U.S. stocks rise on Fed cut bets; earnings continue to flow

Introduction & Market Context

PennyMac Mortgage Investment Trust (NYSE:PMT) reported a net loss for the second quarter of 2025, marking its second consecutive quarterly loss despite maintaining its dividend. According to the company’s Q2 earnings presentation released on July 22, PMT posted a net loss attributable to common shareholders of $3 million, or $(0.04) per diluted share, compared to a loss of $(0.01) per share in the previous quarter.

The mortgage REIT maintained its quarterly dividend of $0.40 per common share despite the losses, highlighting its commitment to shareholder returns. Following the earnings release, PMT’s stock closed at $12.48, up 1.64% for the day, with minimal activity in after-hours trading.

Quarterly Performance Highlights

PMT’s Q2 results revealed mixed performance across its three main business segments. The company’s book value per share declined to $15.00 from $15.43 at the end of the first quarter, reflecting ongoing challenges in the current interest rate environment.

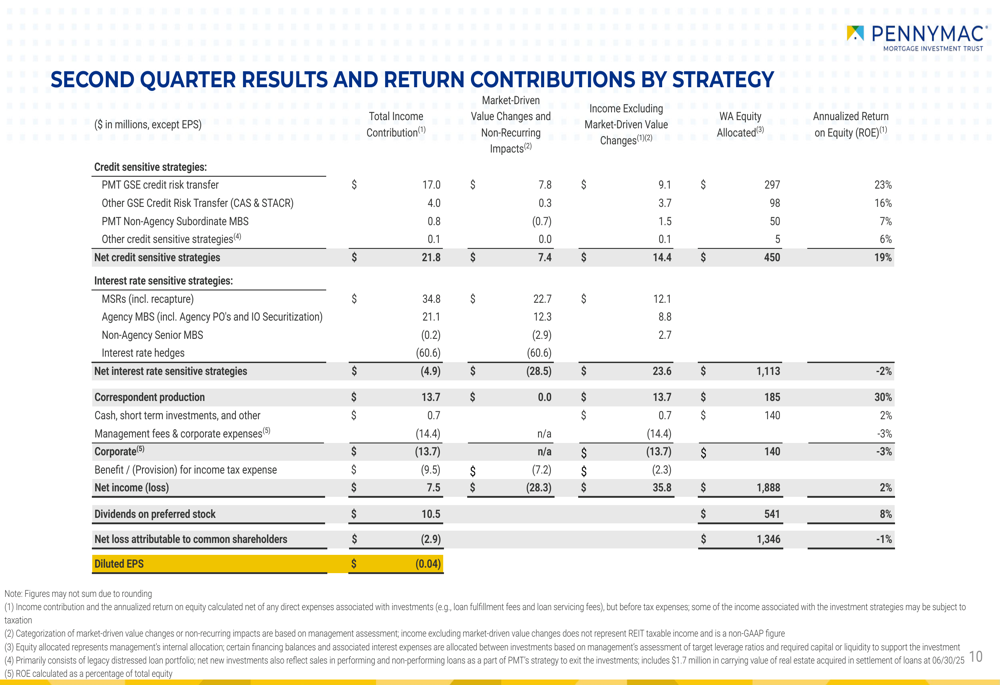

As shown in the following detailed breakdown of quarterly results by strategy:

Credit Sensitive Strategies generated pretax income of $14.4 million with a 19% annualized return on equity, while Interest Rate Sensitive Strategies posted a pretax income of $23.6 million excluding market-driven value changes but a pretax loss of $(5) million when including those changes. Correspondent Production delivered pretax income of $13.7 million with a strong 30% annualized return on equity.

