Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Pitney Bowes Inc (NYSE:PBI) reported its second quarter 2025 results on July 30, showing continued progress in its profitability-focused strategy despite revenue challenges. The company’s stock rose 1.9% to $11.79 in aftermarket trading following the release.

Quarterly Performance Highlights

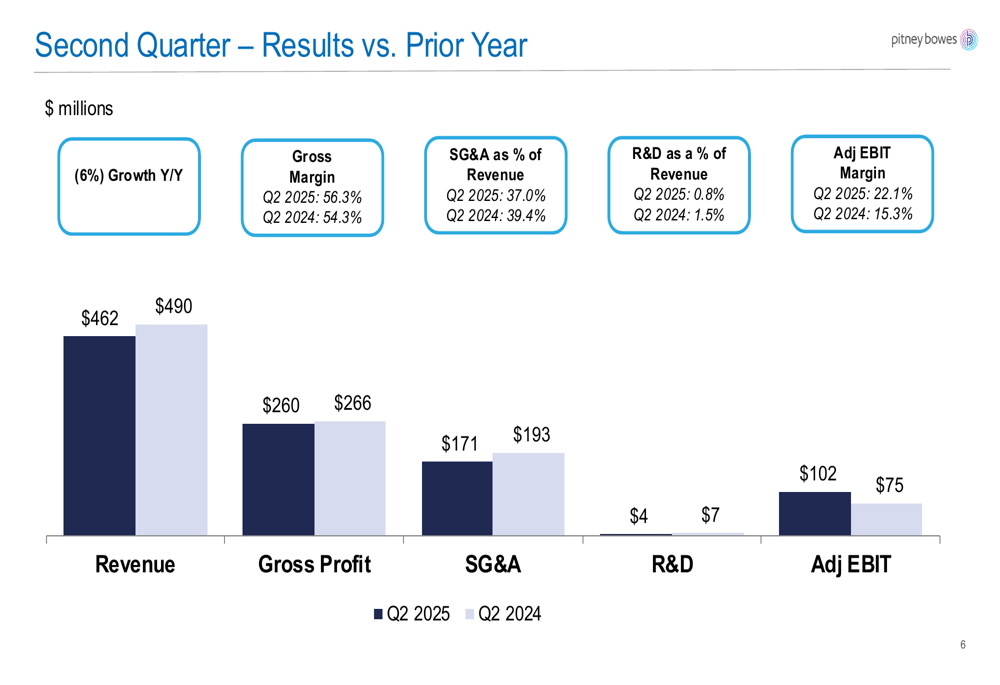

Pitney Bowes delivered mixed results for Q2 2025, with revenue declining but profitability metrics showing substantial improvement. The company reported revenue of $462 million, down 6% year-over-year, while adjusted EBIT increased 37% to $102 million compared to the same period last year.

The shipping and mailing solutions provider posted GAAP EPS of $0.17, an improvement of $0.30 year-over-year, while adjusted EPS reached $0.27, up $0.16 from Q2 2024. GAAP net income was $30 million, representing a significant $55 million improvement from the prior year.

As shown in the following chart comparing key financial metrics between Q2 2025 and Q2 2024:

The company’s gross margin expanded to 56.3% from 54.3% in the prior year, while SG&A expenses as a percentage of revenue improved to 37.0% from 39.4%. These improvements contributed to a substantial increase in adjusted EBIT margin, which reached 22.1% compared to 15.3% in Q2 2024.

Cash flow performance was particularly strong, with GAAP cash from operating activities reaching $111 million, up $31 million year-over-year. Free cash flow was $106 million, excluding $8 million of restructuring payments.

Segment Performance

Pitney Bowes’ two main business segments showed divergent revenue trends but both delivered improved profitability.

