Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

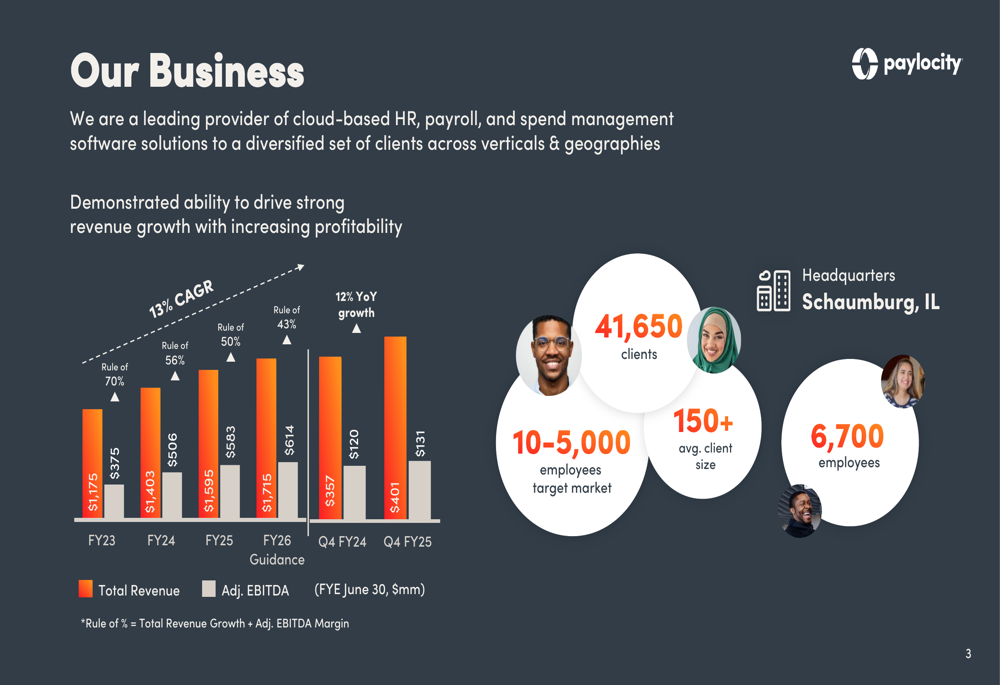

Paylocity Holding (NASDAQ:PCTY) presented its Q4 fiscal 2025 investor slides on August 5, highlighting the company’s continued growth and strategic expansion into finance and spend management solutions. The cloud-based HR and payroll software provider reported solid financial results while outlining its market positioning and long-term growth strategy.

Despite beating analyst expectations with Q4 EPS of $0.86 (14.67% above forecasts) and quarterly revenue of $400.7 million, Paylocity’s stock closed at $183.61, down 1.01% on the day of the presentation. The company maintains a market capitalization of $10.04 billion and operates in the competitive human capital management (HCM) software space.

Q4 and FY25 Performance Highlights

Paylocity reported strong financial performance for both the fourth quarter and full fiscal year 2025. The company achieved total revenue of $401 million for Q4, representing 12% year-over-year growth, with adjusted EBITDA of $131 million.

For the full fiscal year 2025, Paylocity generated total revenue of $1.595 billion, up from $1.403 billion in FY24, maintaining its growth trajectory while improving profitability metrics.

As shown in the following business overview chart, Paylocity has demonstrated consistent growth in both revenue and adjusted EBITDA:

