Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

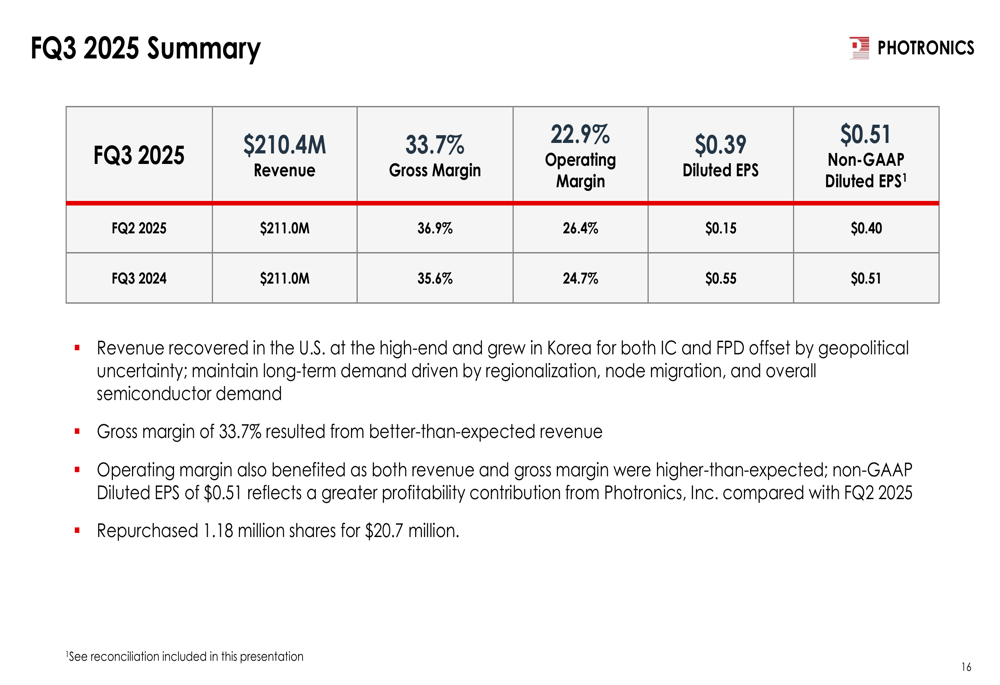

Photronics Inc (NASDAQ:PLAB) shares jumped over 10% in premarket trading after the company presented its fiscal third quarter 2025 results, showing signs of recovery following a disappointing second quarter. The photomask manufacturer reported revenue of $210.4 million and non-GAAP earnings per share of $0.51, demonstrating resilience amid ongoing industry challenges.

The company’s stock traded at $24.60 in premarket activity, up 10.46% from its previous close of $22.27, suggesting investors responded positively to the results and strategic initiatives outlined in the presentation.

Quarterly Performance Highlights

Photronics reported fiscal Q3 2025 revenue of $210.4 million, with a gross margin of 33.7% and operating margin of 22.9%. The company achieved diluted EPS of $0.39, or $0.51 on a non-GAAP basis. While these margins represent a decline from the 37% gross margin and 26% operating margin reported in Q2, the overall performance indicates stabilization after last quarter’s earnings miss.

As shown in the following summary of quarterly results:

Revenue recovery was primarily driven by improvements in the U.S. high-end segment and growth in Korea. The company also repurchased 1.18 million shares for $20.7 million during the quarter, demonstrating confidence in its financial position and commitment to returning value to shareholders.

