Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Parker-Hannifin Corporation (NYSE:PH) presented its fiscal 2025 third quarter earnings on May 1, 2025, highlighting record margins and strong cash flow generation despite a challenging macroeconomic environment. The industrial components manufacturer reported modest sales growth, with strength in aerospace offsetting softness in certain industrial markets.

The company’s stock closed at $605.06 on April 30, 2025, and showed a slight increase of 0.32% in premarket trading following the earnings release. Over the past year, Parker-Hannifin shares have traded between $488.45 and $718.44, reflecting investor confidence in the company’s transformation strategy.

Quarterly Performance Highlights

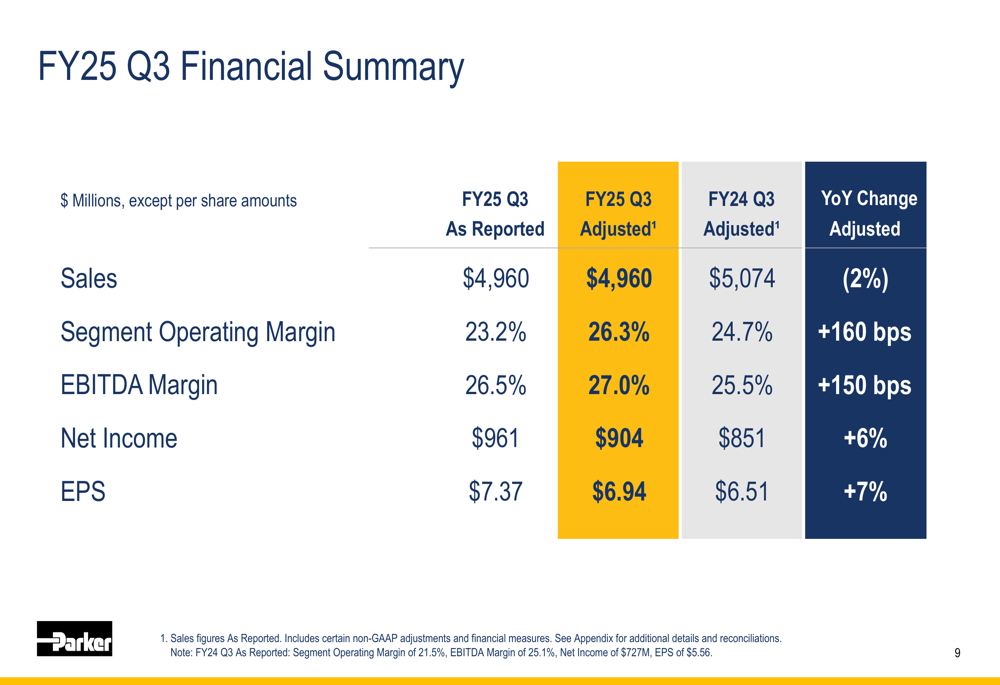

Parker-Hannifin reported sales of $5.0 billion for the third quarter, representing a 2% increase on a reported basis and 1% organic growth compared to the same period last year. The company achieved record adjusted segment operating margin of 26.3%, an improvement of 160 basis points year-over-year.

As shown in the following financial summary, adjusted earnings per share grew 7% to $6.94, while adjusted EBITDA margin reached a record 27.0%, up 150 basis points from the prior year:

