Chip stocks fall with Nvidia after data center rev disappointment

Pilbara Minerals Ltd (ASX:PLS) reported a strong operational recovery in its June Quarter FY25 presentation released on July 30, with production volumes surging 77% quarter-on-quarter despite challenging lithium market conditions. The world’s largest independent hard rock lithium producer completed its P1000 expansion project and announced improved guidance for FY26.

Quarterly Performance Highlights

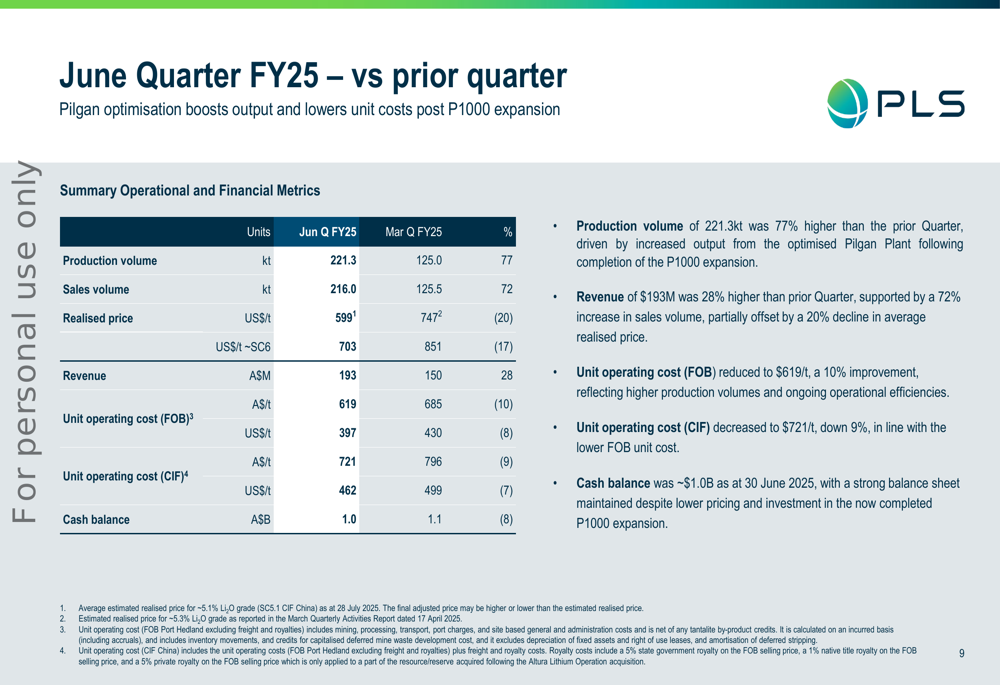

Pilbara delivered substantial improvements across key operational metrics in the June quarter compared to the March quarter. Production volume jumped 77% to 221.3kt, while sales volume increased 72% to 216.0kt. Unit operating costs (FOB) declined 10% to A$619/t (US$397/t), and revenue grew 28% to A$193 million despite a 20% decrease in realized prices.

As shown in the following comprehensive performance comparison:

"P1000 Pilgan plant ramp up completed supporting higher production volume and lower unit operating costs than the prior quarter," the company stated in its presentation. The improved operational efficiency was partly attributed to the Ore Sorting facility, which allows higher usage of lower grade contact material.

