S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

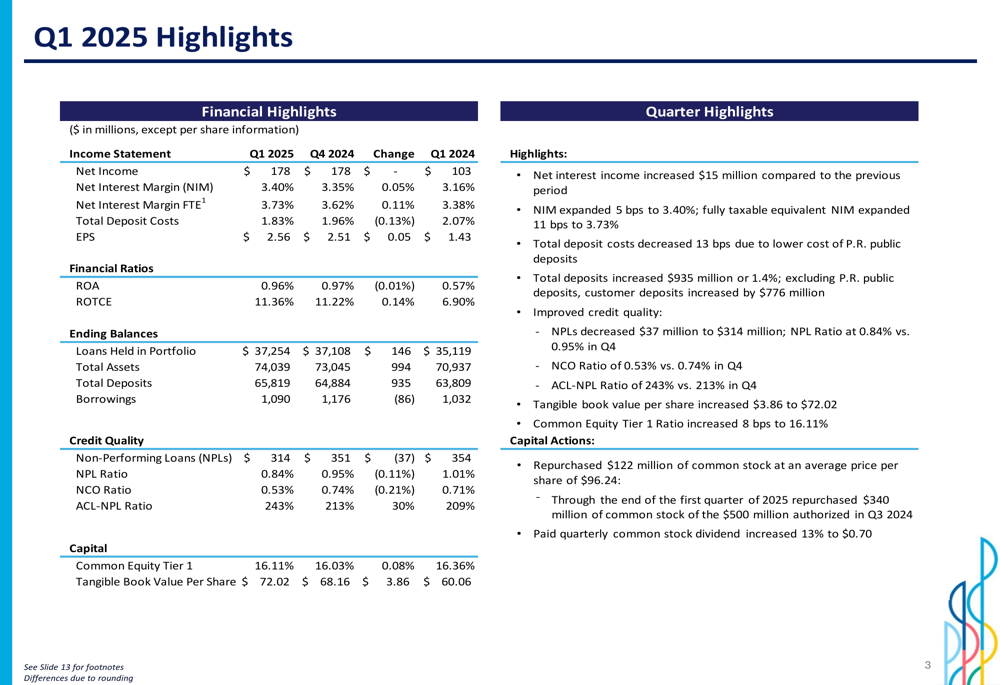

Popular, Inc. (NASDAQ:BPOP) released its first quarter 2025 investor presentation on April 23, showing steady financial performance driven by net interest margin expansion and improved credit quality metrics. The Puerto Rico-based financial institution reported net income of $178 million, unchanged from the previous quarter but significantly higher than the $103 million reported in Q1 2024, demonstrating the company’s continued stability in its core markets.

The presentation comes after Popular reported strong Q4 2024 results earlier this year, when the company beat analyst expectations with earnings per share of $2.51 compared to the forecasted $2.06. The Q1 2025 results build on this momentum, with EPS increasing to $2.56, up $0.05 from the previous quarter.

Quarterly Performance Highlights

Popular’s Q1 2025 financial results reflect the company’s solid operational execution across key metrics. Net income remained stable at $178 million compared to Q4 2024, while earnings per share increased to $2.56, up $0.05 from the previous quarter. The company’s net interest margin expanded by 5 basis points to 3.40%, while net interest margin on a fully taxable equivalent (FTE) basis increased by 11 basis points to 3.73%.

As shown in the following comprehensive overview of key financial metrics, Popular demonstrated improvements across multiple performance indicators:

Total (EPA:TTEF) assets grew by $994 million to $74.0 billion, while loans held in portfolio increased by $146 million to $37.3 billion. The company saw strong deposit growth of $935 million, bringing total deposits to $65.8 billion. This deposit growth occurred while deposit costs decreased by 13 basis points to 1.83%, highlighting Popular’s ability to attract and retain deposits in a competitive environment.