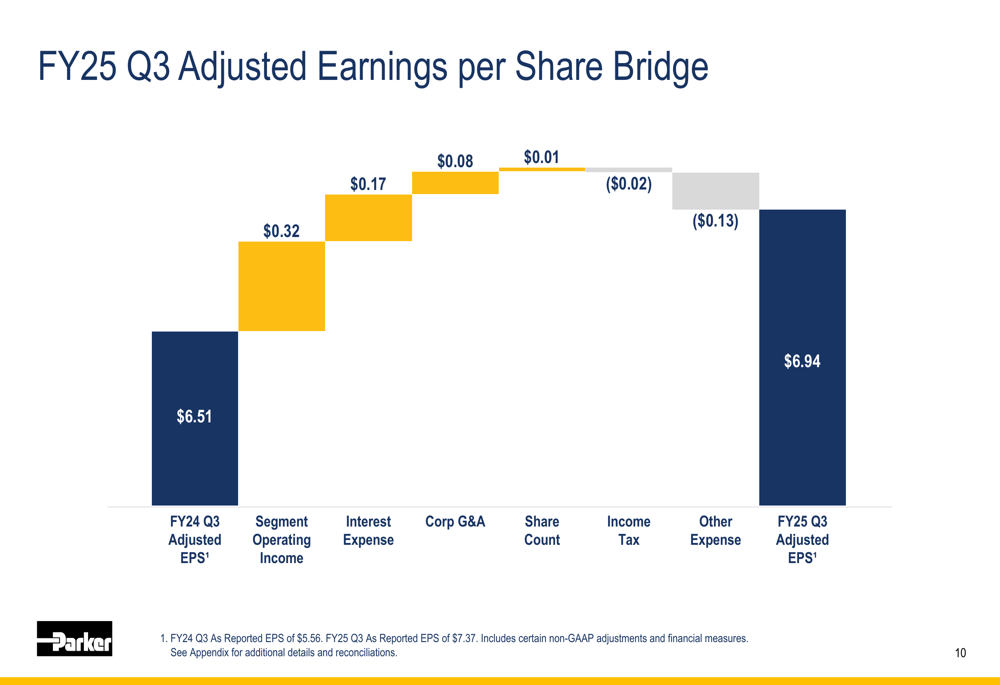

The company’s EPS growth was primarily driven by segment operating income improvement ($0.32), reduced interest expense ($0.17), and lower corporate G&A costs ($0.08), partially offset by higher other expenses ($-0.13) and a slight increase in income tax ($-0.02):

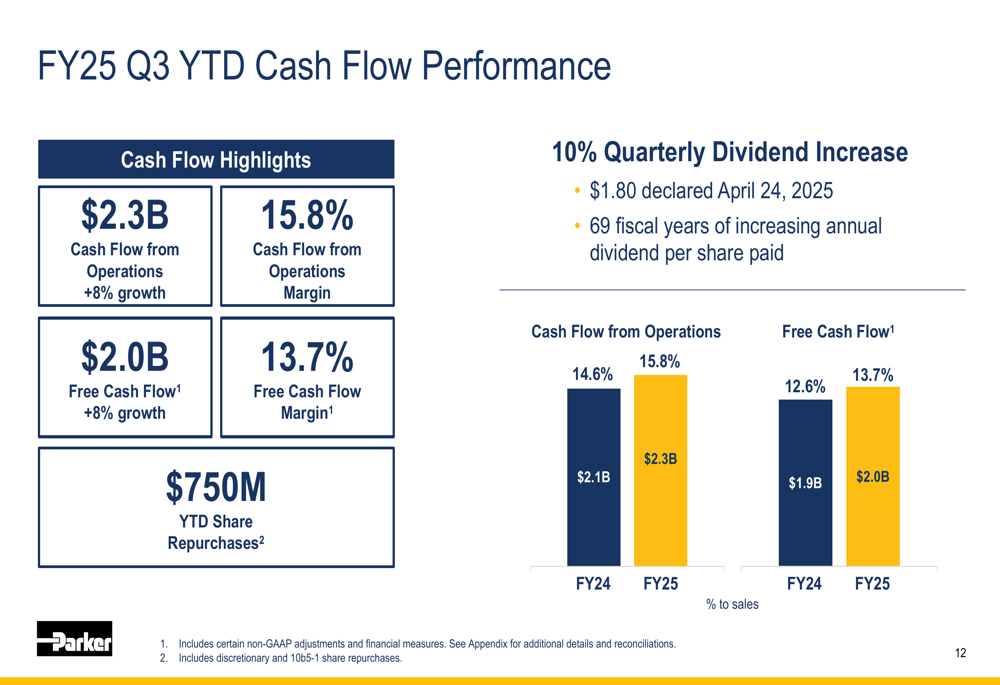

Cash flow performance remained robust, with year-to-date cash flow from operations reaching $2.3 billion, an 8% increase compared to the prior year. Free cash flow grew at a similar rate to $2.0 billion, representing a 13.7% free cash flow margin. The company also announced a 10% increase in its quarterly dividend to $1.80 per share, marking the 69th consecutive fiscal year of dividend increases.