Full-Year FY25 Results

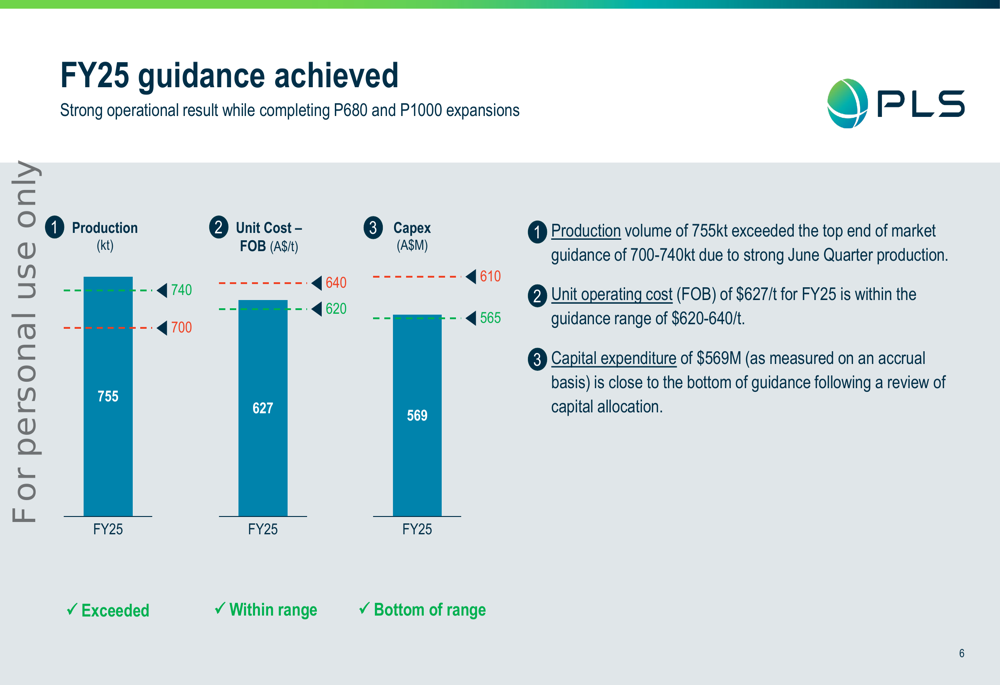

Pilbara successfully achieved its FY25 guidance across all key metrics. Production volume reached 755kt, exceeding the top end of guidance (700-740kt). Unit operating costs (FOB) of A$627/t fell within the guidance range of A$620-640/t, while capital expenditure of A$569 million was at the bottom of the guidance range.

The following chart illustrates the company’s performance against guidance:

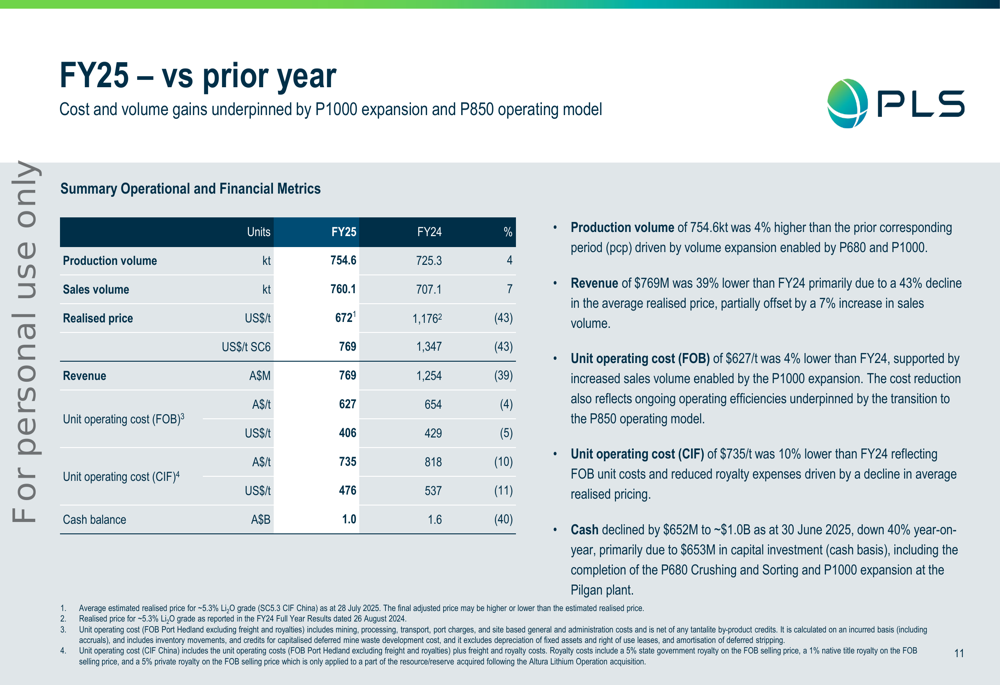

Year-over-year comparisons reveal mixed results, with production and sales volumes increasing by 4% and 7% respectively, while realized prices declined significantly by 43% to US$672/t, reflecting challenging market conditions in the lithium sector.

