Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

Piaggio Group (BIT:PIA) presented its first half 2025 financial results on July 29, showing the company’s ability to maintain strong margins despite facing significant headwinds across its key markets. The Italian motorcycle and scooter manufacturer reported a 13.9% decline in net sales compared to the same period last year, reflecting broader market challenges that have affected the entire two-wheeler industry.

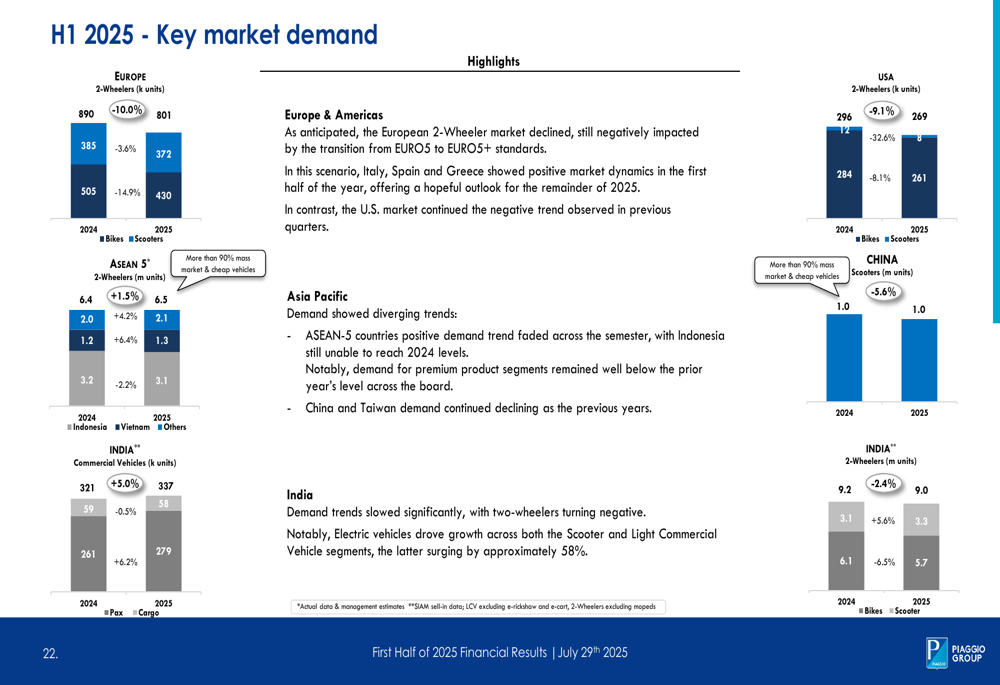

Market demand for two-wheelers contracted across all major regions, with Europe experiencing a 10% decline, the United States down 9.1%, China falling 5.6%, and India seeing a 2.4% decrease. Only the Indian commercial vehicles segment showed positive momentum with 5% growth year-over-year.

As shown in the following chart of key market demand figures:

These market conditions align with the challenges highlighted in Piaggio’s Q1 2025 earnings call, where CEO Michele Konanino emphasized the importance of cash management amid global market uncertainties. The stock has continued to face pressure, trading at €1.978 as of July 29, down 1.31% on the day and significantly below its 52-week high of €2.768.