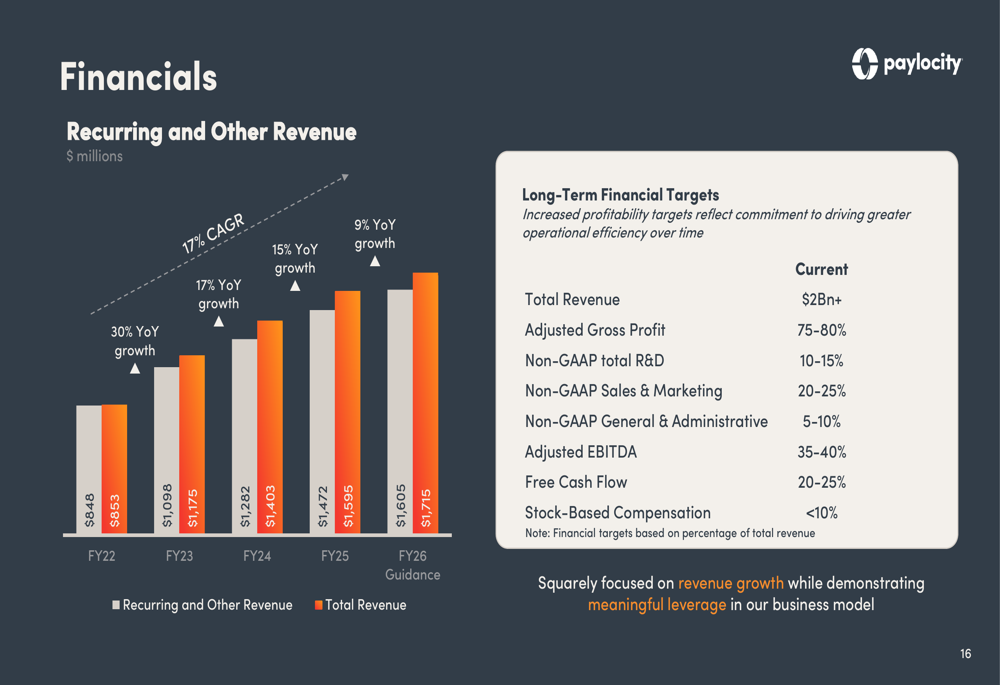

The company’s recurring revenue, which forms the backbone of its business model, grew to $1.472 billion in FY25, representing a 15% year-over-year increase. This growth has been supported by increasing average revenue per user (ARPU), which reached $35,300 in FY25, up 8% from the previous year.

The following chart illustrates Paylocity’s recurring revenue growth trajectory:

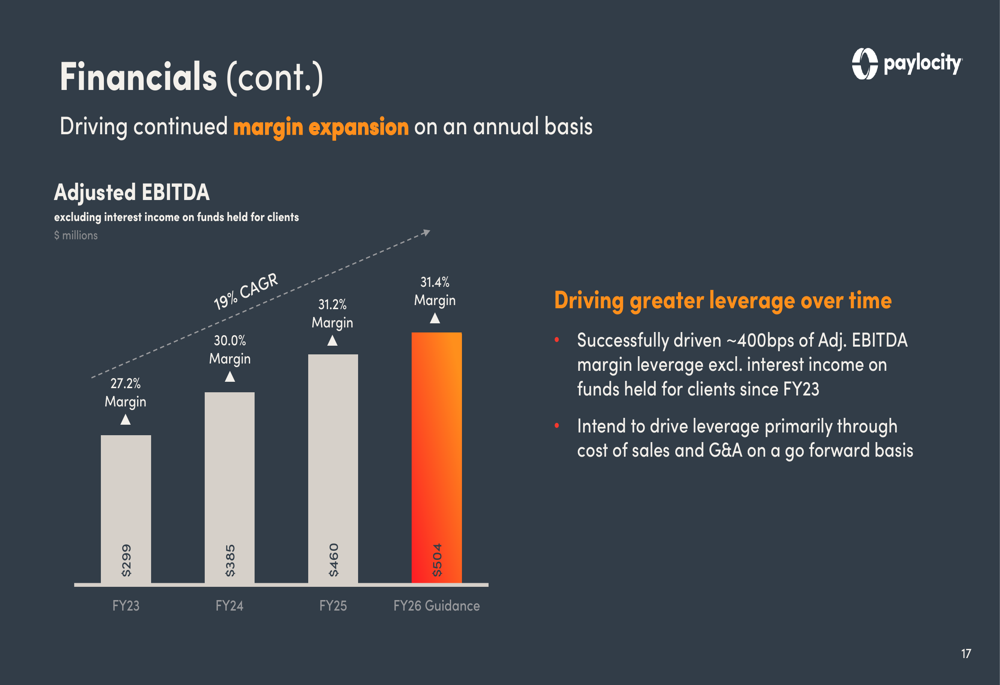

Profitability metrics showed significant improvement, with adjusted EBITDA margin expanding to 31.2% in FY25 from 30.0% in FY24. This represents approximately 400 basis points of margin improvement since FY23 when excluding interest income on funds held for clients.

