Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Pagaya Technologies Ltd. (NASDAQ:PGY) reported strong financial results for the first quarter of 2025, achieving GAAP profitability ahead of its previously announced schedule. The fintech company, which uses artificial intelligence to help financial institutions manage risk and optimize returns, saw its stock surge in pre-market trading following the earnings announcement, with shares up 12.79% to $12.96.

The company’s Q1 2025 earnings presentation, released on May 7, 2025, revealed that Pagaya has successfully transitioned to profitability, reporting net income of $8 million compared to a $21 million loss in the same period last year. This achievement comes earlier than expected, as the company had previously guided for GAAP net income positivity by the second quarter of 2025 during its Q4 2024 earnings call.

Quarterly Performance Highlights

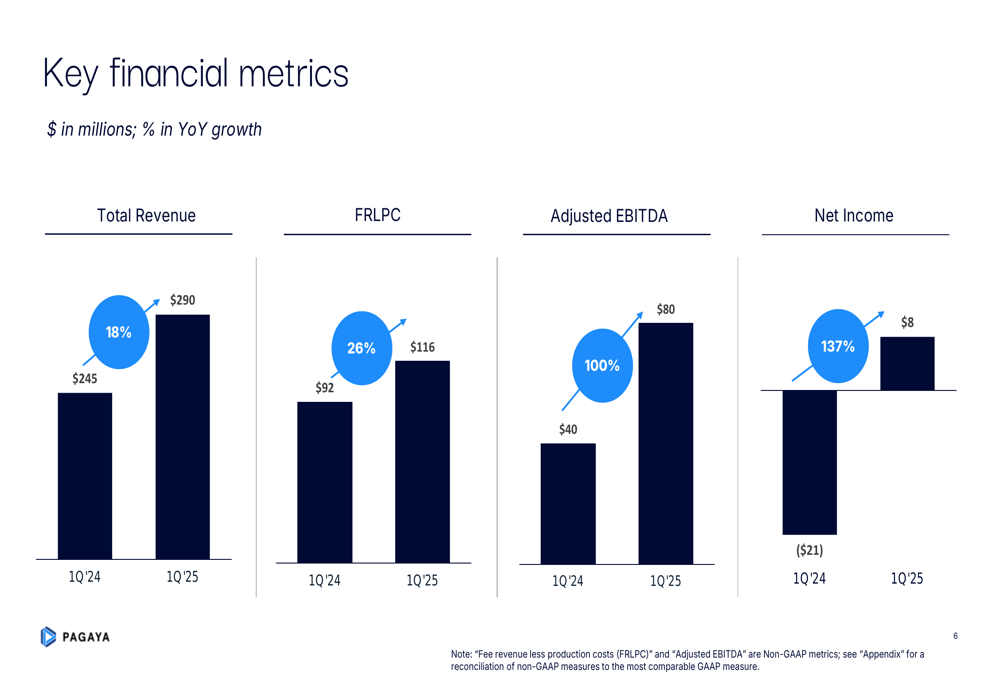

Pagaya reported total revenue of $290 million for Q1 2025, representing an 18% increase from $245 million in Q1 2024. This growth was primarily driven by a 19% year-over-year increase in revenue from fees, which reached $283 million.

As shown in the following chart of key financial metrics, Pagaya demonstrated significant improvement across multiple performance indicators:

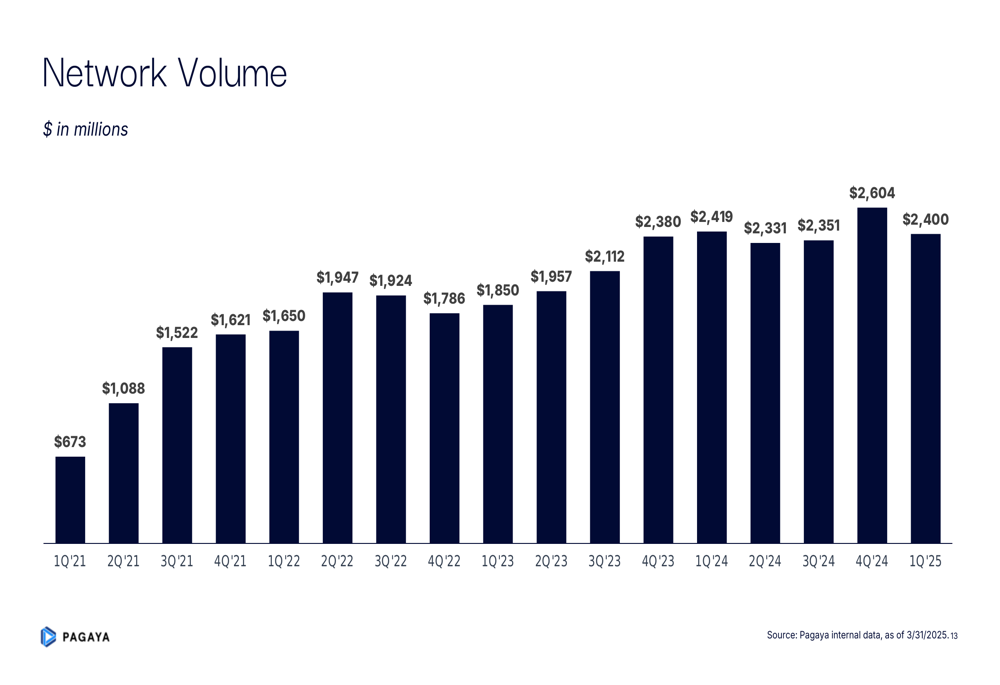

The company’s Fee Revenue Less Production Costs (FRLPC), a key non-GAAP metric that Pagaya uses to measure its core business performance, grew by 26% year-over-year to $116 million. This growth was achieved despite a slight 1% decline in network volume, which totaled $2,400 million for the quarter.

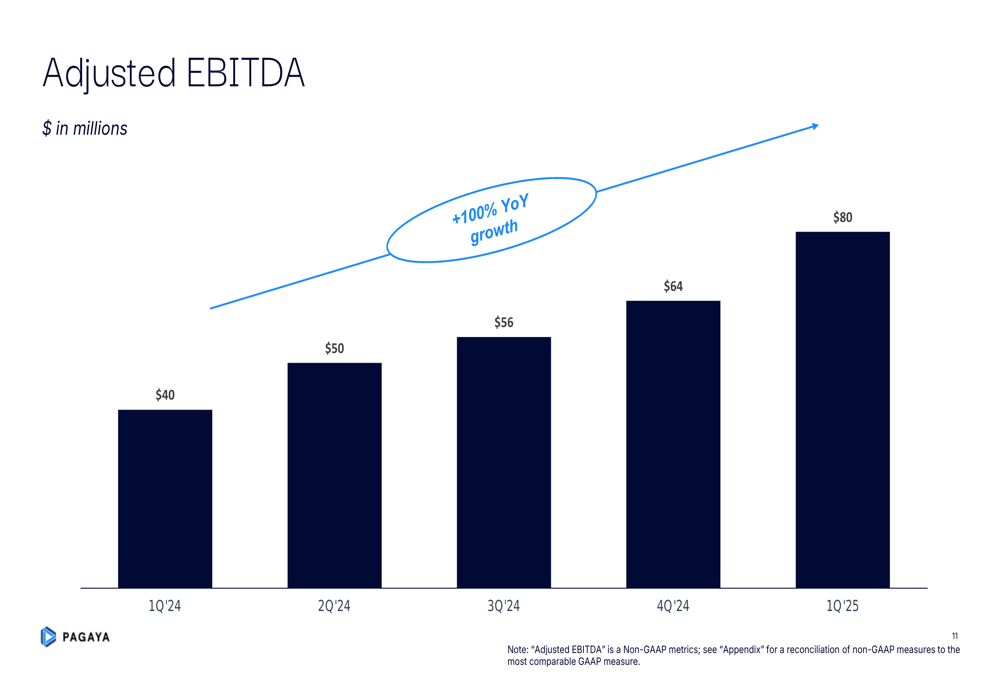

Most notably, Pagaya reported net income of $8 million for Q1 2025, a 137% improvement from the $21 million loss in the same period last year. Adjusted EBITDA doubled to $80 million, while Adjusted Net Income surged 299% to $53 million.

