Sprouts Farmers Market closes $600 million revolving credit facility

Introduction & Market Context

PagerDuty (NYSE:PD) released its Q1 FY26 investor presentation on May 29, 2025, highlighting the company’s continued focus on operational efficiency and profitability while maintaining steady revenue growth. The digital operations management platform provider reported results for the quarter ended April 30, 2025, showing improved margins despite some signs of slowing customer retention.

The company’s stock has experienced significant volatility over the past year, trading near its 52-week low of $14.30 with a current price of $16.00. Following the recent Q4 FY25 earnings announcement, PagerDuty’s stock had risen 5.77% in after-hours trading, reflecting investor confidence in the company’s financial performance and strategic initiatives.

Quarterly Performance Highlights

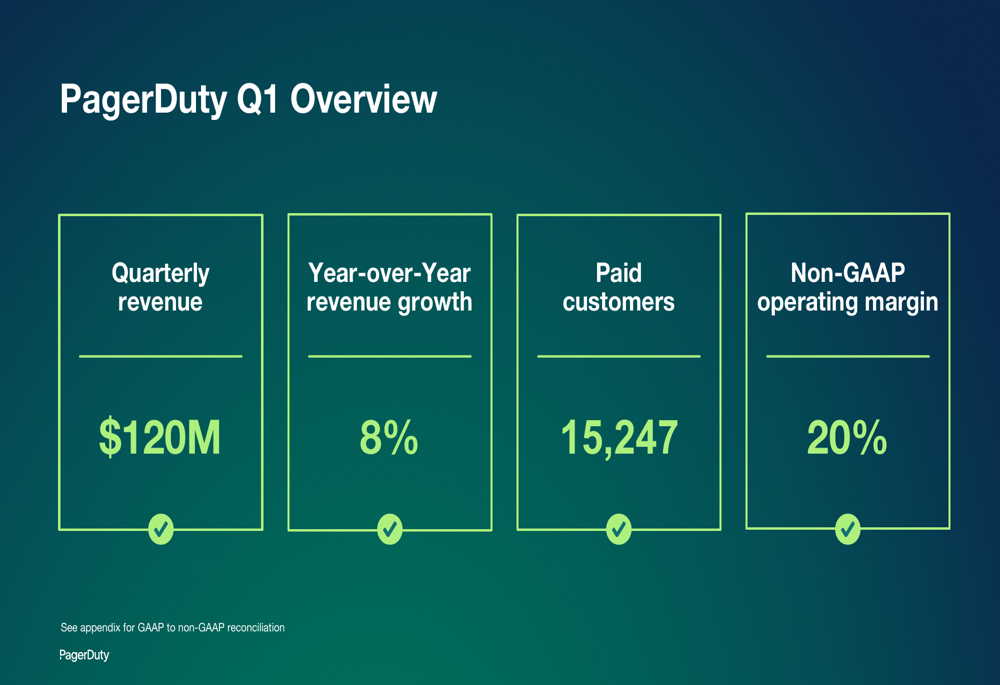

PagerDuty reported Q1 FY26 revenue of $120 million, representing an 8% year-over-year growth, slightly below the $121.4 million reported in the previous quarter. The company’s annual recurring revenue (ARR) reached $496 million, continuing its upward trajectory.

As shown in the following overview of key Q1 metrics:

The company achieved a non-GAAP operating margin of 20%, showing improvement from 18% in the previous quarter and 14% in the same quarter last year. Free cash flow margin expanded significantly to 24%, demonstrating the company’s increasing operational efficiency.

However, PagerDuty’s dollar-based net retention rate (DBNR) declined slightly to 104%, down from 106% in the previous quarter, potentially signaling some challenges in customer expansion. The company reported 15,247 paid customers, with 848 customers generating over $100,000 in ARR, a slight decrease from 849 in the previous quarter.