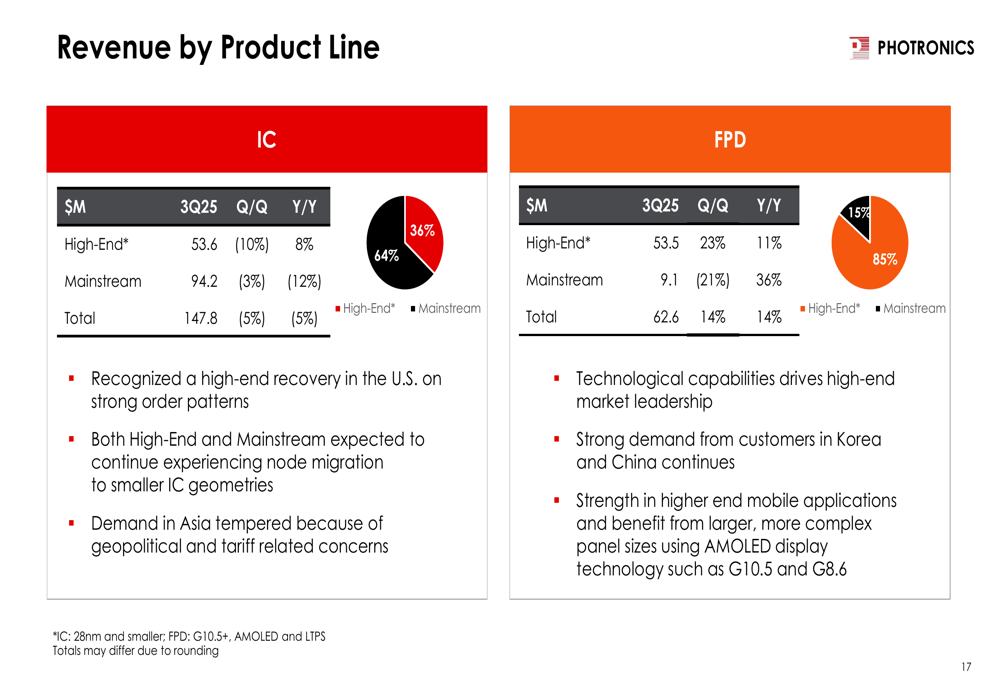

Breaking down revenue by product line reveals divergent performance between segments:

The Integrated Circuit (IC) segment, which accounts for approximately 70% of total revenue, experienced a 5% sequential decline to $147.8 million. Within this segment, high-end IC revenue decreased 10% quarter-over-quarter but increased 8% year-over-year.

Meanwhile, the Flat Panel Display (FPD) segment showed strong growth, with revenue increasing 14% both sequentially and year-over-year to $62.6 million. High-end FPD products, which represent 85% of FPD revenue, grew an impressive 23% quarter-over-quarter and 11% year-over-year, driven by increased demand for advanced displays.

Financial Position

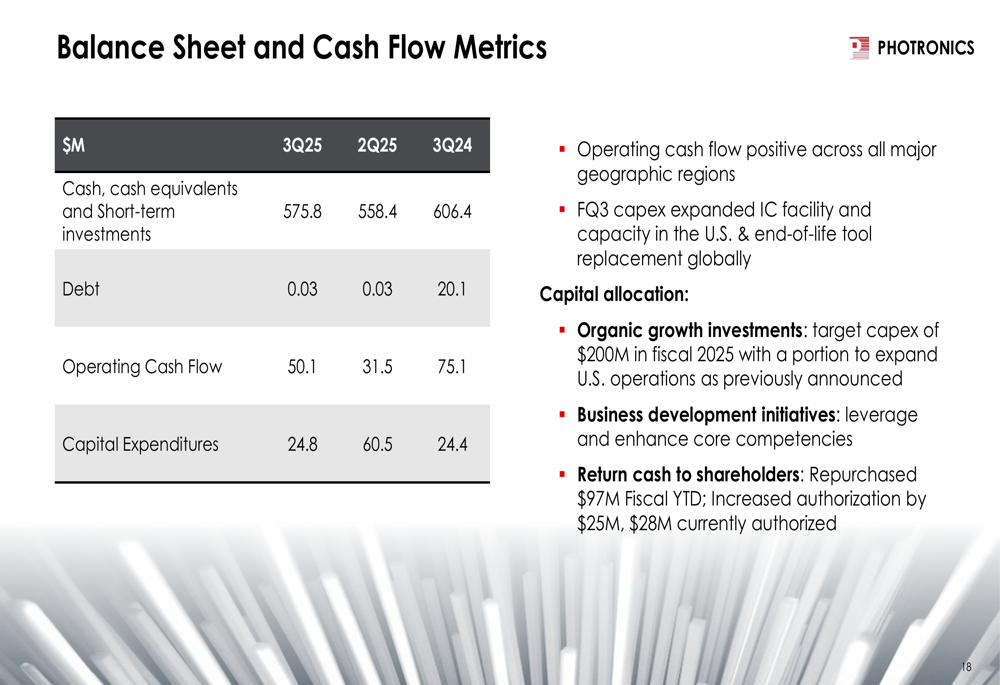

Photronics maintains a robust financial position with $575.8 million in cash and short-term investments, up from $558.4 million in the previous quarter. The company has virtually no debt ($0.03 million) and generated $50.1 million in operating cash flow during Q3.