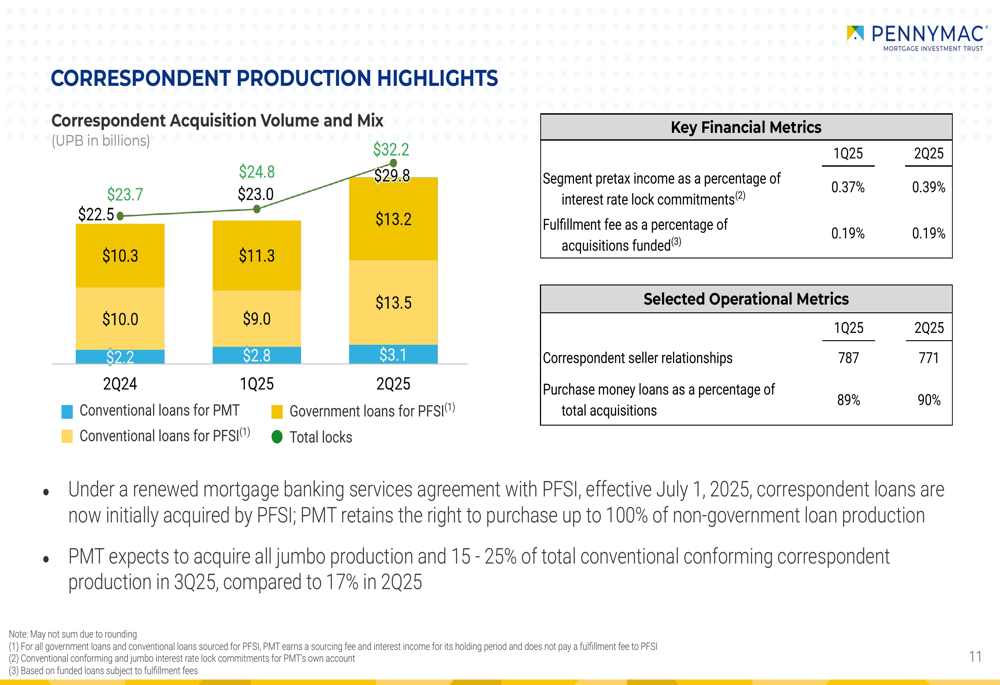

The company’s correspondent production volume remained substantial, with PMT acquiring $3.1 billion in unpaid principal balance (UPB) during the quarter. The following chart illustrates key metrics from the correspondent business:

Under a renewed mortgage banking services agreement with PennyMac Financial Services (NYSE:PFSI) effective July 1, 2025, correspondent loans are now initially acquired by PFSI, with PMT retaining the right to purchase up to 100% of non-government loan production. The company expects to acquire all jumbo production and 15-25% of total conventional conforming correspondent production in Q3 2025, compared to 17% in Q2.