As shown in the adjusted EBITDA chart below, Paylocity has maintained a 19% CAGR while steadily improving margins:

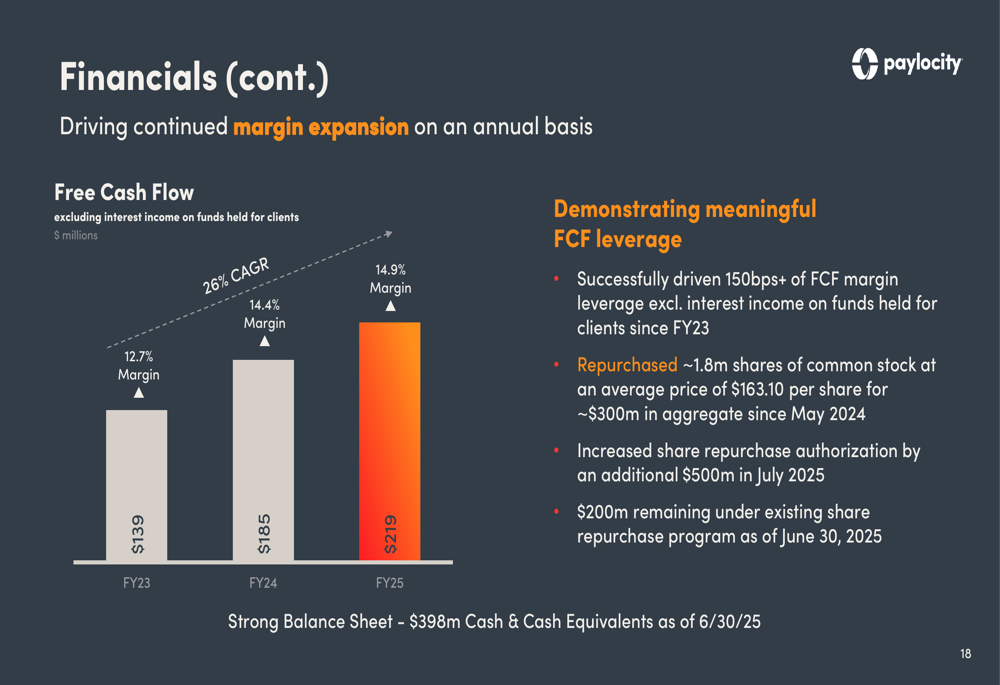

Free cash flow also demonstrated strong growth, reaching $219 million in FY25 with a 14.9% margin, up from $185 million and 14.4% margin in FY24. This represents a 26% CAGR since FY23.

The company has leveraged its strong cash position to return value to shareholders, repurchasing approximately 1.8 million shares at $163.10 per share for a total of $300 million since May 2024. Paylocity increased its share repurchase authorization by an additional $500 million in July 2025 and reported $398 million in cash and cash equivalents as of June 30, 2025.

