S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Plumas Bancorp (NASDAQ:PLBC), a regional bank with $1.6 billion in assets headquartered in Reno, Nevada, recently shared its investor presentation highlighting full-year 2024 performance. The bank, which operates 15 branches across California and Nevada, demonstrated resilience in a challenging banking environment characterized by high interest rates and economic uncertainty.

The bank’s stock closed at $43.94 on June 26, 2025, up 1.64% for the day, and currently trades within its 52-week range of $33.26 to $51.33.

Executive Summary

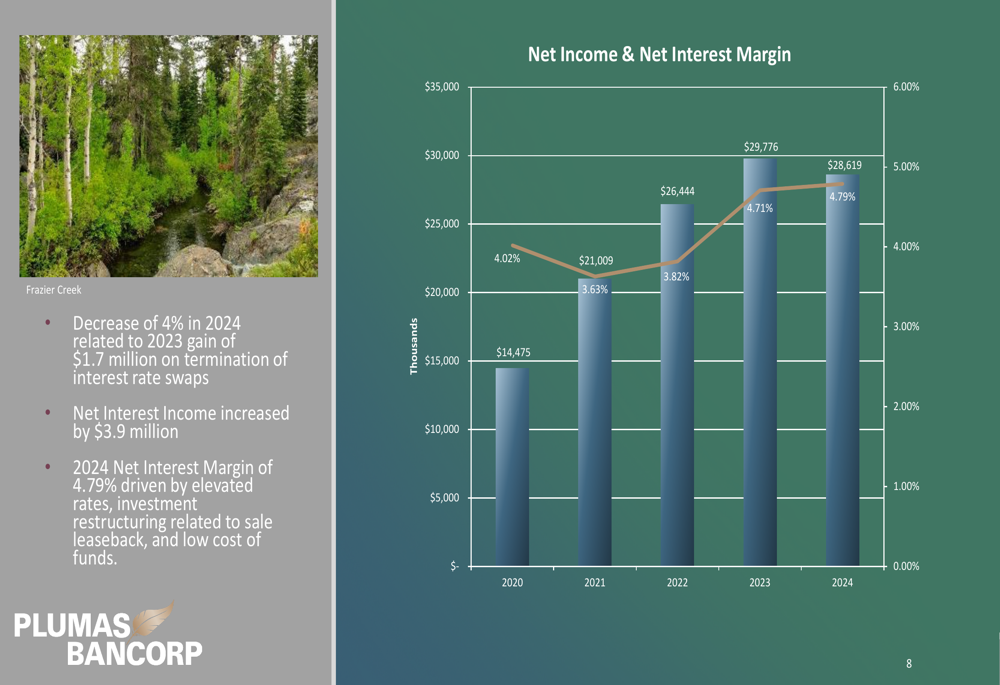

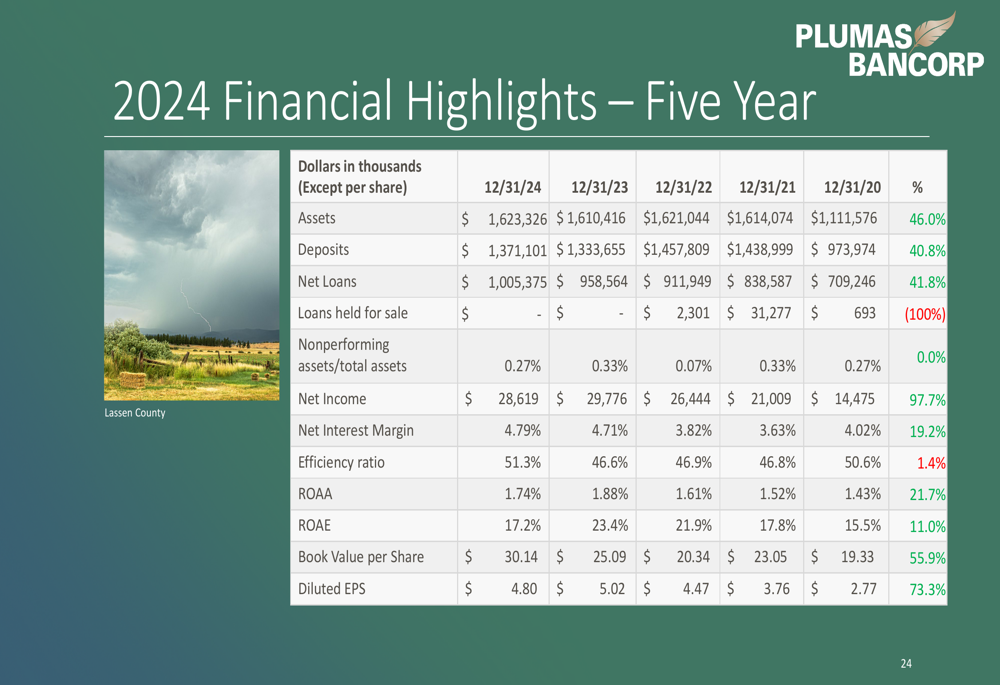

Plumas Bancorp reported net income of $28.6 million for 2024, a slight decrease of 4% from $29.8 million in 2023. However, the bank’s net interest margin improved to 4.79% from 4.71% in the prior year, demonstrating effective management of its balance sheet in the high-rate environment.

