TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Palvella Therapeutics (NASDAQ:PVLA) presented its Q2 2025 financial results and corporate update on August 14, 2025, highlighting significant progress across its pipeline of treatments for rare genetic skin diseases. Despite the positive developments, shares fell 11.51% in premarket trading to $39.50, following a 3.31% gain to $44.64 in the previous session.

The clinical-stage biopharmaceutical company is focused on developing first-in-disease therapies for patients with rare genetic skin diseases, with its lead product candidate QTORIN™ Rapamycin advancing through late-stage clinical trials. The company’s stock has shown remarkable strength with an 80.8% year-to-date return, according to previous reports, despite today’s premarket pressure.

Pipeline Progress & Near-Term Catalysts

Palvella outlined several high-impact milestones expected by Q1 2026, demonstrating the company’s progress in addressing significant unmet medical needs in rare skin conditions.

As shown in the following milestone timeline:

The company’s Phase 3 SELVA trial for microcystic lymphatic malformations (LMs) has exceeded its enrollment target and remains on track for a Q1 2026 data readout. This represents a significant advancement toward potentially securing the first FDA-approved therapy for this condition, which affects an estimated 30,000 diagnosed patients in the U.S.

The Phase 2 TOIVA trial for cutaneous venous malformations (VMs) continues enrollment and is expected to deliver results in Q4 2025. This proof-of-concept study will enroll approximately 15 patients without statistical hierarchy of endpoints. The company received FDA Fast Track Designation for this indication in 2024, underscoring the significant unmet need.

The following slide details the company’s lead program:

Palvella is accelerating its New Drug Application (NDA) planning while simultaneously preparing for commercial launch in the U.S. The company recently appointed Ashley Kline as Chief Commercial Officer to lead these efforts.

For its second indication, cutaneous venous malformations, Palvella highlighted the significant market opportunity:

This indication represents a larger potential market with an estimated U.S. diagnosed prevalence exceeding 75,000 patients. The company emphasized the significant unmet need for targeted, localized therapy for these patients, who currently have no FDA-approved treatment options.

Financial Performance & Position

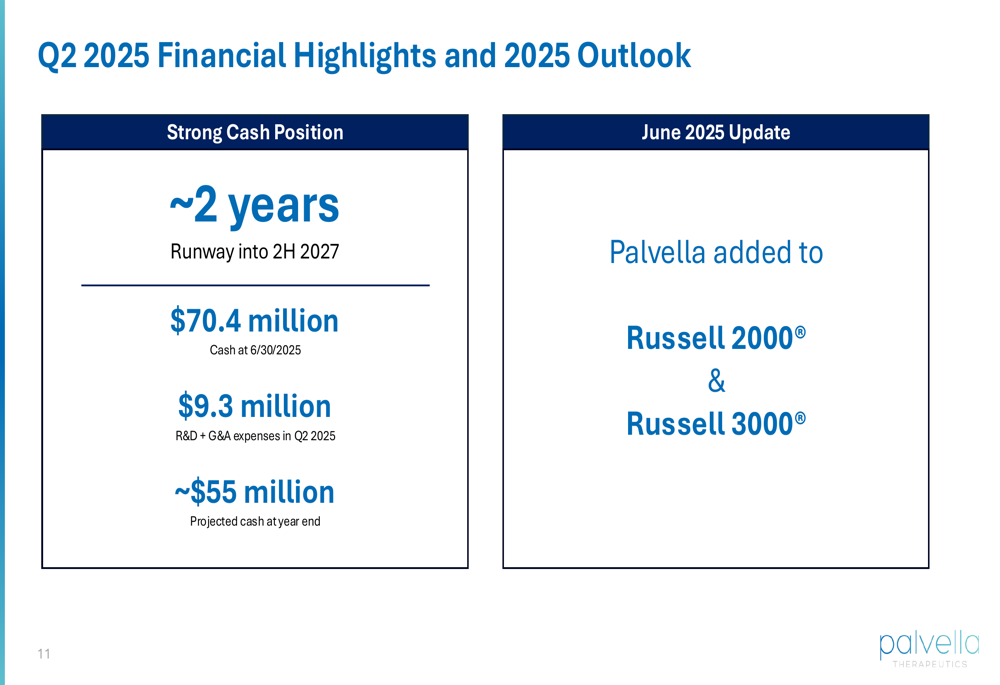

Palvella reported a strong financial position with approximately two years of runway extending into the second half of 2027. As of June 30, 2025, the company held $70.4 million in cash, down from $75.6 million at the end of Q1 2025, reflecting ongoing investments in research and development.

The company’s financial highlights are illustrated in the following slide:

Operating expenses for Q2 2025 totaled $9.3 million, covering both R&D and general and administrative costs. This represents a significant increase from the previous year, consistent with the company’s Q1 trend when R&D expenses rose to $4.1 million from $1 million year-over-year, and G&A expenses increased to $3.8 million from $0.8 million.

Palvella projects a year-end cash position of approximately $55 million, suggesting continued disciplined spending while advancing its clinical programs. The company also announced its addition to the Russell 2000® and Russell 3000® indices in June 2025, potentially expanding its investor base.

