Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

PKO Bank Polski, Poland’s largest bank, reported robust financial results for the first half of 2025, demonstrating strong growth across key business segments despite ongoing challenges in the banking sector. The bank’s presentation, delivered in Warsaw in August 2025, highlighted significant improvements in profitability, asset quality, and business volumes against a backdrop of improving economic conditions in Poland.

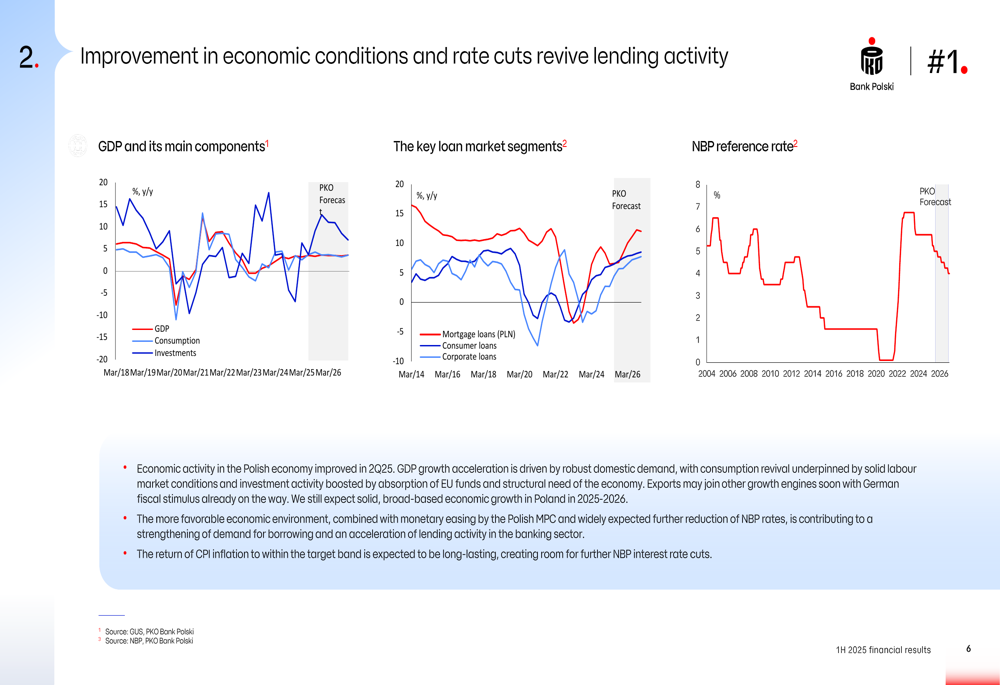

The macroeconomic environment appears favorable for the banking sector, with GDP growth acceleration driven by robust domestic demand. As shown in the following chart of economic conditions, consumption revival is underpinned by solid labor market conditions, while investment activity is boosted by EU funds absorption:

Executive Summary

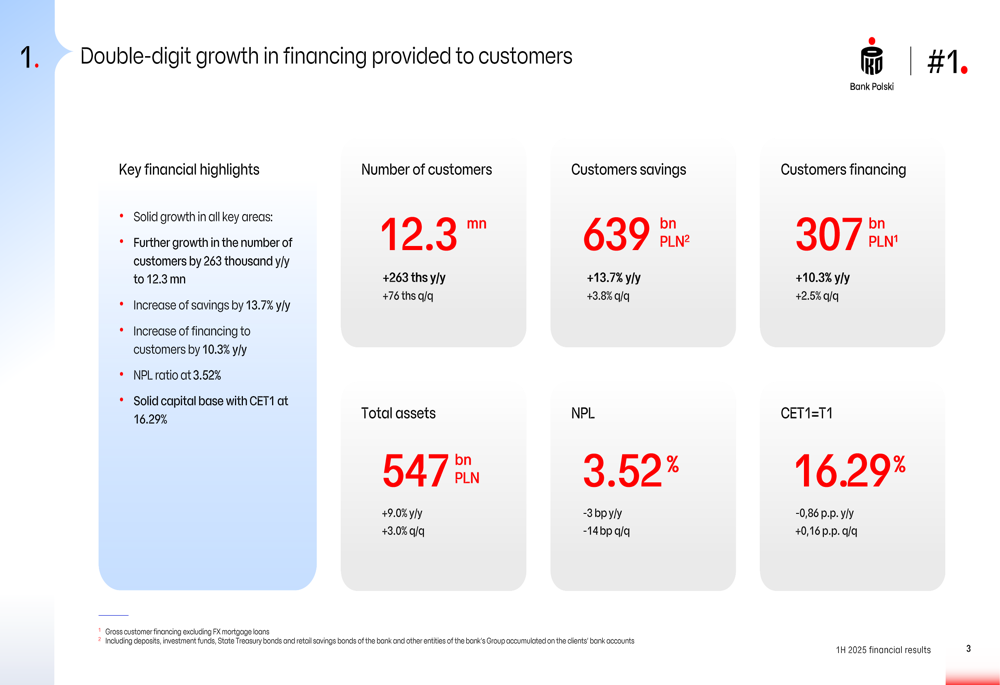

PKO Bank Polski reported a net profit of 5.1 billion PLN for the first half of 2025, representing a 16.7% increase year-over-year. The bank’s return on equity (ROE) reached 19.4%, up 0.5 percentage points from the previous year, while maintaining a cost-to-income ratio of 31.0%. These results were driven by strong growth in customer financing, which increased by 10.3% year-over-year to 307 billion PLN, and customer savings, which grew by 13.7% to 639 billion PLN.

The following slide illustrates the bank’s key financial highlights, including customer growth, savings, financing, and asset quality metrics:

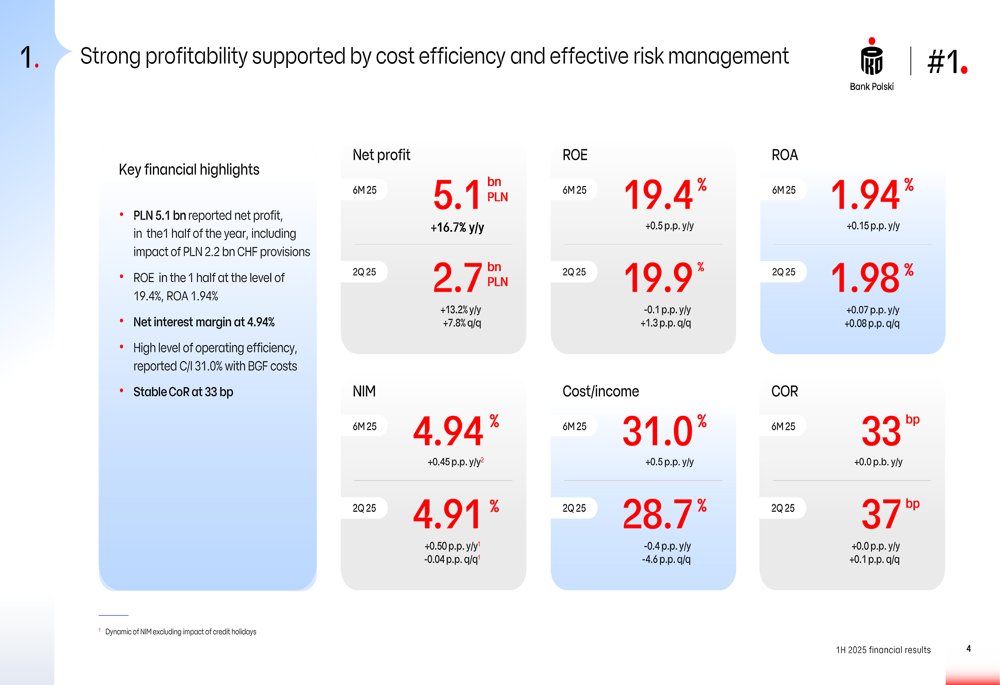

The bank’s profitability metrics show significant improvement across all key indicators, with ROE at 19.4%, ROA at 1.94%, and net interest margin (NIM) at 4.94%. The second quarter of 2025 showed particularly strong performance with net profit reaching 2.7 billion PLN, up 13.2% year-over-year and 7.8% quarter-over-quarter.