Strategic Initiatives and Product Expansion

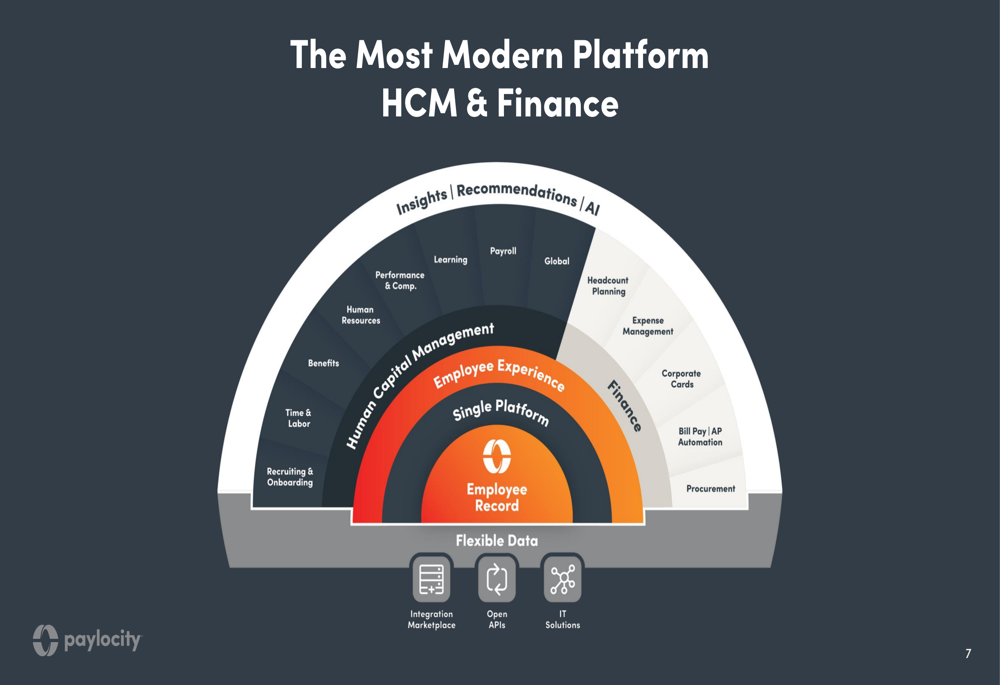

A key focus of Paylocity’s presentation was its strategic expansion beyond traditional HCM into finance and spend management solutions. The company has developed a unified platform that integrates HR and finance functions, creating what it calls "a single source of truth across the enterprise."

The following slide illustrates Paylocity’s comprehensive platform approach:

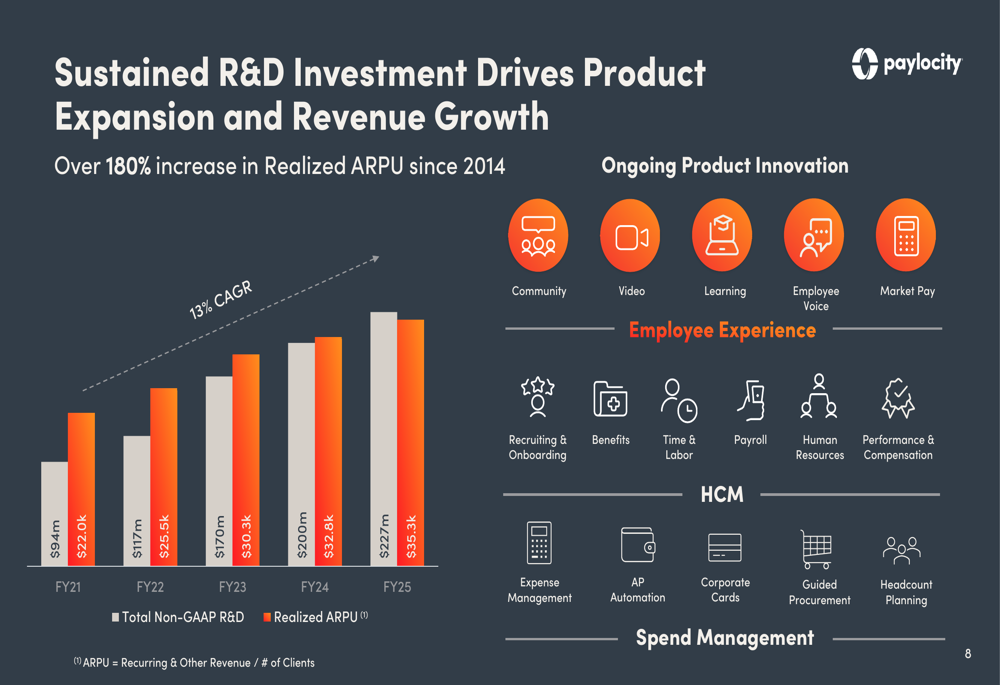

This expansion is supported by sustained R&D investment, which grew to $227 million in FY25, up from $200 million in FY24. This investment has enabled Paylocity to expand its product offerings and increase ARPU by over 180% since 2014.

As shown in the R&D investment chart below, there is a clear correlation between increased R&D spending and ARPU growth:

The company’s new finance and spend management offerings include expense management, AP automation, corporate cards, and guided procurement. These additions significantly expand Paylocity’s total addressable market and provide cross-selling opportunities to existing clients.

The finance platform is designed to give CFOs comprehensive control over company spending while maintaining integration with the HR system:

Competitive Positioning and Market Opportunity (SO:FTCE11B)

Paylocity positions itself in the mid-market segment, targeting businesses with 10-5,000 employees. The company estimates its total addressable market at approximately $22 billion, with current penetration at only about 3%, suggesting significant room for growth.

