United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Perseus Mining Ltd (ASX:PRU) presented its March 2025 quarter results on April 30, highlighting continued financial strength despite some operational challenges. The gold producer, which operates three mines across West Africa, has capitalized on elevated gold prices while advancing two significant growth projects.

The company’s stock has performed well recently, with shares trading at $3.33 as of April 29, 2025, up 3.1% on the day and approaching its 52-week high of $3.61.

Quarterly Performance Highlights

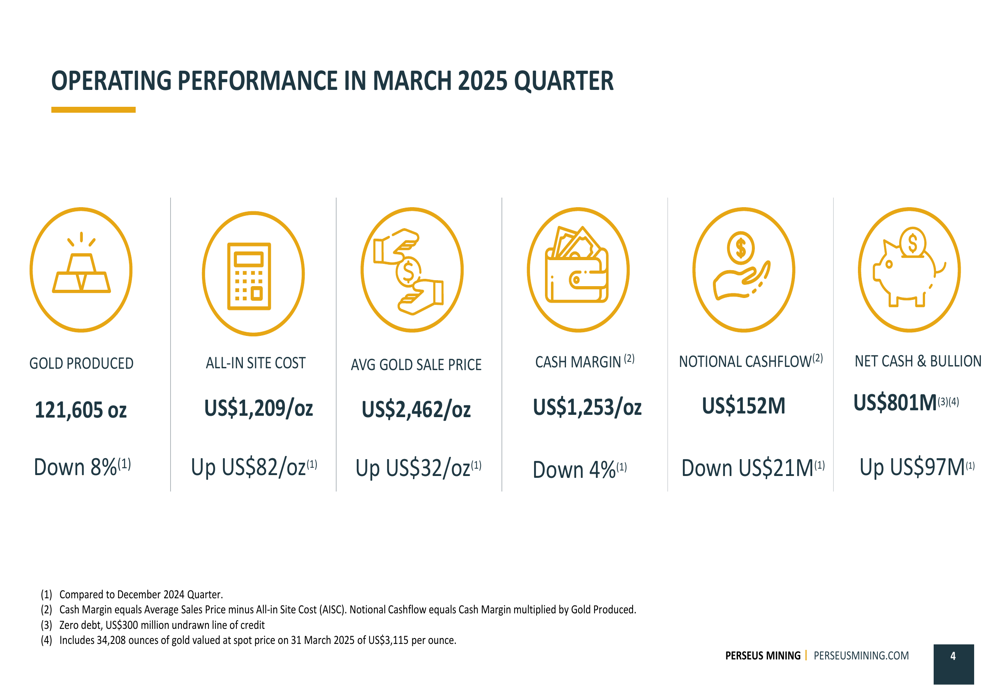

Perseus produced 121,605 ounces of gold during the quarter, representing an 8% decrease compared to the December 2024 quarter. Despite this production dip, the company’s financial position strengthened due to higher gold prices.

As shown in the following quarterly performance summary:

The average gold sale price rose to US$2,462 per ounce, up US$32 from the previous quarter. However, the all-in site cost increased by US$82 to US$1,209 per ounce, resulting in a cash margin of US$1,253 per ounce, down 4%. Despite the margin compression, Perseus generated notional cashflow of US$152 million.

Production and performance varied significantly across Perseus’s three operating mines:

- Yaouré (Côte d’Ivoire): The standout performer, contributing 68,822 ounces (57% of total production), with an all-in site cost of US$981 per ounce, down US$56 from the previous quarter. The mine generated US$99 million in cashflow.

- Edikan (Ghana): Produced 41,668 ounces (34% of total), down 15% quarter-on-quarter, with costs rising 15% to US$1,177 per ounce. Despite cost increases, the mine contributed US$57 million in cashflow.

- Sissingué (Côte d’Ivoire): The weakest performer, producing 11,115 ounces (9% of total), down 34% from the previous quarter with high costs of US$2,736 per ounce, resulting in a negative cash margin and US$4 million cash outflow.