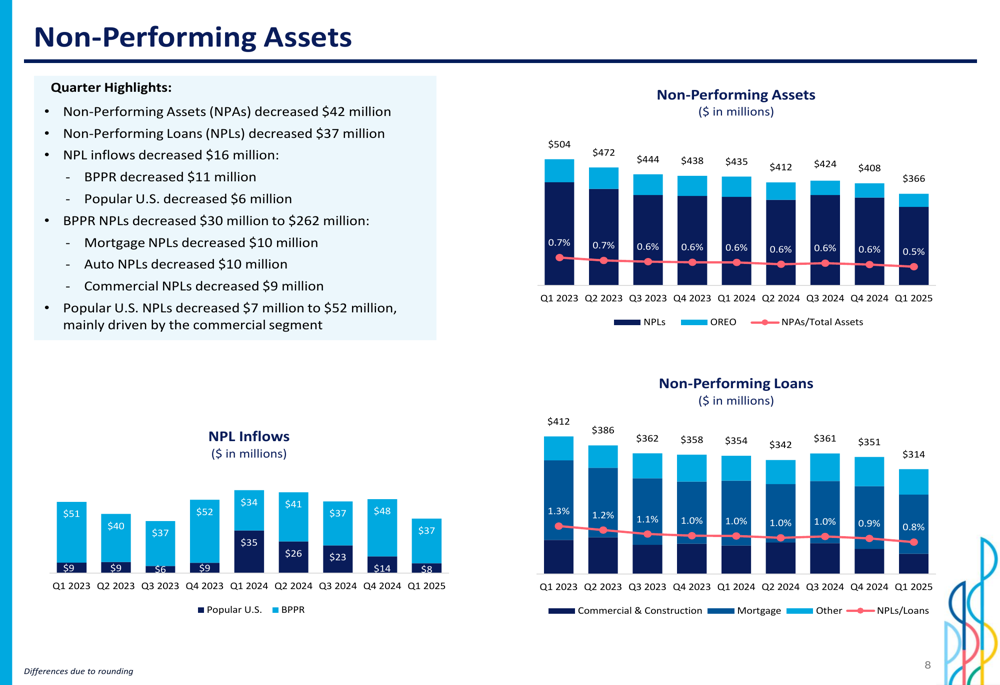

Credit quality metrics showed notable improvement, with non-performing loans decreasing by $37 million to $314 million and the NPL ratio declining by 11 basis points to 0.84%. The net charge-off ratio decreased by 21 basis points to 0.53%, reflecting the company’s prudent risk management approach.

Detailed Financial Analysis

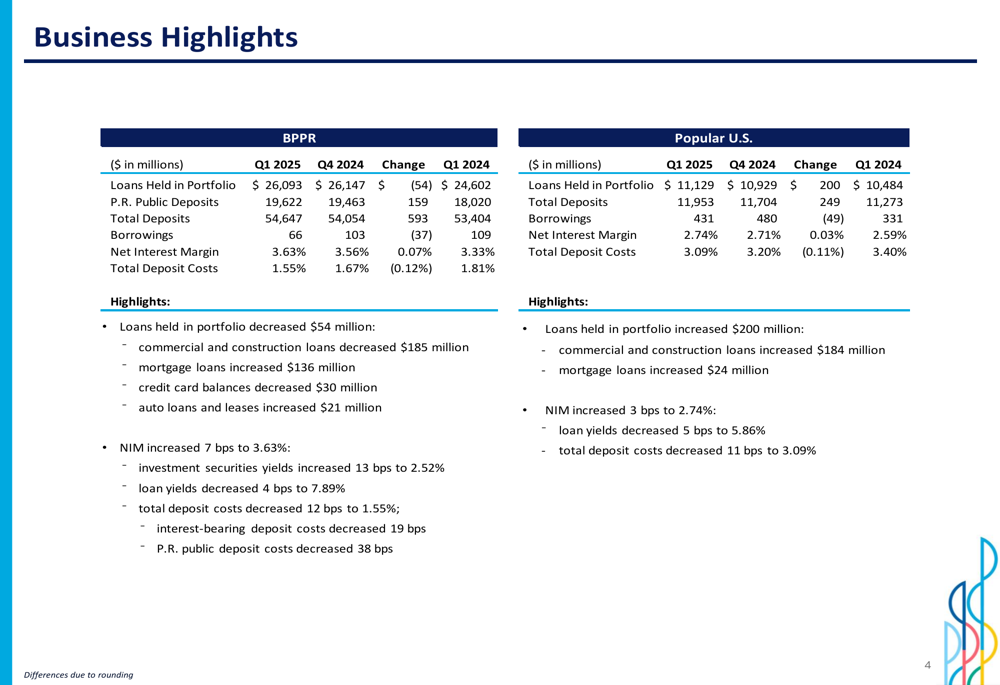

Popular’s business performance showed some divergence between its Puerto Rico (BPPR) and U.S. mainland operations. BPPR experienced a slight decrease in loans held in portfolio of $54 million, while Popular U.S. saw growth of $200 million. The following breakdown illustrates these differences:

Net interest margin expanded at both BPPR (7 basis points to 3.63%) and Popular U.S. (3 basis points to 2.74%). Total deposit costs decreased at both entities, with BPPR seeing a 12 basis point reduction to 1.55% and Popular U.S. experiencing an 11 basis point decrease to 3.09%.

