Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Perimeter Solutions SA (NYSE:PRM) released its first quarter 2025 earnings presentation on May 8, 2025, revealing a 22% year-over-year revenue increase and a return to profitability. The company, which specializes in fire safety products and specialty chemicals, demonstrated significant improvement in its core Fire Safety segment while maintaining its strategic focus on value creation.

The results come as Perimeter Solutions continues to build on momentum from its strong performance in 2024, when it reported 74% annual sales growth. The stock closed at $10.25 on May 7, 2025, down 2.57% for the day, and currently trades well below its 52-week high of $14.44.

Quarterly Performance Highlights

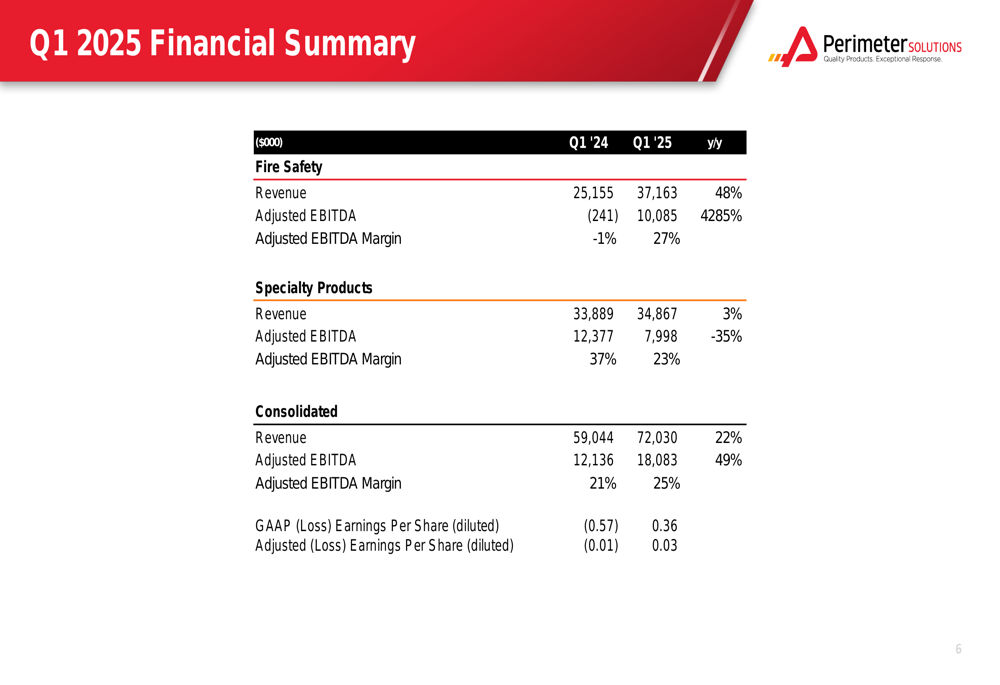

Perimeter Solutions reported consolidated revenue of $72.0 million for Q1 2025, up 22% from $59.0 million in the same period last year. Adjusted EBITDA showed even stronger growth, increasing 49% to $18.1 million, with margins expanding from 21% to 25%.

