US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Photronics Inc. (NASDAQ:PLAB), a global leader in the photomask industry, presented its fiscal second quarter 2025 financial results on May 28, 2025, revealing a slight revenue decline amid ongoing market challenges. The company’s stock fell 5.18% in premarket trading to $19.02, suggesting investors were disappointed with the results or cautious guidance.

The presentation highlighted Photronics’ continued focus on high-end segments and geographic expansion despite a challenging demand environment. The company emphasized its strategic positioning to benefit from semiconductor regionalization trends and node migration toward smaller geometries.

Quarterly Performance Highlights

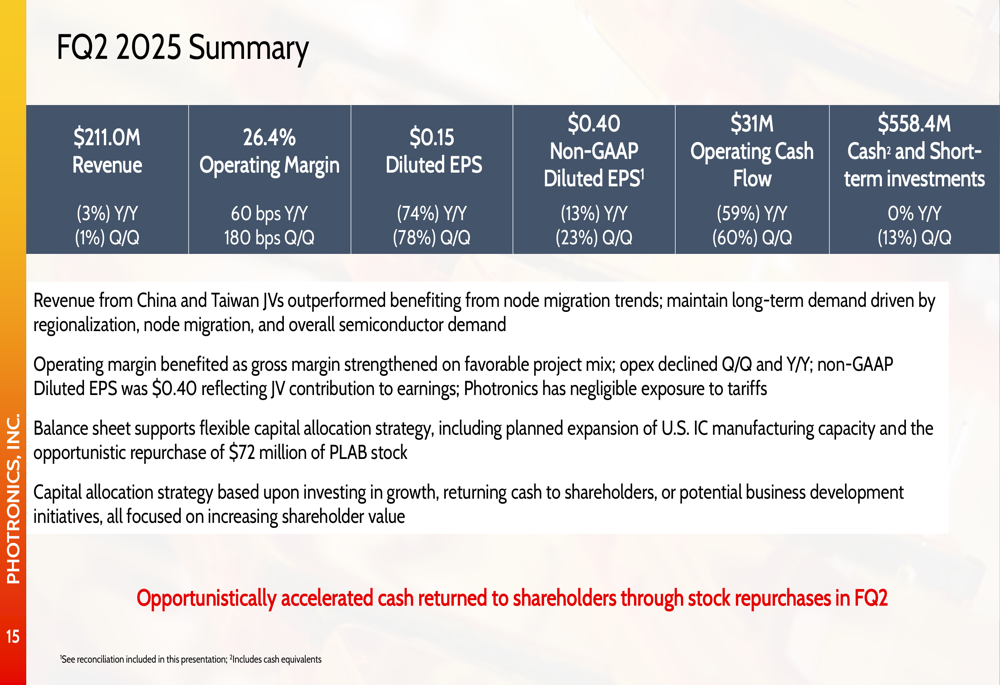

Photronics reported Q2 2025 revenue of $211.0 million, representing a 3% year-over-year decline and a 1% sequential decrease from the previous quarter. Despite the revenue dip, the company improved its operating margin to 26.4%, up 60 basis points year-over-year and 180 basis points quarter-over-quarter.

As shown in the following comprehensive financial summary:

GAAP diluted earnings per share fell significantly to $0.15, down 74% year-over-year and 78% quarter-over-quarter. However, non-GAAP diluted EPS, which adjusts for foreign exchange impacts, was $0.40, representing a more modest decline of 13% year-over-year and 23% sequentially.

Operating cash flow decreased substantially to $31 million, down 59% year-over-year and 60% quarter-over-quarter, while the company maintained a strong cash position with $558.4 million in cash and short-term investments.