The bank’s loan portfolio grew to over $1 billion, representing a 6% increase from 2023, while deposits increased by 2.8% to $1.37 billion. Book value per share saw significant growth, rising 20.1% to $30.14.

As shown in the following chart of net income and net interest margin trends over the past five years, Plumas has maintained strong profitability metrics despite recent challenges:

Detailed Financial Analysis

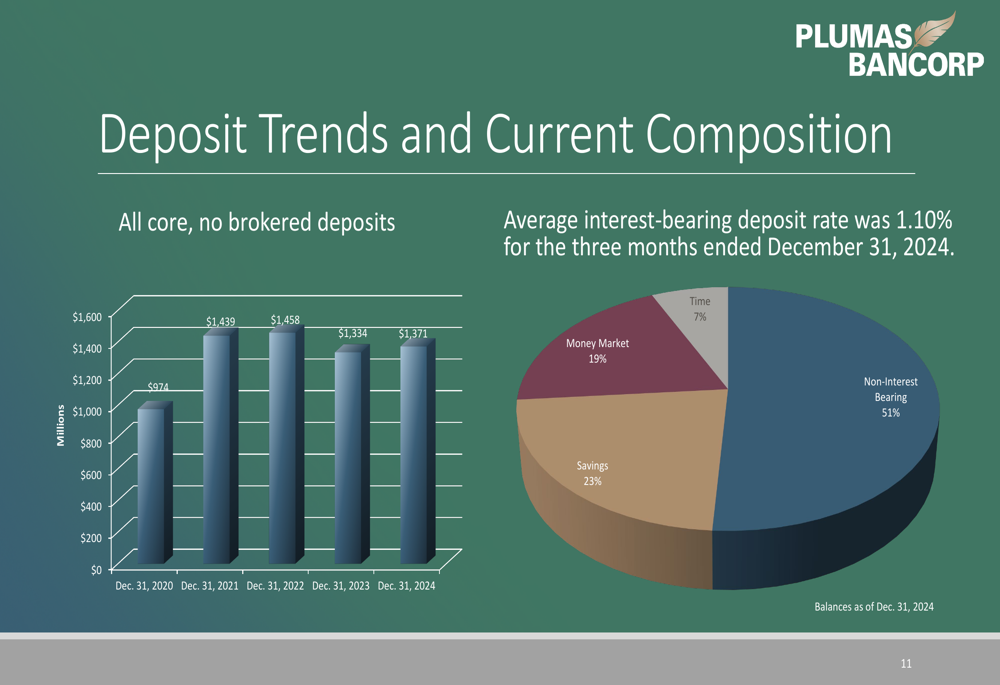

Plumas Bancorp’s deposit base remains a key strength, with 51% of deposits in non-interest bearing accounts as of December 31, 2024. This favorable deposit mix has helped the bank maintain a relatively low average interest-bearing deposit rate of 1.10% for the fourth quarter of 2024.