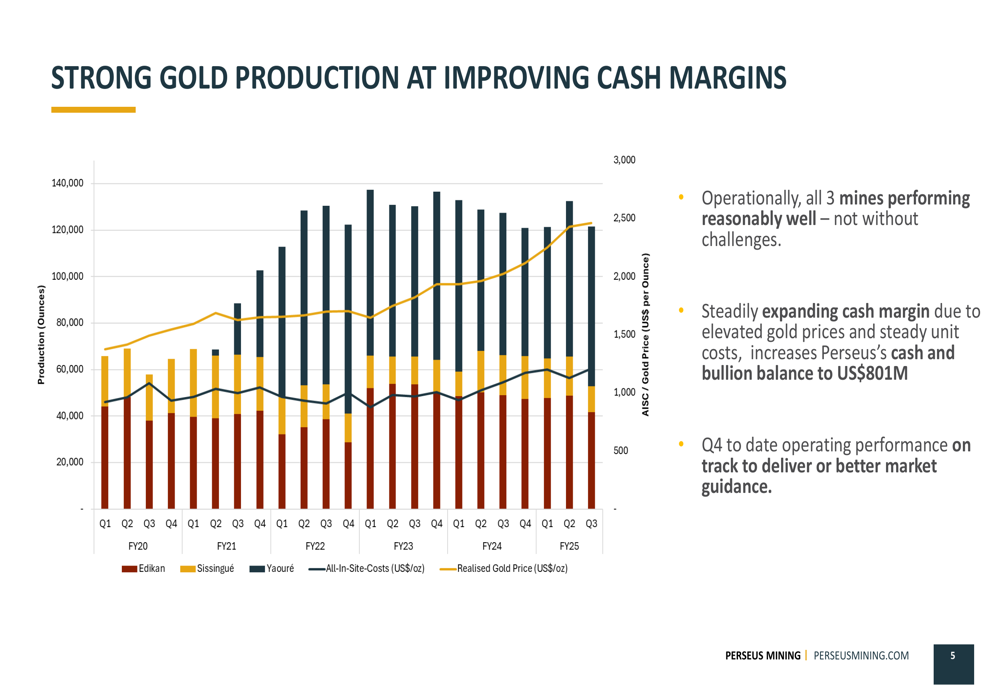

The company’s production and cost trends over recent years show the impact of higher gold prices on overall margins:

Detailed Financial Analysis

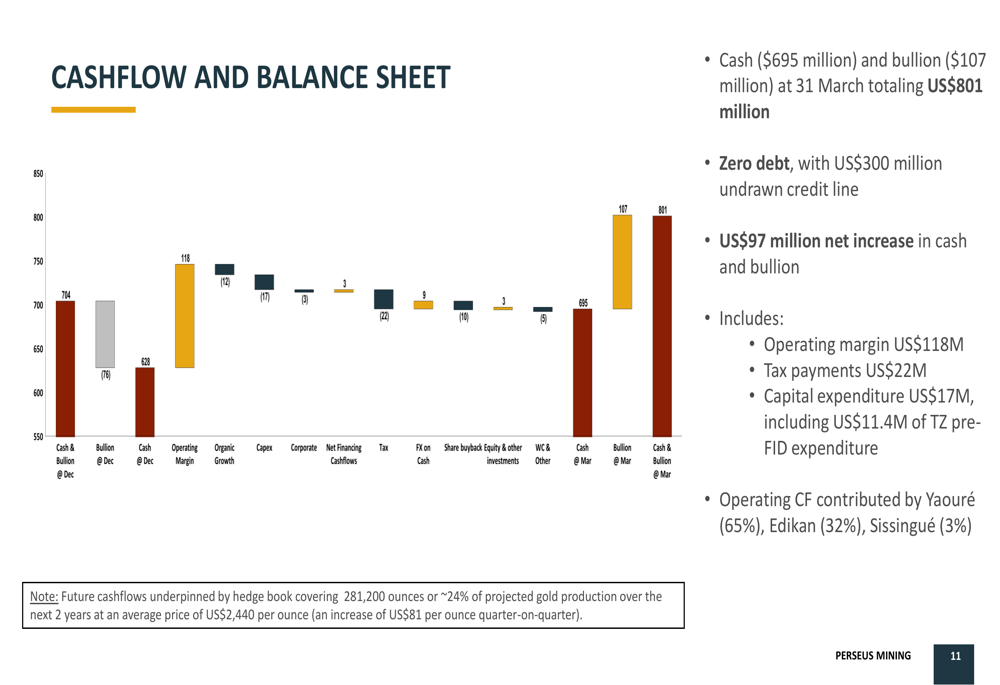

Perseus’s financial position continued to strengthen during the quarter, with net cash and bullion increasing by US$97 million to reach US$801 million. The company remains debt-free and maintains a US$300 million undrawn credit facility.

The following cashflow waterfall chart illustrates the components of the company’s financial performance:

Operating margins contributed US$118 million, partially offset by tax payments of US$22 million and capital expenditures of US$17 million. By operation, Yaouré contributed 65% of operating cashflow, Edikan 32%, and Sissingué just 3%.

Perseus continues to implement its hedging strategy to provide downside protection for approximately 24% of gold production over the next three years. The company has shifted toward zero-cost collars for new hedges, with current positions covering 46,200 ounces for FY25, 105,000 ounces for FY26, 25,000 for FY27, and 5,000 for FY28.