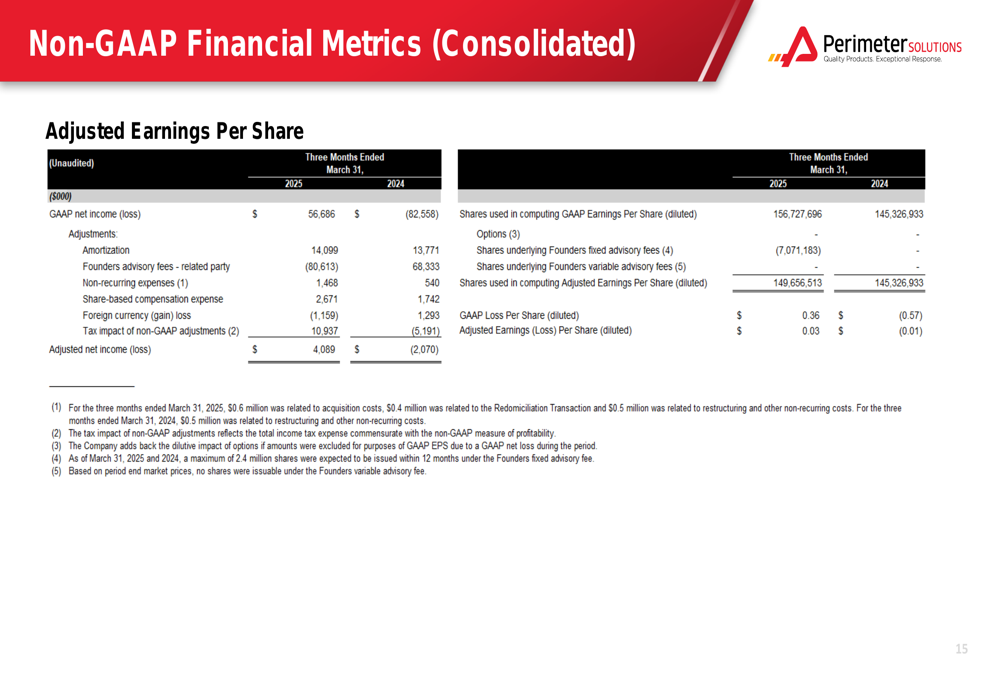

The company’s return to profitability was evident in its earnings per share figures, with GAAP EPS improving dramatically from -$0.57 in Q1 2024 to $0.36 in Q1 2025. Adjusted EPS also turned positive, reaching $0.03 compared to -$0.01 in the prior year period.

As shown in the following financial summary from the company’s presentation:

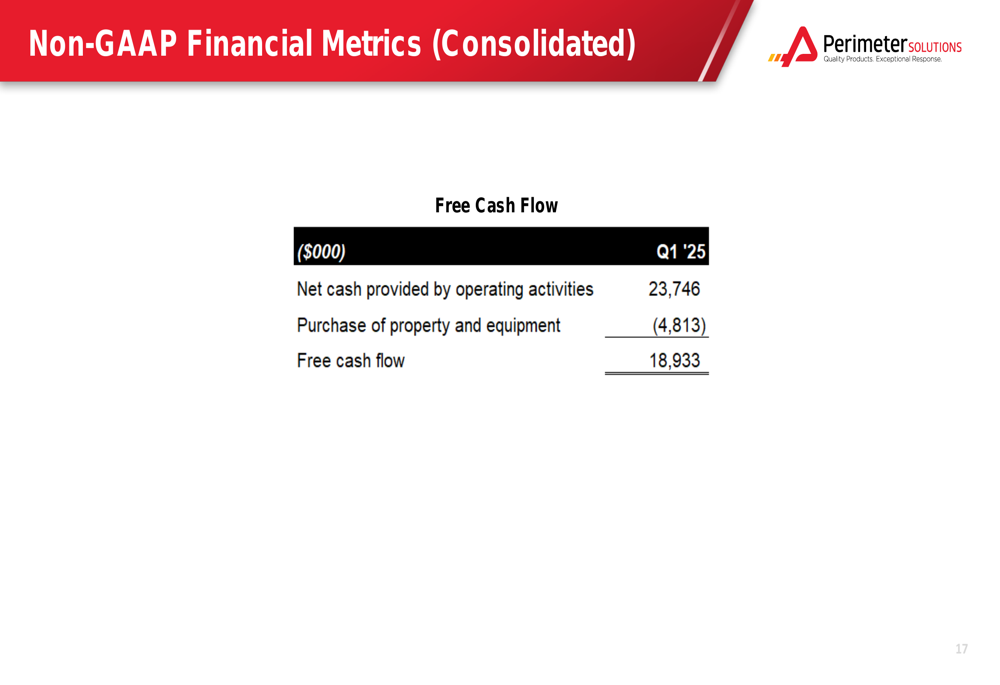

Free cash flow for the quarter reached $18.9 million, calculated as $23.7 million in net cash from operating activities minus $4.8 million in capital expenditures. This represents a solid cash generation performance that supports the company’s capital allocation strategy.