Strategic Initiatives & Commercial Preparations

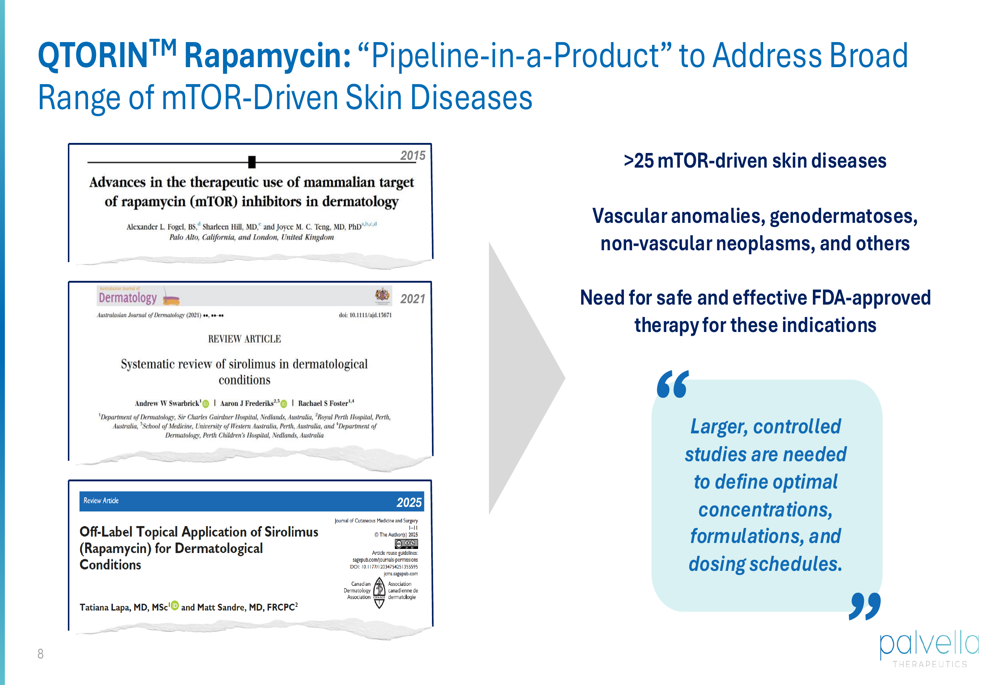

Palvella is positioning QTORIN™ Rapamycin as a "pipeline-in-a-product" with potential applications across more than 25 mTOR-driven skin diseases. The company’s strategic approach is illustrated in this comprehensive overview:

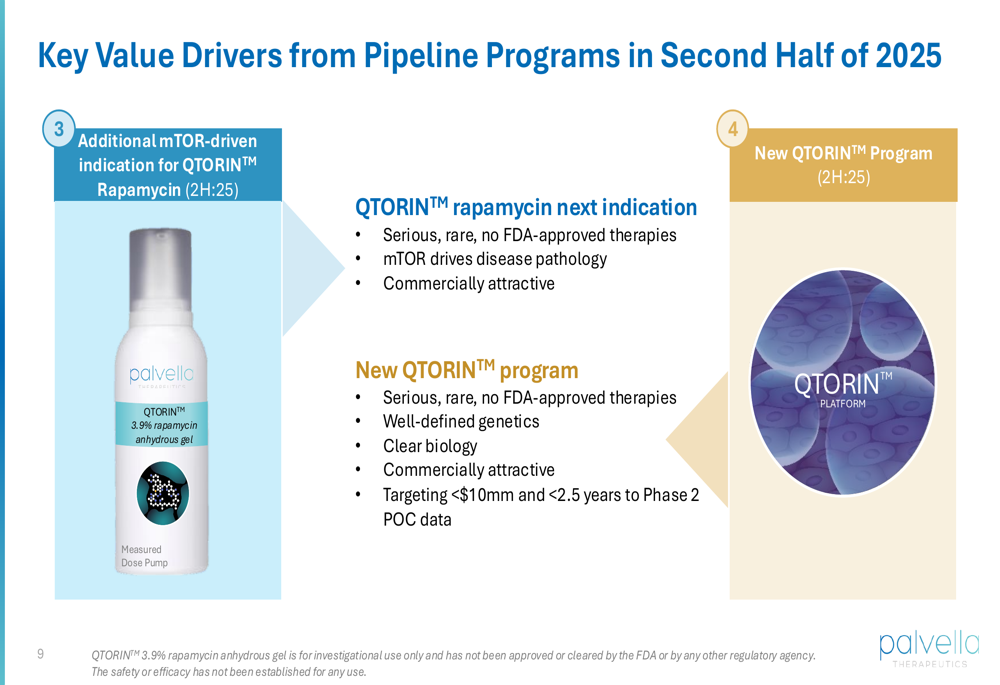

Beyond its two lead indications, Palvella plans to announce an additional mTOR-driven indication for QTORIN™ Rapamycin in the second half of 2025. This expansion targets another serious, rare condition with no FDA-approved therapies where mTOR drives disease pathology.

The company also intends to unveil a new QTORIN™ program in the second half of 2025, focusing on conditions with well-defined genetics and clear biology. Palvella emphasized its disciplined approach to pipeline expansion, targeting programs requiring less than $10 million and less than 2.5 years to reach Phase 2 proof-of-concept data.

The following slide outlines these key value drivers:

Forward-Looking Statements & Outlook

Palvella’s near-term focus remains on delivering clinical data from its two lead programs while expanding its pipeline. The company is preparing for potential commercialization of QTORIN™ Rapamycin, should clinical trials prove successful and regulatory approval be granted.

The significant premarket stock decline suggests investors may be reacting to factors beyond the presentation’s content, potentially related to broader market conditions or specific concerns about the company’s cash burn rate, which increased from Q1 to Q2.

While Palvella maintains a positive outlook based on its pipeline progress and financial position, investors will likely be watching closely for the upcoming clinical readouts that could validate the company’s approach to treating rare genetic skin diseases. The Q4 2025 data from the Phase 2 TOIVA trial will provide the next major catalyst, followed by the Phase 3 SELVA results in Q1 2026, both representing potential inflection points for the company’s valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.