Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

Icelandic low-cost carrier Fly Play hf (ICE:PLAY) presented its Q1 2025 results on April 29, showing continued financial challenges despite implementing a strategic pivot toward leisure travel and aircraft leasing. The airline’s stock closed at $0.66, near its 52-week low of $0.63, reflecting investor concerns about the company’s path to profitability.

PLAY transported 286,000 passengers in Q1 2025, down from 349,000 in the same period last year, while maintaining a fleet of eight aircraft serving 27 destinations. The company’s load factor declined to 77.2%, a 4.6 percentage point decrease year-over-year.

As shown in the following snapshot of PLAY’s key performance indicators for Q1 2025:

Quarterly Performance Highlights

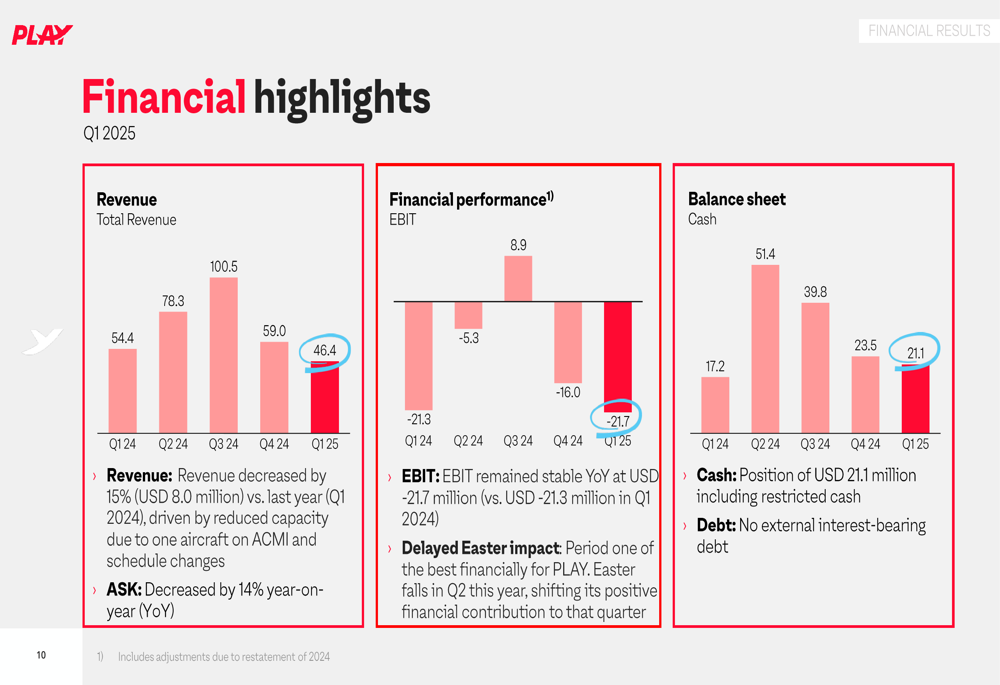

PLAY reported revenue of $46.4 million for Q1 2025, a 15% decrease compared to the same period last year. The company attributed this decline to reduced capacity, with one aircraft deployed on ACMI (Aircraft, Crew, Maintenance, and Insurance) lease and schedule changes. EBIT remained stable year-over-year at -$21.7 million, indicating persistent profitability challenges.

The following financial snapshot illustrates PLAY’s key metrics for the quarter:

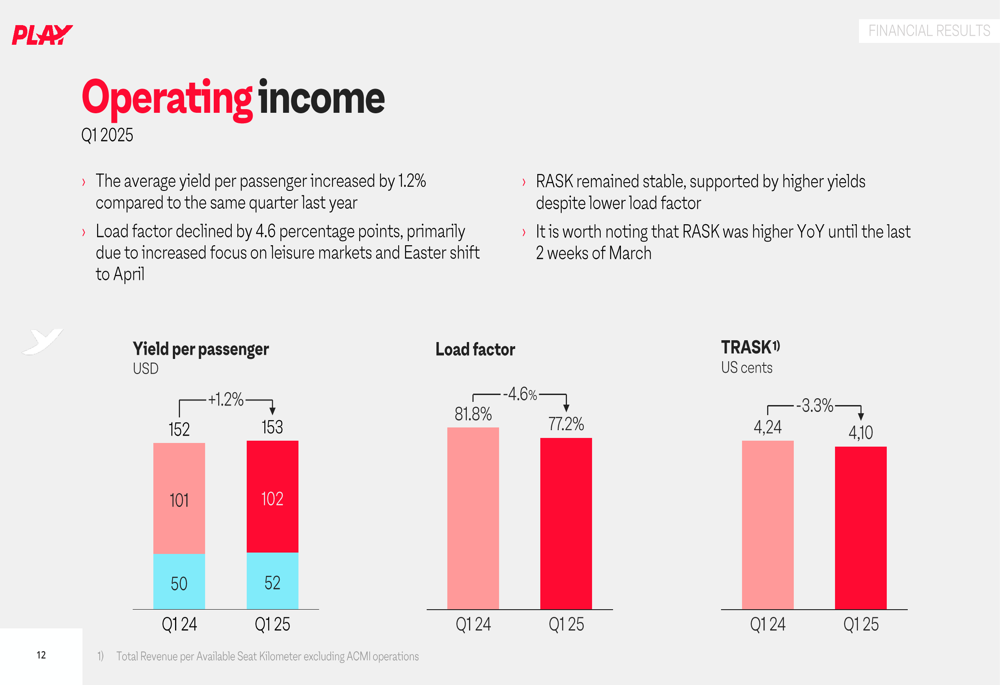

Despite the revenue decline, PLAY saw a slight improvement in yield per passenger, which increased by 1.2% compared to Q1 2024. However, this was offset by the significant drop in load factor. The company’s cash position stood at $21.1 million at quarter-end, with $12.3 million unrestricted and $8.8 million restricted.