The composition of deposits illustrates the bank’s stable funding position:

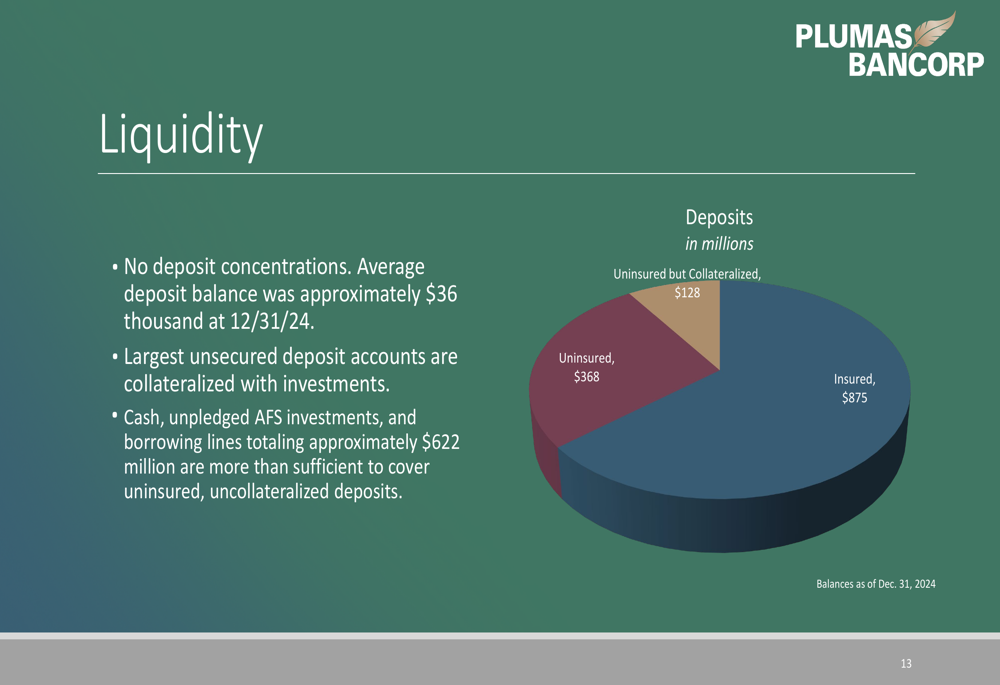

The bank’s liquidity position appears solid, with $875 million in insured deposits and $128 million in uninsured but collateralized deposits. Management noted that cash, unpledged AFS investments, and borrowing lines totaling approximately $622 million are more than sufficient to cover the $368 million in uninsured deposits.