Financial Position and Capital Management

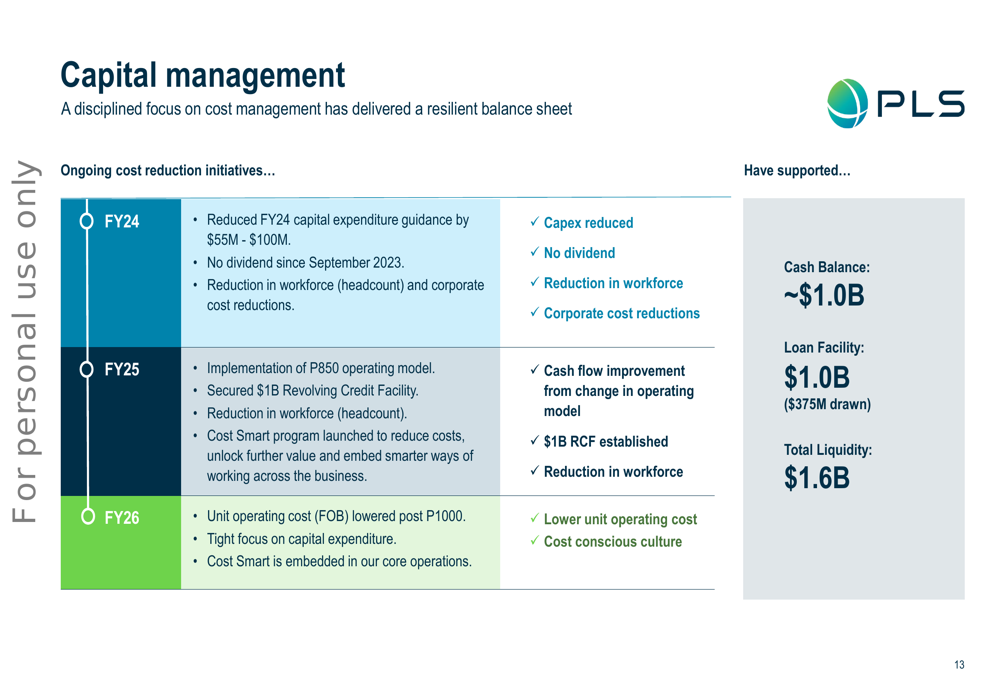

Pilbara maintained a strong financial position with a cash balance of approximately A$1.0 billion as of June 30, 2025, though this represents a decline from A$1.6 billion a year earlier. The company’s cash flow for FY25 shows total outflows of A$652 million, primarily driven by capital expenditure of A$653 million related to expansion projects.

The company has implemented several capital management and cost reduction initiatives throughout FY24 and FY25, including workforce reductions, corporate cost reductions, and the implementation of the P850 operating model. These measures have helped maintain a strong liquidity position of A$1.6 billion, including an undrawn credit facility.

"These initiatives improved cash flow in a period of lower lithium prices," Pilbara noted in its presentation.