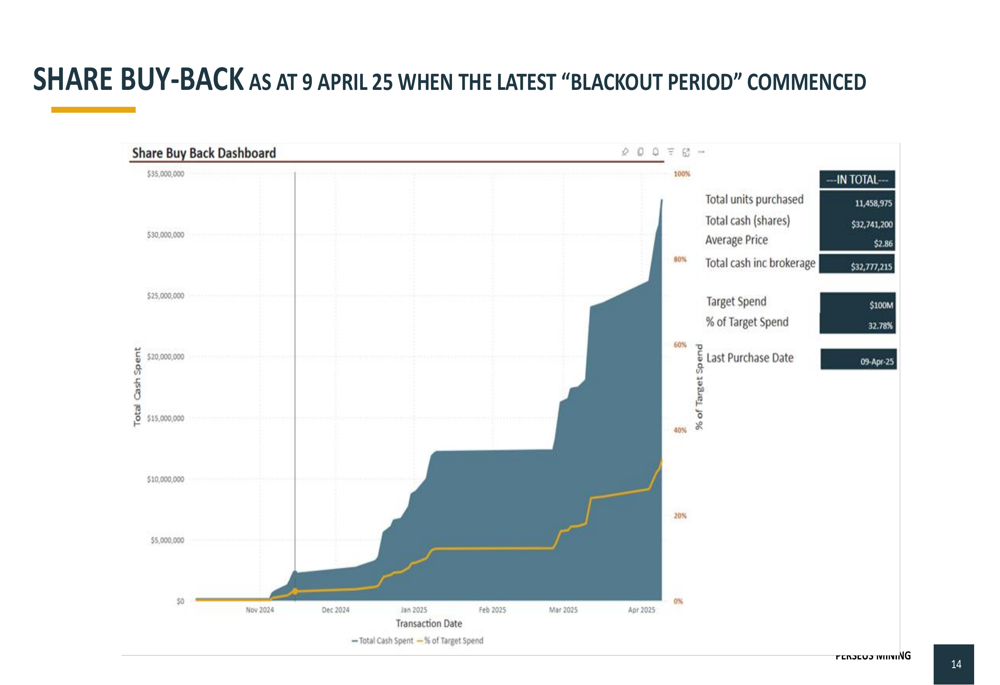

The share buyback program is progressing steadily, with 11,458,975 shares repurchased at an average price of $2.86, representing nearly 33% of the $100 million target allocation:

Strategic Growth Initiatives

Perseus is advancing two major growth projects that will significantly expand its production profile in the coming years.

The CMA Underground Mine Development at Yaouré received final investment decision approval in January 2025, with work scheduled to begin on July 1, 2025. Byrnecut has been selected as the primary contractor. The project contains significant resources:

"Measured and Indicated Mineral Resource is 55.6 Mt grading 1.52 g/t Au, containing 2.7 Moz of gold including 7.4 Mt grading 4.16 g/t Au, containing 0.966 Moz of gold," the company stated, adding that "Ore Reserves estimated at 35.2 Mt grading 1.53 g/t Au, containing 1.73 Moz of gold including 4.5 Mt at 3.52 g/t for 0.51 Moz."

The underground development is expected to extend Yaouré’s mine life until 2035.