As demonstrated in the profitability metrics slide below, PKO Bank Polski maintained strong financial performance despite challenging market conditions:

Quarterly Performance Highlights

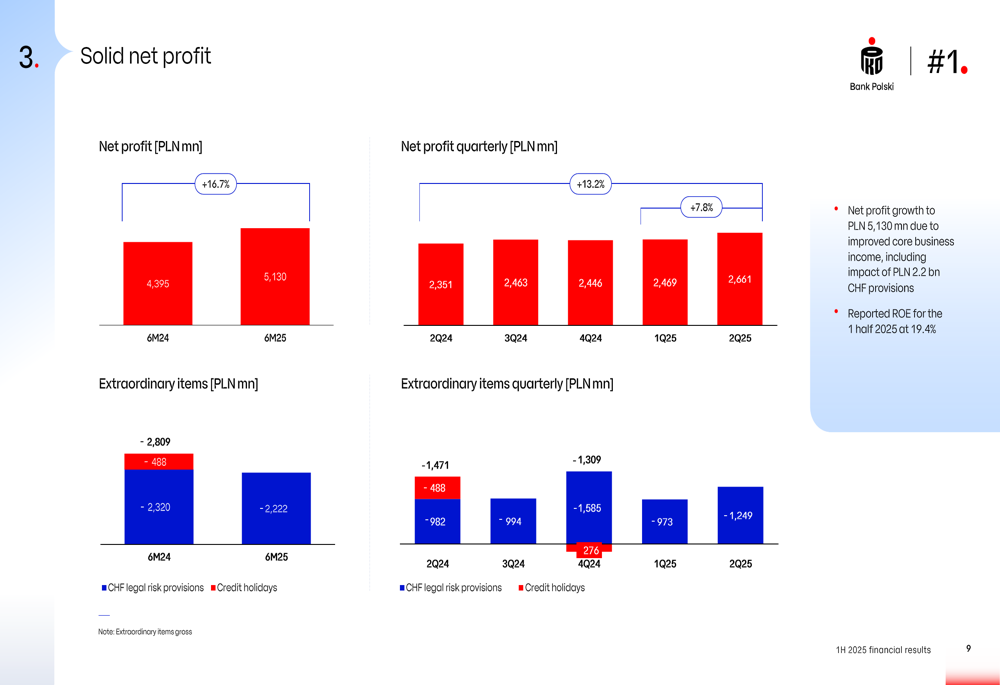

PKO Bank Polski’s net profit for Q2 2025 reached 2.7 billion PLN, up 13.2% year-over-year and 7.8% quarter-over-quarter. This performance was achieved despite significant extraordinary items, including CHF legal risk provisions and credit holidays, which amounted to 1.25 billion PLN in Q2 2025.

The following chart illustrates the bank’s solid net profit performance over recent quarters:

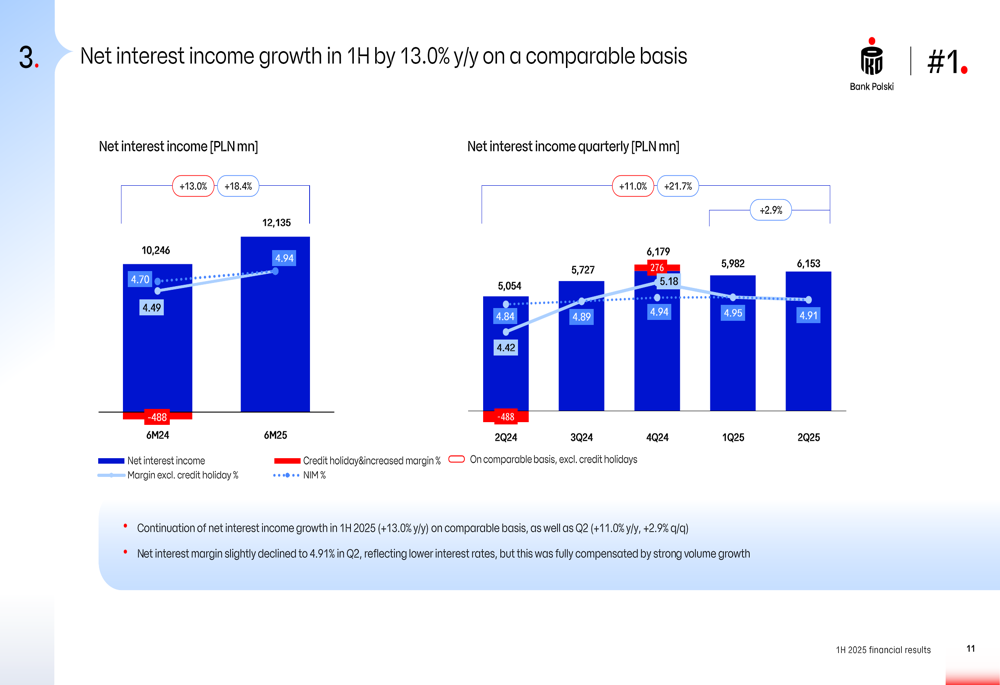

Net interest income, the bank’s primary revenue driver, grew by 13.0% year-over-year in the first half of 2025 on a comparable basis. The net interest margin slightly declined to 4.91% in Q2, reflecting lower interest rates, but this was fully compensated by strong volume growth.