Segment Performance Analysis

The Fire Safety segment was the primary driver of growth, with revenue surging 48% to $37.2 million compared to $25.2 million in Q1 2024. More impressively, the segment’s Adjusted EBITDA swung from a $0.2 million loss to a $10.1 million profit. This dramatic improvement reflects the company’s strong market position in fire retardants and suppressants.

In contrast, the Specialty Products segment showed more modest revenue growth of 3%, increasing from $33.9 million to $34.9 million. However, Adjusted EBITDA for this segment declined 35% to $8.0 million from $12.4 million in the prior year period, indicating potential margin pressure or increased costs in this business line.

The company’s operational focus spans across four key areas as illustrated in the presentation:

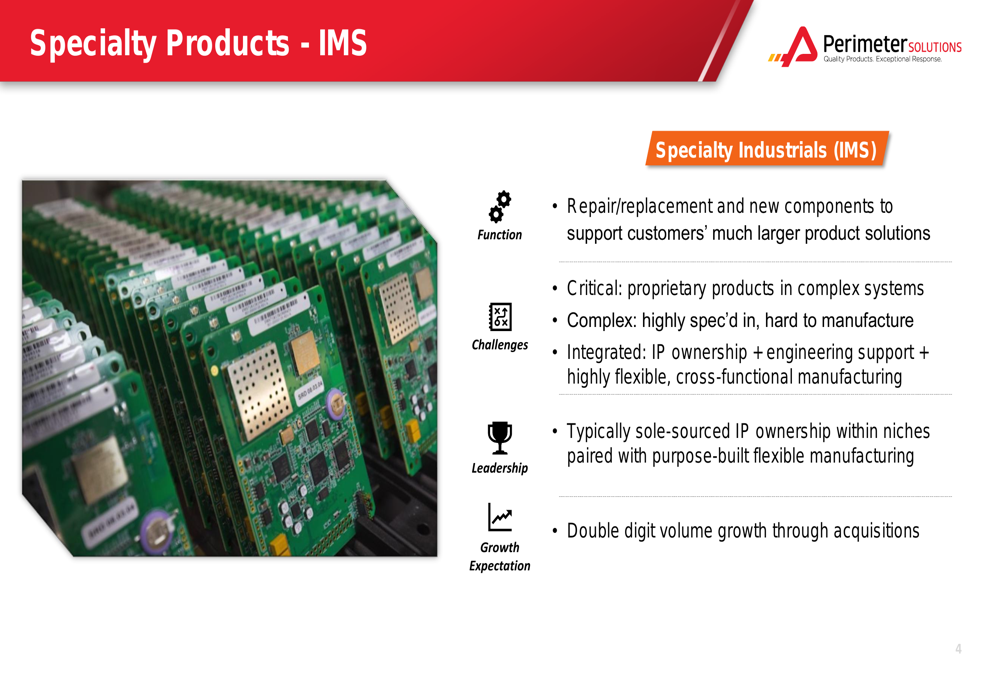

Perimeter Solutions continues to emphasize its Specialty Industrials (IMS) products, which provide critical components for complex systems. The company highlighted that these products are typically sole-sourced with proprietary IP and supported by purpose-built flexible manufacturing capabilities. Management expects double-digit volume growth through acquisitions in this segment.