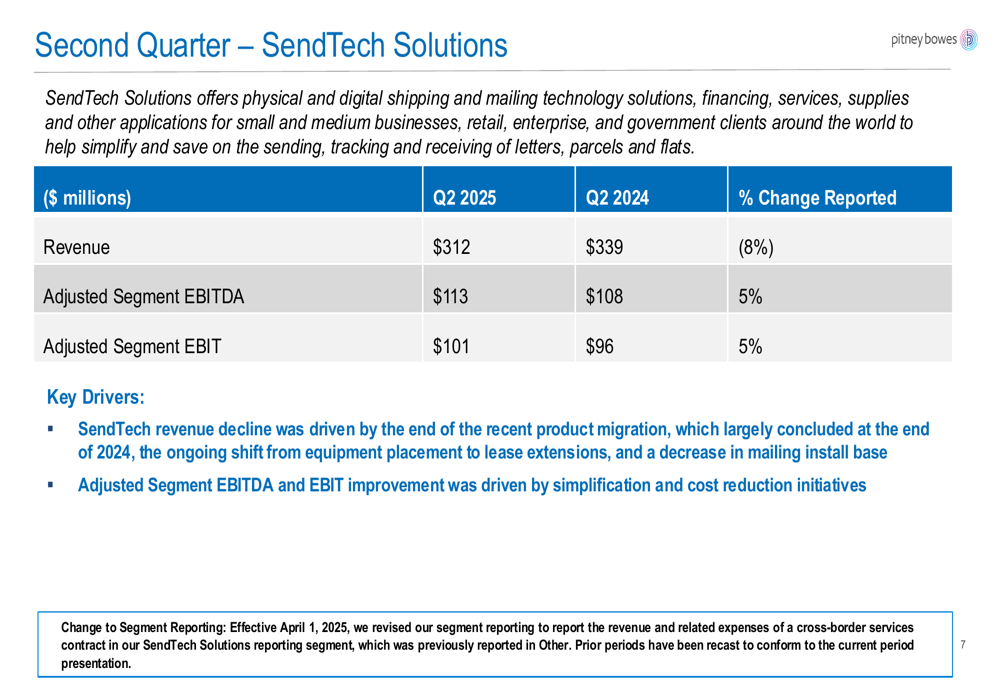

The SendTech Solutions segment, which provides mailing and shipping technology solutions, reported revenue of $312 million, down 8% from the prior year. Despite the revenue decline, the segment’s adjusted EBIT increased 5% to $101 million. The company attributed the revenue decline to the end of a recent product migration, ongoing shift from equipment placement to lease extensions, and a decrease in the mailing install base.

The following slide details SendTech’s performance:

Within SendTech, Global Financial Services maintained stable performance with net finance receivables at $1.15 billion, flat from year-end. Portfolio quality remained stable with low levels of delinquencies and write-offs, while bank deposits were $684 million, down seasonally from year-end.