As shown in the following chart of net interest income growth:

Detailed Financial Analysis

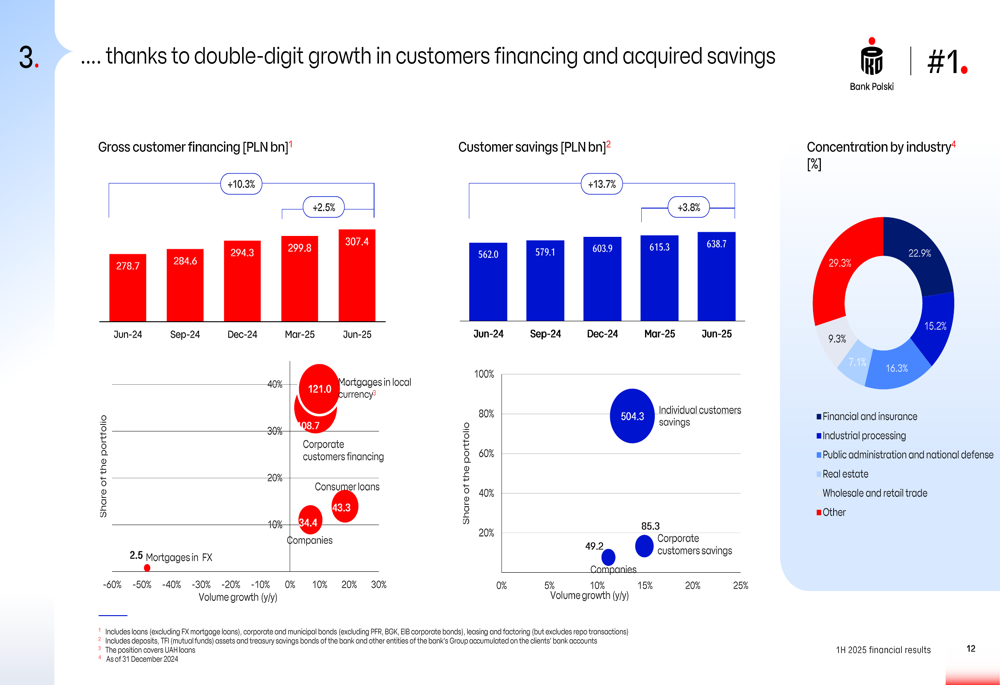

Customer financing showed impressive growth across all segments, with gross customer financing increasing by 10.3% year-over-year. Mortgage loans in local currency grew by 2.5%, corporate financing by 15.2%, and consumer loans by 23.3%. Customer savings also showed strong growth, up 13.7% year-over-year.

The following slide illustrates the growth in customer financing and savings:

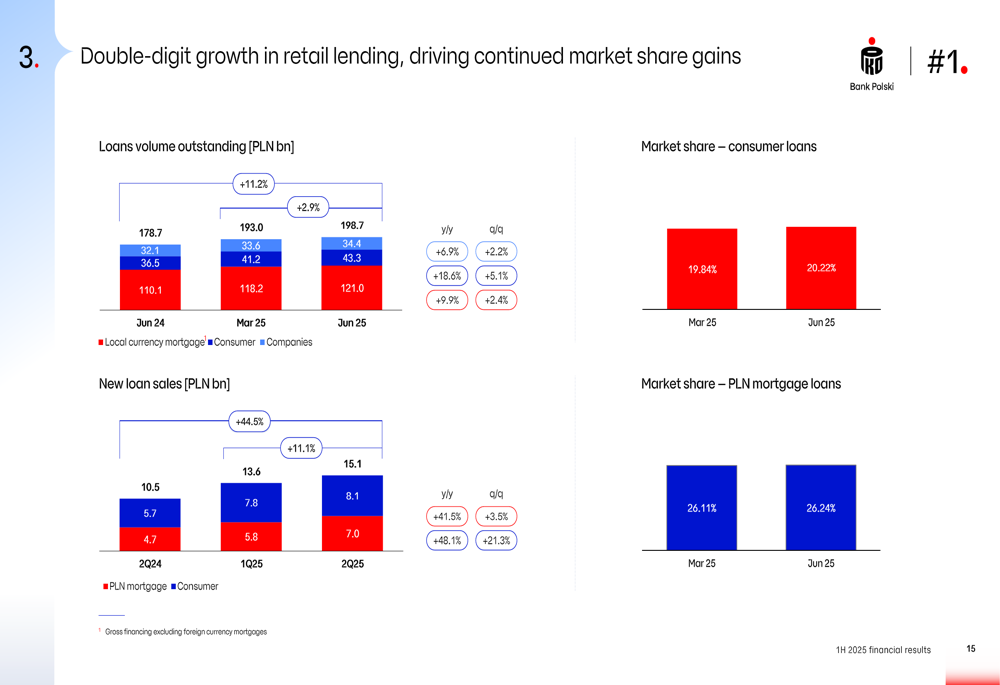

Retail lending demonstrated particularly strong performance, with double-digit growth in both consumer and mortgage loans. Consumer loans increased by 11.2% to 198.7 billion PLN, while mortgage loans grew by 18.6% to 43.3 billion PLN. New loan sales also showed significant growth, with mortgage loans up 48.9% and consumer loans up 36.8%.

The retail lending growth is illustrated in the following chart:

Corporate financing grew by 8.7% year-over-year to 108.7 billion PLN, while corporate customer savings increased by 14.9% to 85.3 billion PLN. The bank maintained its leadership position in major transactions, participating in 11 significant deals during the quarter.

The bank’s cost efficiency remained high, with a reported cost-to-income ratio of 31.0%. Operating expenses increased by 14.1% year-over-year in the first half, and by 12.4% in Q2. The cost-to-income ratio for H1 reflected the seasonally high Bank Guarantee Fund (BGF) costs in Q1.

Asset quality remained strong, with the share of stage 3 receivables (non-performing loans) at 3.52%, down from the previous year. The cost of risk was stable at 33 basis points, reflecting the lack of significant pressure on asset quality.

The bank maintained a solid capital position, with a CET1 ratio of 16.29%, well above the minimum regulatory requirement of 10.55%. The bank’s stress test results showed it to be one of the most resilient banks in Europe, with the CET1 ratio projected to increase from 15.58% at the end of 2024 to 16.32% in 2027 in an adverse scenario.

Strategic Initiatives

PKO Bank Polski continued to make progress in resolving legal issues related to CHF mortgage loans, with 53,000 settlements concluded. The bank made additional legal risk provisions, but the number of pending court proceedings continued to decline.

The bank is increasingly leveraging artificial intelligence in customer service and sales, with 6.6 million conversations completed by bots in Q2 2025, up from 2.6 million in Q2 2022. The bank has also robotized 152 processes, with robots completing 27 million tasks in Q2 2025, up from 12 million in Q3 2022.

Digital banking adoption continues to grow, with the number of IKO mobile banking applications reaching 8.6 million in Q2 2025, up from 8.0 million in Q2 2024. The number of clients logging into IKO increased to 6.1 million, up from 5.6 million a year earlier.

Forward-Looking Statements

The bank expects the favorable economic environment to continue, with GDP growth projected at 3.3% in 2025 and 3.5% in 2026. Inflation is expected to remain within the target band, creating room for further interest rate cuts by the National Bank of Poland.

The banking sector outlook remains positive, with total loans expected to grow by 6.2% in 2025 and 8.6% in 2026. Mortgage loans are projected to grow by 8.3% in 2025 and 12.0% in 2026.

PKO Bank Polski is well-positioned to capitalize on these favorable conditions, with its strong capital position, high operational efficiency, and growing digital capabilities. The bank’s focus on profitable growth, as summarized in its conclusion slide, emphasizes its 5.1 billion PLN net profit, 8.7% growth in corporate financing, 13% growth in net interest income, 19.4% ROE, 31.0% cost-to-income ratio, and 33 basis points cost of risk.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.