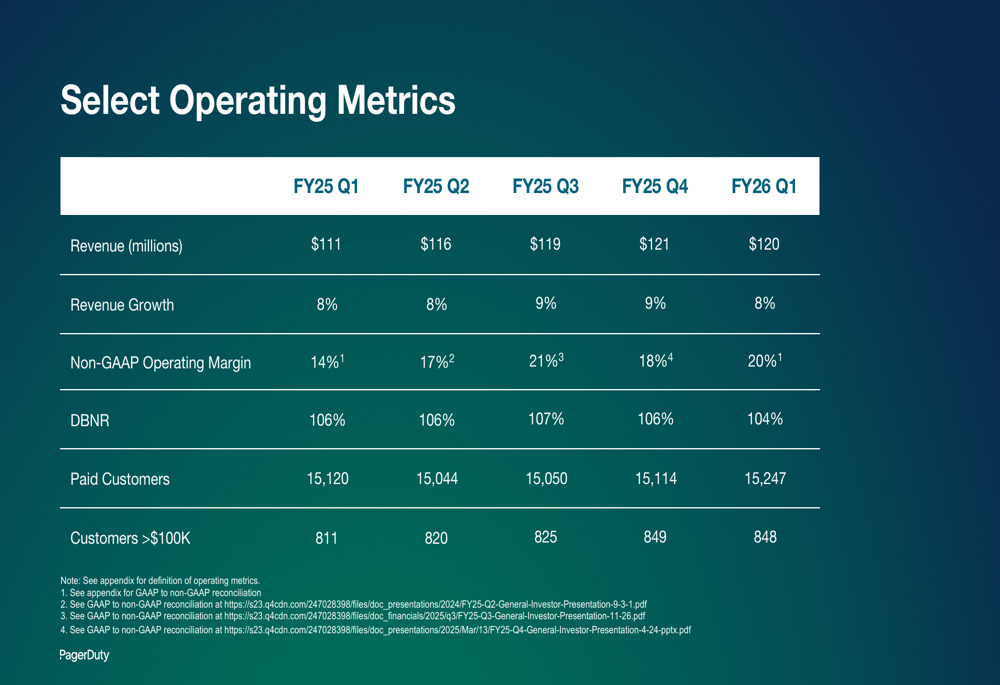

The following table illustrates PagerDuty’s performance trends over the past five quarters:

Strategic Initiatives and Product Development

PagerDuty continues to position itself as a leader in digital operations management with its AI-powered Operations Cloud platform. The company serves a significant portion of Fortune 500 and Forbes AI 50 companies, as well as two-thirds of the Fortune 100.

The PagerDuty Operations Cloud integrates automation and AI capabilities to help organizations improve operational efficiency:

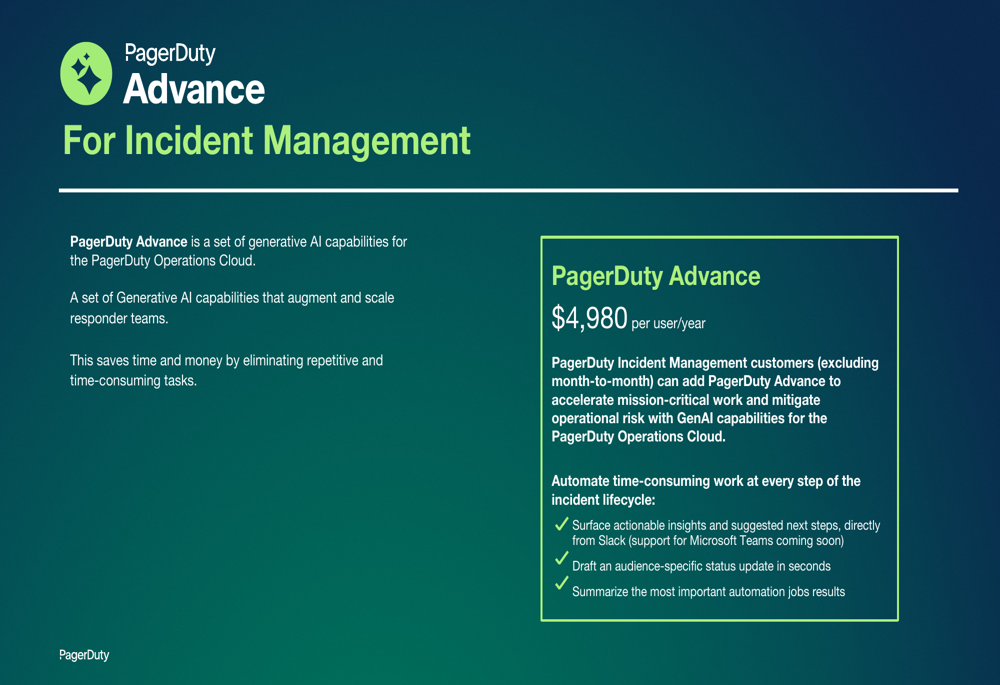

A key strategic initiative is PagerDuty Advance, which provides generative AI capabilities for the Operations Cloud at $4,980 per user/year. This offering aims to automate time-consuming work throughout the incident lifecycle, helping customers save time and money by eliminating repetitive tasks.