Quarterly Performance Highlights

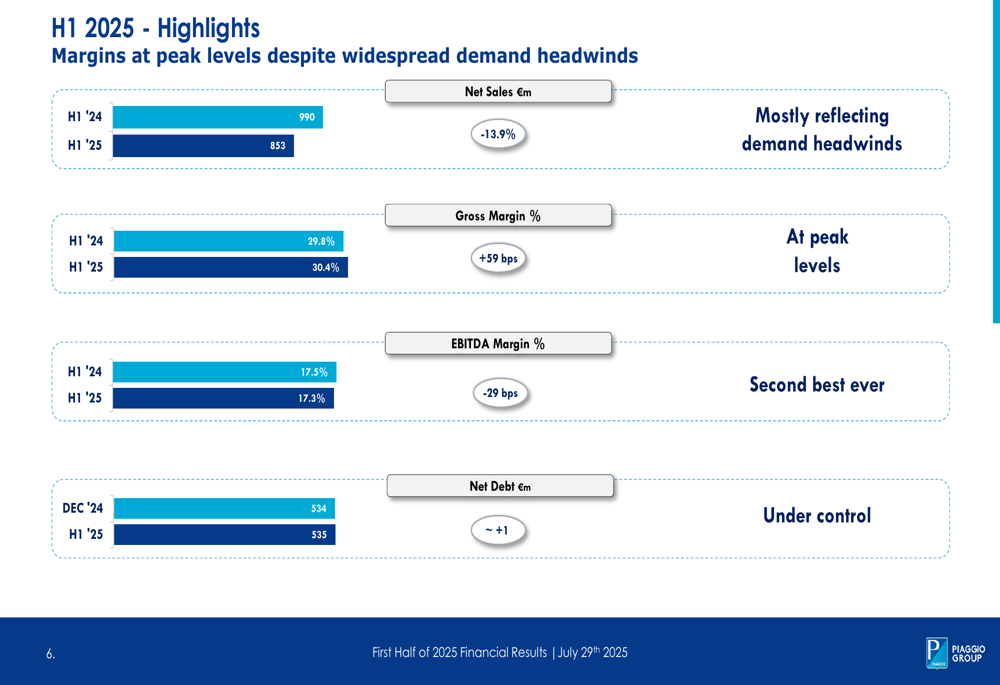

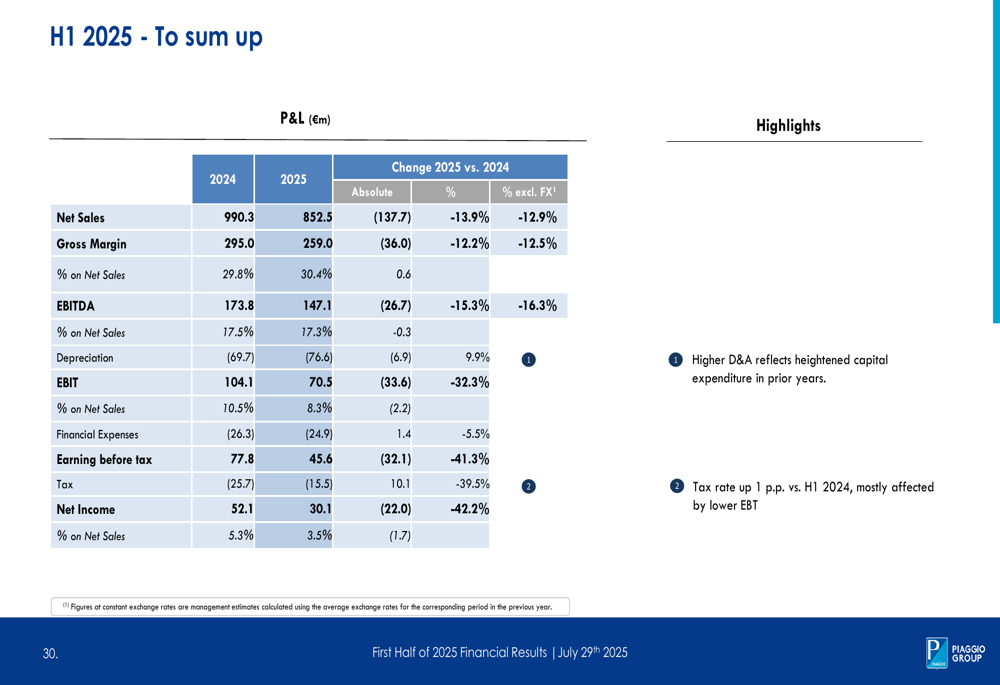

Despite the challenging environment, Piaggio maintained impressive profitability metrics. The company reported net sales of €853 million for H1 2025, down from €990 million in H1 2024. However, gross margin improved to 30.4%, up 59 basis points from 29.8% in the prior year, reaching what the company described as "peak levels."

The EBITDA margin remained strong at 17.3%, only slightly below the 17.5% achieved in H1 2024, which the company characterized as the "second best ever" result. Net income came in at €30.1 million, representing 3.5% of net sales, though this marked a 42.2% decline from the €52.1 million reported in H1 2024.

The following chart illustrates Piaggio’s key financial metrics for H1 2025:

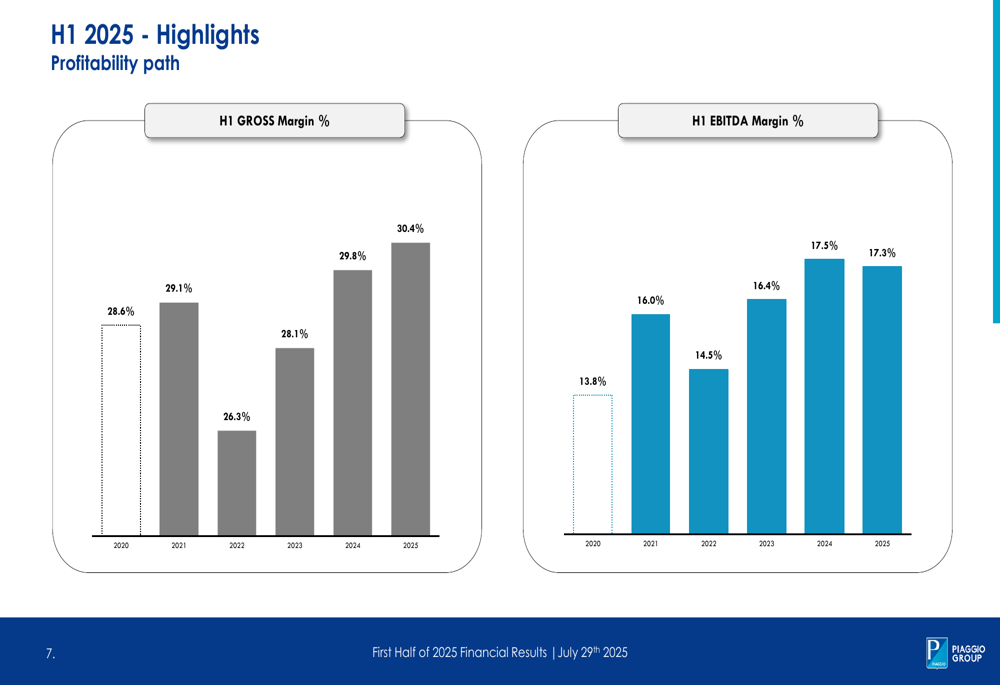

The company’s ability to maintain strong margins despite revenue declines reflects its successful pricing strategy and cost management. This is particularly evident in the historical trend of gross and EBITDA margins over the past six years:

Detailed Financial Analysis

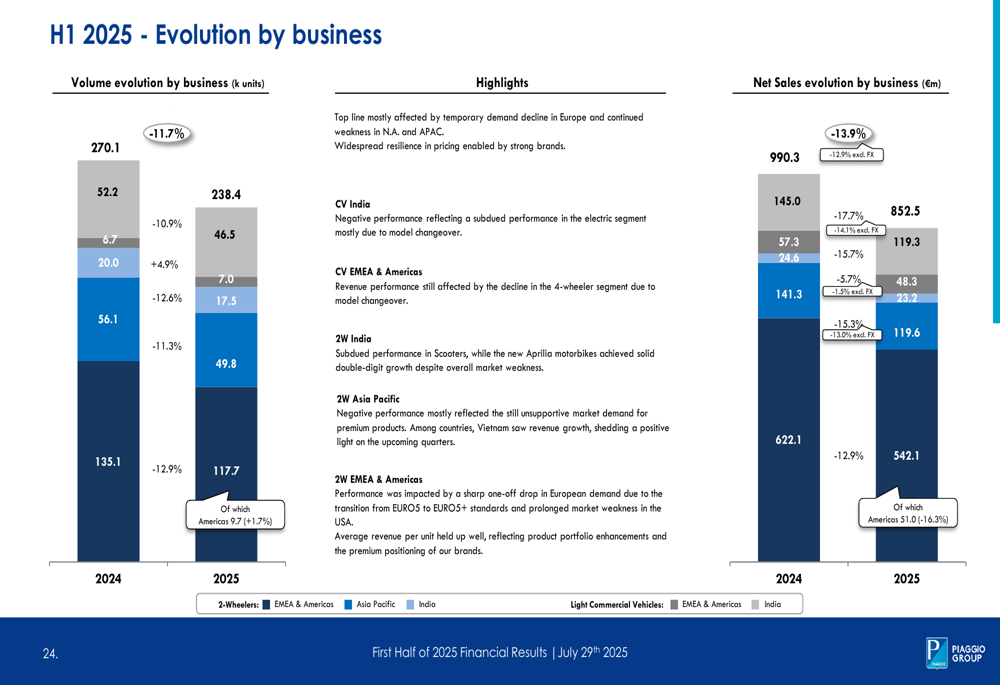

The revenue decline was broad-based across Piaggio’s business segments and regions. In EMEA & Americas, 2-wheeler volumes fell from 135,100 units to 117,700 units, while Asia Pacific declined from 56,100 to 49,800 units. Only the Indian 2-wheeler segment showed modest growth, increasing from 20,000 to 20,900 units. Light commercial vehicles saw declines in both EMEA & Americas and India.

