Hulk Hogan, wrestling icon, dies at 71 in Florida home

Introduction & Market Context

Pegasystems Inc . (NASDAQ:PEGA) released its Q2 2025 investor presentation on July 22, 2025, highlighting continued strong performance in its cloud business and significant improvements in cash flow generation. The enterprise software company, which specializes in AI decisioning and workflow automation, reported accelerating growth in its Pega Cloud segment while continuing its successful transition to a subscription-based business model.

Following a strong Q1 2025 performance that saw the company beat earnings expectations with an EPS of $1.53 (versus $0.54 forecast), Pegasystems has maintained momentum into the second quarter. The stock, which had surged nearly 30% after Q1 results, closed at $51.34 on July 22, with a slight uptick in aftermarket trading.

Quarterly Performance Highlights

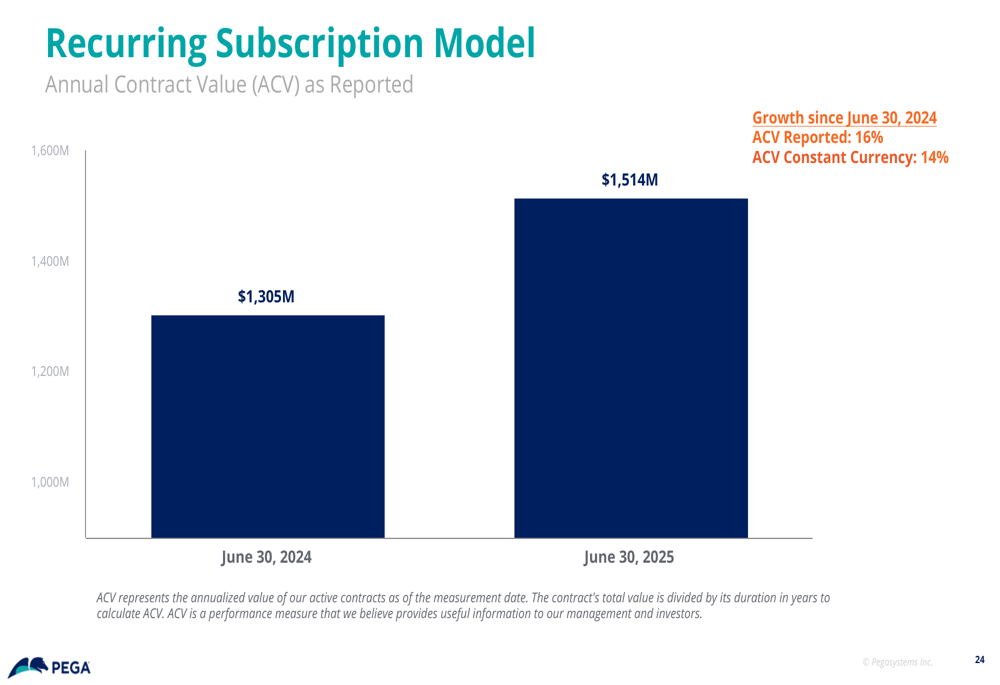

Pegasystems reported 14% Annual Contract Value (ACV) growth in constant currency for Q2 2025, with Pega Cloud ACV growing at an impressive 25% in constant currency. The company’s total ACV reached $1.514 billion as of June 30, 2025, up from $1.305 billion a year earlier.