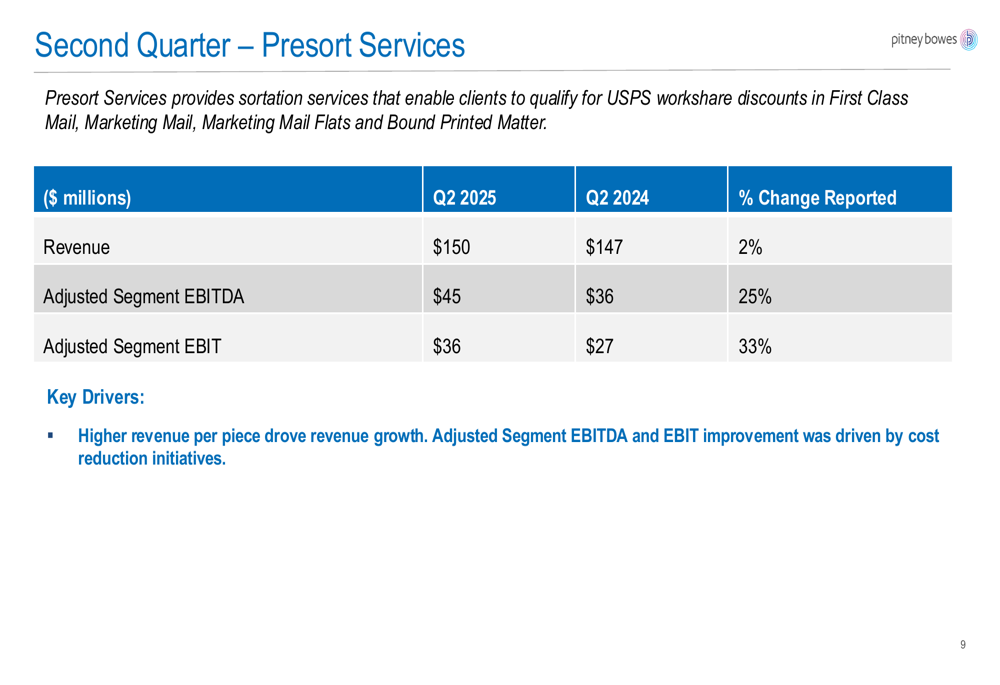

The Presort Services segment, which provides mail sortation services, delivered revenue of $150 million, up 2% from Q2 2024. More impressively, adjusted EBIT for this segment increased 33% to $36 million, driven by cost reduction initiatives.

As illustrated in the Presort Services performance slide:

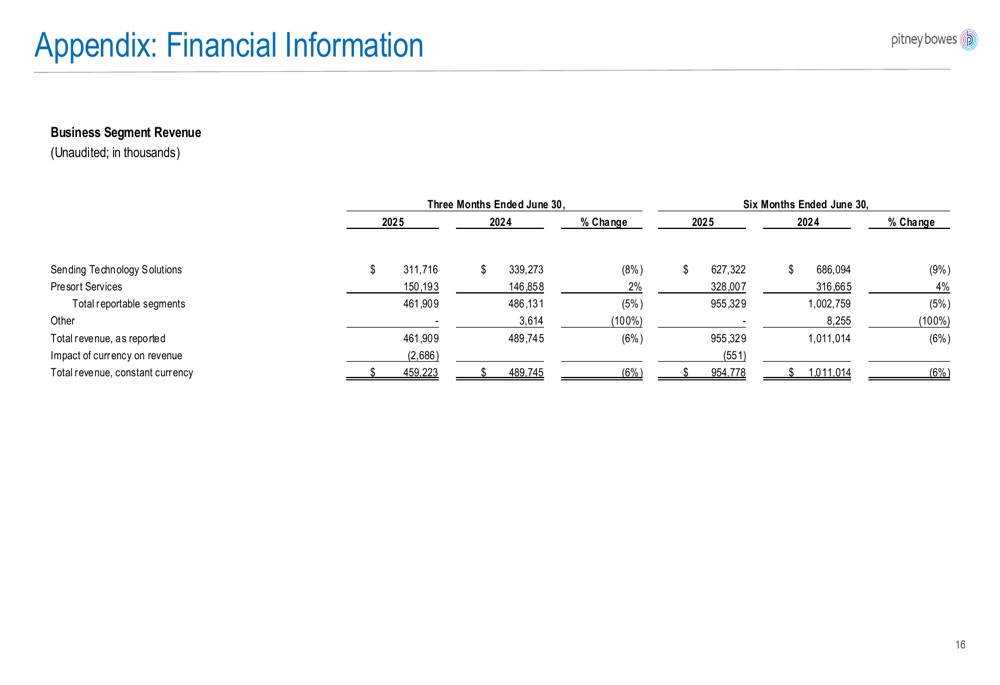

The company’s segment revenue breakdown provides additional context for the overall performance:

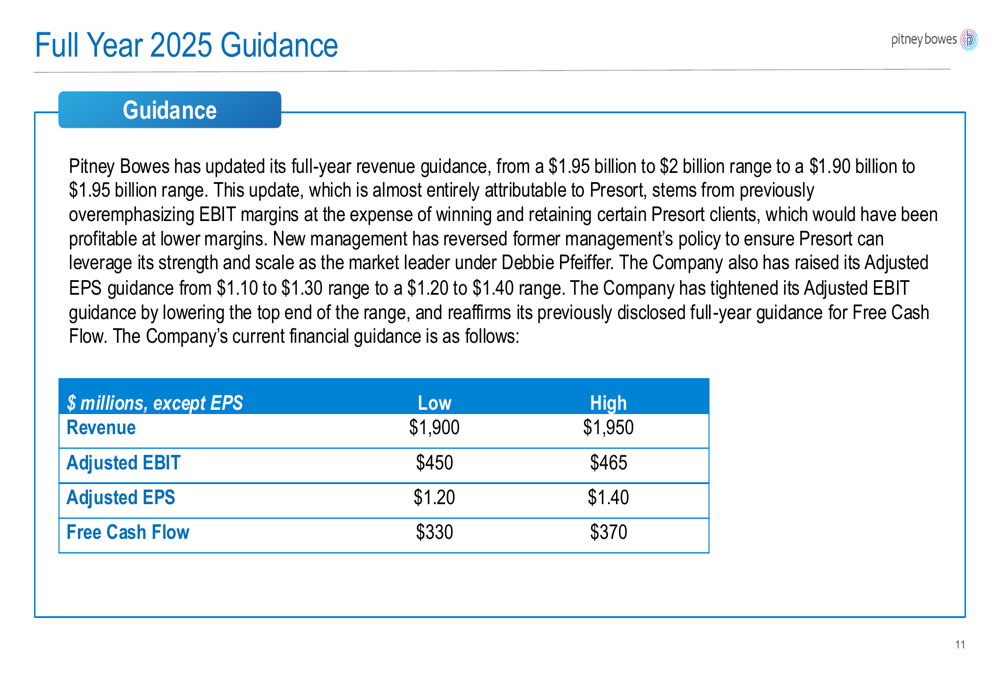

Updated Guidance

Pitney Bowes updated its full-year 2025 guidance, lowering revenue expectations while raising its adjusted EPS outlook. The company now expects revenue between $1.90 billion and $1.95 billion, down from the previous range of $1.95 billion to $2.0 billion.

The company explained this reduction stemmed from "previously overemphasizing EBIT margins at the expense of winning and retaining certain Presort clients." Despite the revenue adjustment, Pitney Bowes raised its adjusted EPS guidance to a range of $1.20 to $1.40, up from the previous $1.10 to $1.30 range.

The full updated guidance is presented in this slide:

The company maintained its free cash flow guidance of $330 million to $370 million, consistent with the outlook provided in Q1 2025.