The quarterly financial trends are illustrated in the following chart:

Operating income metrics show mixed performance, with yield improvements unable to offset load factor declines:

Strategic Initiatives

A major development in PLAY’s evolving business model was the establishment of a Maltese Air Operator Certificate (AOC) through its wholly-owned subsidiary, Play Europe. This strategic milestone, completed on March 28, 2025, enables the company to operate aircraft for other airlines outside of the PLAY brand.

As shown in the following image of the certificate acquisition:

The Maltese AOC has already facilitated a significant deal with SkyUp, with four A321neo aircraft leased to the carrier starting in Q2 2025. These aircraft will operate entirely outside of Iceland and PLAY’s route network, representing a substantial diversification of revenue streams through 2027.

Simultaneously, PLAY continues to increase its focus on leisure travel to sunny destinations in Southern Europe. Leisure capacity increased by 17% in Q1 2025 compared to the same period last year. Despite a 14% reduction in overall available seat kilometers, leisure destinations now represent 31% of PLAY’s network, up from 23% in Q1 2024.

The company also reported significant improvement in customer satisfaction, with its Net Promoter Score (NPS) increasing by 48% year-over-year:

Detailed Financial Analysis

PLAY’s total CASK (Cost per Available Seat Kilometer) rose by 2.5% in Q1 2025, with ex-fuel CASK increasing by 1.8%. The company’s balance sheet shows negative shareholders’ equity of $60.4 million, though total liabilities decreased to $423.3 million.

On a positive note, cash flow improved by $3.9 million year-over-year, with net cash from operations in Q1 2025 amounting to $0.4 million. The company has also implemented a fuel hedging strategy to manage price volatility, with coverage ranging from up to 60% for the next 1-3 months to up to 30% for 7-12 months out.

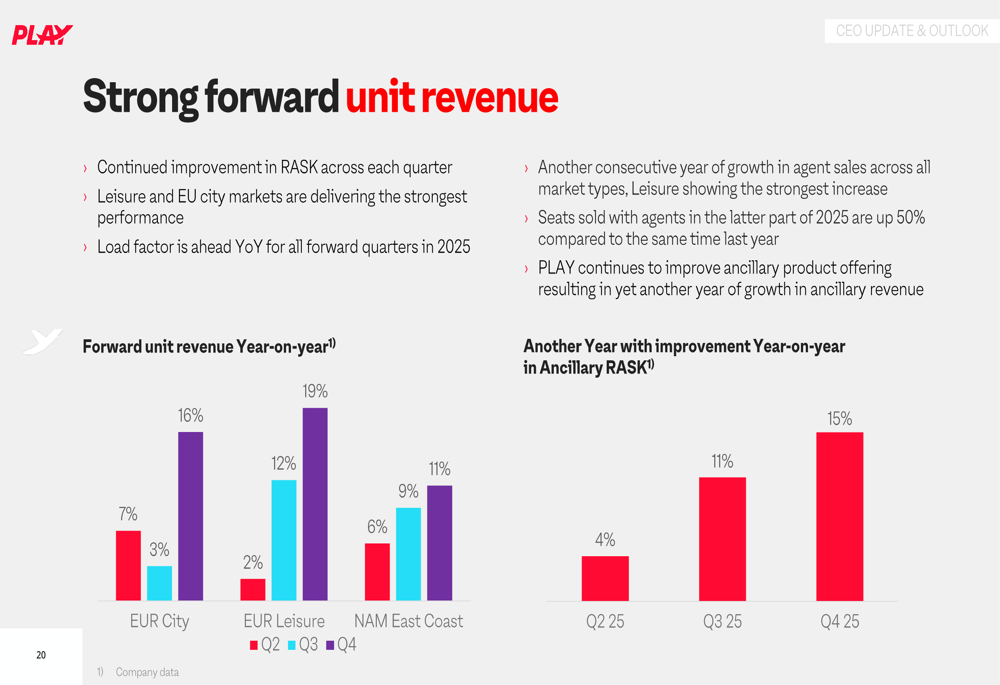

Forward unit revenue shows encouraging trends across PLAY’s markets, as illustrated in the following chart:

Forward-Looking Statements

PLAY’s management expressed confidence that all elements of its new business model are progressing as planned. The company expects to achieve a 15-20% reduction in overhead costs and projects improved financial performance in upcoming quarters.

The key components of PLAY’s strategy going forward include a 7% increase in leisure capacity in 2025, the deployment of four aircraft for SkyUp, and continued focus on profitable routes. Management emphasized that the company enters the summer season with a well-planned network and balanced fleet deployment strategy.

As summarized in the company’s key takeaways:

While PLAY highlights its stronger cash position compared to the previous year and emphasizes cost control measures, the persistent quarterly losses and negative equity position suggest significant challenges remain. The success of the company’s strategic pivot toward leisure travel and aircraft leasing will be crucial in determining whether PLAY can achieve sustainable profitability in the highly competitive airline industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.