Strategic Initiatives

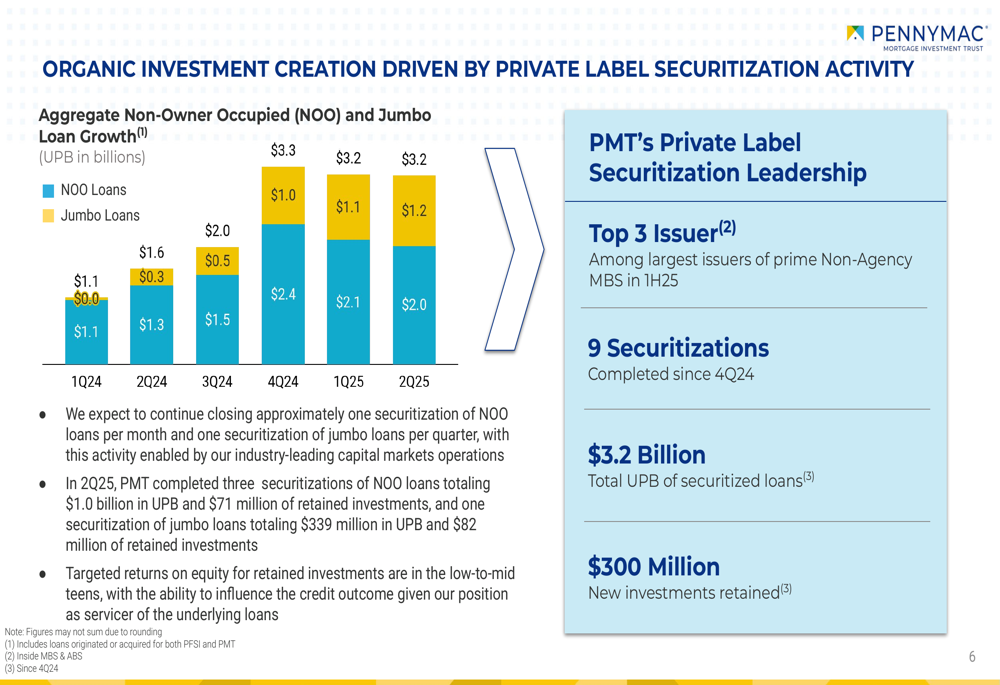

PMT continues to emphasize its private label securitization activity as a key strategic differentiator. The company has positioned itself as a top 3 issuer among the largest issuers of prime Non-Agency MBS in the first half of 2025, completing 9 securitizations since Q4 2024 with a total UPB of $3.2 billion and retaining $300 million in new investments.

The following chart demonstrates the growth in Non-Owner Occupied (NOO) and Jumbo Loan production that drives PMT’s securitization activity:

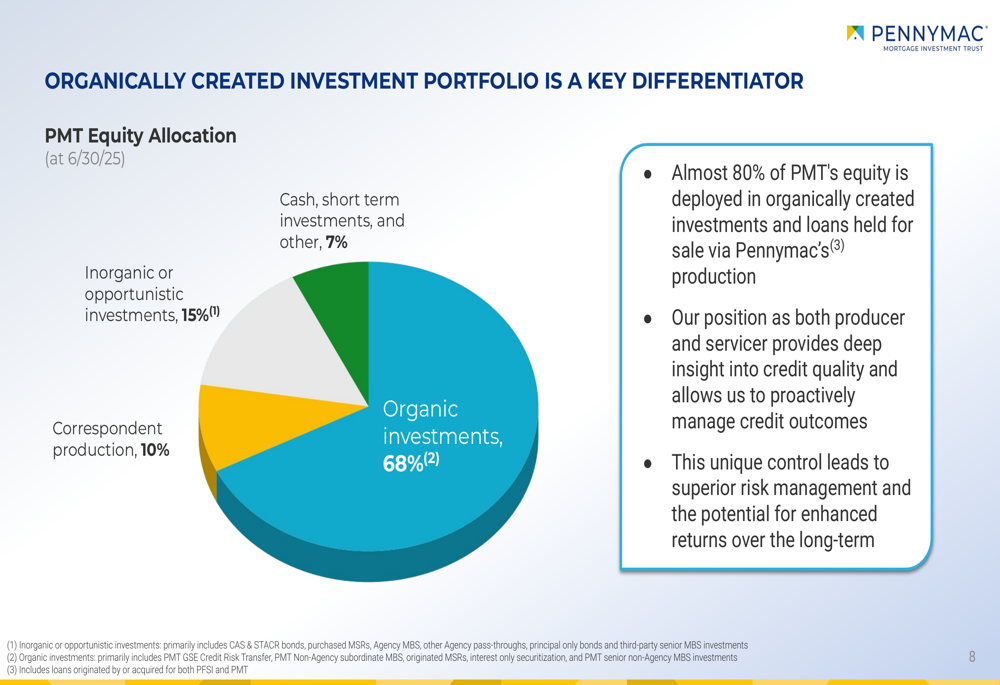

PMT emphasizes that its organically created investment portfolio is a key differentiator in the market. As illustrated in the following equity allocation breakdown, 68% of the company’s equity is deployed in organic investments, with an additional 10% in correspondent production:

The company highlighted its synergistic relationship with PennyMac Financial Services as providing a competitive advantage in a market characterized by consolidation and regulatory changes. This relationship enables PMT to operate as a tax-efficient investment vehicle while leveraging PFSI’s operational platform, multi-channel origination business, and servicing capabilities.