The following chart illustrates the company’s balance sheet strength and cash flow generation:

Capital expenditures for the quarter totaled $24.8 million, primarily directed toward expanding IC facility and capacity in the U.S. and replacing end-of-life tools globally. The company reiterated its fiscal 2025 capex target of $200 million, with a significant portion allocated to U.S. operations expansion.

This financial strength provides Photronics with flexibility to pursue its strategic initiatives while continuing to return cash to shareholders. The company has repurchased $97 million in shares fiscal year-to-date and increased its repurchase authorization by $25 million, with $28 million currently authorized.

Strategic Initiatives

Photronics highlighted its global footprint as a key competitive advantage, with facilities strategically located near major semiconductor manufacturing hubs. The company’s expansion of U.S. capacity aligns with the broader industry trend of semiconductor production reshoring, supported by government initiatives.

As illustrated in the company’s global presence map:

The company’s Boise site is positioned as the only high-end commercial mask maker in the U.S., while its Taichung facility represents the largest commercial mask maker in Taiwan. This geographic diversification allows Photronics to capitalize on supply chain regionalization trends and mitigate geopolitical risks.

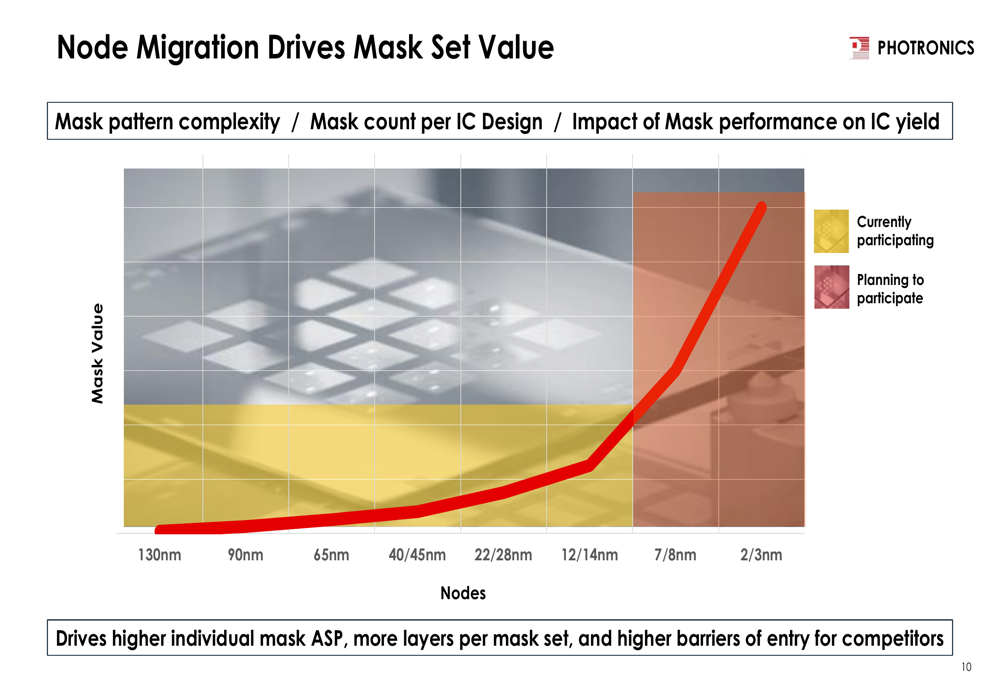

Another key strategic focus is the company’s investment in advanced node technologies. As semiconductor manufacturing moves to smaller nodes, mask set values increase significantly:

This node migration drives higher individual mask average selling prices (ASPs), requires more layers per mask set, and creates higher barriers to entry for competitors. Photronics is strategically positioned to benefit from this trend, with plans to participate in more advanced nodes in the future.