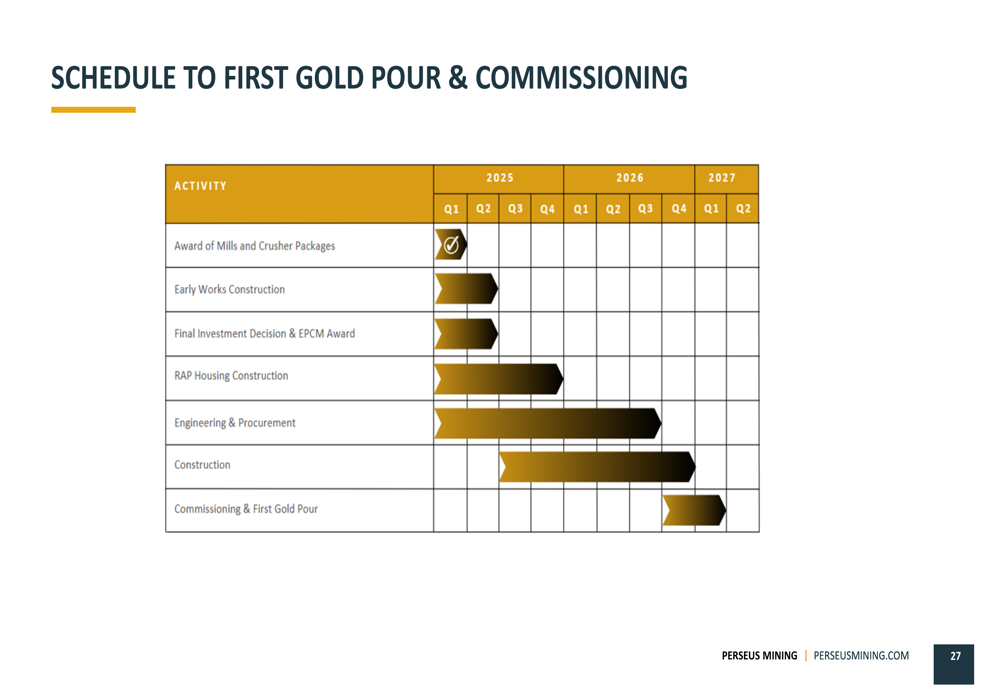

The Nyanzaga Gold Project in Tanzania represents Perseus’s most significant growth initiative. The company took the final investment decision after the end of the quarter, with development and pre-production capital costs estimated at US$523.1 million.

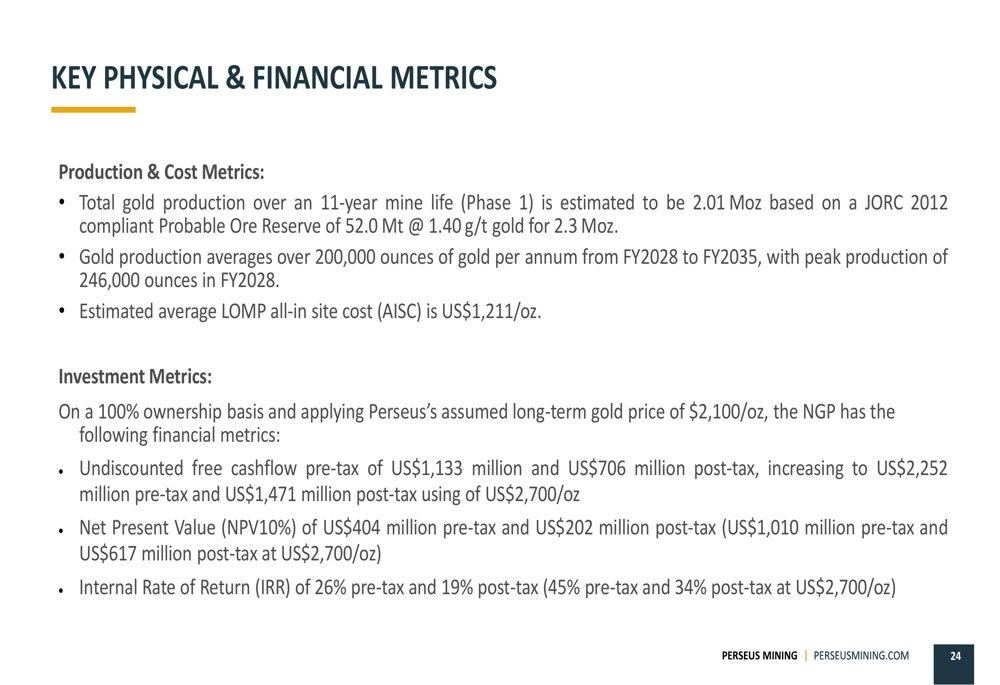

The key metrics for the Nyanzaga project highlight its potential to become a cornerstone asset:

The project is expected to produce 2.01 million ounces over an 11-year mine life, averaging over 200,000 ounces annually from FY2028 to FY2035 at an all-in site cost of US$1,211 per ounce. The project has an estimated pre-tax NPV (10%) of US$404 million and IRR of 26% (19% post-tax).

First gold pour at Nyanzaga is scheduled for the first quarter of 2027, as shown in the project timeline:

Forward-Looking Statements

Perseus provided production and cost guidance for the remainder of FY25, projecting group production of 469,709 to 504,709 ounces for the full year at an all-in site cost of US$1,250 to US$1,280 per ounce.

The company reported that current operating performance is on track to meet or exceed market guidance for the June 2025 half-year. Management noted that all three mines are "performing reasonably well, though with challenges," and highlighted the "steadily expanding cash margin due to elevated gold prices and steady unit costs."

On the sustainability front, Perseus reported a Total (EPA:TTEF) Recordable Injury Frequency Rate (TRIFR) of 0.74, with four recordable injuries in the quarter. The company’s economic contribution to host countries was approximately US$193 million, representing about 67% of revenue, while local and national employment remained stable at 95%.

With its strong cash position, Perseus is well-positioned to fund its growth projects while potentially returning capital to shareholders through continued share buybacks. The development of the CMA Underground and Nyanzaga projects is expected to significantly extend the company’s production profile and mine life, providing a foundation for sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.