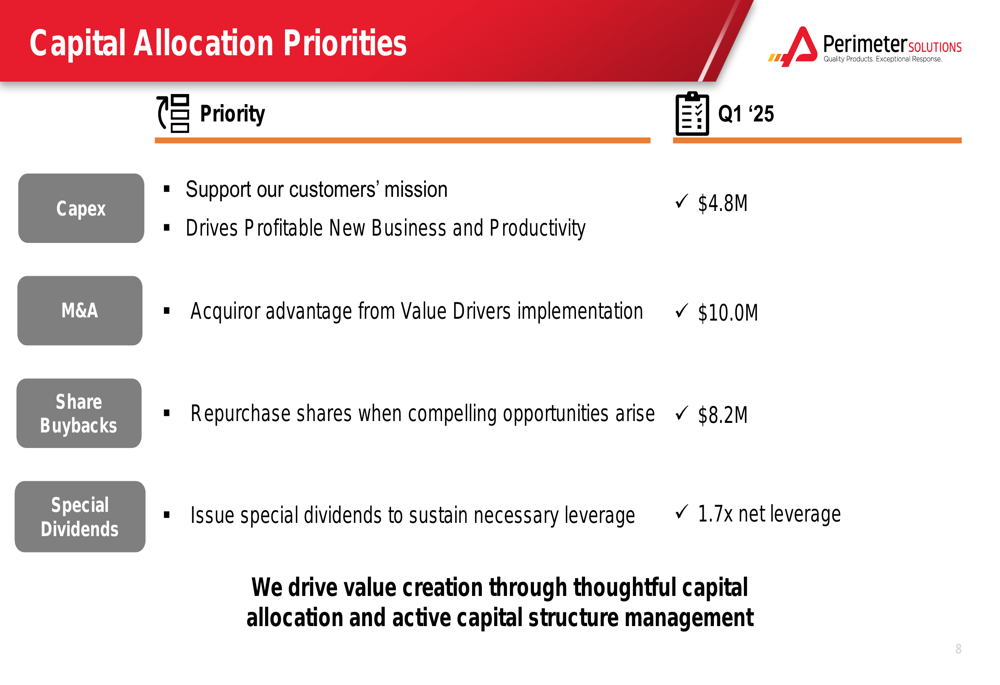

Balance Sheet and Capital Allocation

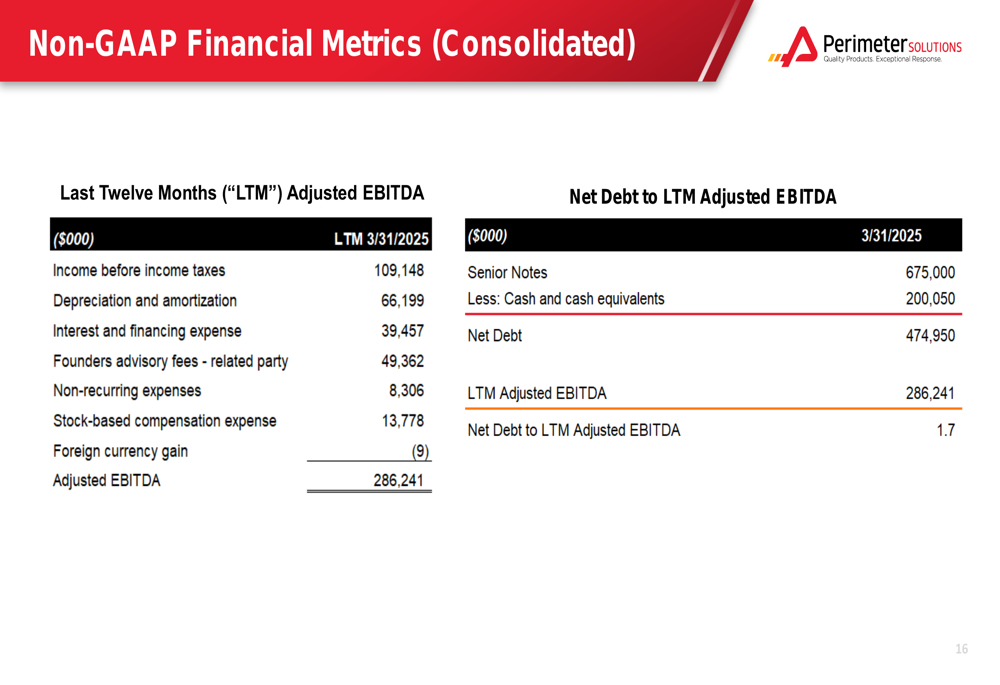

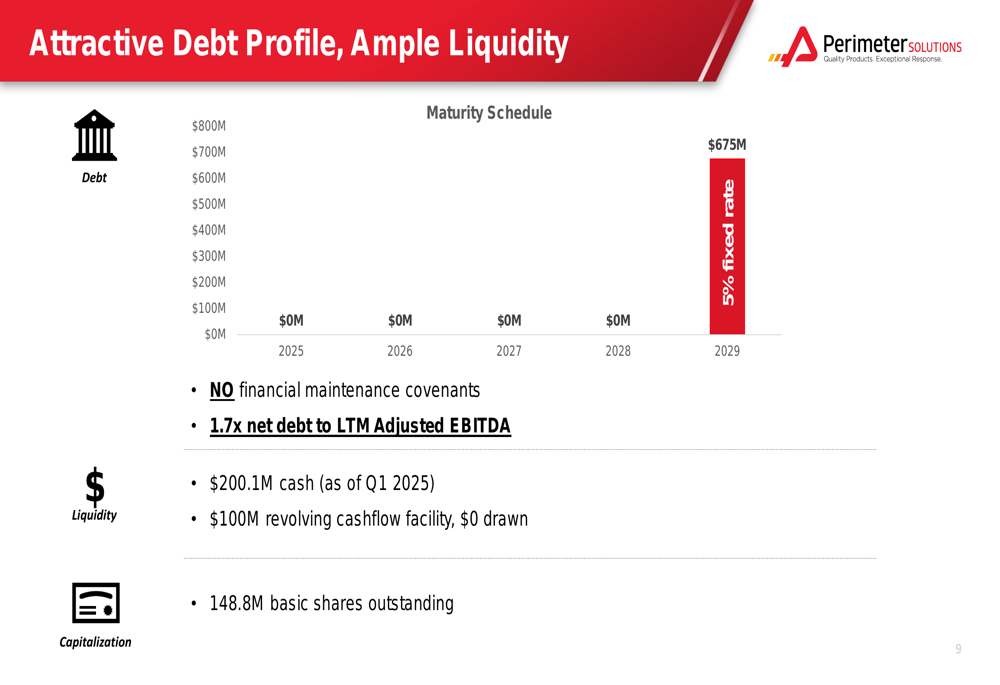

Perimeter Solutions maintains a healthy balance sheet with a net debt to LTM Adjusted EBITDA ratio of 1.7x, well below the industry average. The company reported $200.1 million in cash as of Q1 2025 and has an undrawn $100 million revolving credit facility, providing ample liquidity for operations and strategic initiatives.

The debt profile is attractive with a single $675 million maturity in 2029 at a 5% fixed rate and no financial maintenance covenants, giving the company significant financial flexibility.

Perimeter Solutions’ capital allocation strategy focuses on four key areas: capital expenditures, mergers and acquisitions, share buybacks, and special dividends. During Q1 2025, the company allocated $4.8 million to capex, $10.0 million to M&A activities, and $8.2 million to share repurchases.