Forward-Looking Statements

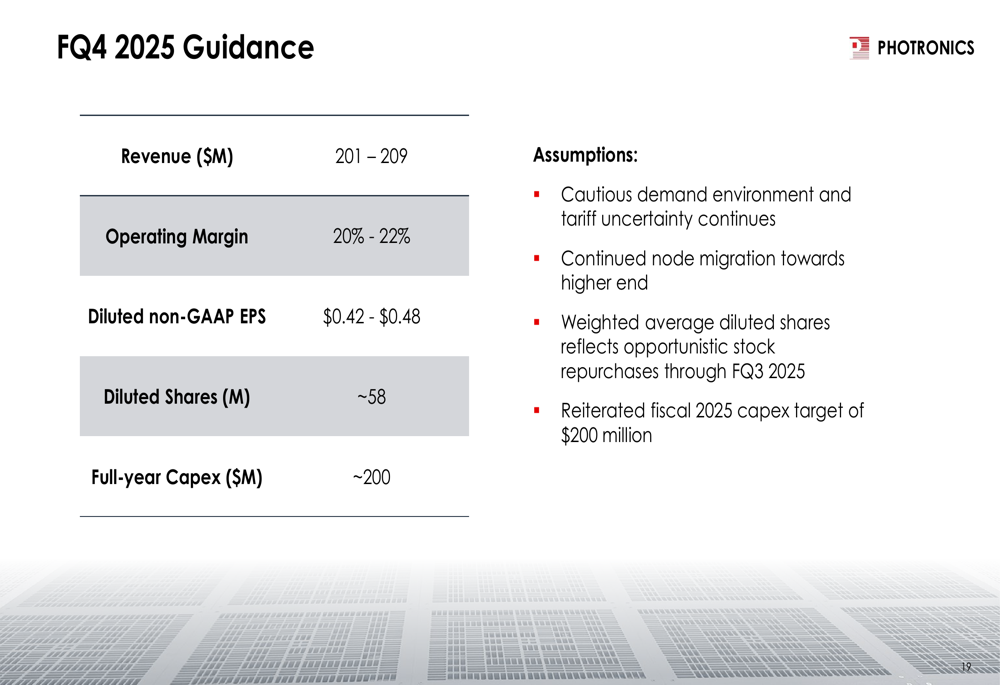

For the fourth quarter of fiscal 2025, Photronics provided guidance that reflects ongoing caution about market conditions:

The company expects Q4 revenue between $201-209 million, operating margin of 20-22%, and non-GAAP diluted EPS of $0.42-$0.48. This guidance suggests a slight sequential decline from Q3 results, reflecting what management described as a "cautious demand environment" and "tariff uncertainty."