Detailed Financial Analysis

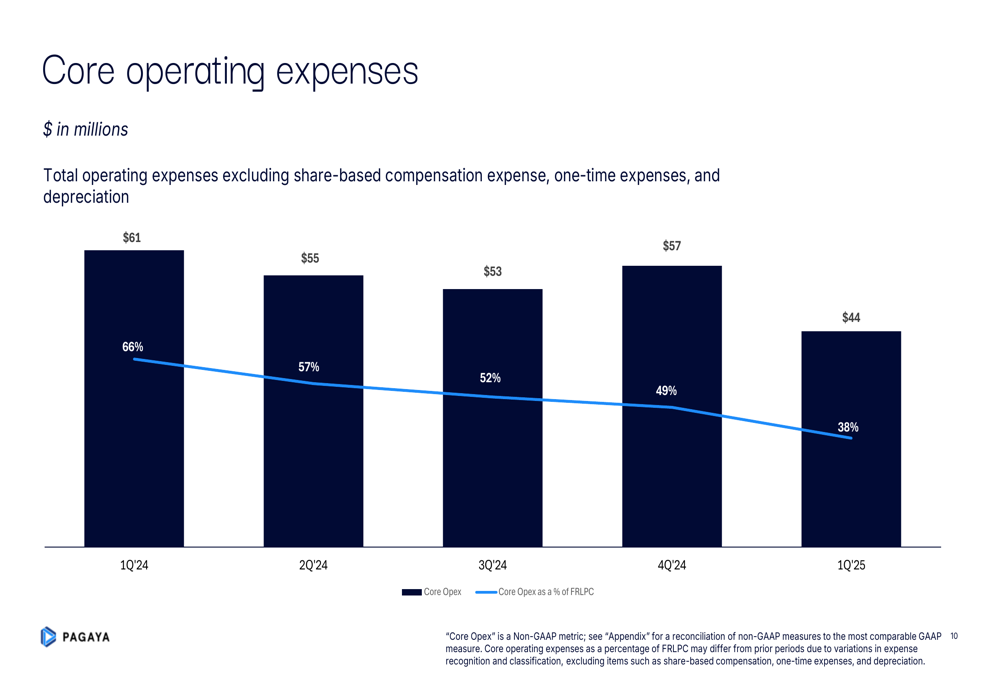

A significant driver of Pagaya’s improved profitability has been its focus on operational efficiency. Core operating expenses decreased by 27% year-over-year to $44 million, while core operating expenses as a percentage of FRLPC improved dramatically from 66% in Q1 2024 to 38% in Q1 2025.

The following chart illustrates this trend of improving operational efficiency:

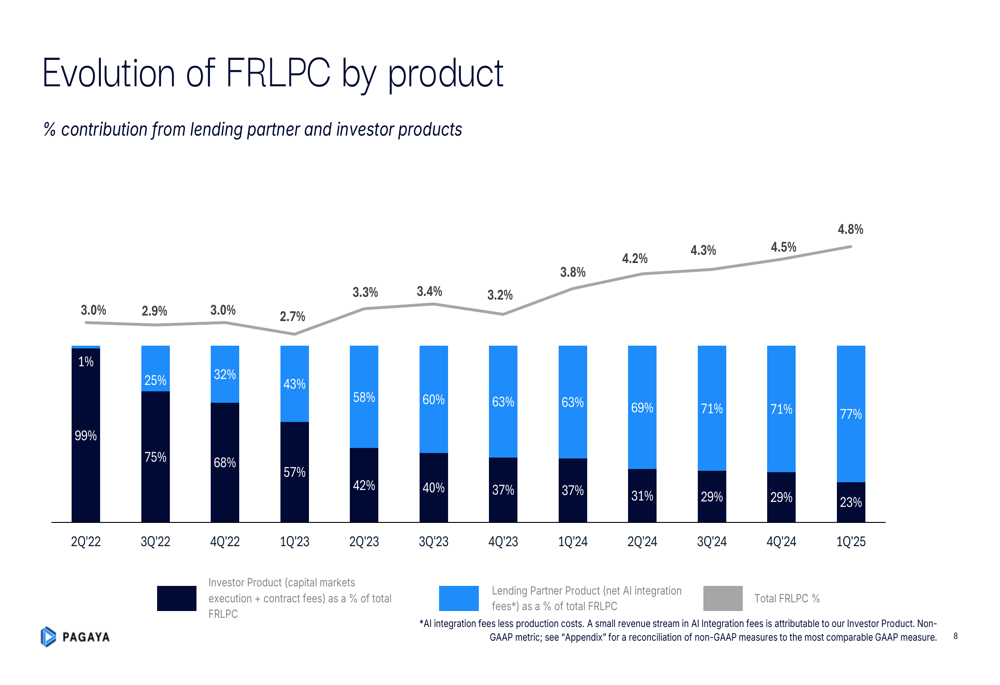

Pagaya’s FRLPC as a percentage of network volume has also shown positive evolution, reaching 4.8% in Q1 2025. The company has set a target range of 4.0%-5.0% for this metric in 2025, indicating that they are already performing at the high end of their expectations.

The composition of FRLPC has been shifting over time, with increasing contributions from investor products. This evolution reflects Pagaya’s strategic pivot toward higher-margin business segments:

The company’s adjusted EBITDA has shown consistent growth over the past five quarters, doubling year-over-year to $80 million in Q1 2025:

Strategic Initiatives

While Pagaya’s network volume showed a slight year-over-year decline in Q1 2025, the company has maintained substantial scale with $2,400 million in volume. The historical trend shows significant growth from 2021 through 2024:

Pagaya continues to expand its market reach, with applications evaluated reaching $224 billion in Q1 2025, though the conversion rate remains at approximately 1%. This indicates the company’s AI-driven platform is processing a large volume of potential transactions while maintaining selective approval criteria.