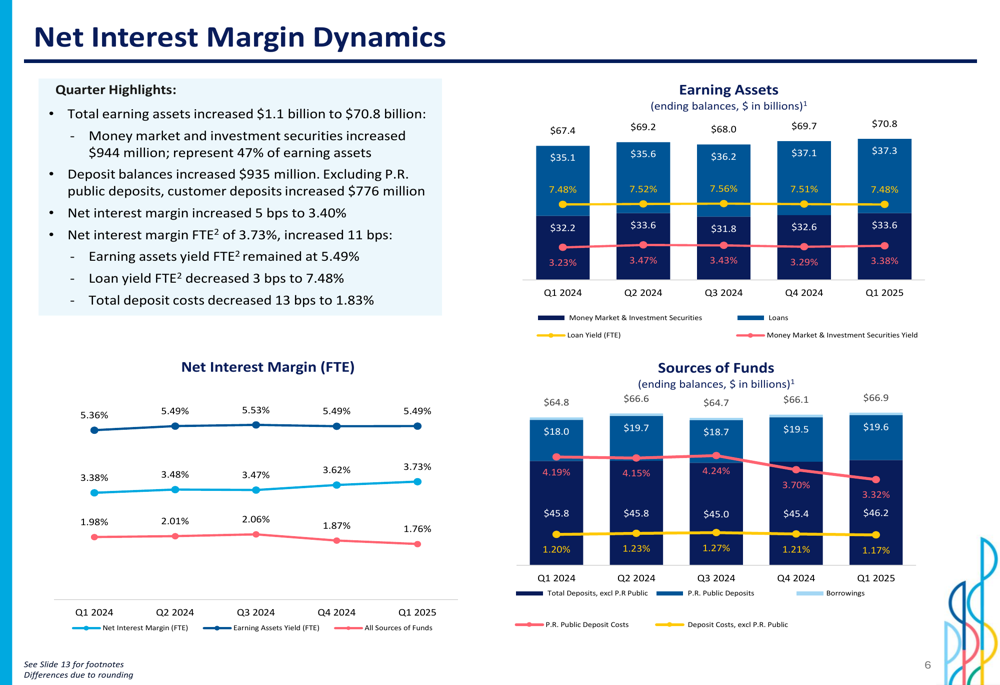

The company’s net interest margin dynamics reveal the factors driving the expansion in Q1 2025:

Total earning assets increased $1.1 billion to $70.8 billion, while deposit balances increased $935 million. The earning assets yield FTE remained at 5.49%, while loan yield FTE decreased slightly by 3 basis points to 7.48%. The decrease in total deposit costs by 13 basis points to 1.83% was a key driver of the NIM expansion.