The company’s extensive integration ecosystem remains a significant competitive advantage, with over 700 integrations across monitoring, security, DevOps, customer service, infrastructure automation, and collaboration tools:

Competitive Industry Position

PagerDuty estimates its total addressable market at $50 billion, targeting four key personas: developers (30 million users), infrastructure and operations (23 million), customer service (28 million), and SecOps (6 million).

The following slide illustrates the market opportunity and key statistics related to incident management:

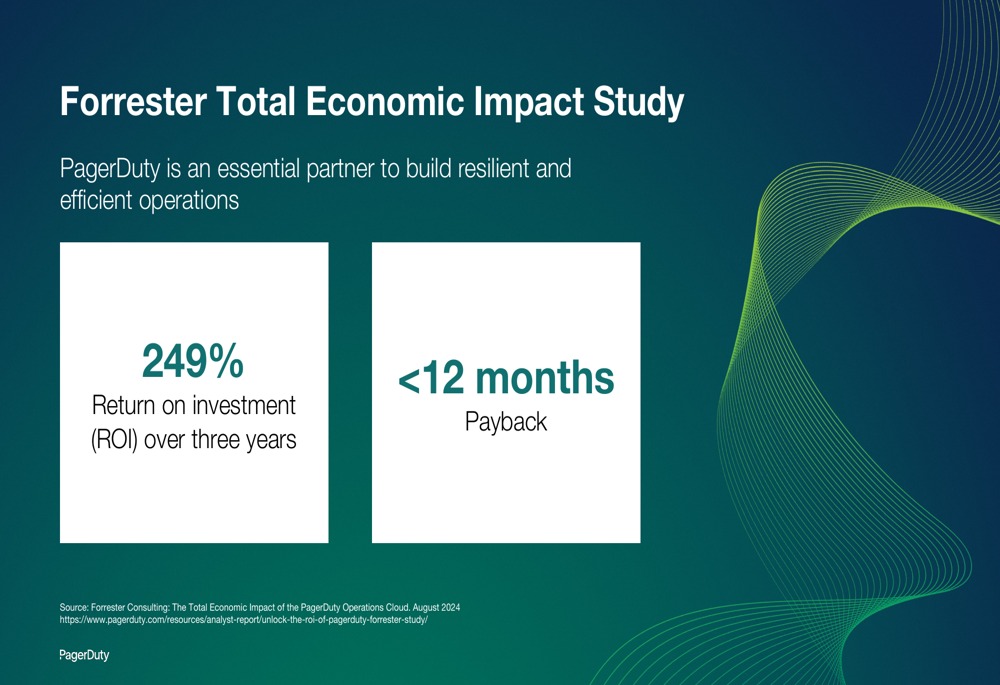

The company cites a Forrester Total (EPA:TTEF) Economic Impact study showing a 249% return on investment over three years with a payback period of less than 12 months, highlighting the value proposition of its platform.