The company has also been diversifying its ABS (Asset-Backed Securities) funding network, which is crucial for its business model. Pagaya’s investor base includes asset managers, banks, hedge funds, and insurance companies, providing a stable funding source for its lending operations.

Credit performance remains a key focus area for Pagaya, with detailed monitoring of both personal and auto loan portfolios. The company’s presentation included comprehensive data on weighted average coupon rates and delinquency metrics, demonstrating its risk management capabilities.

Forward-Looking Statements

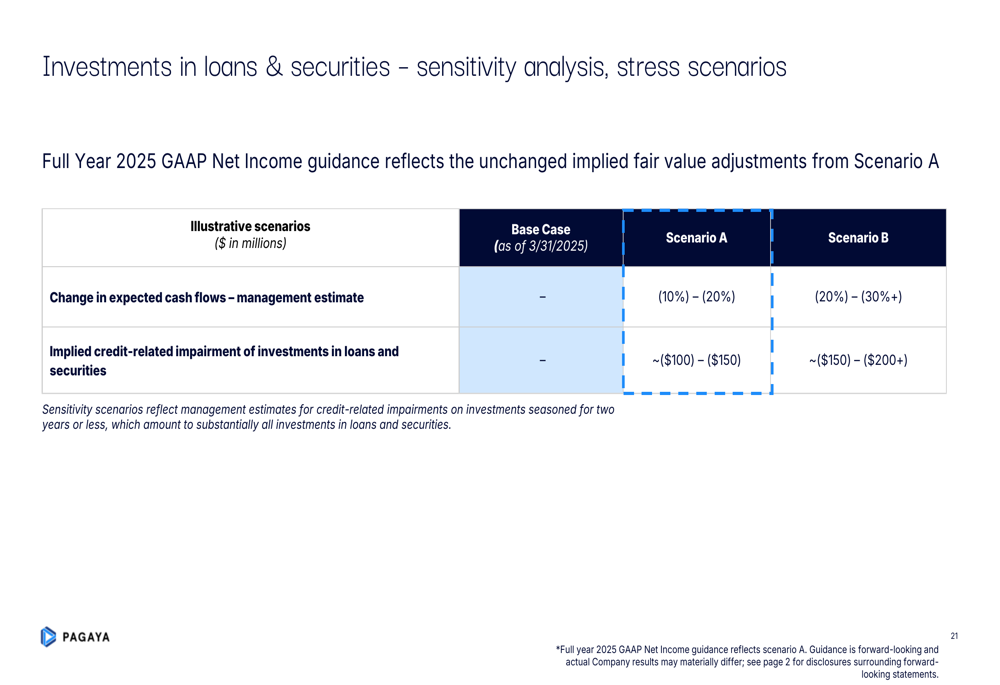

Pagaya’s presentation included a sensitivity analysis for investments in loans and securities, illustrating the company’s approach to risk management under different economic scenarios. This analysis helps investors understand potential impacts on the company’s financial performance under varying market conditions.

The following table presents Pagaya’s sensitivity analysis for investments in loans and securities:

Based on the Q4 2024 earnings call, Pagaya had projected network volume of $10.25 to $11.75 billion for 2025, with total revenue expected between $1.15 and $1.275 billion. The strong Q1 2025 results, with revenue growth of 18% year-over-year, suggest the company is on track to meet or potentially exceed these projections.

The achievement of GAAP profitability in Q1 2025, ahead of the previously guided Q2 2025 timeline, demonstrates Pagaya’s accelerating financial performance and operational efficiency improvements. With continued growth in revenue and significant margin expansion, Pagaya appears well-positioned to deliver on its target of a 20% compound annual growth rate over the cycle.

Analyst Perspectives

According to the previous earnings report context, analysts maintain a strong buy consensus recommendation for Pagaya, with a consensus rating of 1.6 out of 5. The company’s financial health score was rated as "GOOD" by InvestingPro data.

The early achievement of GAAP profitability, combined with strong revenue growth and margin expansion, is likely to reinforce positive analyst sentiment. Pagaya’s ability to grow revenue by 18% while reducing core operating expenses by 27% demonstrates effective execution of its efficiency initiatives.

With the stock trading at $11.49 as of the previous close, and showing significant pre-market gains following the earnings announcement, investors appear to be responding positively to Pagaya’s continued financial improvement and earlier-than-expected profitability milestone.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.