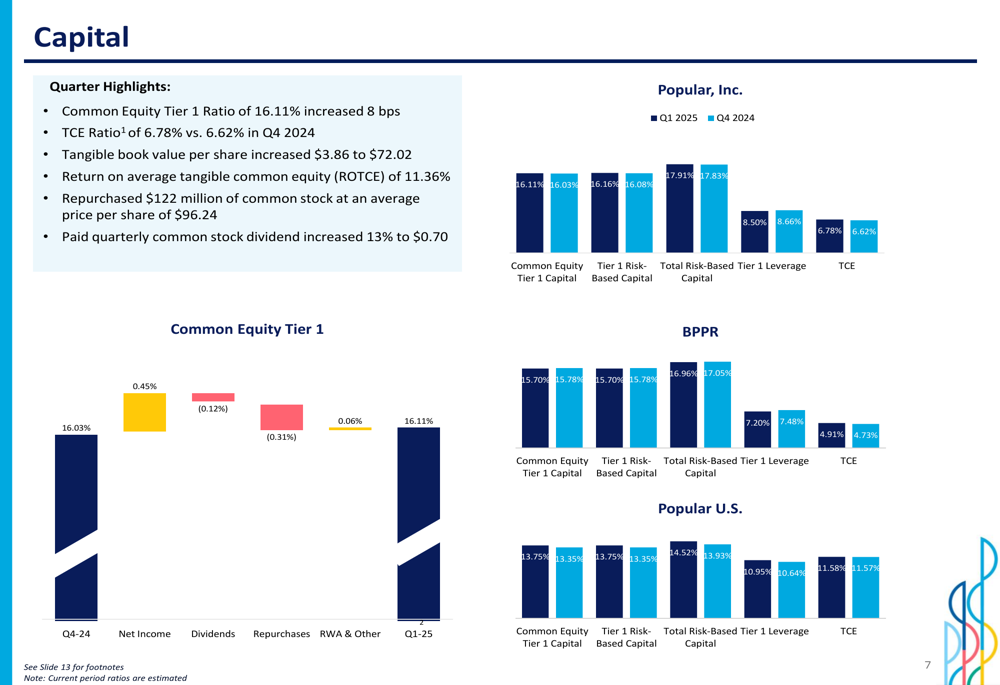

Popular maintained strong capital levels, with the Common Equity Tier 1 ratio increasing by 8 basis points to 16.11% and the tangible common equity (TCE) ratio improving to 6.78% from 6.62% in Q4 2024. Tangible book value per share increased by $3.86 to $72.02.

Credit quality continued to improve in Q1 2025, with non-performing assets decreasing by $42 million and non-performing loans declining by $37 million. NPL inflows decreased by $16 million, with BPPR NPLs decreasing by $30 million to $262 million and Popular U.S. NPLs decreasing by $7 million to $52 million.

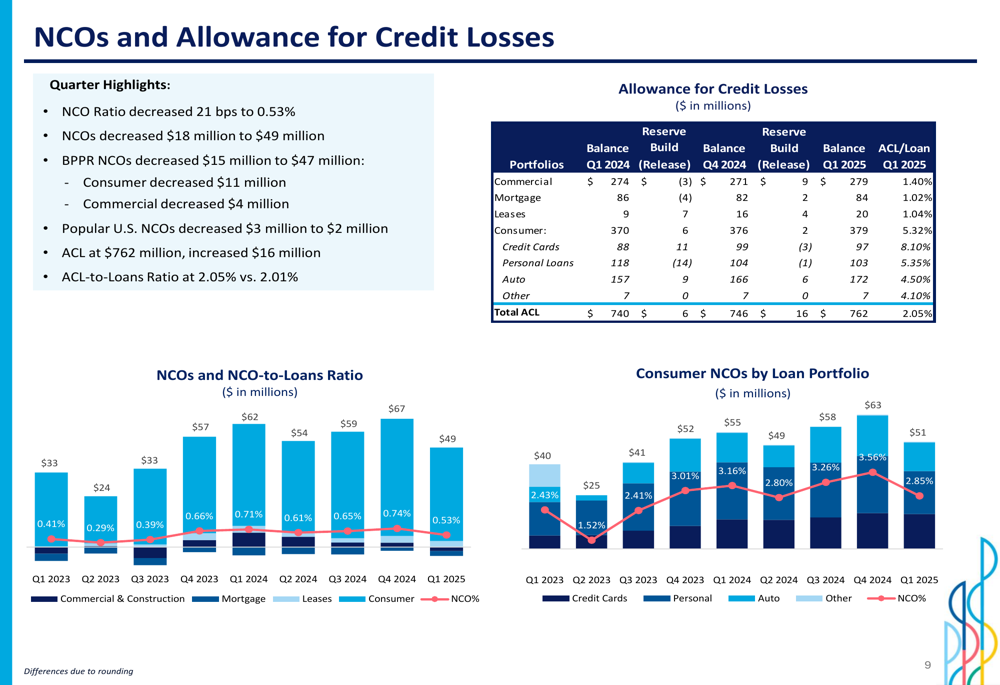

The net charge-off ratio decreased 21 basis points to 0.53%, with NCOs decreasing by $18 million to $49 million. BPPR NCOs decreased by $15 million to $47 million. The allowance for credit losses increased by $16 million to $762 million, resulting in an ACL-to-loans ratio of 2.05%, up slightly from 2.01% in the previous quarter.