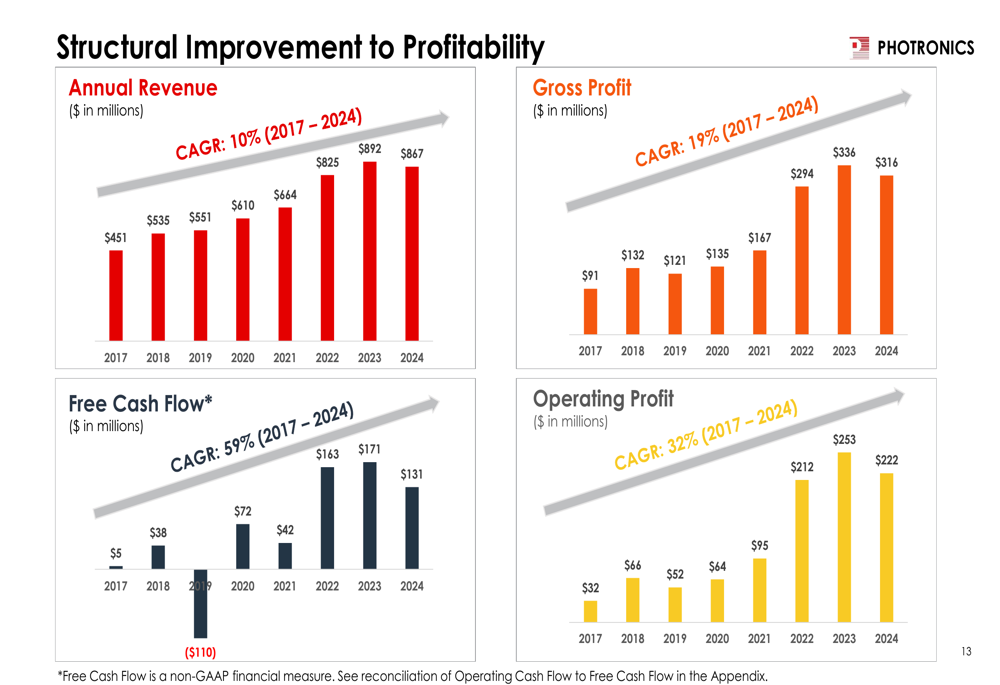

Despite these near-term challenges, Photronics remains optimistic about long-term growth opportunities driven by continued node migration toward higher-end technologies. The company’s structural profitability improvements over recent years provide a solid foundation for navigating current market uncertainties:

From 2017 to 2024, Photronics achieved impressive compound annual growth rates (CAGRs) across key financial metrics: 10% for revenue, 19% for gross profit, 32% for operating profit, and 59% for free cash flow. This track record demonstrates the company’s ability to drive sustainable growth and profitability improvements over time.

Competitive Industry Position

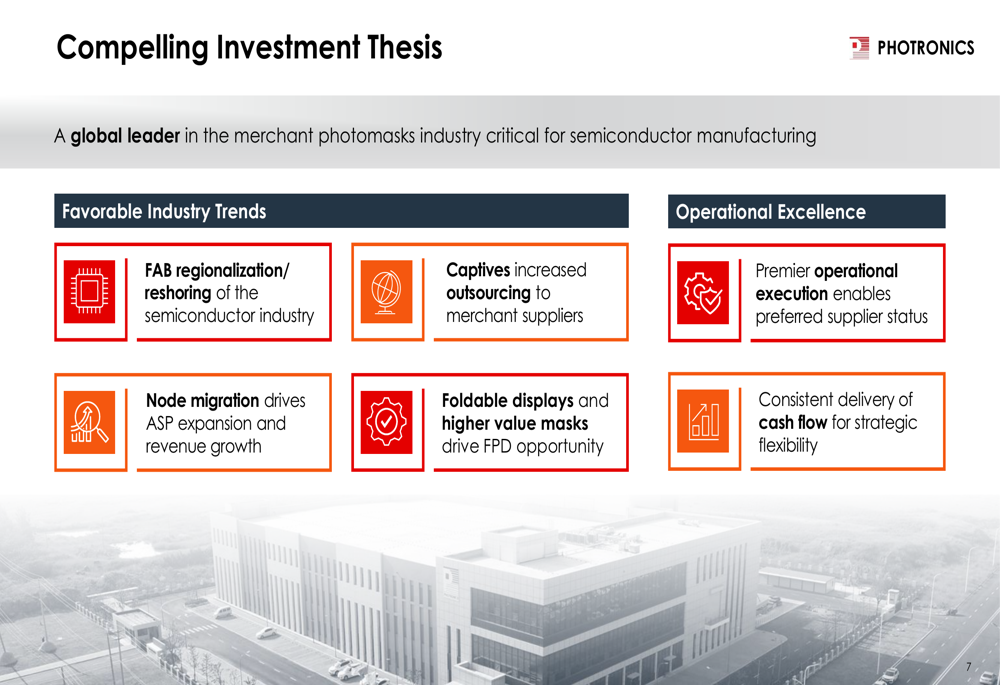

Photronics positions itself as a global leader in the merchant photomasks industry, which plays a critical role in semiconductor manufacturing. The company’s investment thesis emphasizes favorable industry trends, including fab regionalization/reshoring, increased outsourcing by captives, node migration driving ASP expansion, and foldable displays creating new opportunities in the FPD segment.

The company’s compelling investment case is summarized as follows:

In the IC segment, new chip designs continue to drive photomask demand, with the semiconductor market projected to grow from $584.17 billion in 2023 to $1.137 trillion by 2033, according to Precedence Research. Similarly, in the FPD segment, advanced displays are driving innovation, with increasing demand for larger, high-performance displays in consumer electronics.

Photronics’ competitive advantages stem from its operational excellence, commercial expertise, technology leadership, and global footprint. These strengths position the company to capitalize on industry growth trends while navigating near-term challenges.

As semiconductor manufacturing continues to evolve and regionalize, Photronics’ strategic investments in U.S. capacity expansion and advanced node technologies should enable it to maintain its leadership position in the photomask market and deliver long-term value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.