The following chart breaks down the company’s performance by business segment:

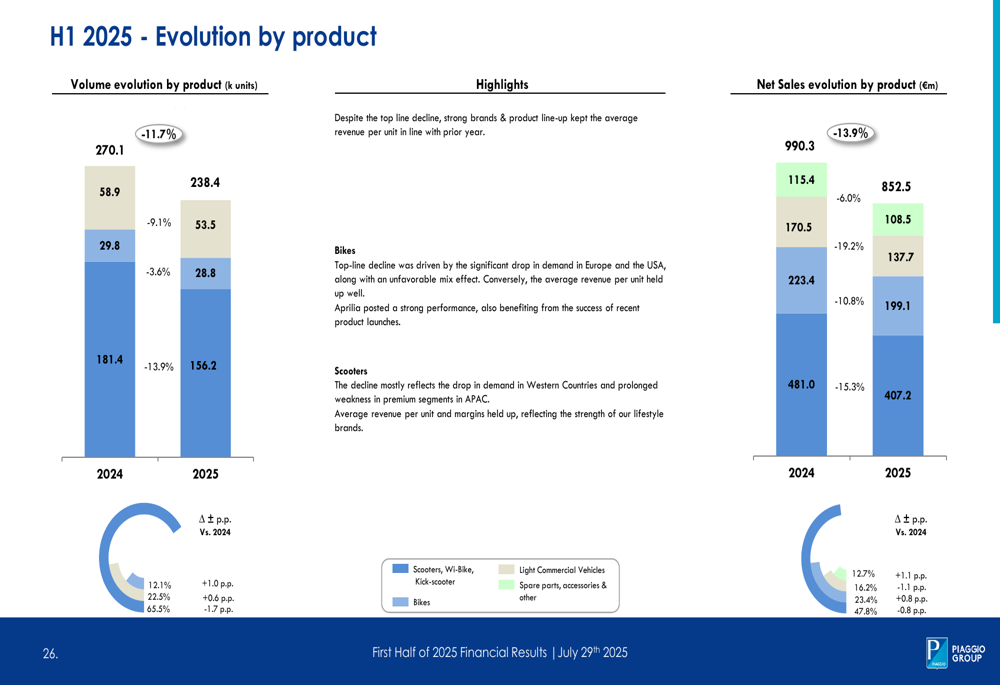

By product category, scooters, Wi-Bikes, and kick-scooters experienced the largest volume decline, falling from 181,400 to 156,200 units. Bikes decreased from 29,800 to 28,800 units, while light commercial vehicles dropped from 58,900 to 53,500 units.

The product segment breakdown is illustrated here:

Despite these volume declines, Piaggio’s strong brand positioning helped maintain average revenue per unit, demonstrating the company’s pricing power in a challenging market.

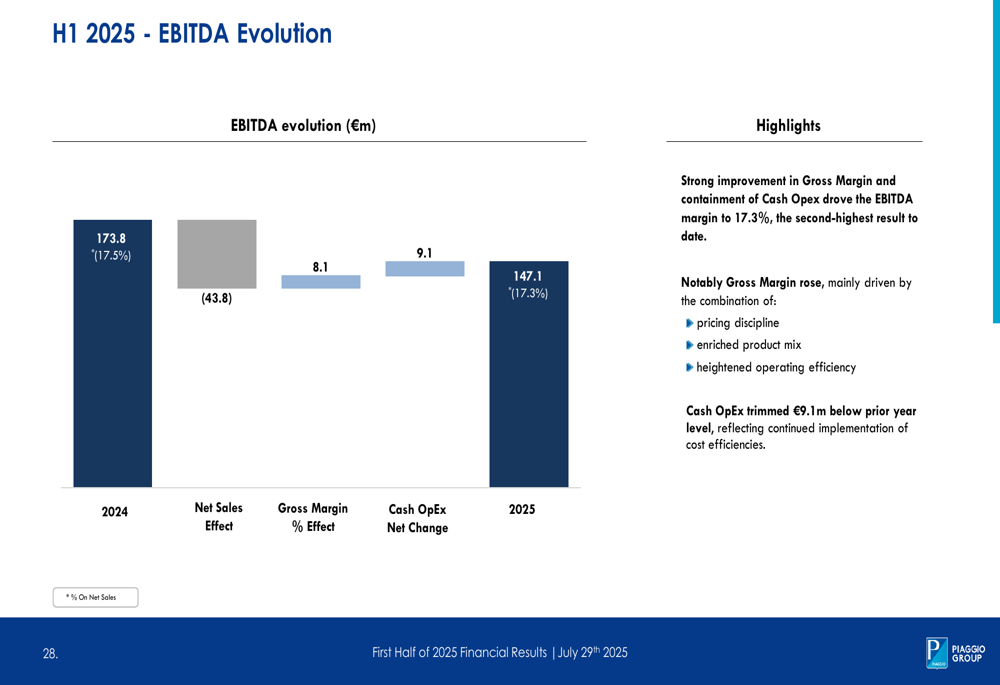

The EBITDA evolution reveals how the company managed to largely offset the negative impact of lower sales through improved gross margin and reduced operating expenses:

The comprehensive financial summary shows that while net income declined significantly by 42.2% to €30.1 million, this was primarily due to higher depreciation and amortization reflecting increased capital expenditure in prior years, as well as a higher tax rate:

Strategic Initiatives

Piaggio continues to leverage its diverse brand portfolio, with each brand targeting specific market segments: Vespa for "Lifestyle," Piaggio for "City," Aprilia for "Race," and Moto Guzzi for "Road." This strategic positioning allows the company to address different consumer preferences and maintain its market presence despite overall industry challenges.

The company is also advancing its innovation agenda through Piaggio Fast Forward, its robotics division. The presentation highlighted how PFF is developing robots that can safely operate in proximity to people, with applications that align with UN Sustainable Development Goals by enhancing human well-being and supporting safer, more inclusive communities.

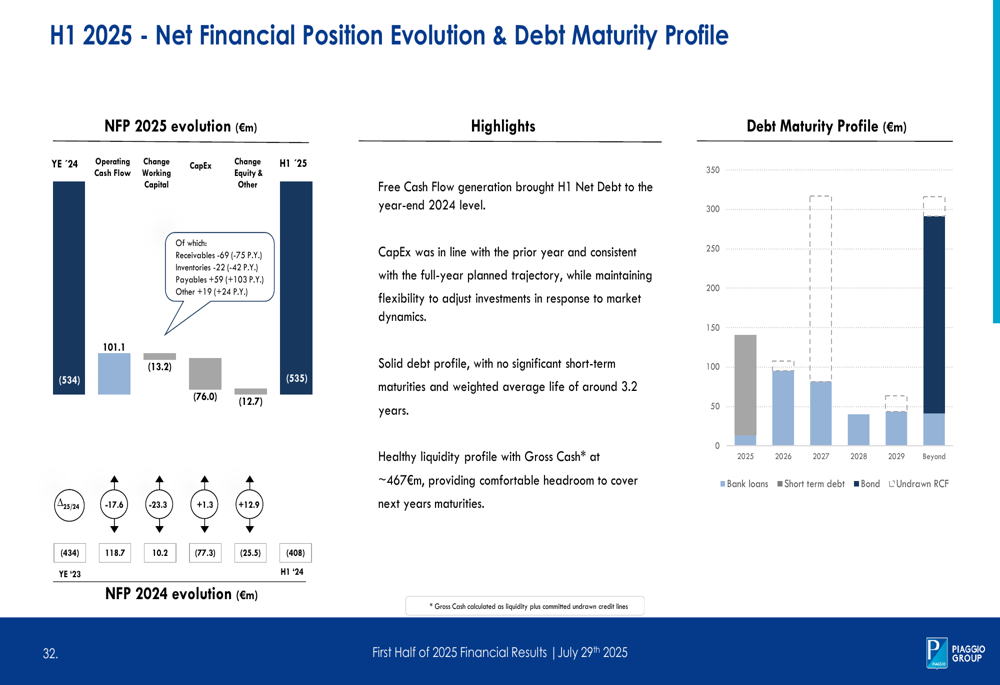

On the financial front, Piaggio has maintained a stable net debt position of €535 million, virtually unchanged from the €534 million reported at the end of 2024. The company’s debt maturity profile shows no significant bank loans or short-term debt due until 2028, providing financial flexibility:

Forward-Looking Statements

While the presentation did not provide specific forward guidance, the company’s focus on maintaining margins and controlling costs suggests a continued emphasis on operational efficiency in the face of market challenges. The stable debt position and careful cash management align with CEO Konanino’s previous statements about cash being "the priority for everybody around the world."

The company’s ability to improve gross margins despite revenue declines demonstrates resilience in its business model. However, the significant drop in net income highlights the challenges Piaggio faces in a contracting market environment.

As mentioned in the Q1 earnings call, Piaggio remains focused on both thermal and electric engine technologies, with potential market recovery expected in the second half of 2025. The company also continues to explore expansion opportunities in Africa, which Konanino previously described as potentially "the next India for our business."

With the stock trading significantly below its 52-week high and near-term market challenges likely to persist, investors will be watching closely to see if Piaggio’s strong brand portfolio and pricing power can continue to support margins while the company navigates through this difficult market cycle.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.