As shown in the following chart detailing the company’s ACV growth:

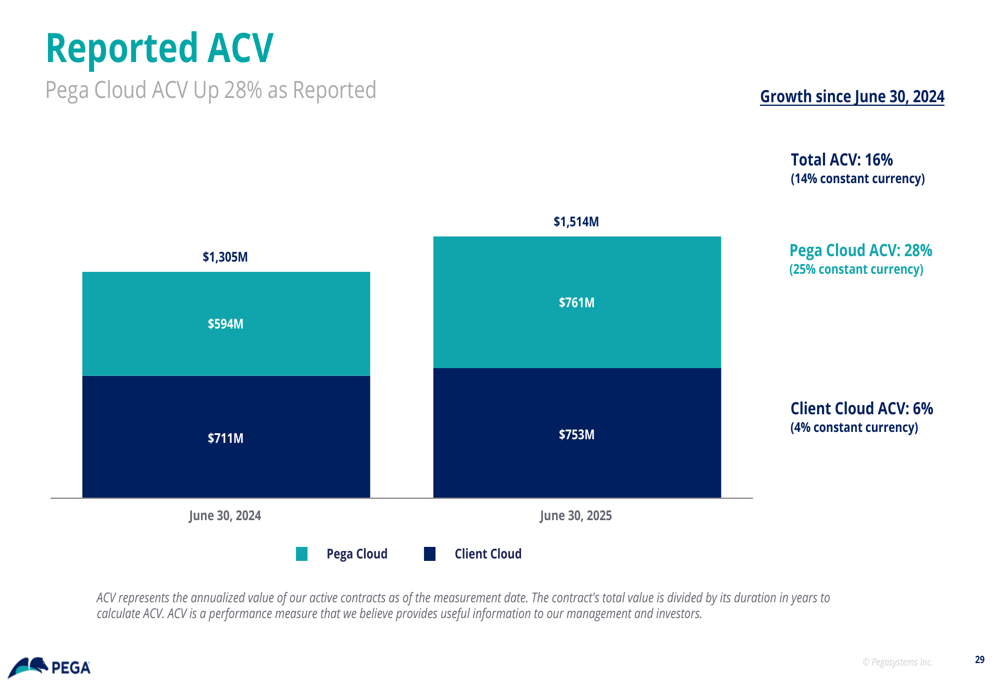

The breakdown between Pega Cloud and Client Cloud reveals the company’s continued shift toward cloud-based solutions. Pega Cloud ACV grew 28% as reported (25% in constant currency) to $761 million, while Client Cloud ACV increased by 6% as reported (4% in constant currency) to $753 million.

This detailed breakdown of ACV by segment provides further insight into the company’s revenue composition:

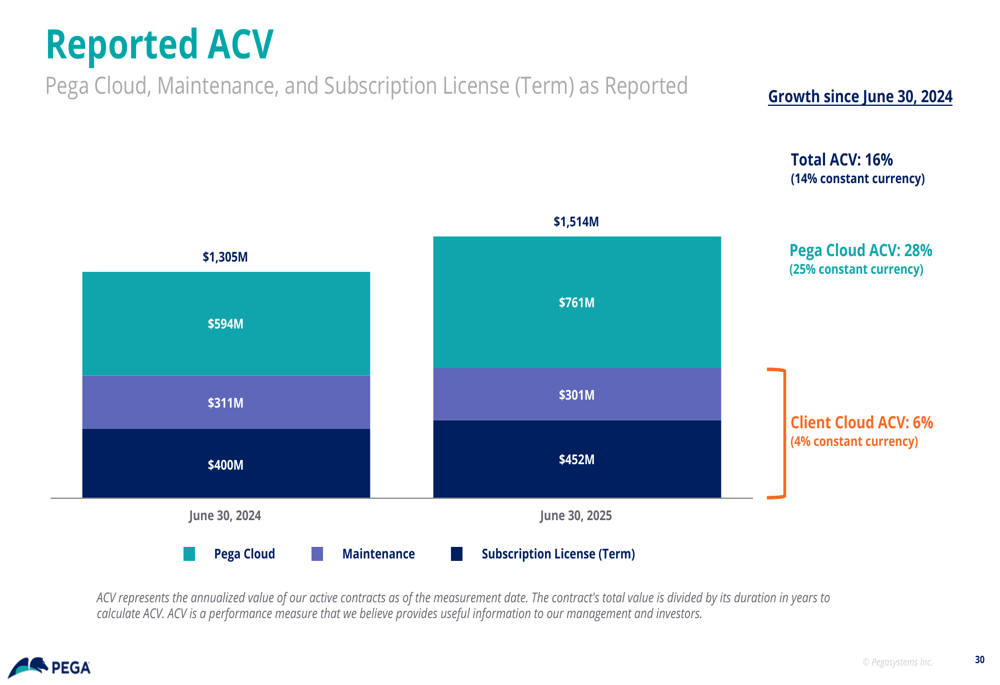

When examining ACV by type, the presentation shows the continued growth in Pega Cloud alongside subscription licenses, while maintenance revenue has slightly declined:

Cloud Growth and Subscription Transition

Pegasystems’ transition from a perpetual license model to a subscription-based business continues to yield positive results. The company highlighted its evolution from "Perpetual, Less Predictable, Lagging Growth & Margins" to "Recurring, More Predictable, Rule of 40 Driven" as a key strategic achievement.

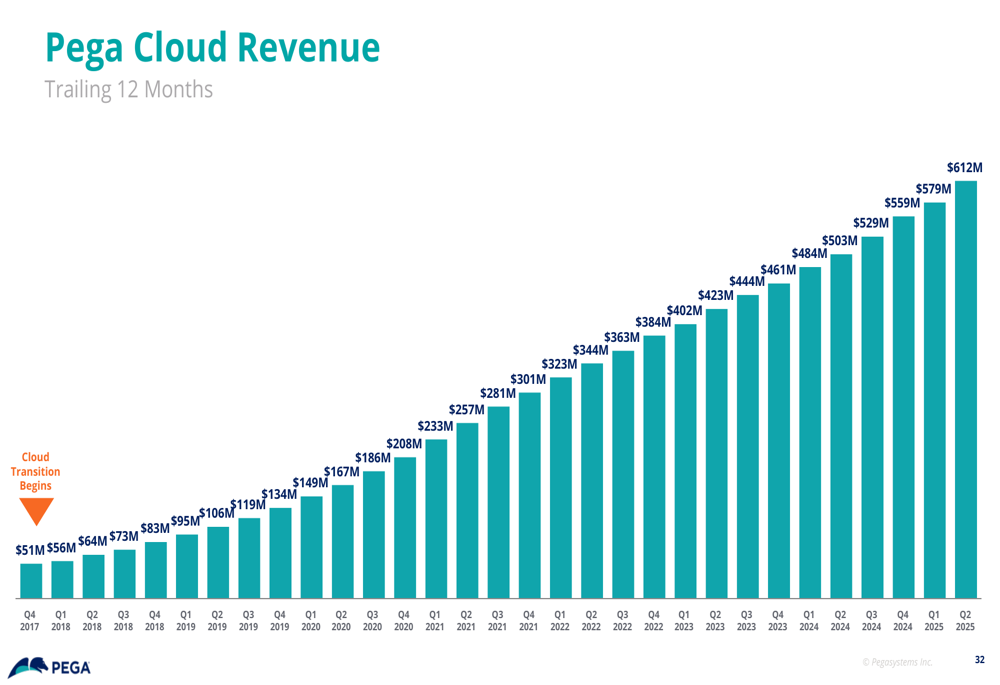

The Pega Cloud revenue has shown consistent growth over time, reaching $612 million on a trailing 12-month basis by Q2 2025. This represents significant progress from the $51 million reported in Q2 2017 when the company began its cloud transformation.