Segment Analysis

Parker-Hannifin’s performance varied across its business segments, with aerospace showing particularly strong results while industrial segments demonstrated resilience and margin improvement despite mixed market conditions.

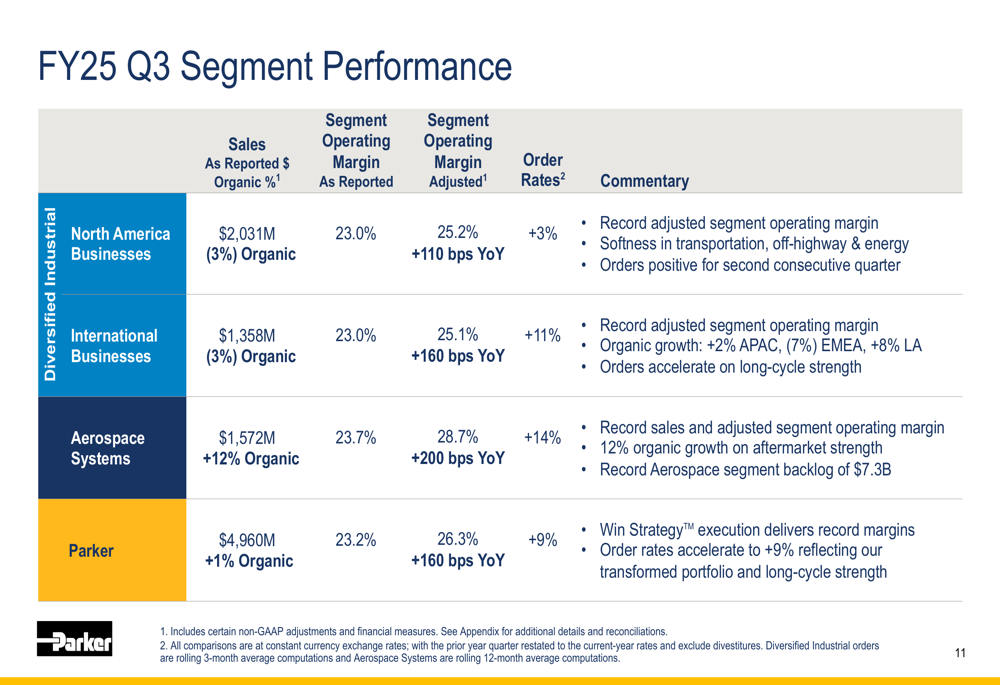

The Aerospace Systems segment led growth with sales of $1.57 billion, representing 12% organic growth driven primarily by aftermarket strength. The segment achieved a record adjusted operating margin of 28.7%, up 200 basis points year-over-year, and reported a record backlog of $7.3 billion. Order rates increased 14%, indicating continued momentum in this sector.

In the Diversified Industrial segments, North America reported sales of $2.03 billion with 3% organic growth and a record adjusted operating margin of 25.2%, while International achieved sales of $1.36 billion with 3% organic growth and a record adjusted margin of 25.1%. The following segment breakdown illustrates performance across the business:

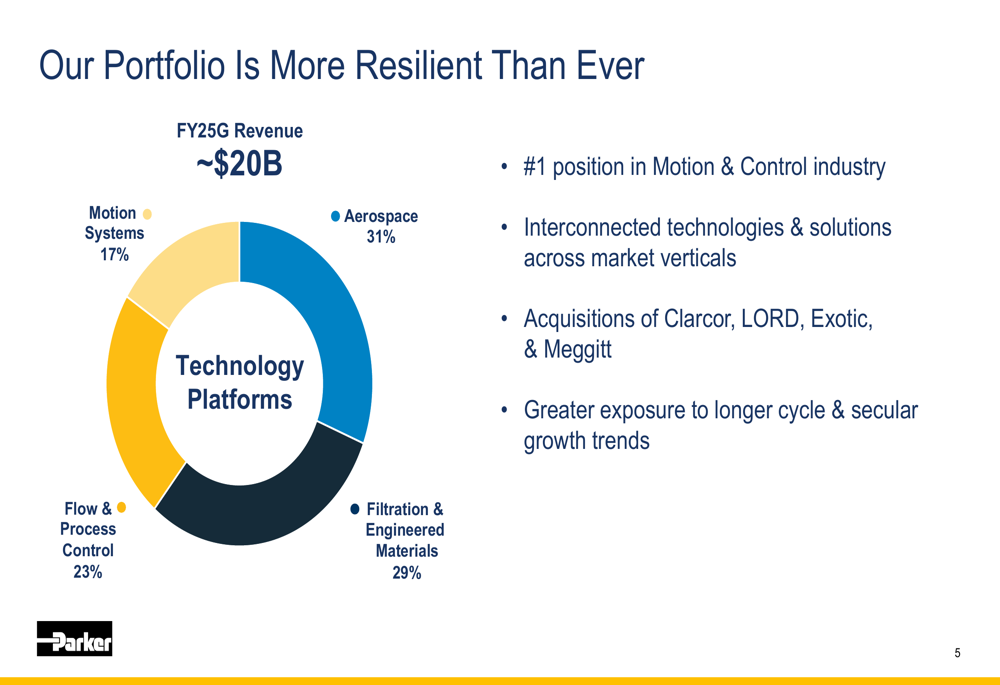

The company’s diversified portfolio has evolved significantly through acquisitions, with Aerospace now representing 31% of revenue, followed by Filtration & Engineered Materials at 29%, Flow & Process Control at 23%, and Motion Systems at 17%:

Strategic Initiatives

Parker-Hannifin’s "Win Strategy 3.0," updated in July 2024, continues to drive operational improvements across the organization. The strategy focuses on four key goals: Engaged People, Customer Experience, Profitable Growth, and Financial Performance.

Margin expansion has been supported by several simplification initiatives, including structure and footprint optimization, organizational design improvements, revenue complexity reduction through the 80/20 principle, and the company’s "Simple by Design" approach to product development.

The company has also emphasized its strategic supply chain as a competitive differentiator, focusing on demand and capacity planning, dual sourcing for resilience, local-for-local manufacturing, and tariff mitigation strategies to protect earnings per share.