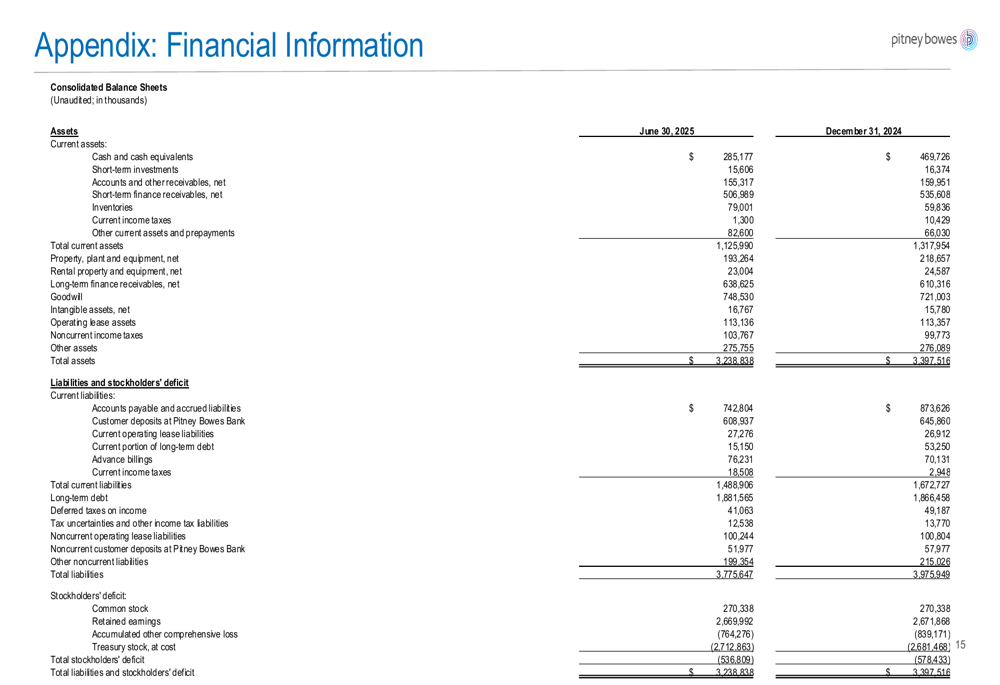

Financial Position

Pitney Bowes continues to manage its debt profile, with total principal debt of approximately $1.93 billion as of June 30, 2025, slightly down from $1.96 billion at the end of 2024. The company’s debt structure includes a mix of term loans and notes with maturities ranging from 2026 to 2043.

The company’s consolidated balance sheet shows:

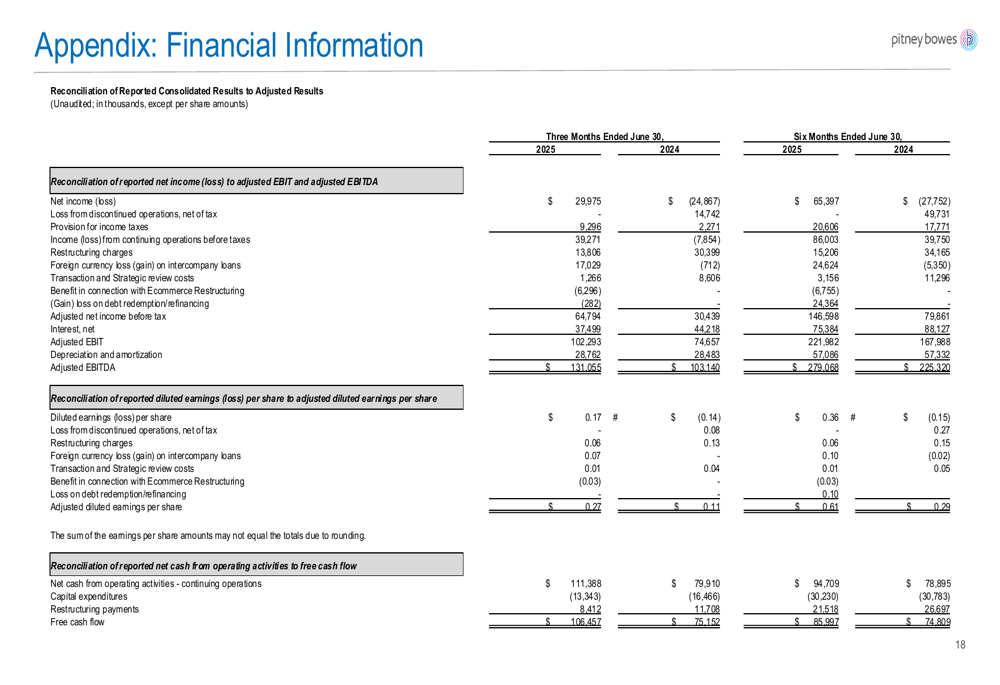

The reconciliation of reported results to adjusted metrics provides insight into the company’s underlying performance:

The Q2 2025 results demonstrate Pitney Bowes’ continued execution of its strategy to prioritize profitability and cash flow over revenue growth. While the company faces ongoing challenges in its traditional mailing business, cost reduction initiatives and strategic shifts are yielding significant improvements in margins and earnings.

This performance builds on the momentum seen in Q1 2025, when the company beat EPS forecasts with adjusted EPS of $0.33. The consistent improvement in profitability metrics despite revenue headwinds suggests management’s strategy is gaining traction as Pitney Bowes navigates the evolving shipping and mailing landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.