The following chart illustrates this impressive growth trajectory in Pega Cloud revenue:

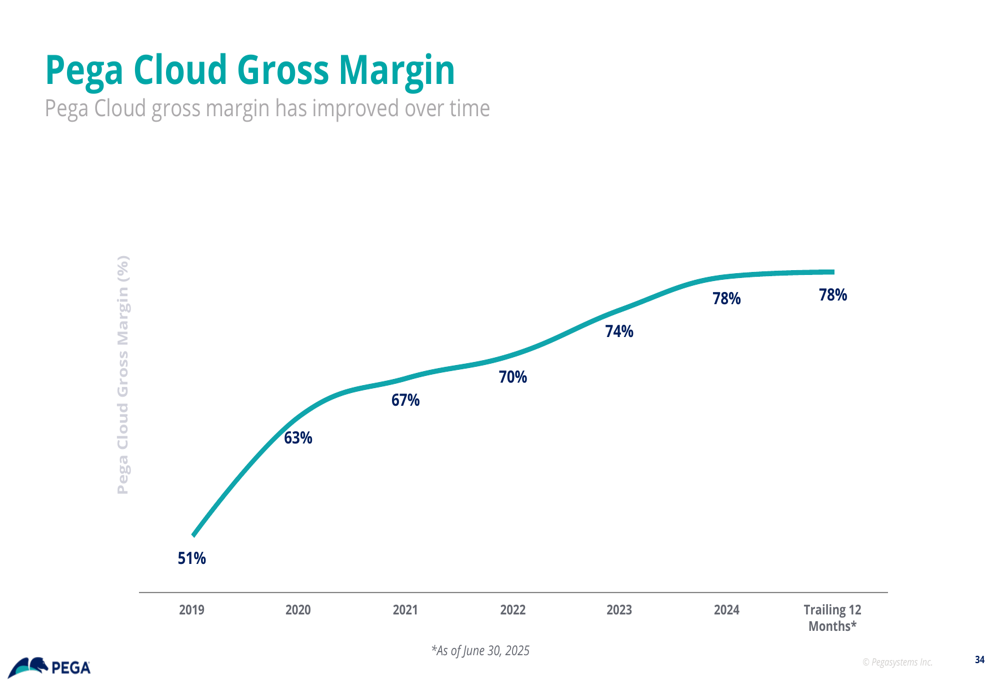

Notably, Pegasystems has also achieved substantial improvement in Pega Cloud gross margins, which have increased from 51% in 2019 to 78% in the trailing 12 months as of June 30, 2025. This margin expansion demonstrates the increasing efficiency and scale of the company’s cloud operations.

The progression of Pega Cloud gross margins is shown in this chart:

Cash Flow and Margin Expansion

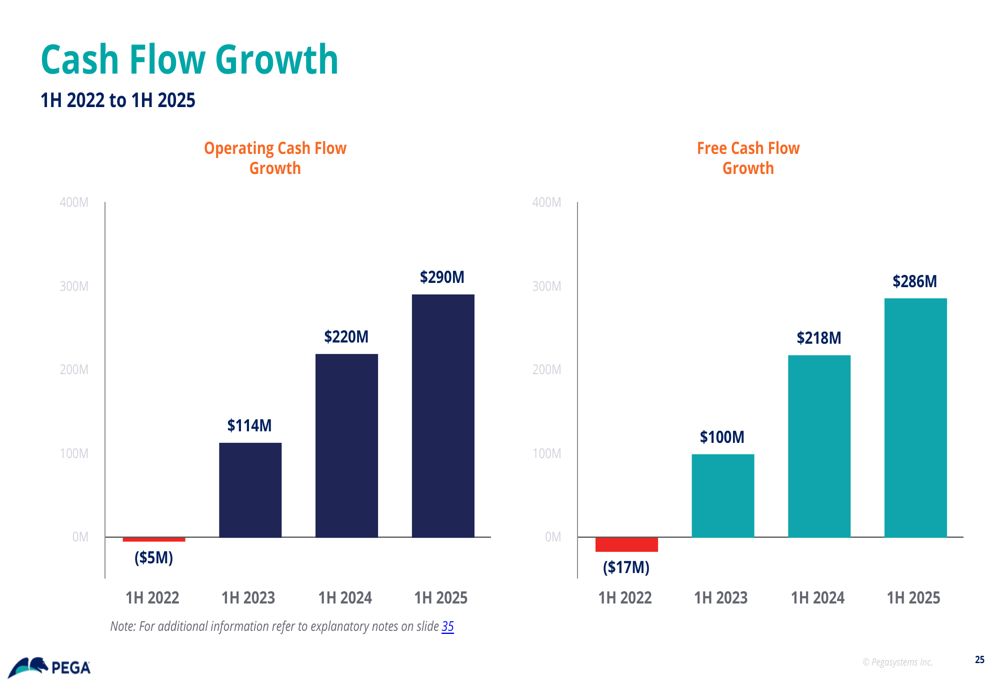

One of the most significant highlights of Pegasystems’ Q2 2025 presentation is the substantial improvement in cash flow generation. The company reported Year-to-Date Free Cash Flow of $286 million, continuing the strong momentum from Q1 where it had already matched its total free cash flow for 2023.

The presentation details the impressive growth in both operating and free cash flow over recent years:

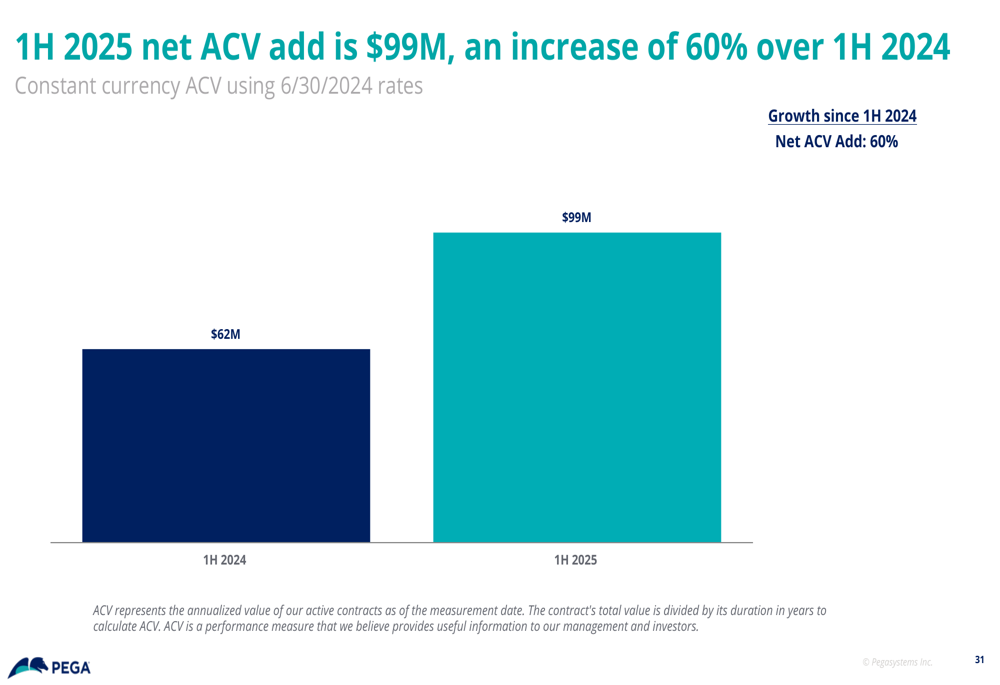

Net ACV additions for the first half of 2025 reached $99 million, representing a 60% increase over the same period in 2024. This acceleration in new business acquisition demonstrates the company’s growing market traction.