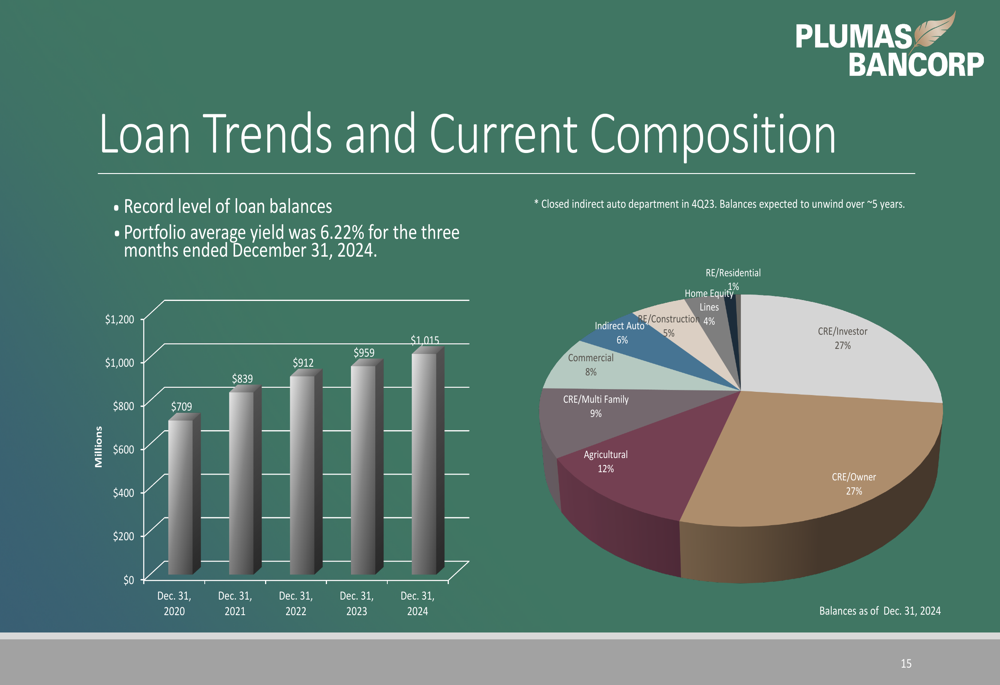

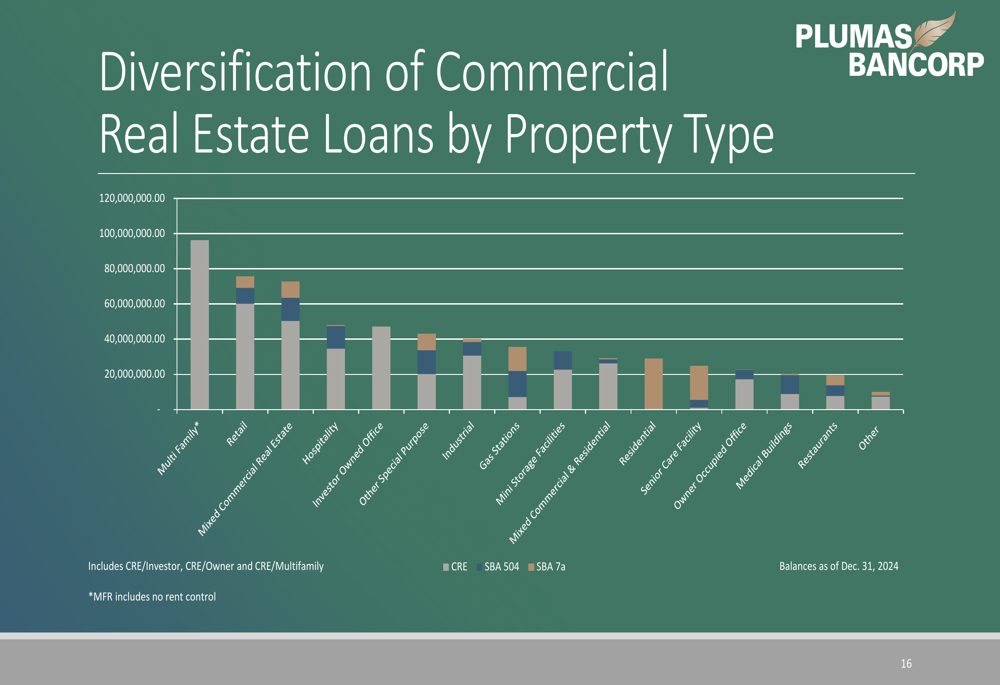

On the lending side, Plumas reported record loan balances of $1.015 billion, with a well-diversified portfolio. Commercial real estate loans make up the largest portion at 54% (split evenly between owner-occupied and investor properties), followed by agricultural loans at 12%. The loan portfolio generated a healthy average yield of 6.22% for the fourth quarter of 2024.

The following chart illustrates the bank’s loan growth and diversification:

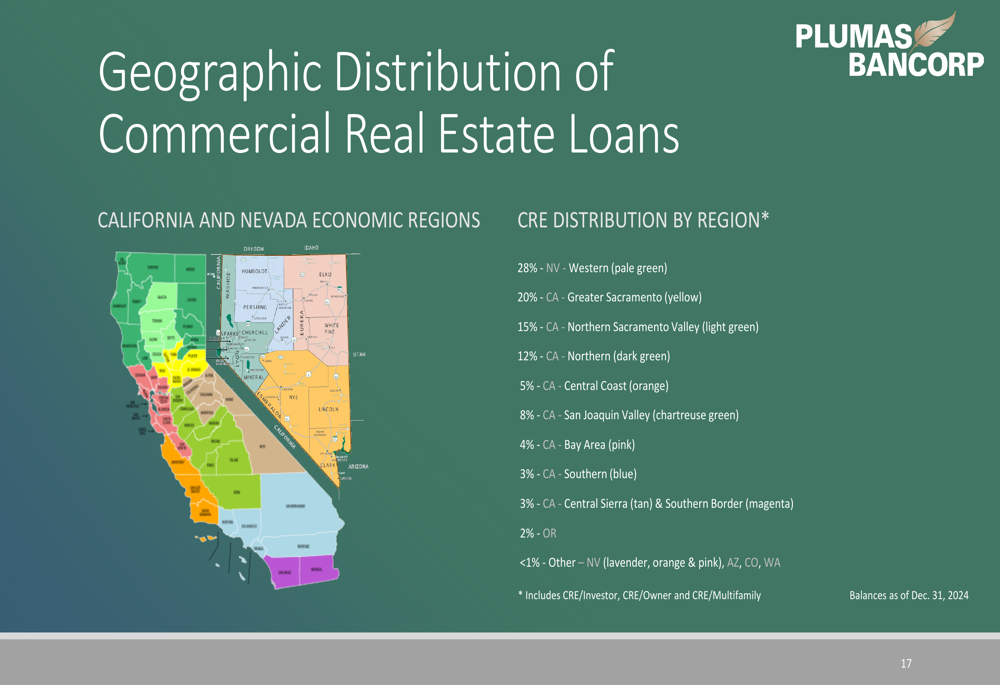

Commercial real estate loans, which represent the largest component of the bank’s portfolio, are well-diversified across property types and geographic regions:

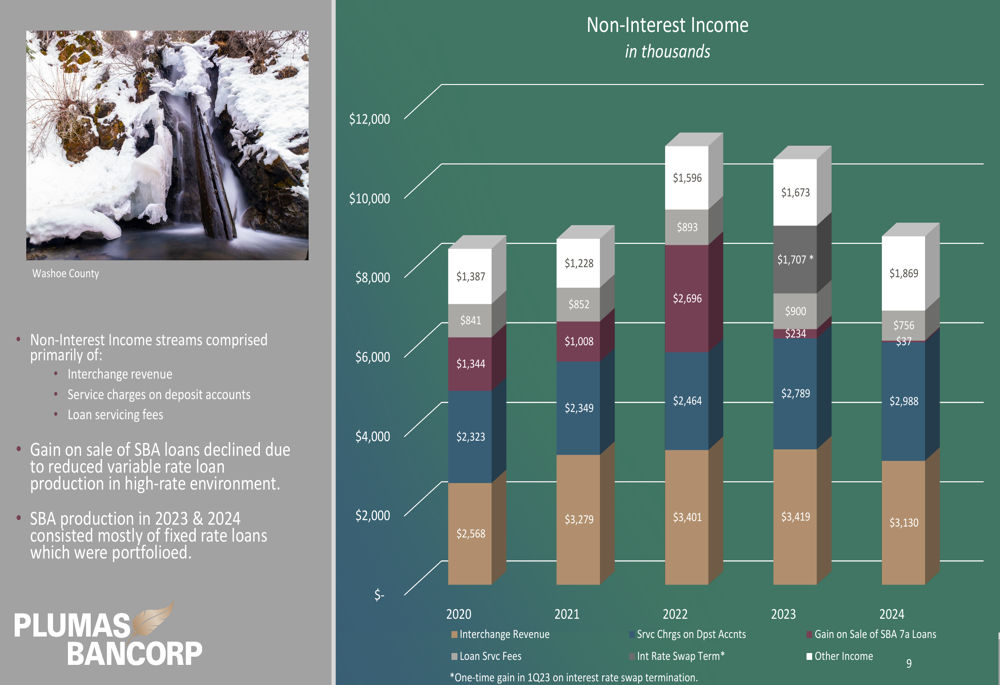

Non-interest income streams have been relatively stable, with interchange revenue, loan servicing fees, and service charges on deposit accounts being the primary contributors. However, total non-interest income decreased in 2024 compared to 2023, primarily due to a one-time $1.7 million gain on termination of interest rate swaps recorded in 2023.