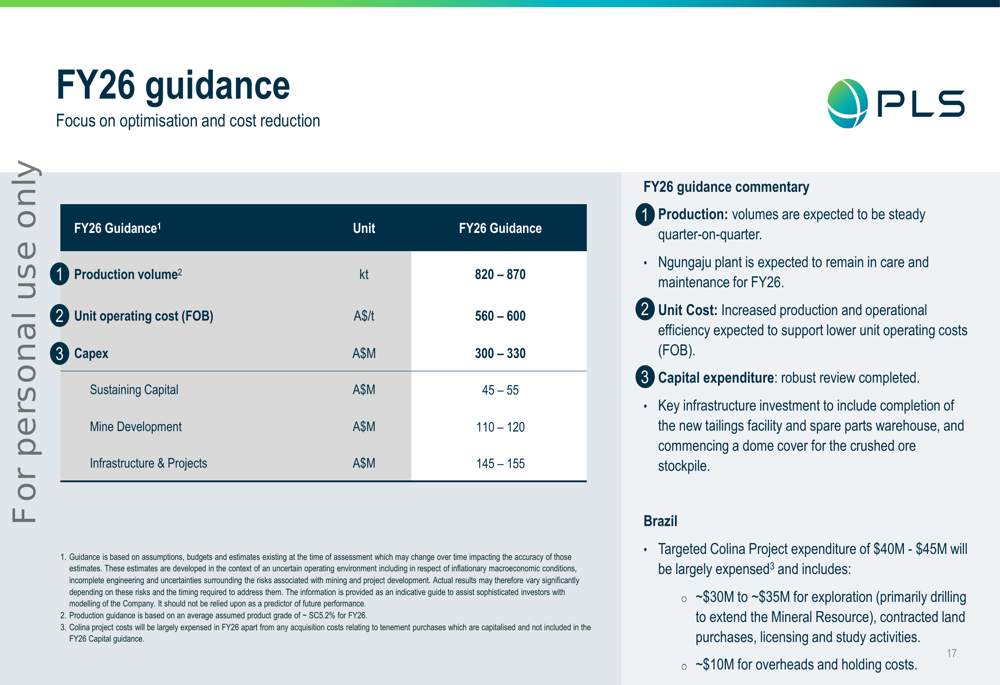

FY26 Outlook and Guidance

Looking ahead to FY26, Pilbara has outlined four key priorities: operational excellence to unlock value from recent investments, study-only focus in the Pilgangoora asset investment cycle, progression of P-PLS Train 2 certification, and modest investment in Colina Project exploration.

The company provided the following guidance for FY26:

The FY26 operating plan leverages new processing capability (ore sorting) to achieve lower operational costs. The company expects to progressively increase contact ore feed throughout FY26 to fully utilize the new Pilgan ore sorting facility, leading to lower mining costs and reduced reliance on clean ore. Average lithium recovery for FY26 is targeted at approximately 72%.