The net ACV addition growth is illustrated in this chart:

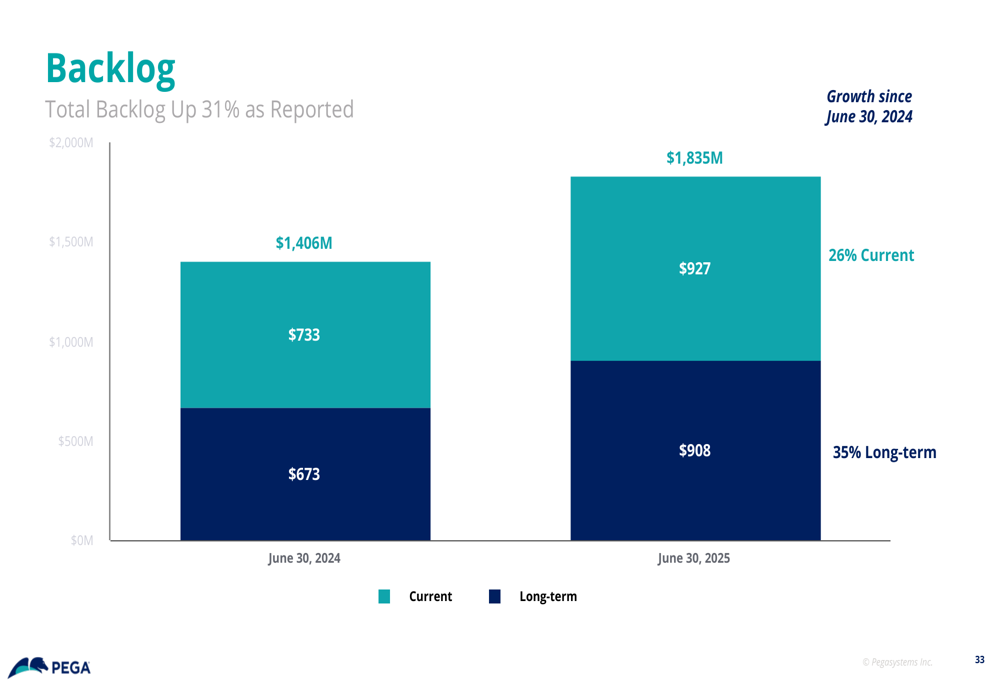

Additionally, Pegasystems reported a 31% increase in total backlog, which reached $1.835 billion as of June 30, 2025. This backlog consists of $927 million in current backlog (up 26%) and $908 million in long-term backlog (up 35%), providing strong visibility into future revenue.

The backlog growth and composition are shown here:

Strategic Positioning and Market Opportunity (SO:FTCE11B)

Pegasystems positions itself as a leader in AI decisioning and workflow automation, with recognition from industry analysts including Gartner (NYSE:IT) and Forrester. The company’s platform addresses three key business areas: 1:1 Customer Engagement, Customer Service, and Workflow Automation.

The presentation highlights Pegasystems’ client base, which includes major enterprises across various industries such as financial services (Citi, Rabobank), telecommunications (Virgin Media), government (Australian Department of Home Affairs), healthcare (HCA Healthcare (NYSE:HCA)), insurance (Aflac (NYSE:AFL)), and manufacturing ( Unilever (LON:ULVR)).

Pegasystems estimates its addressable market opportunity at over $90 billion in FY 2025, growing to more than $150 billion by FY 2029. This substantial market opportunity in the Platform & CRM space provides significant runway for continued growth.

Forward-Looking Statements

Looking ahead, Pegasystems aims to sustain growth by continuing its technology leadership, improving sales productivity, and executing its targeted go-to-market strategy. The company plans to expand margins by driving ACV growth and leveraging Pega Cloud efficiencies.

Management emphasized its commitment to balancing growth and margin expansion, guided by the "Rule of 40" principle, which suggests that a software company’s combined growth rate and profit margin should exceed 40%. The company also intends to continue returning capital to shareholders while increasing cash flow.

Given the strong performance in the first half of 2025 and the growing backlog, Pegasystems appears well-positioned to maintain its growth trajectory. The continued shift toward higher-margin cloud business, combined with improving operational efficiency, suggests potential for further margin expansion in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.