Detailed Financial Analysis

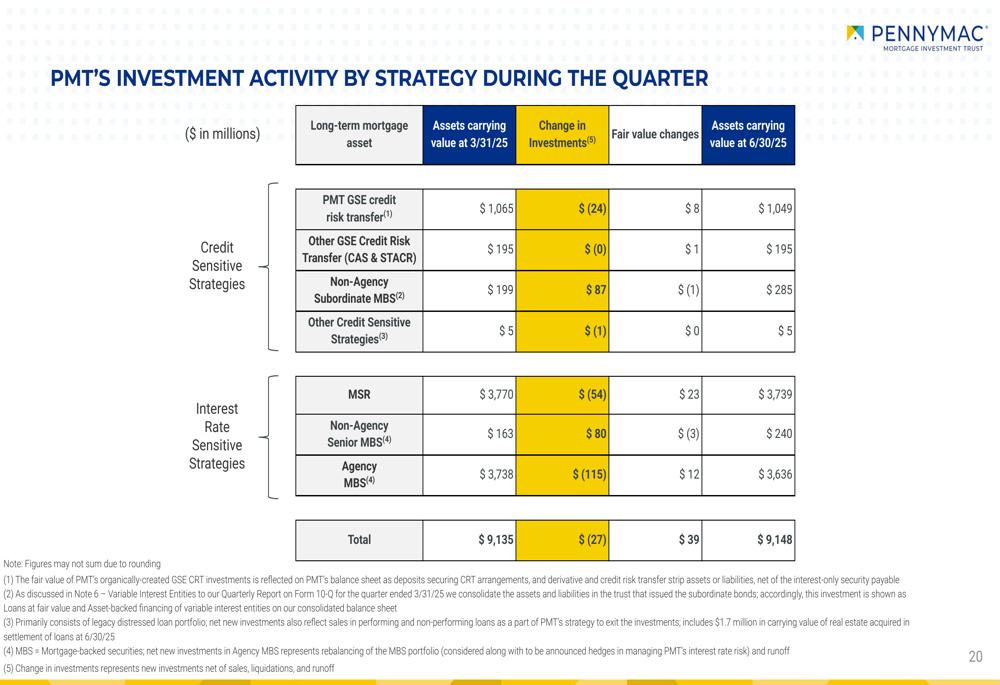

PMT’s investment portfolio consists primarily of mortgage servicing rights (MSRs) and credit risk transfer (CRT) investments. Nearly two-thirds of the company’s shareholders’ equity is deployed to these seasoned investments, which management expects to perform well over the long term despite current challenges.

The following chart shows the company’s investment activity by strategy during the quarter:

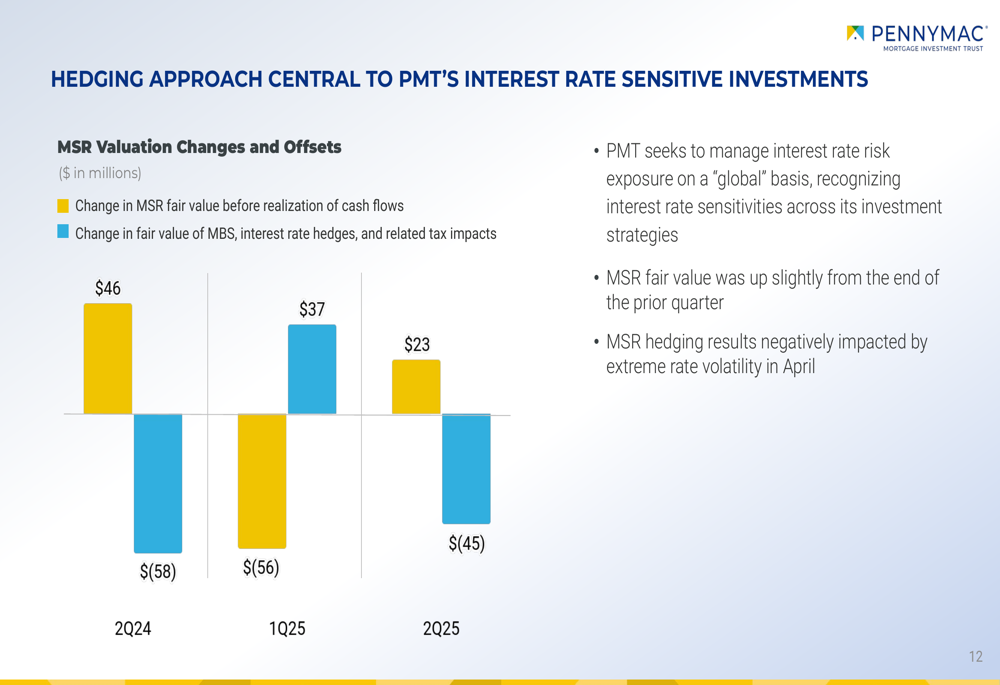

MSR assets were valued at $3.7 billion as of June 30, 2025, down slightly from March 31, 2025. The company’s approach to hedging these interest rate sensitive investments is central to its strategy, though extreme rate volatility in April negatively impacted hedging results:

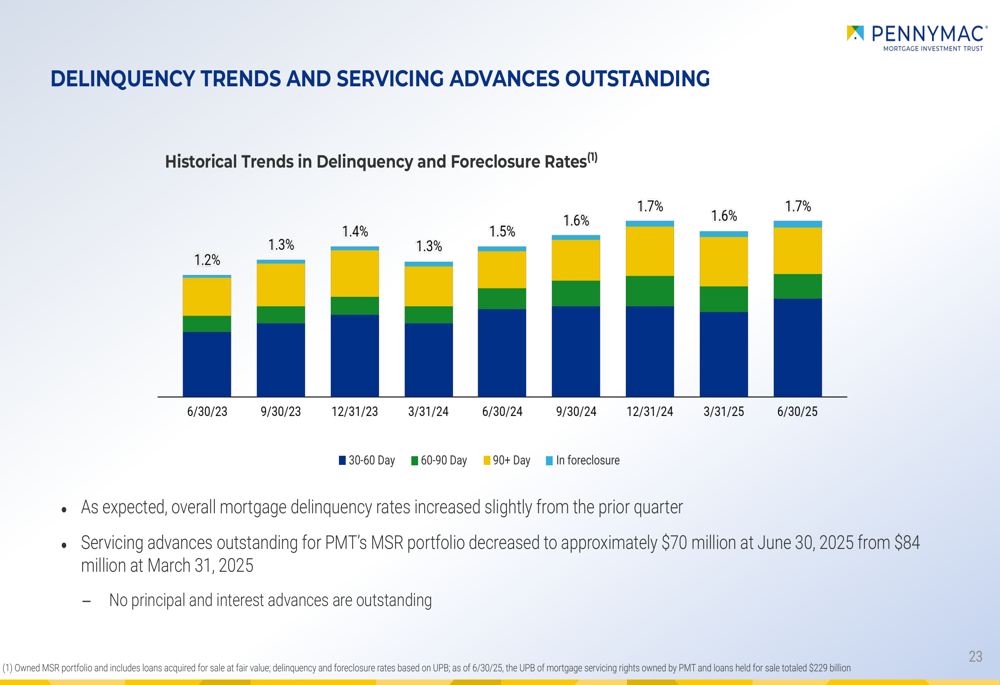

Delinquency rates in PMT’s portfolio increased slightly to 1.7% from 1.6% in the previous quarter, continuing a gradual upward trend:

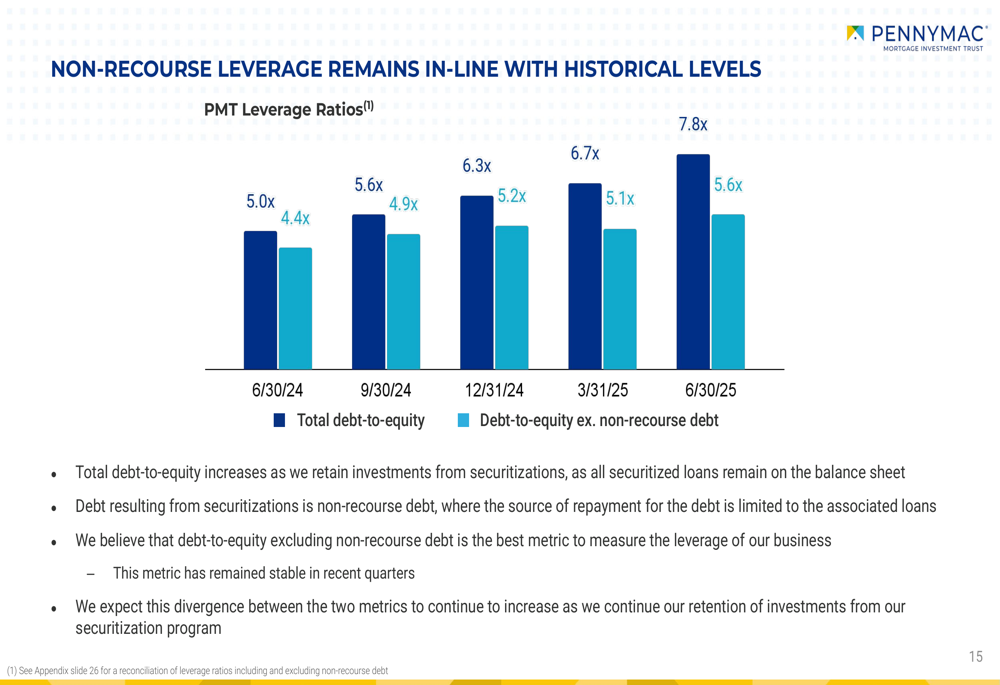

The company’s leverage has increased notably, with total debt-to-equity rising to 7.8x from 6.7x in the previous quarter. Management noted that this increase is partly due to the retention of investments from securitizations, as all securitized loans remain on the balance sheet:

Forward-Looking Statements

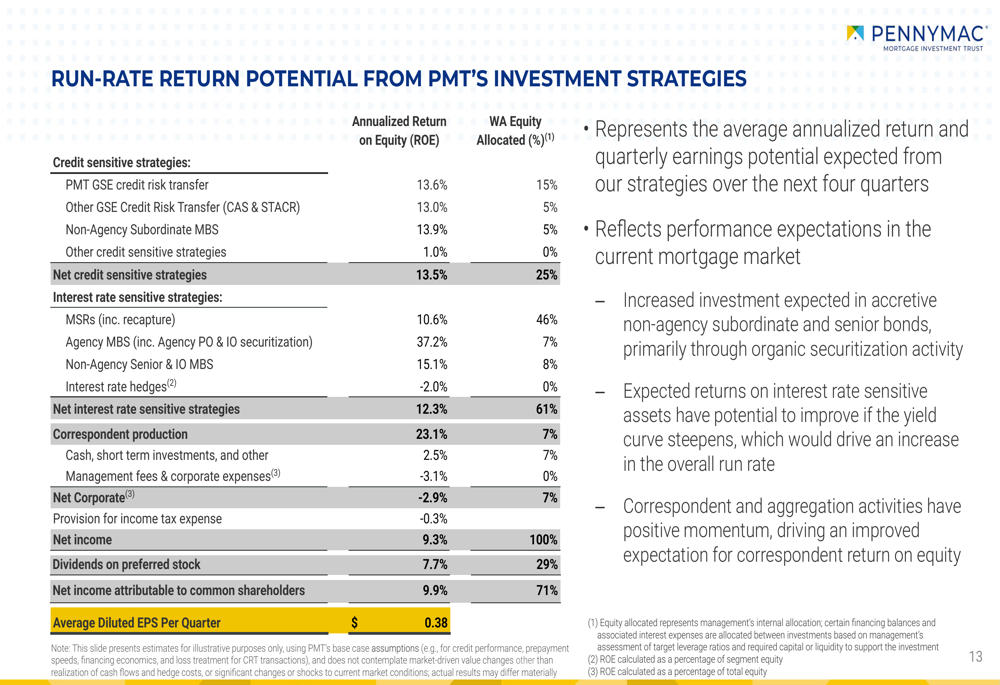

Looking ahead, PMT provided estimates of run-rate return potential from its investment strategies, projecting annualized returns ranging from 10.6% to 13.9% for its major investment categories:

The company expects the U.S. origination market to grow from $1.7 trillion in 2024 to $2.0 trillion in 2025 and $2.3 trillion in 2026, providing opportunities for expansion of its correspondent business. Management continues to emphasize the long-term value of its seasoned investment portfolio, particularly given the low delinquencies and LTV ratios of the underlying mortgages.

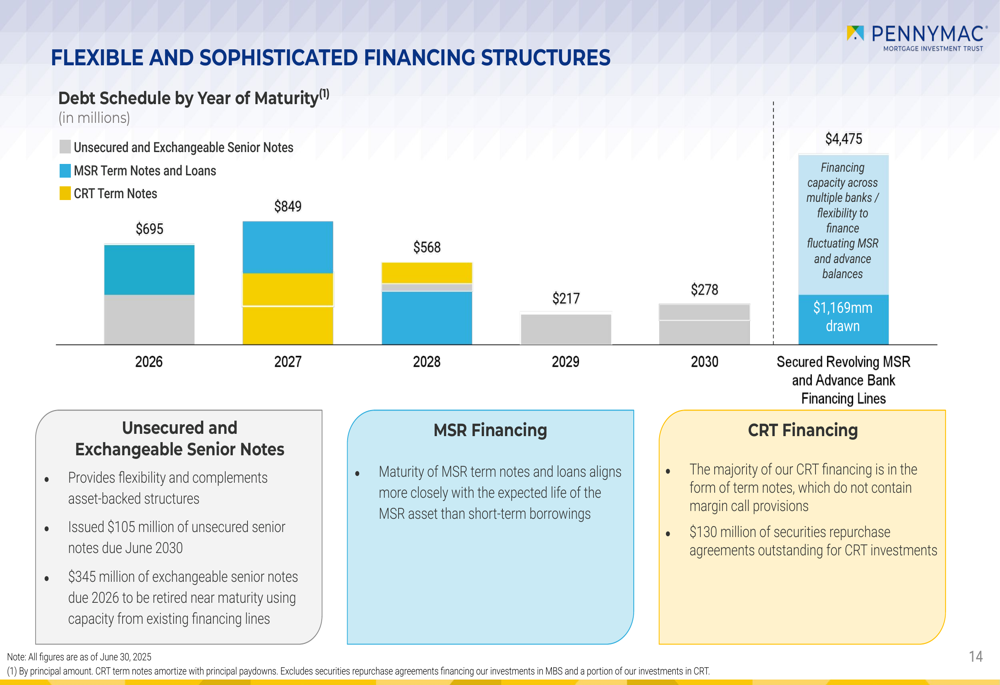

Despite two consecutive quarterly losses, PMT maintains that its flexible financing structures and sophisticated hedging approach position it well for future performance. The company’s debt maturity schedule is designed to align with the expected life of its assets, particularly for MSRs:

While PMT faces ongoing challenges from interest rate volatility and changing market conditions, management remains confident in the company’s strategic positioning and long-term return potential from its diversified investment portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.