Wall St futures flat amid US-China trade jitters; bank earnings in focus

PennyMac Financial Services Inc (NYSE:PFSI) released its second quarter 2025 earnings presentation on July 22, showing a significant rebound from its disappointing first quarter results. The mortgage services company reported net income of $136 million and diluted earnings per share of $2.54, representing a substantial improvement from the $76 million and $1.42 EPS reported in Q1. The stock rose 2.27% to $101.94 during regular trading hours on the day of the announcement.

Quarterly Performance Highlights

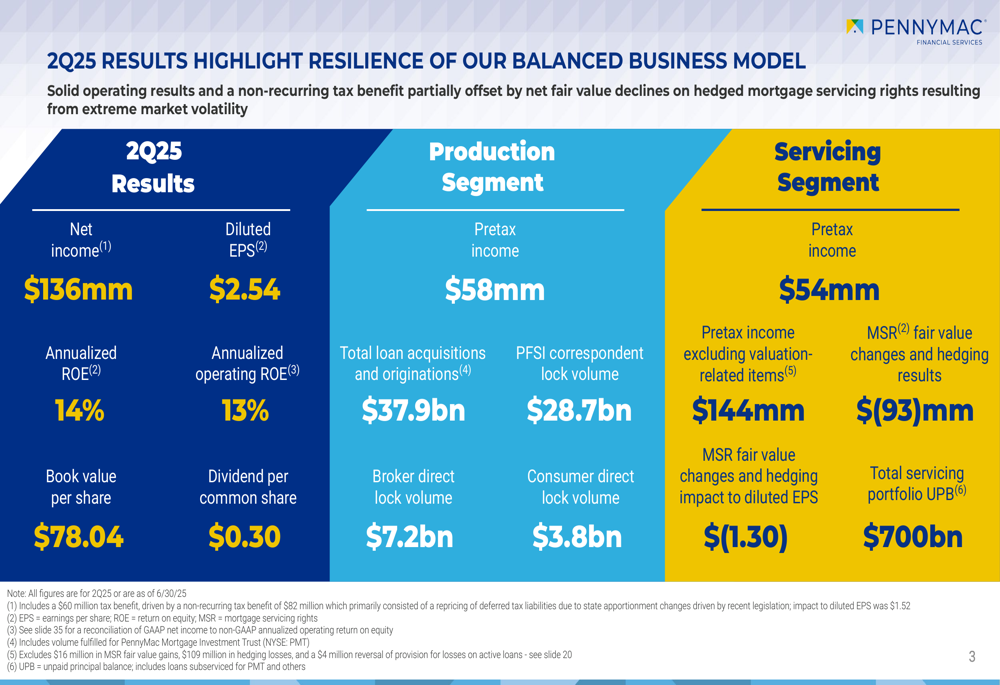

PennyMac’s Q2 results demonstrated the resilience of its balanced business model, with net income of $136 million including a $60 million tax benefit (equivalent to $1.52 EPS). The company achieved an annualized return on equity of 14% and an operating ROE of 13%, with book value per share reaching $78.04.

As shown in the following comprehensive results summary, PennyMac maintained strong performance across both its production and servicing segments:

The company’s production segment generated pretax income of $58 million on total loan acquisitions and originations of $37.9 billion. This represents a significant increase from the $28.9 billion reported in Q1 2025. Meanwhile, the servicing segment contributed pretax income of $54 million, with pretax income excluding valuation-related items reaching $144 million.