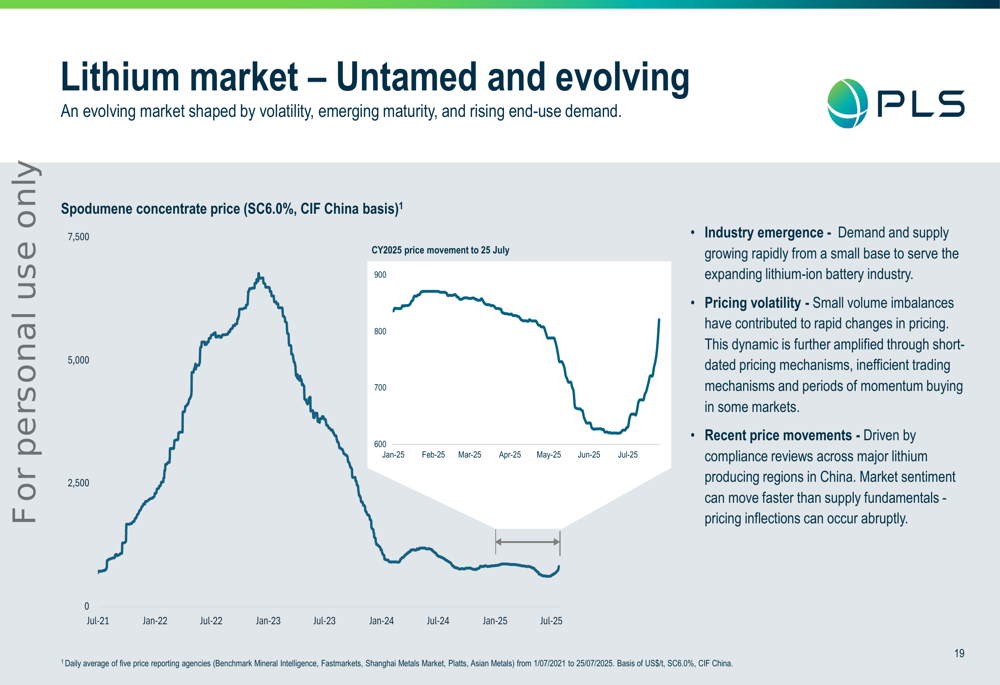

Lithium Market Dynamics

Pilbara characterized the lithium market as "untamed and evolving," shaped by volatility, emerging maturity, and rising end-use demand. The company noted that current pricing remains unsustainable, with a significant portion of the supply chain estimated to be loss-making.

The following chart illustrates the extreme price volatility in the spodumene concentrate market over the past four years:

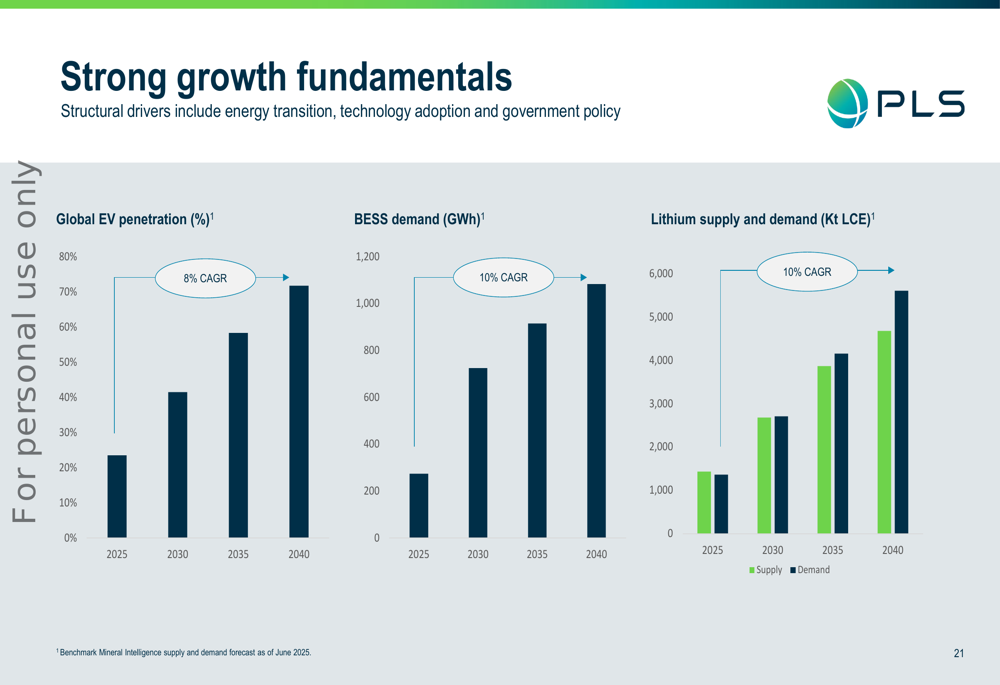

Despite near-term challenges, Pilbara remains optimistic about long-term fundamentals, highlighting strong growth projections for EV penetration and battery energy storage systems (BESS). The company forecasts global EV penetration to increase from approximately 20% to 70% between 2025 and 2040, with BESS demand growing at a 10% CAGR over the same period.

Pilbara’s strategic positioning across established and ex-China supply chains, combined with its flexible operating platform and diversified portfolio across Australia, South Korea, and Brazil, positions the company to navigate market volatility while capitalizing on long-term growth opportunities in the lithium sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.