The following chart illustrates Paylocity’s position in the HCM competitive landscape:

With 41,650 clients as of June 30, 2025, and an average client size of over 150 employees, Paylocity has established a strong foothold in its target market. The company’s client acquisition strategy focuses on converting customers from competitors like ADP and Paychex (NASDAQ:PAYX), which represent the largest source of new clients.

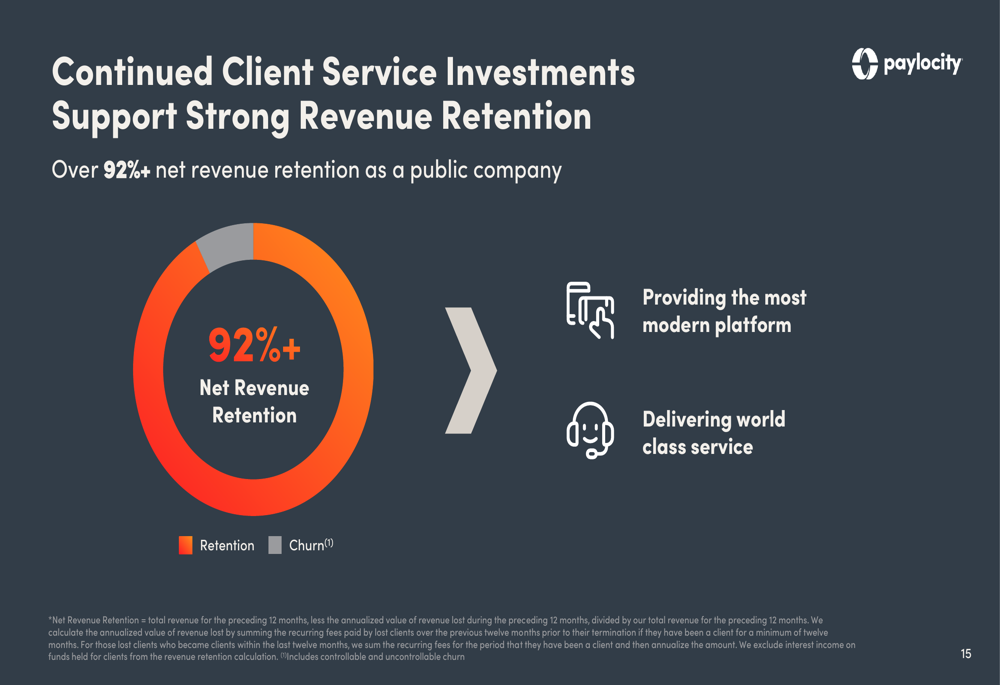

Paylocity attributes its competitive success to its modern platform, strong client service focus, and channel partner relationships. The company maintains a strong client retention rate, with over 92% net revenue retention as a public company.

The company’s go-to-market strategy relies on its direct sales force, which grew to 952 representatives in FY25, an 8% increase from 885 in FY24. Additionally, more than 25% of new client revenue comes from referrals through channel partners such as insurance brokers and benefits consultants.

Financial Outlook and Long-Term Targets

Looking ahead, Paylocity provided guidance for fiscal 2026, projecting total revenue between $1.707 billion and $1.722 billion, representing approximately 8% year-over-year growth. Recurring revenue is expected to be between $1.597 billion and $1.612 billion, a 9% increase from FY25.

The company outlined ambitious long-term financial targets, including:

- Total (EPA:TTEF) revenue exceeding $2 billion

- Adjusted gross profit margin of 75-80%

- Adjusted EBITDA margin of 35-40%

- Free cash flow margin of 20-25%

Paylocity’s management emphasized their focus on balancing revenue growth with margin expansion, primarily through leveraging cost of sales and G&A expenses.

During the earnings call, executives highlighted positive early feedback on Paylocity for Finance and expressed confidence in the company’s strategic direction. CEO Toby Williams reiterated the company’s commitment to its broker channel, while CFO Ryan Glenn expressed confidence in sustaining revenue growth.

As Paylocity continues to expand its product offerings and penetrate its addressable market, the company appears well-positioned for continued growth, though it faces challenges including market saturation, macroeconomic factors, and increasing competition in the integrated platform space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.