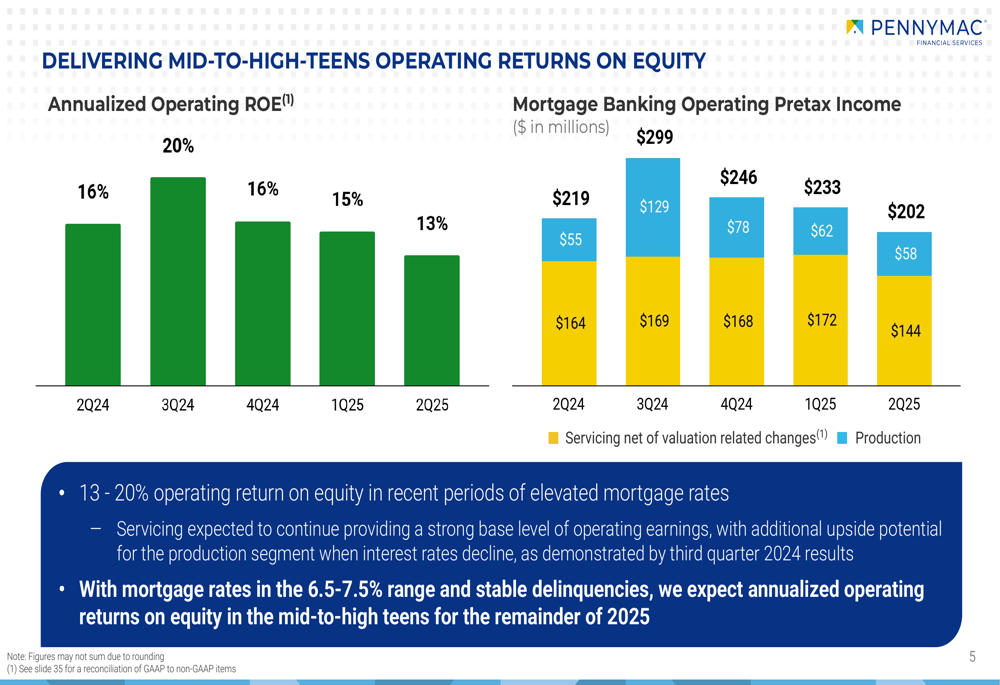

PennyMac has maintained consistent operating returns on equity in the mid-teens range over the past five quarters, despite fluctuations in mortgage banking pretax income:

"We expect annualized operating returns on equity in the mid-to-high teens for the remainder of 2025, assuming mortgage rates stay in the 6.5-7.5% range and delinquencies remain stable," the company stated in its presentation.