Forward Guidance

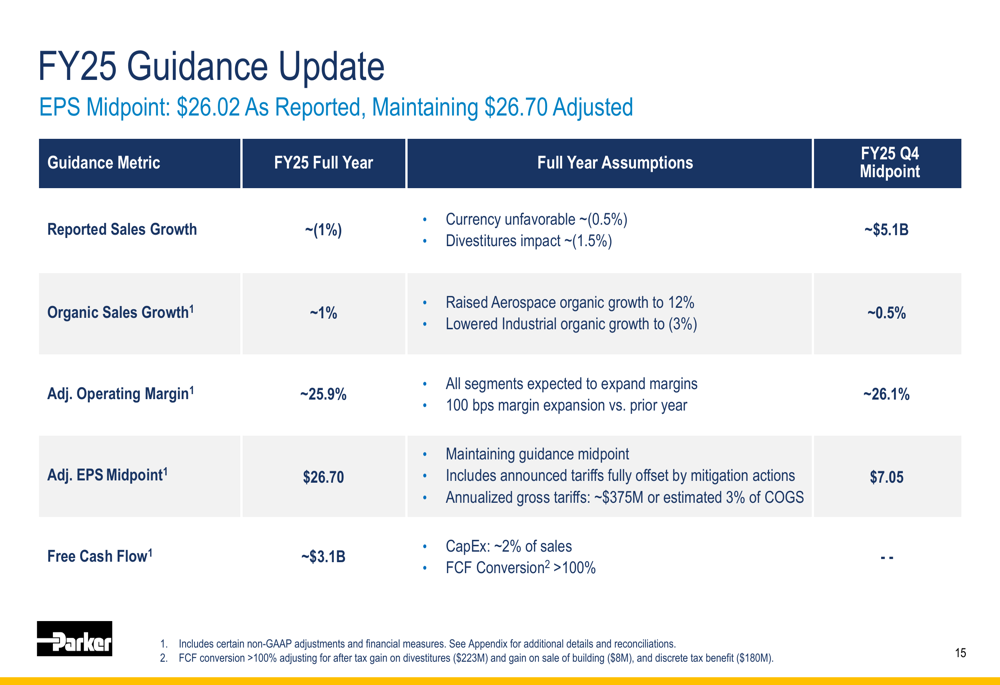

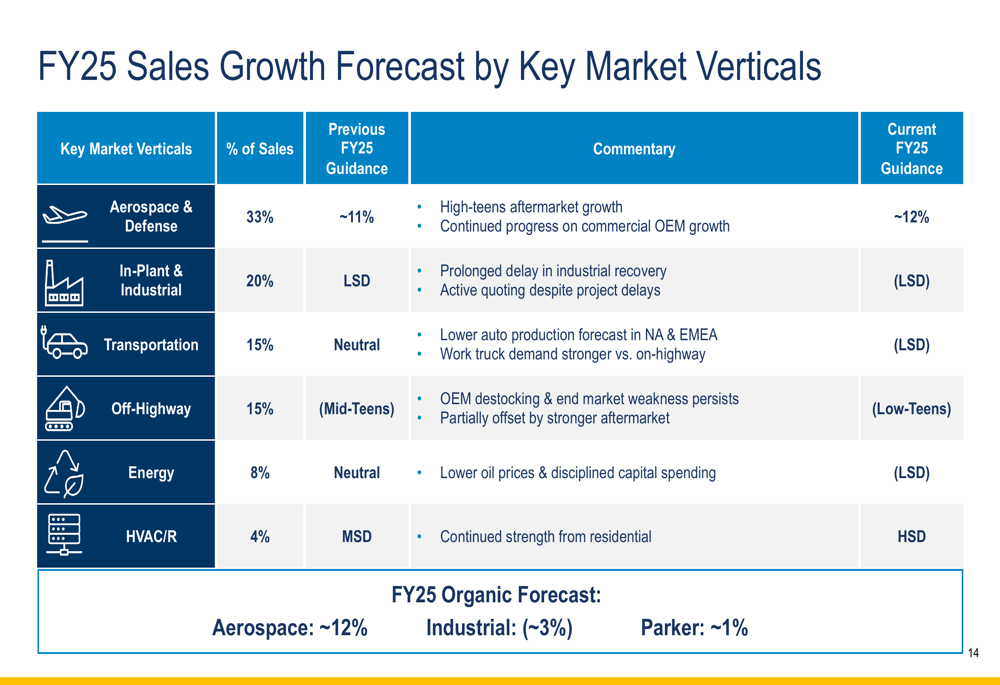

Looking ahead, Parker-Hannifin updated its fiscal 2025 guidance, maintaining its adjusted EPS midpoint at $26.70 despite currency headwinds and the impact of divestitures. The company expects approximately 1% organic sales growth for the full year, with aerospace continuing to lead at around 12% growth while industrial segments are projected to decline by approximately 3%.

By market vertical, aerospace and defense is expected to grow approximately 12%, HVAC/R in the high single digits, while transportation, energy, and in-plant industrial markets are forecasted to decline in the low single digits. The off-highway market faces the most significant challenges with an expected decline in the low teens.

Conclusion

Parker-Hannifin’s third quarter results demonstrate the company’s ability to drive margin expansion and cash flow growth despite mixed market conditions. The transformed portfolio, with increased exposure to longer-cycle businesses like aerospace, has provided resilience against industrial market softness.

Order rates accelerated to 9% growth during the quarter, suggesting potential improvement in future periods, particularly in long-cycle businesses. With continued execution of its Win Strategy and focus on operational efficiency, Parker-Hannifin appears well-positioned to navigate the current economic environment while delivering shareholder value through margin expansion, strong cash flow, and consistent dividend growth.

Investors will be watching for signs of recovery in industrial markets and continued strength in aerospace when the company reports its fourth quarter results on August 7, 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.