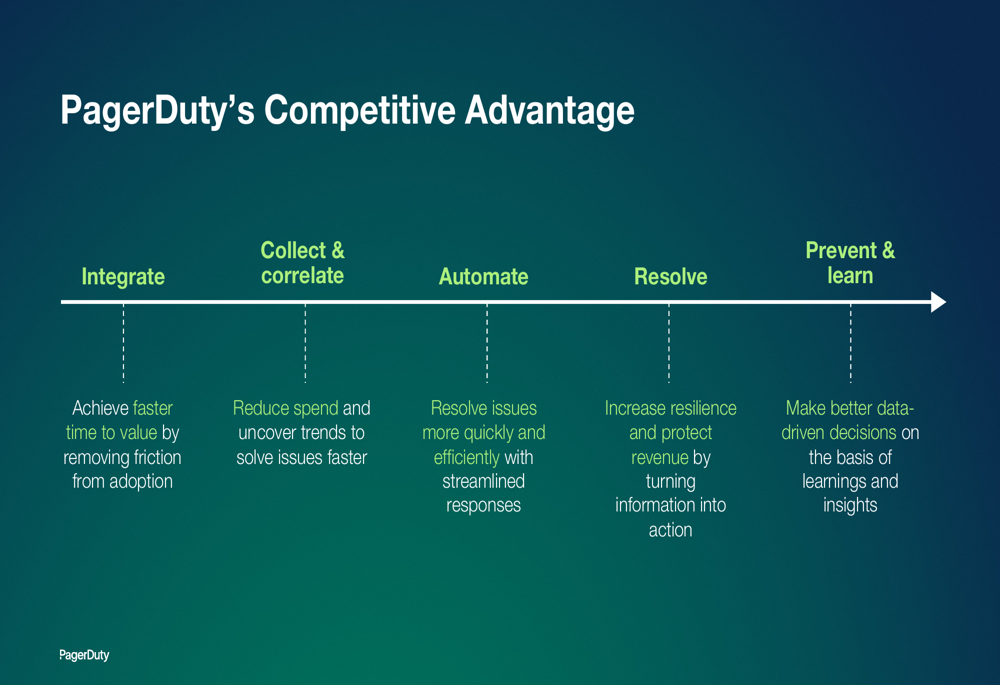

PagerDuty’s competitive advantage stems from its comprehensive approach to incident management, combining integration capabilities, data collection and correlation, automation, resolution, and continuous learning:

Forward-Looking Statements

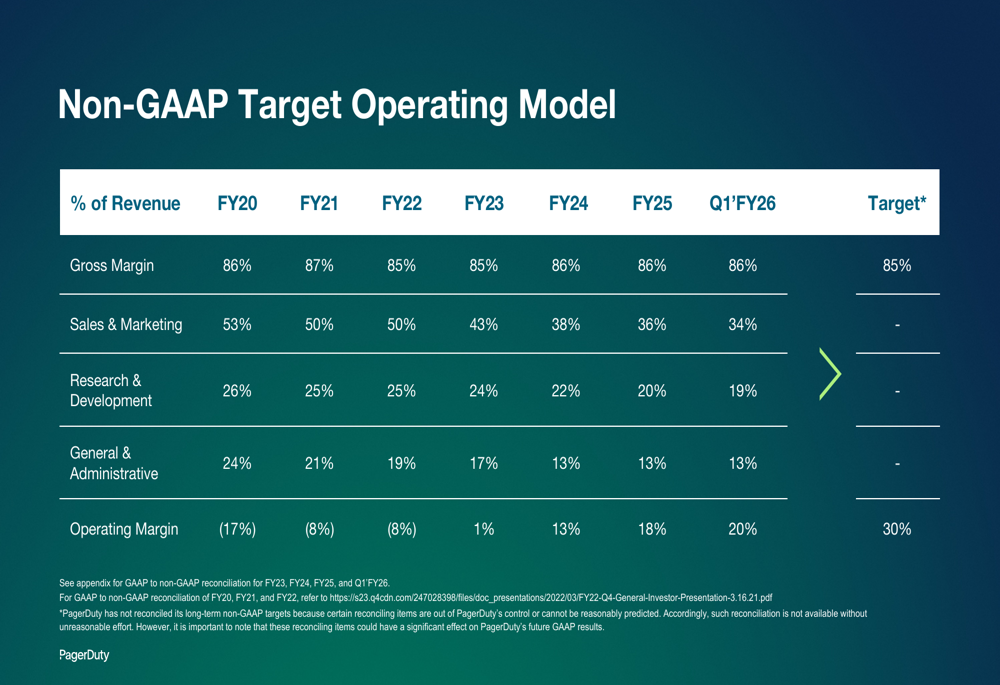

PagerDuty has demonstrated consistent progress toward its long-term financial targets, with significant improvement in operating margins over the past several years. The company’s non-GAAP operating margin has improved from -17% in FY20 to 20% in Q1 FY26, with a target of 30%.

The following chart illustrates this progression and the company’s target operating model:

In the recent earnings call for Q4 FY25, PagerDuty provided revenue guidance of $500-$507 million for FY26, representing 7-8% growth. The company anticipates an acceleration in ARR growth in the latter half of the year, with a continued focus on enhancing enterprise sales and recovering the commercial segment.

CEO Jennifer Tejada emphasized that "operational maturity and resilience are no longer nice to have. They’re becoming central to the enterprise business strategy," highlighting the company’s strategic positioning in an increasingly digital-first business environment.

While PagerDuty faces challenges from a volatile macroeconomic environment and increasing competition in AI operations, its strong gross profit margins of 82.5% and improving operational efficiency position the company to maintain profitability while investing in growth initiatives. The slight decline in customer retention metrics will be an important area to monitor in upcoming quarters as the company executes its sales transformation strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.