Strategic Initiatives

Popular’s presentation highlighted its strategic focus on three key areas: franchise strength, transformation, and capital actions. The company emphasized its market leadership in Puerto Rico, diversified deposit base, strong risk-adjusted loan margins, and the geographic diversification provided by its mainland U.S. banking operations.

The company is pursuing an ongoing transformation effort focused on ensuring long-term success by evolving its operations, customer opportunities, and corporate culture. This transformation aims to meet the rapidly changing needs of customers, provide employees with a thriving workplace, promote progress in the communities it serves, and generate sustainable value for shareholders.

Popular continued its active capital return program, repurchasing $122 million of common stock at an average price of $96.24 per share during the quarter. The company also increased its quarterly common stock dividend by 13% to $0.70 per share, demonstrating its commitment to returning capital to shareholders.

Forward-Looking Statements

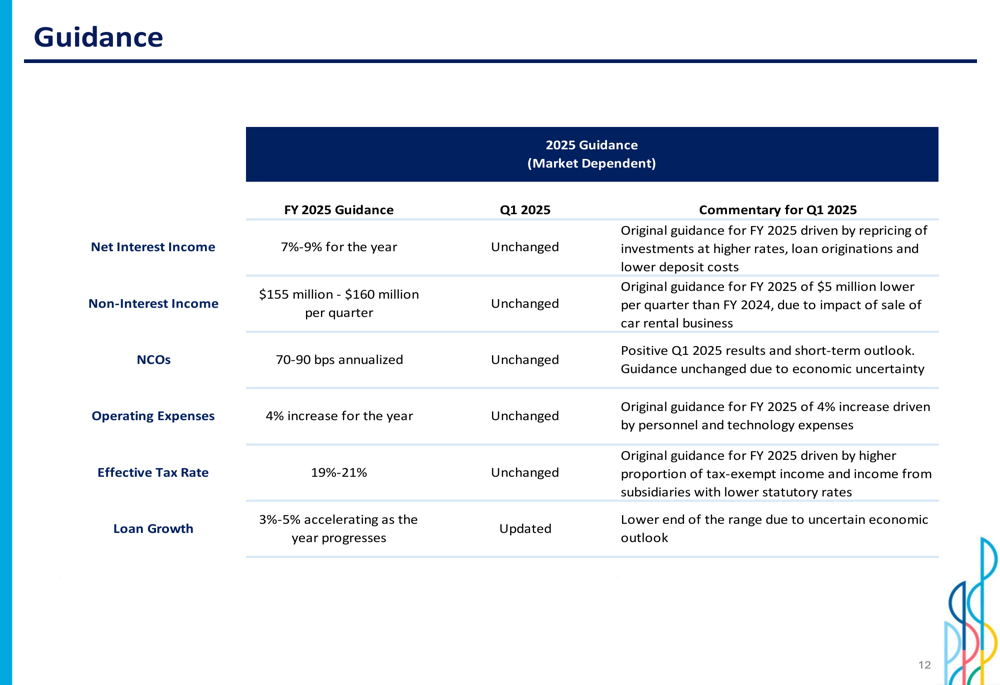

Popular maintained its guidance for 2025, projecting net interest income growth of 7%-9% for the year and non-interest income of $155-$160 million per quarter. The company expects net charge-offs to be in the range of 70-90 basis points annualized and operating expenses to increase by 4% for the year.

The effective tax rate is projected to be 19%-21%, unchanged from previous guidance. Popular updated its loan growth guidance to 3%-5%, noting that growth is expected to accelerate as the year progresses. The company attributed the guidance toward the lower end of the range to the uncertain economic outlook.

Looking ahead, Popular’s management remains focused on leveraging its strong market position in Puerto Rico while continuing to grow its U.S. mainland operations. The company’s solid capital position, improving credit metrics, and expanding net interest margin provide a strong foundation for sustainable growth and continued shareholder returns.

The company’s conservative investment portfolio, with a duration of 2.1 years, positions it well for the current interest rate environment. Popular’s limited exposure to office space (1.9% of total loan portfolio) also mitigates potential risks in the commercial real estate sector that have affected some other financial institutions.

As Popular moves through 2025, its focus on transformation initiatives, prudent risk management, and strategic capital allocation should continue to support its financial performance and competitive position in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.