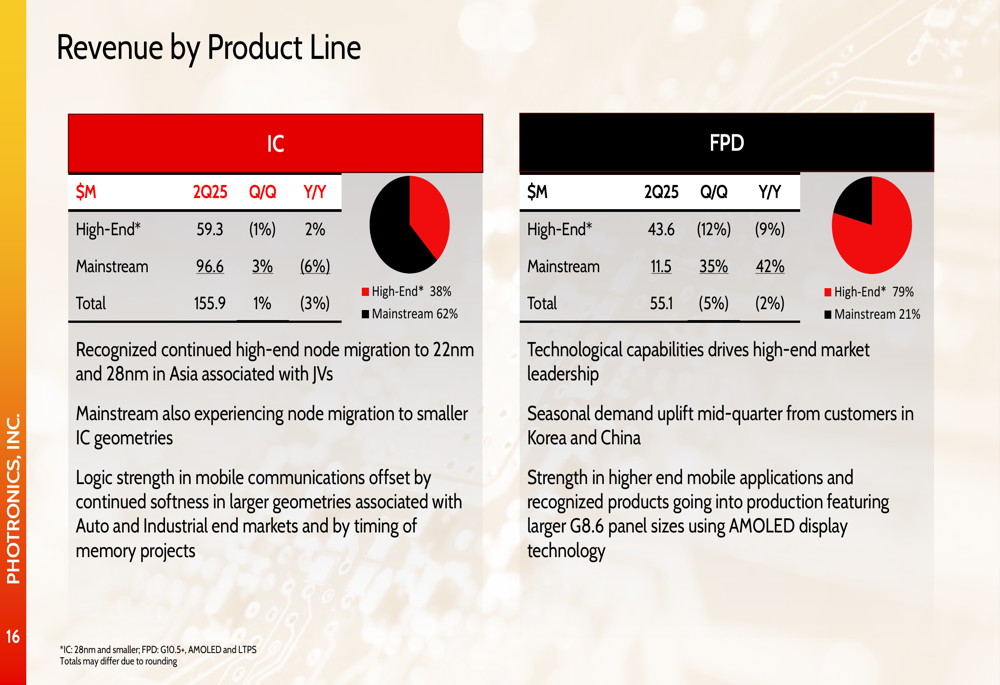

The revenue breakdown by product line reveals divergent performance across segments:

In the IC segment, which represents 74% of total revenue, high-end products (28nm and smaller) grew 2% year-over-year to $59.3 million, while mainstream products declined 6% to $96.6 million. The FPD segment showed mixed results with high-end products (G10.5+, AMOLED, and LTPS) declining 9% year-over-year to $43.6 million, while mainstream products surged 42% to $11.5 million.

Management noted that revenue from China and Taiwan joint ventures outperformed, benefiting from node migration trends toward 22nm and 28nm geometries. The company also highlighted strength in mobile communications within the logic segment, offset by continued softness in larger geometries associated with automotive and industrial end markets.

Strategic Initiatives

Photronics continues to execute its strategic investment strategy focused on sustaining profitable growth through targeted capacity expansion and technology leadership:

The company emphasized its approach to capital allocation, balancing investments in growth, business development initiatives, and returning cash to shareholders. In Q2, Photronics opportunistically repurchased $72 million of its stock, reflecting management’s confidence in the company’s long-term prospects despite near-term challenges.

Capital expenditures for the quarter totaled $60.5 million, primarily directed toward expanding facility and IC capacity in the United States and replacing end-of-life tools. The company reiterated its full-year capital expenditure target of approximately $200 million.

Photronics’ long-term growth strategy continues to be driven by several industry trends, including semiconductor design activity, regional diversification of semiconductor production, and innovations in advanced displays:

The company is particularly well-positioned to benefit from supply chain regionalization, with operations in four of the top five countries for semiconductor manufacturing. This strategic geographic footprint provides Photronics with competitive advantages in an industry with high barriers to entry.