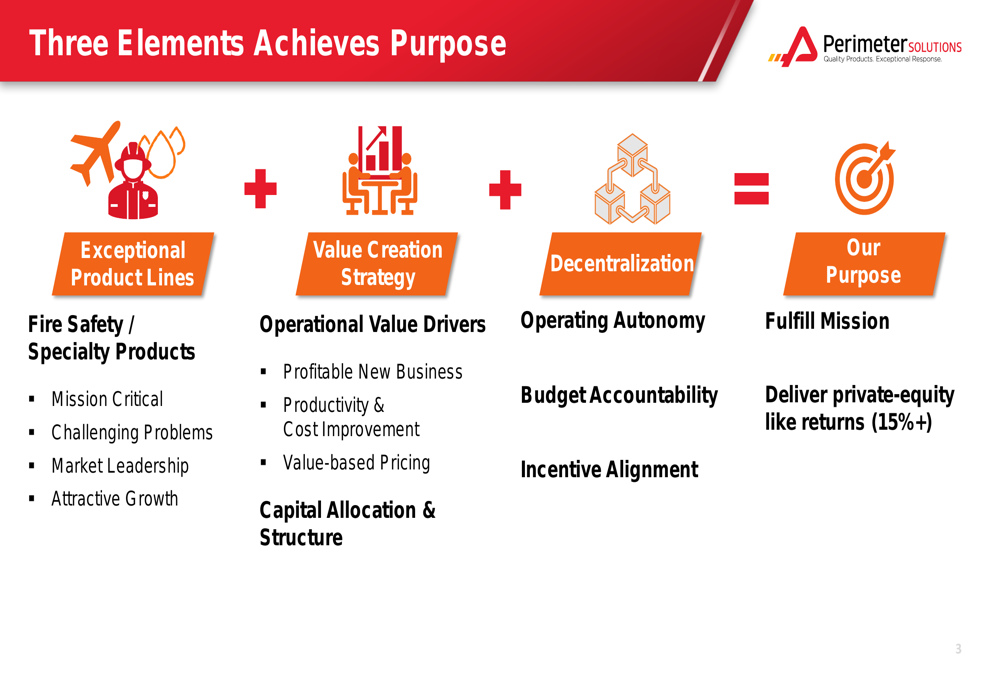

Strategic Initiatives and Forward-Looking Statements

The company’s strategic framework centers around three key elements: exceptional product lines, value creation strategies, and decentralization. Management aims to deliver "private-equity like returns" of 15%+ while fulfilling its mission of providing trusted solutions that save lives.

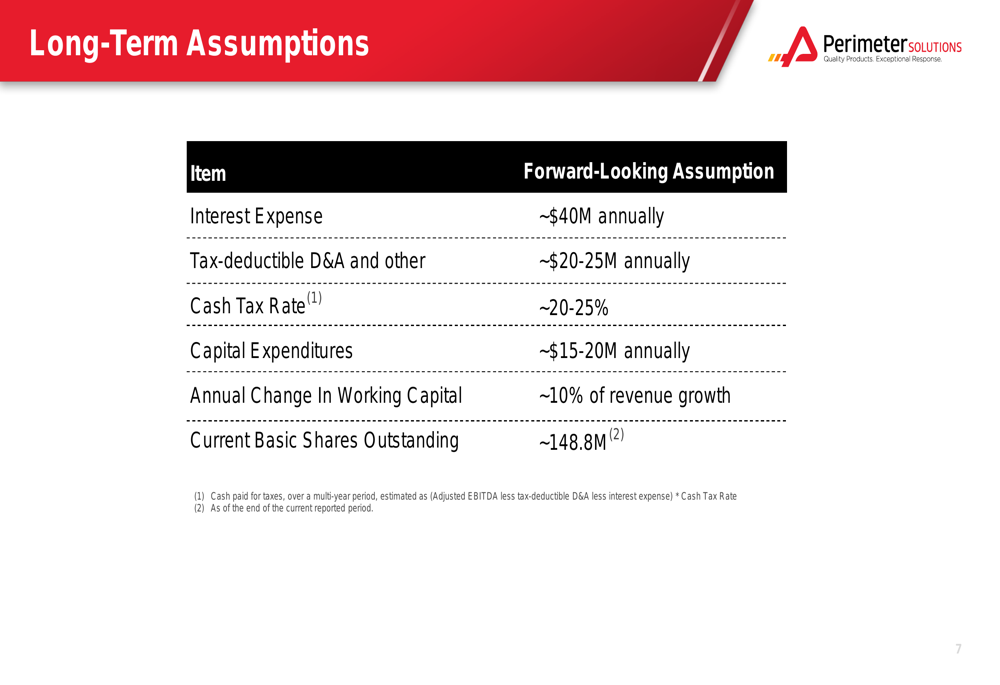

Looking ahead, Perimeter Solutions provided several long-term financial assumptions, including approximately $40 million in annual interest expense, $20-25 million in tax-deductible depreciation and amortization, a 20-25% cash tax rate, and $15-20 million in annual capital expenditures. The company also expects working capital to increase by approximately 10% of revenue growth.

The adjusted EPS calculation provides additional insight into the company’s performance, showing significant improvement from the prior year period. The reconciliation highlights the impact of amortization, founders advisory fees, and other non-recurring expenses on the company’s GAAP results.

While Perimeter Solutions delivered strong results for Q1 2025, investors will be watching closely to see if the company can maintain this momentum throughout the year, particularly in the Specialty Products segment where performance was mixed. The company’s continued focus on strategic acquisitions and operational efficiency improvements will be key factors in its ability to deliver on its long-term growth and profitability targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.