Servicing and Production Segment Analysis

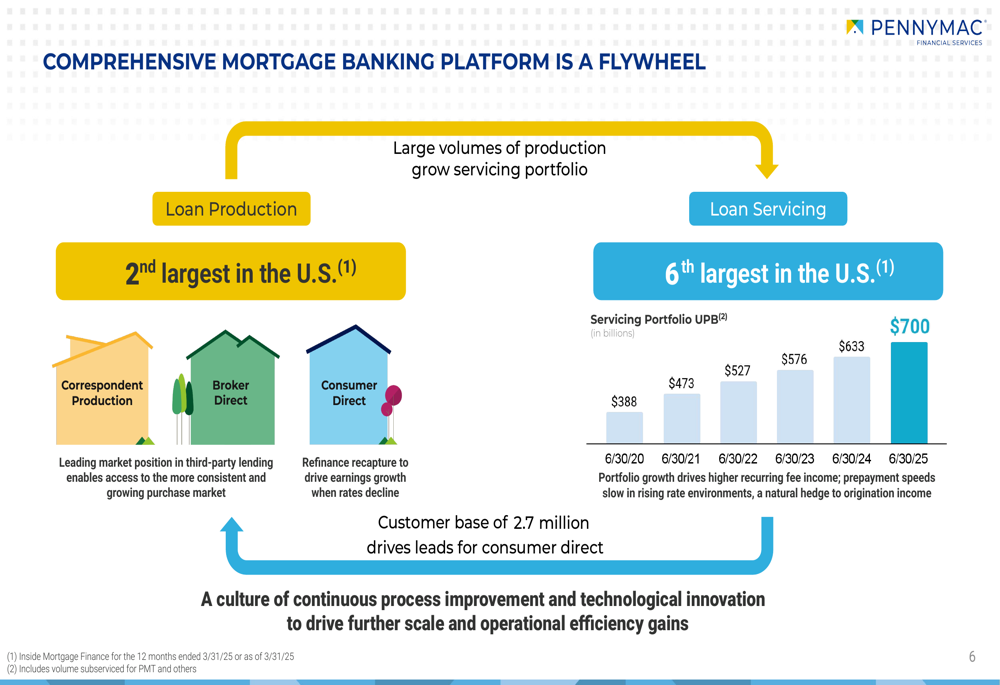

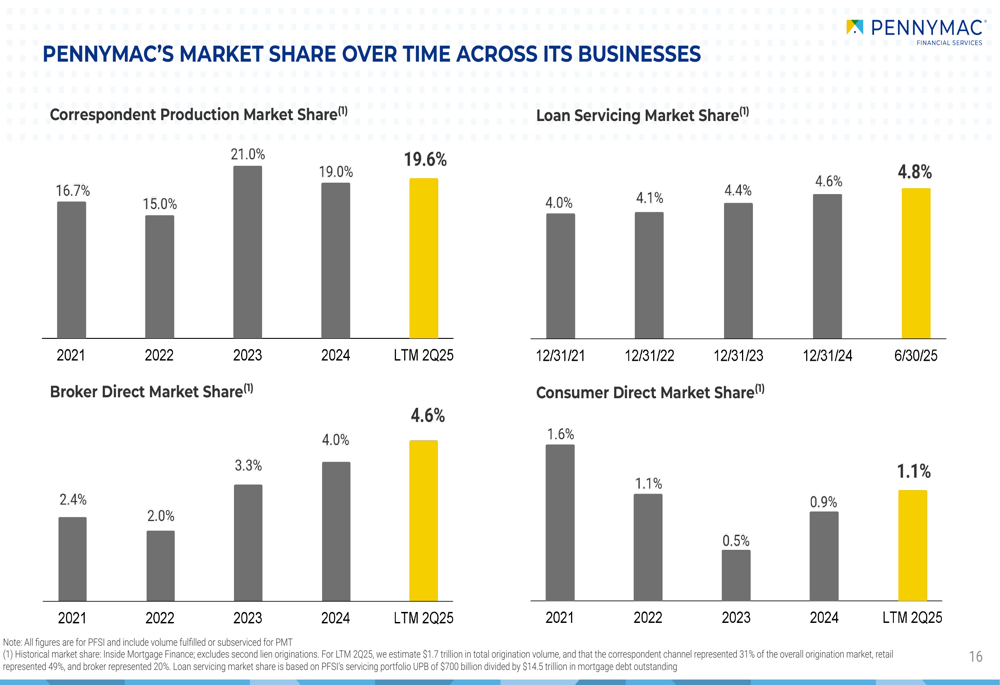

PennyMac’s servicing portfolio reached a milestone of $700 billion in unpaid principal balance (UPB) as of June 30, 2025, continuing its steady growth trajectory from $388 billion in 2020. The company maintains its position as the 6th largest servicer in the U.S. with a market share of 4.8%.

The company’s business model operates as a flywheel, with loan production feeding into loan servicing, which in turn generates leads for consumer direct originations:

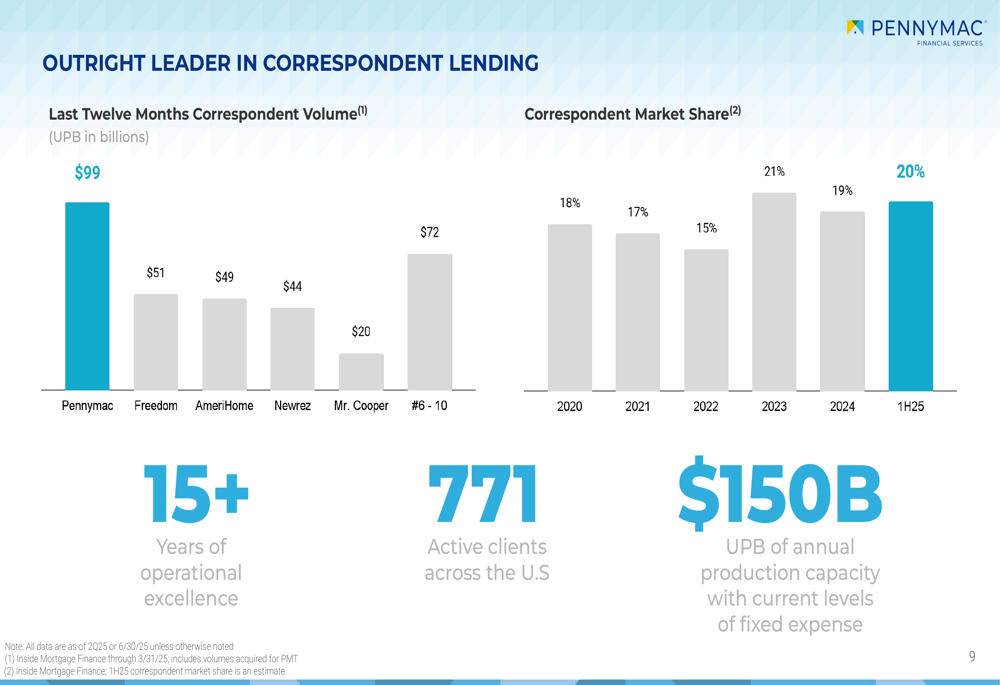

In the production segment, PennyMac continues to be an outright leader in correspondent lending with $99 billion in volume over the last twelve months and 771 active clients across the U.S. The company maintains a 19.6% market share in this channel:

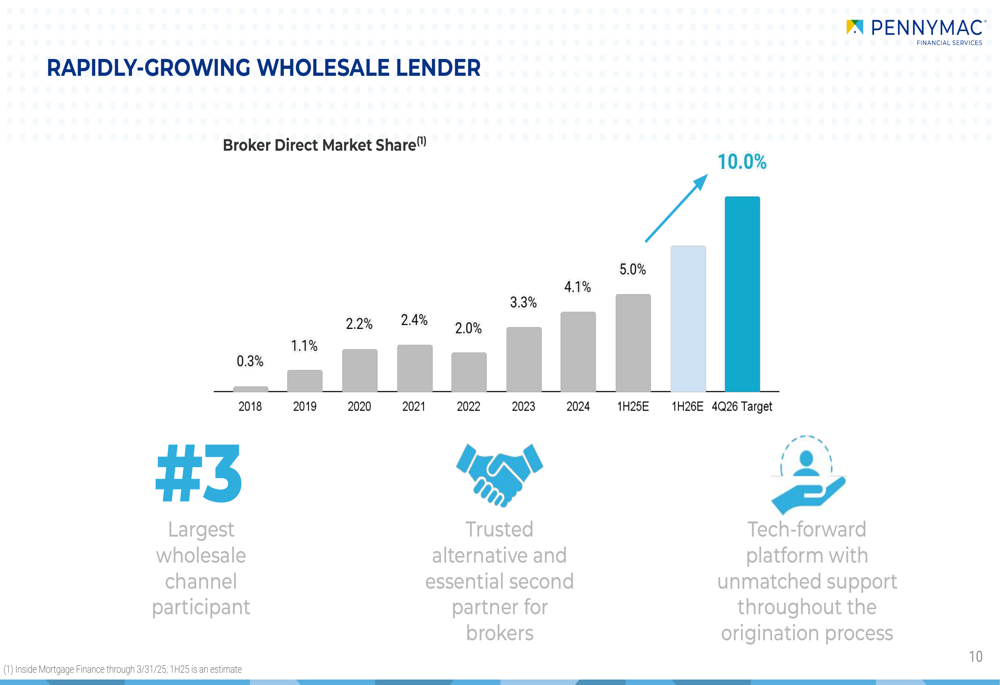

Particularly notable is PennyMac’s rapid growth in the wholesale lending channel, where its broker direct market share has increased from 0.3% in 2018 to 5.0% in the first half of 2025, with an ambitious target of reaching 10% by the first half of 2026:

Strategic Initiatives

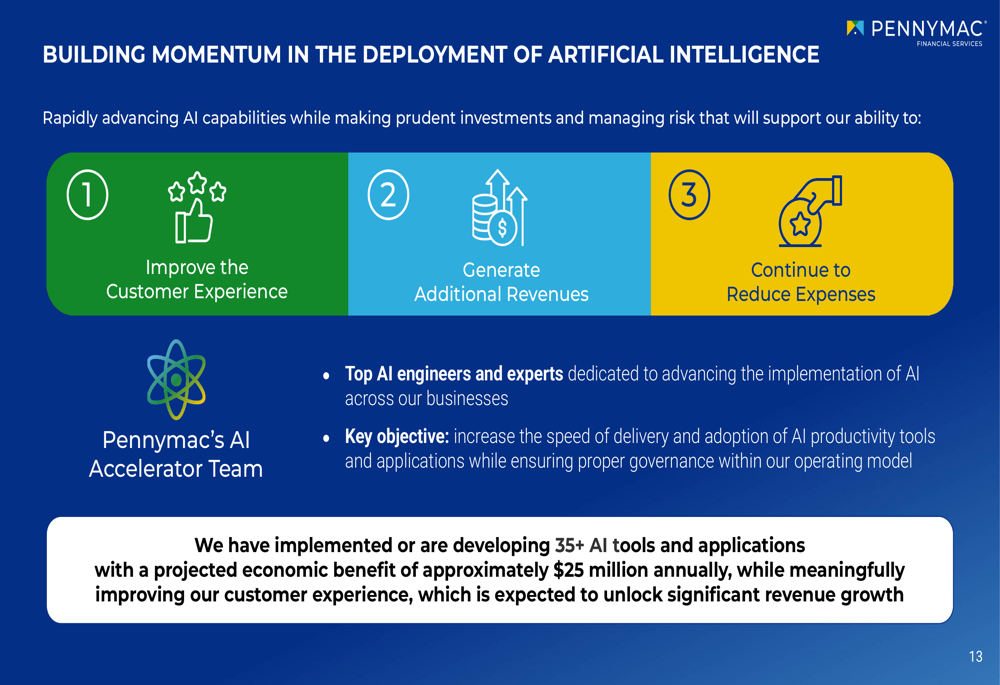

PennyMac is placing significant emphasis on artificial intelligence as a key driver of future growth and efficiency. The company is focusing on rapidly advancing AI capabilities to improve customer experience, generate additional revenues, and continue to reduce expenses.

The presentation highlights the company’s comprehensive AI strategy:

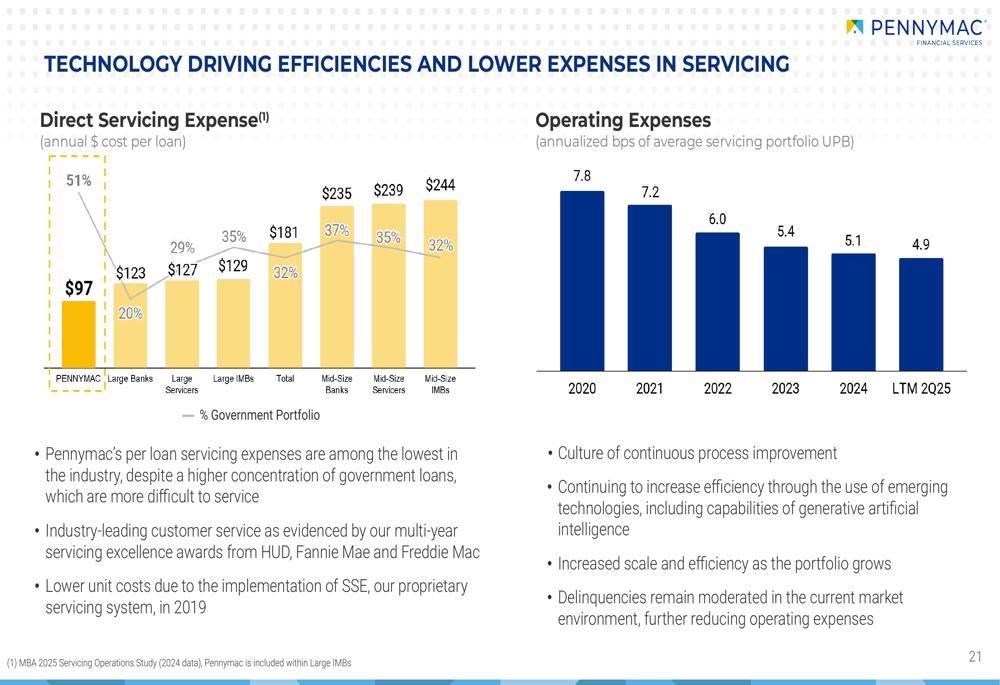

"We have implemented or are developing 35+ AI tools and applications with a projected economic benefit of $25 million annually," the company noted in its presentation. This focus on technology is also driving efficiencies in servicing, with operating expenses as a percentage of the average servicing portfolio UPB declining from 7.8 basis points in 2020 to 4.9 basis points in the last twelve months ending Q2 2025:

Financial Strength and Balance Sheet

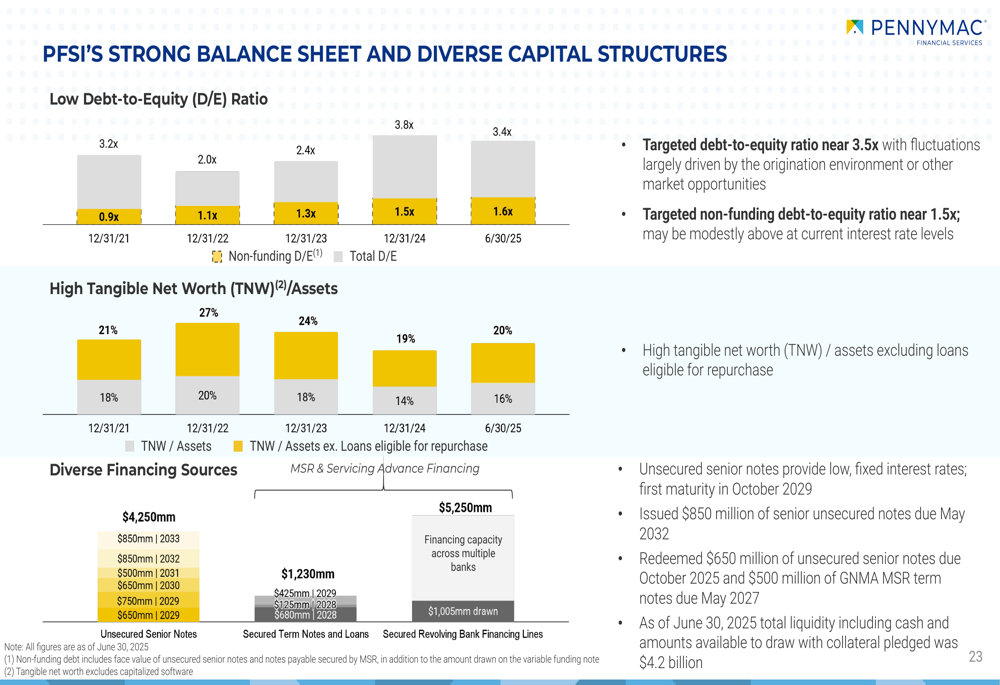

PennyMac emphasized its strong balance sheet and diverse capital structure, maintaining a low debt-to-equity ratio and high tangible net worth to assets ratio:

The company targets a debt-to-equity ratio near 3.5x with fluctuations largely driven by the origination environment or other market opportunities. Its non-funding debt-to-equity ratio target is near 1.5x, though it may be modestly above at current interest rate levels.

Forward-Looking Statements

Looking ahead, PennyMac expects to continue delivering mid-to-high teens operating returns on equity for the remainder of 2025. The company’s market share trends across its businesses show steady growth or stability in correspondent production, broker direct, loan servicing, and consumer direct channels:

The U.S. mortgage origination market is forecast to grow from $1.7 trillion in 2024 to $2.0 trillion in 2025 and $2.2 trillion in 2026, providing a favorable backdrop for PennyMac’s growth ambitions, particularly in the purchase market which now represents 90% of correspondent acquisitions and 81% of broker direct originations.

The Q2 results represent a significant improvement from Q1 2025, when the company missed analyst expectations with EPS of $1.42 compared to the forecasted $2.78. The rebound in performance, coupled with the company’s strategic focus on AI and technology, appears to have resonated positively with investors, as evidenced by the stock’s 2.27% gain on the day of the announcement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.