Forward-Looking Statements

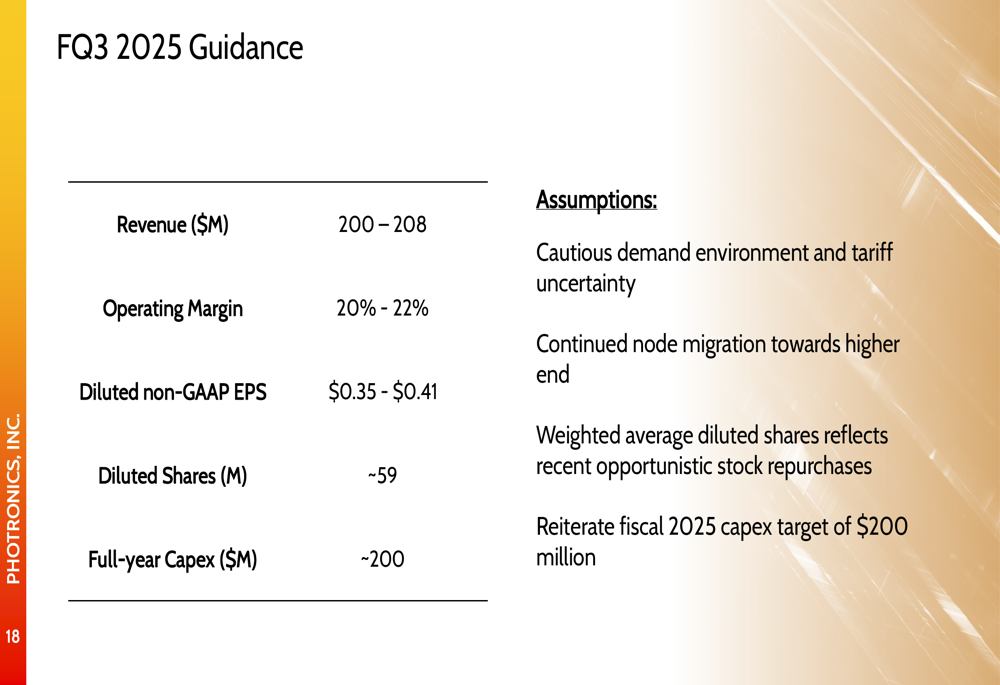

For the third quarter of fiscal 2025, Photronics provided the following guidance:

The company expects Q3 revenue between $200-208 million, operating margin of 20-22%, and non-GAAP diluted EPS of $0.35-0.41. This guidance reflects management’s cautious outlook on the demand environment and uncertainty related to tariffs.

The projected sequential decline in both revenue and operating margin suggests continued challenges in the near term. However, management remains committed to its full-year capital expenditure target of $200 million, indicating confidence in the company’s long-term growth prospects.

Competitive Industry Position

Despite current market challenges, Photronics maintains a strong competitive position in the photomask industry, supported by its global footprint, technological leadership, and operational excellence:

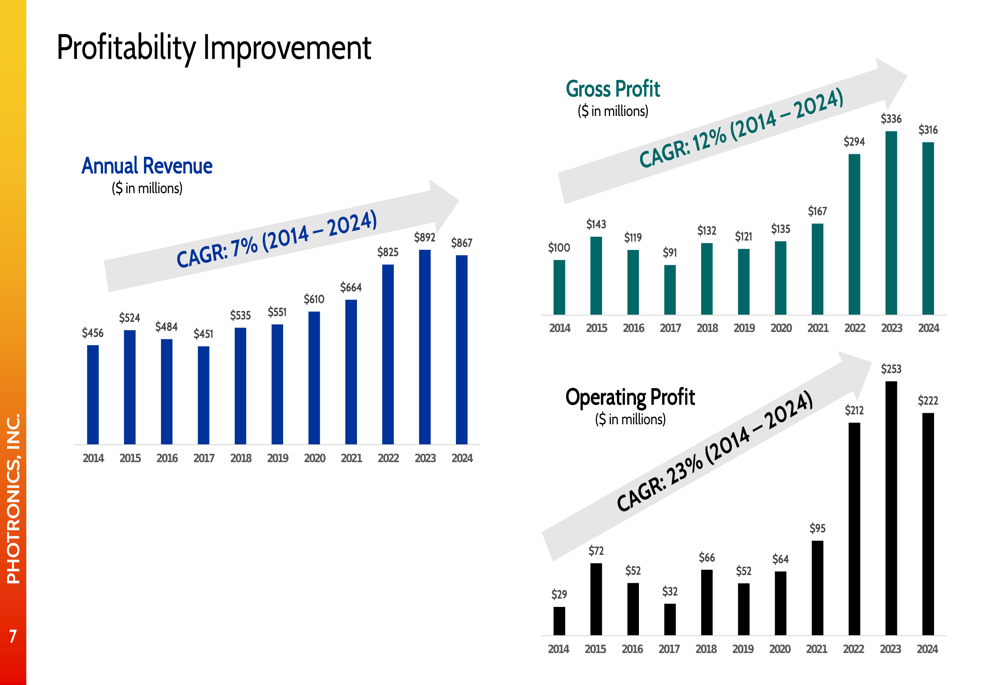

The company’s historical financial performance demonstrates its ability to deliver sustained growth and improved profitability over time:

From 2014 to 2024, Photronics achieved a compound annual growth rate (CAGR) of 7% in revenue, 12% in gross profit, and 23% in operating profit. This track record of performance improvement provides context for the company’s current strategy of investing through market cycles to capture long-term growth opportunities.

In the advanced display market, Photronics is capitalizing on the increasing adoption of AMOLED technology in mobile displays and the development of larger G8.6 panel sizes, which require high-quality, advanced photomasks:

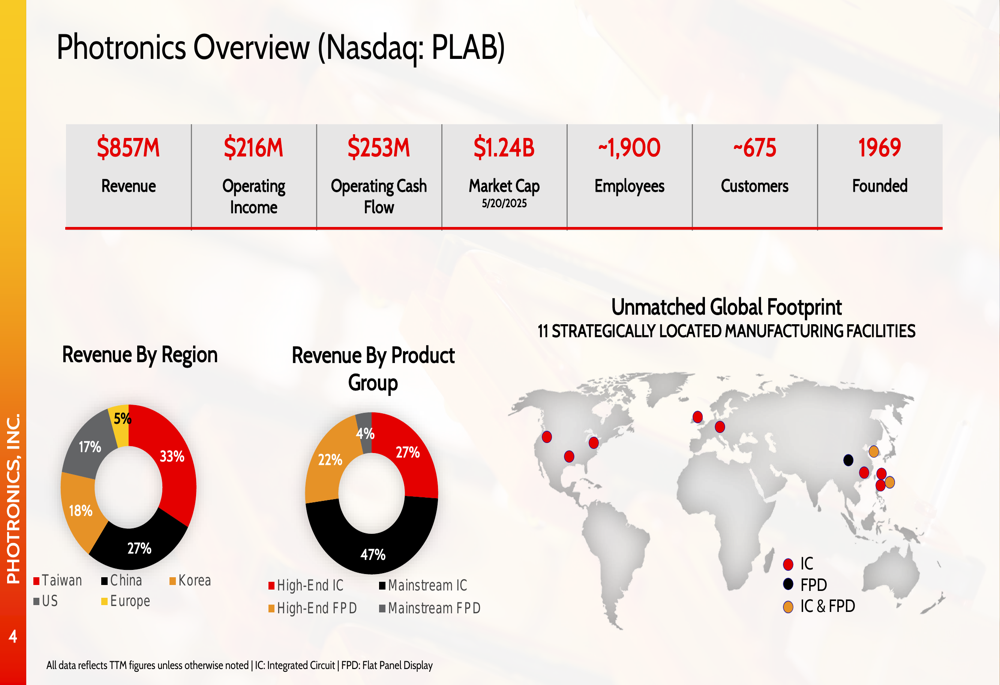

With a global footprint spanning 11 strategically located manufacturing facilities, Photronics serves approximately 675 customers worldwide. The company’s revenue is well-diversified geographically, with China (33%), Korea (27%), US (18%), Taiwan (17%), and Europe (5%) contributing to its global business.

In conclusion, while Photronics faces near-term challenges reflected in its Q2 2025 results and cautious Q3 guidance, the company maintains a strong financial position and continues to execute its long-term strategy focused on high-end segments, geographic expansion, and technology leadership. Investors will be watching closely to see if these strategic initiatives can offset the current market headwinds and deliver improved performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.