions totaled $224.8 million at original cost in Q1 2025, down from $247.0 million in the previous quarter.

The weighted average effective yield of CLO equity investments at current cost was 9.0% in Q1 2025, a slight improvement from 8.8% in Q4 2024 but down from 9.8% a year ago. Cash flow diversion amounts decreased significantly to $0.1 million in Q1 2025 from $1.3 million a year ago, indicating improved performance of underlying CLO structures.

The following table provides a detailed summary of the company’s CLO portfolio:

Forward-Looking Statements

While Oxford Square did not provide specific guidance for future quarters, the company’s strategic shift toward first-lien secured debt and away from second-lien debt suggests a continued focus on risk management in an uncertain economic environment. The reduction in non-accrual investments indicates progress in addressing problem assets, though the declining NAV remains a concern.

The company faces challenges in maintaining its current distribution level of $0.105 per share given that net investment income of $0.09 per share falls short of covering the dividend. This shortfall, combined with continued net realized losses, suggests potential pressure on the sustainability of the current distribution level if performance trends do not improve.

Oxford Square’s ability to navigate the leveraged loan market while managing credit quality will be crucial for stabilizing NAV and improving total returns for shareholders in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.