The bank’s five-year financial performance shows impressive growth across key metrics:

Strategic Initiatives

Plumas Bancorp has pursued a measured expansion strategy over recent years, extending its footprint across California and Nevada. Notable recent expansions include the opening of a Chico branch in April 2023 and the acquisition of Bank of Feather River in July 2021.

The following map illustrates the bank’s expansion strategy:

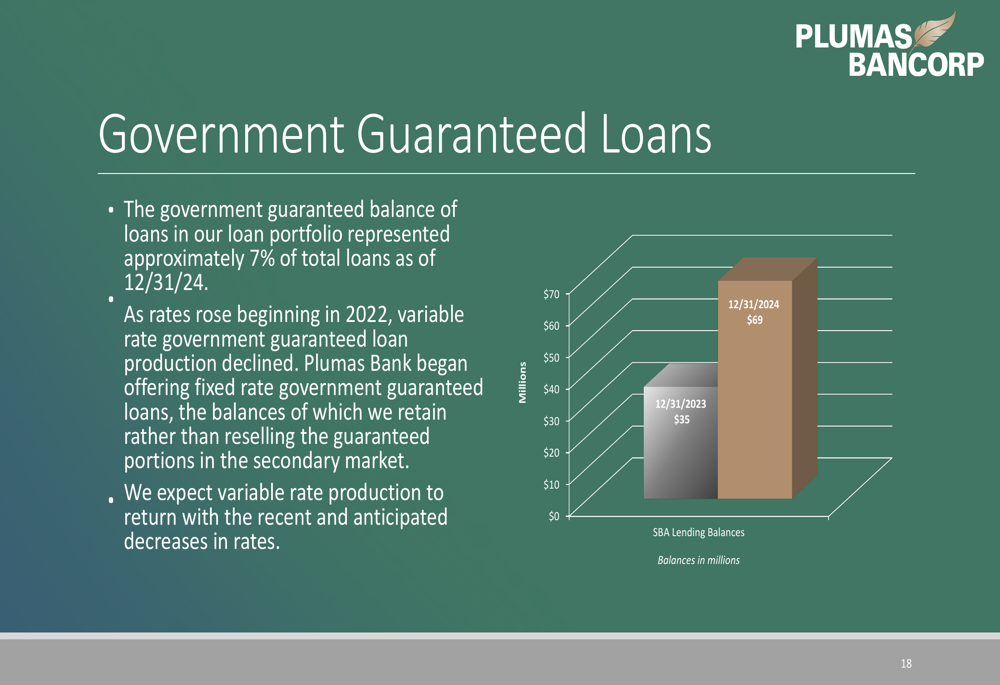

Government-guaranteed lending has become an increasingly important part of the bank’s business model, with SBA (LON:SBA) lending balances nearly doubling from $35 million in 2023 to $69 million in 2024. These loans now represent approximately 7% of the total loan portfolio.

Agricultural lending remains a significant focus for Plumas, representing 12% of total loans. The portfolio is diversified across cattle, hay, orchard crops, and rice. Management noted challenges in the walnut sector, with pricing declines in 2022 resulting in approximately $10 million in substandard loans.

Forward-Looking Statements

Management identified several strengths that position the bank for continued success, including its stable leadership team, strong core deposits, low cost of funds, and diversified loan portfolio. The bank also highlighted potential challenges, including growth opportunities in a competitive environment, leadership succession planning, and maintaining credit quality.

The bank’s asset quality metrics remain relatively strong, with non-accrual loans representing just 17% of classified assets. Total (EPA:TTEF) classified assets remain manageable relative to the bank’s capital position.

Plumas Bancorp has received numerous industry recognitions, including being named to the Bankers Cup (2017-2023), Annual Bank Honor Roll (2022-2024), and CB Top 10 (2015-2024), underscoring its consistent performance relative to peers.

With its strong deposit base, growing loan portfolio, and solid capital position, Plumas Bancorp appears well-positioned to navigate the current banking environment while pursuing strategic growth opportunities in its California and Nevada markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.